It's been a blessedly quiet start to the week in Asia with Japan taking a much-needed holiday for Mountain Day, after the Nikkei tumbled down a mountain of its own last week and sent global markets reeling…

… and with markets in CALM (before the storm) mode and ahead of CPI folks reflecting on the week that was. I reflected HERE with a few thoughts as well as many from Global Wall.

A weekly look at 10yy and with this mornings calm, an updated daily …

10yy DAILY: an almost unremarkable DAILY chart …

… middle of range with momentum ALSO middlin’ so this mornings price action, reveling in the calm, awaiting next impulse (stocks, PPI, CPI) suggests NOTHING and sometimes best course of action is to be sitting on ones hands …

… from this TO Bloomberg offering a reminder as I did of how …

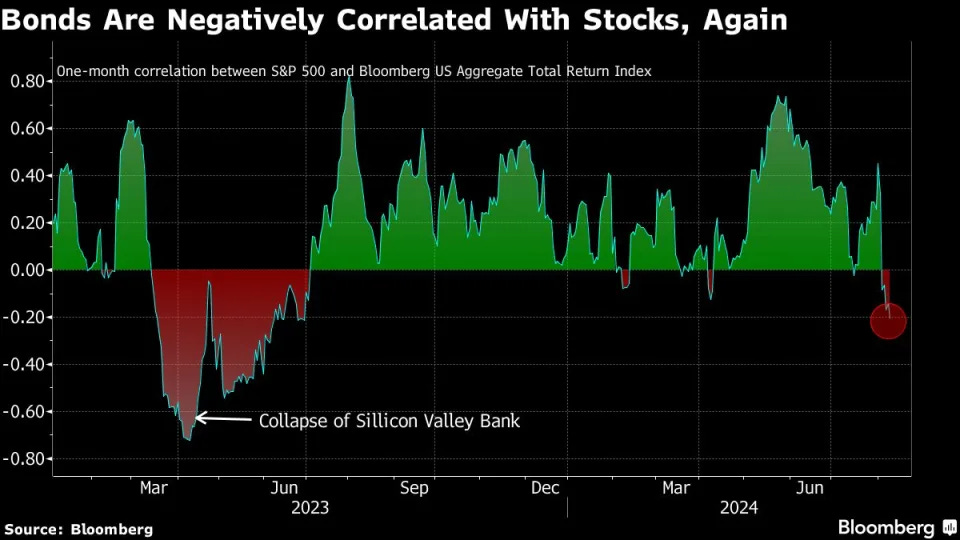

Bloomberg: Bonds Are Back as a Hedge After Failing Investors for Years

‘Finally the reason for bonds is shining through’: Abella

Inverse relationship between bonds and stocks has returned

Gregg Abella, a money manager in New Jersey, wasn’t expecting the flood of phone calls he got from clients this past week. “Suddenly people are saying to us, ‘Wow, do you think it’s a good time for us to add bonds?’”

It’s something of a vindication for Abella. He’s been, in his words, “banging the gong” for bonds — and asset diversification, more broadly — for years. This was long a decidedly out-of-favor recommendation. Until, that is, stocks started to tumble this month. Quickly, demand for the safety of debt soared, driving 10-year Treasury yields at one point early last week to the lowest levels since mid-2023…

… “Finally the reason for bonds is shining through,” said Abella, whose firm — Investment Partners Asset Management — oversees about $250 million including for wealthy Americans and nonprofits.

As the S&P 500 Index lost about 6% across the first three trading days of August, the Treasury market posted gains of almost 2%. That enabled investors with 60% of their assets in stocks and 40% in bonds — a once time-honored strategy for building a diversified portfolio with less volatility — to outperform one that merely held equities…

… BONDS are BACK, baby … (? never knew they left … ) and with that little in mind, here is a snapshot OF USTs as of 628a:

… and for some MORE of the news you might be able to use…

Reuters: China's bond market rattled as central bank squares off with bond bulls

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ in addition TO what was noted over the weekend where … Yield forecasts were revised LOWER (BAML), apparently the sky NOT falling (BARCAP), lots of attention TO the TRADE OF THE YEAR (couple years runnin’) as we’re advised to STAY in steepeners (BMO, MS) and SOME are thinkin’ ‘bout BUYIN’ PPI inspired DIP (BMO) if we get one … call it a DIPportunity … Today…

Markets reacted strongly to the BoJ and soft US payrolls; we do not see a shift in economic fundamentals. We keep our long-standing call for a 25bps cut by the Fed in September.

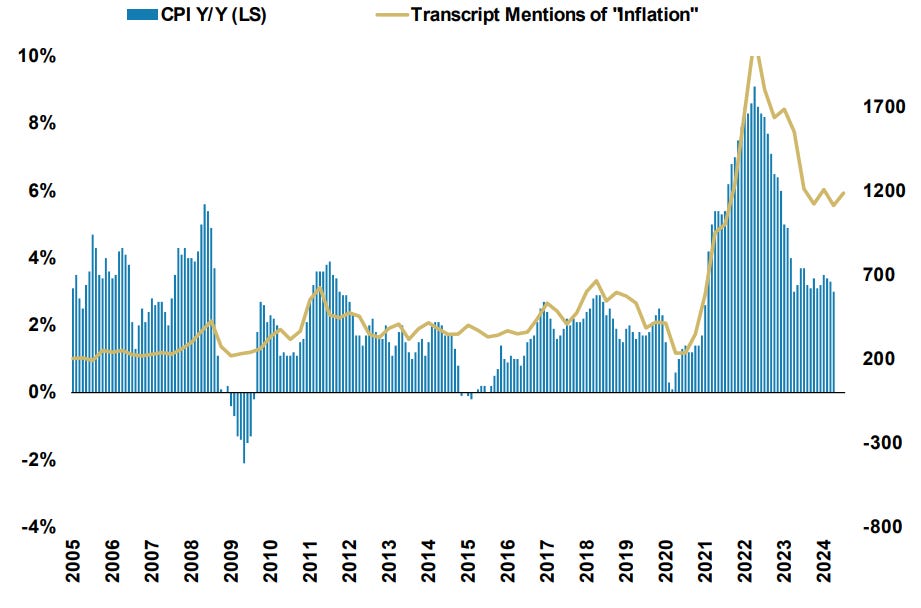

At the risk of tempting fate, financial markets seem to have got the past week’s hysteria out of their systems and are prepared to go back to looking to economists for guidance. Unfortunately, there is relatