while WE slept: RATES aggressively unch, RBA 'dovish hold'; IF Dec AND Jan cuts, THEN buy FF -MS (via BBG); "...the 10yr heads for 5%+ in 2025" -ING; does CRB=flation?

Good morning … a shorter / earlier note than normal and I’ll lead with an updated / quick look at 3yy in shorter-term context ahead of today’s upcoming $58bb 3yr UST auction …

… momentum remains overBOUGHT on a daily basis SO this is a more bearish than not, visual … BUT as we can see, yields are RANGEBOUND (4.20 - 3.90) … still a bit of a concession was evident yesterday and if it were to continue, well … that would likely help and attract those betting on rate CUTS … To THAT, one of the best in the biz …

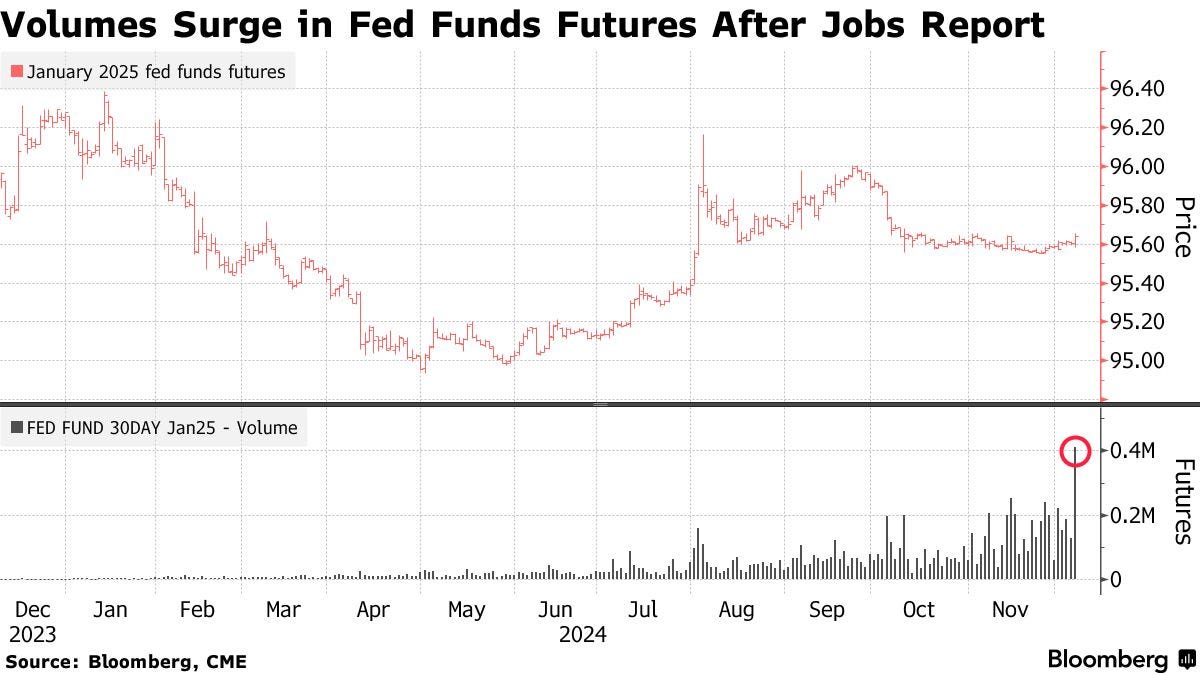

Bloomberg: Traders Rush to Join Fed Rate-Cut Bet Touted by Morgan Stanley

Open interest in fed funds futures soared in Friday’s rally

Trade recommendation assumes rate cuts in December and January

Wagers in the fed funds futures market on Federal Reserve interest-rate cuts in both December and January have ballooned in size, aided by Morgan Stanley’s endorsement.

The number of January and February contracts in which traders have positions soared Friday as their prices climbed on record volume for each. Morgan Stanley strategists in a report said they’d recommended buying the February contract.

“We think investors should position for a higher market-implied probability of a 25bp rate cut at the January 29 FOMC meeting,” strategists led by Matthew Hornbach said in a note, referring to the central bank’s rate-setting Federal Open Market Committee.

Recommended ways to do that included buying the February fed funds contract and receiving the overnight index swap rate corresponding to the January meeting, they wrote.

Morgan Stanley’s economists expect the Fed to cut rates by a quarter point in both December and January, while investors still harbor doubt. The OIS market prices in about 20 basis points of easing for the Dec. 18 decision, or 80% odds of rate cut. That compares with about 64% before November jobs data released Friday ignited wagers on a rate cut this month.

January and February fed funds futures saw record trading volume Friday as buyers piled in. The 410,842 January contracts that changed hands eclipsed the 250,000-odd traded on Nov. 14, when Fed Chair Powell said the recent performance of the US economy had been “remarkably good,” giving central bankers room to lower interest rates at a careful pace.

Open interest in January the contract increased by about 7% to more than 500,000. For the February contract open interest increased by more than 3% to 318,000, also a record. Friday’s activity included a block trade of some 20,000 contracts at a price of 95.715.

Morgan Stanley’s recommendation was to buy at 95.71 or receive the OIS rate at 4.300%.

Potential catalysts this week for the market to more fully price in Fed rate cuts in December and January include November consumer and producer price index reports on Wednesday and Thursday.

… NOTED and moving right along … ahead of today’s upcoming $58bb 3yr UST auction, a look at USTs from someone with A Terminal …

CHARTbeat: Fixed Income: Treasuries Weekly rotation of debt-based charts

… AND in as far as the day that WAS …

ZH: Momo Massacred: Bullion & Black Gold Bid As Stocks, Bonds, & Crypto Tank

… onward and upward TO the day that will be … here is a snapshot OF USTs as of 541a:

… and for some MORE of the news you might be able to use…

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ … a quick and EARLY run through the inbox with topics ranging from 2025 as well as thoughts on China …

We expect China's exports to remain resilient, at least through Q1 25, as exporters front-load shipments. However, we are concerned about subsequent payback as tariff hikes materialize. We think the deeper contraction in imports suggests the recent domestic demand recovery is still too shallow.

November: 6.7% y/y for exports, and -3.9% y/y for imports (both in USD terms)

Bloomberg consensus (Barclays): 8.7% y/y (8.5%) for exports, and 0.9% y/y (0.3%) for imports

October: 12.7% y/y for exports, and -2.3% y/y for imports (both in USD terms)

BNP China equities: Proactive policy tone, awaiting fiscal follow-through

KEY MESSAGES

China’s Politburo statement is pro growth in tone, but investors will want to see fiscal policy follow-through.

Policymakers’ aim to “stabilize the stock market” may suggest a preference for a “slow bull market”.

We still prefer China onshore to Hong Kong-listed equities on asset reallocation flows.

Corporate governance related themes should continue to deliver alpha given ongoing capital market reforms.

ING: The US 10yr heads back to 4%, but then it’s 5%+ for 2025

Front-end yields can get lower and remain low, but will still end up at least 50bp above what we see as neutral (2yr at 3.3% is neutral). The 10yr yield is ending 2024 below neutral, but will revert to above neutral by around 50bp to 100bp as we progress through 2025 (10yr at 4% to 4.5% is neutral). The 2yr trends around 4% while the 10yr heads for 5%+ in 2025

…The noughties as a neutral reference? During the noughties (2000-09) inflation averaged 2.5% and the funds rate averaged 3%. And the 10yr?

MS: Politburo Memo Raises Stimulus Expectations - Our Take

The Politburo's pledge to boost demand, and stabilise property and stock markets is set to push the market higher in the near term. However, longer-term this will hinge on a follow through of policy actions.

UBS: The CEO Macro Briefing Book 12 questions ahead of 2025

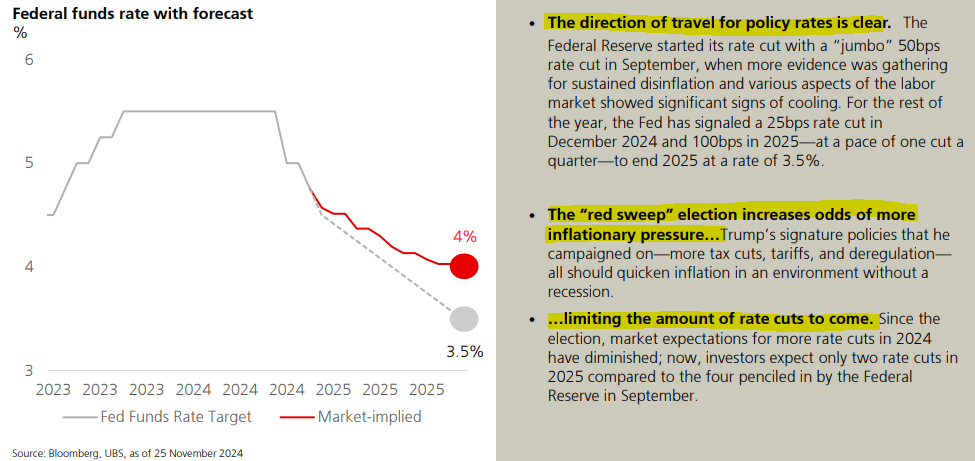

…3. How many rate cuts to expect next year? Expect 100bps of rate cuts in 2025

…11. What to expect from major asset classes in 2025? Expect higher stocks, lower yields, and a weaker USD

…Rates. The yield on the benchmark US 10-year Treasury has spent 2024 mostly above 4%, with a recent surge in the weeks leading up to the election. We believe yields are likely to fall in the year ahead since the Federal Reserve is on track to cut shortterm rates and campaign promises meet fiscal reality…

Wisdomtree: Prof. Siegel: Over-Exuberant Positioning for a December Rally

… The Treasury market reacted swiftly to the employment report, with yields initially dropping on expectations of Fed easing. The 10-year yield closed the week below 4.2% and well below its recent highs, reflecting the softness in the household survey and market confidence in moderating rates as we move into 2025. One key factor calming bond markets was the appointment of Scott Besant as Treasury Secretary, whose mainstream economic views reassured investors concerned about deficits and fiscal policy volatility.

Looking ahead, the Fed's upcoming decision looms large. I anticipate a 25-basis-point cut in December, paired with a strong signal to pause further easing—a so-called "hawkish cut." Markets are pricing in one or two additional cuts in the first half of 2025, but the Fed’s stance on the neutral rate of interest, which I believe is higher than its current estimate, will shape the trajectory and we will learn more about that in the December 18 meeting.

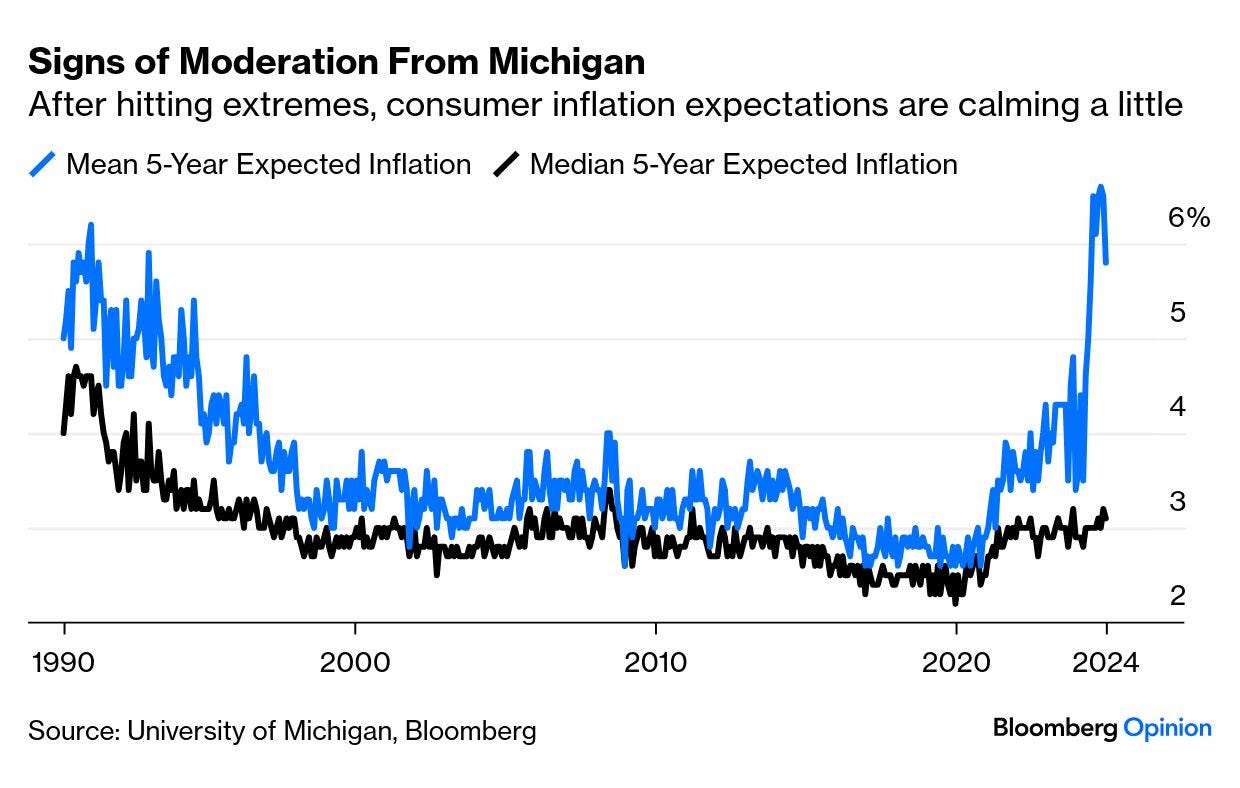

Inflation remains well-contained, though the University of Michigan’s one-year inflation expectations shot up to 2.9%, warranting close attention and possibly signaling concerns about Trump’s tariff policies…

… And from Global Wall Street inbox TO the WWW …

Bloomberg: Inflation Switcheroo Rings Out the Election Year In America, how your party is doing is how you expect the economy to perform. Republicans and Democrats are trading places

What to Expect When You’re Expecting (Inflation) We’re not quite there yet. By Friday next week, global investors are entitled to hope that they can put their feet up and take the rest of the year off from chasing macro indicators. But first we have to survive the US inflation data for November, due this Wednesday morning, and the year’s last round of central bank meetings, starting Thursday with the European Central Bank.

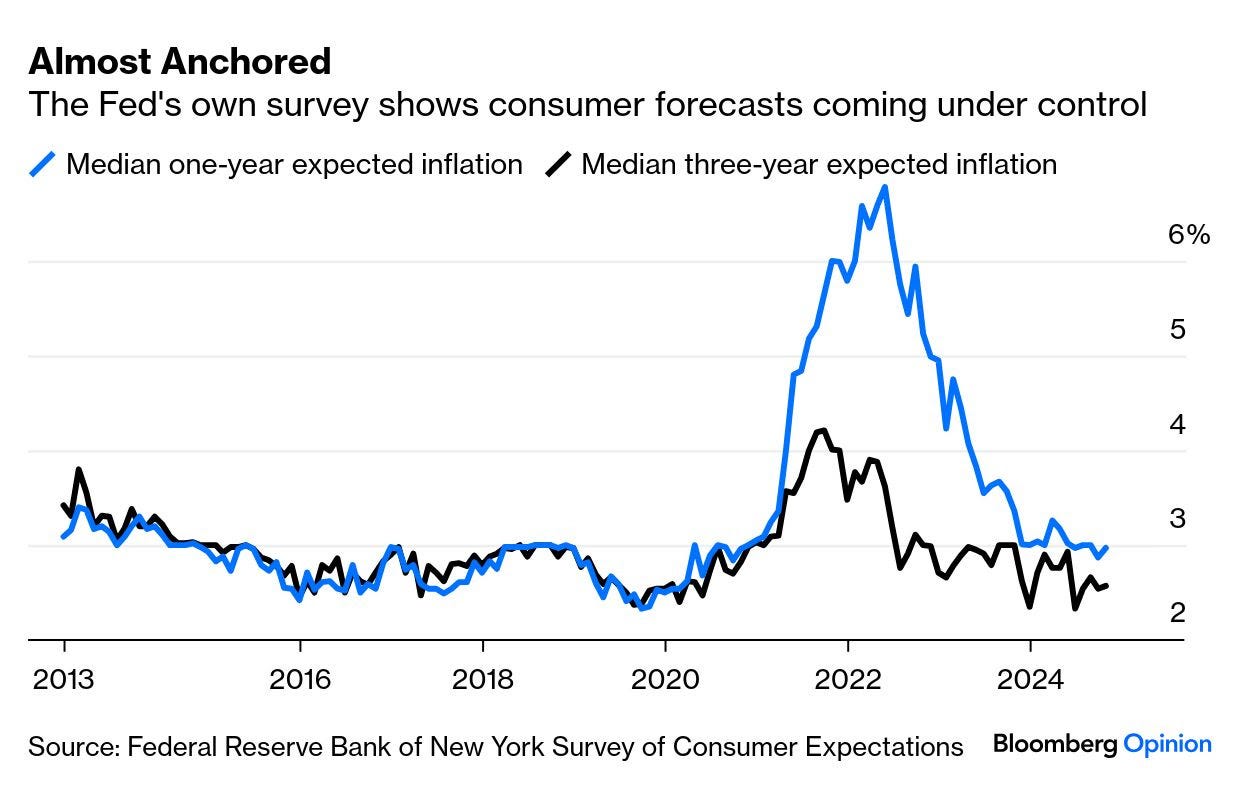

For inflation, expectations are crucial. Arguably, people’s implicit predictions of future price rises are what determine their consumption and drive inflationary outcomes. And according to the New York Fed’s own survey published Monday, consumer expectations are coming under control, although still irritatingly above the official 2% target:

The problem, as with so much else, is intense political polarization…

…Michigan publishes inflation expectation numbers on both a median and a mean basis. The mean has recently moved radically higher than the median, showing that the researchers are encountering a large group of consumers who believe that inflation will soon veer seriously out of control. The survey still shows mean expected five-year inflation close to 6% — a number that, if it happened, would virtually guarantee defeat for the Republicans four years from now — but it has begun to moderate.

As for the expectations of professional economists, Bloomberg’s survey shows they are locked in for core CPI, excluding food and energy, to be broadly unchanged at 3.3%. That’s still uncomfortable, but probably wouldn’t stop the Federal Open Market Committee from one more 25-basis-point cut next week.

My TRADE and TREND Signals are very good at sniffing out proactively predictable behaviors. These often start signaling in the Currency Market, then find their way to Equity Markets ... CRB Commodities Index (19 Commodities) was -0.2% last week to +7.3% in the last 3 months.

Unlike them, we don’t cherry pick random definitions of inflation on what “duration” fits their narrative (their latest has been to look at “3-month rolling” but they’ll stop that WHEN CPI Inflation hits a 3-month high this week).

Nope. We. Don’t. Do. That. We always measure and map everything across ALL 3 TRADE, TREND, TAIL durations.

I posted this BondBeat article on LinkedIn....see what happens ???

Scott Presler on Fox and Friends — We’re going to turn New Jersey red.

https://x.com/EricLDaugh/status/1866468908019876025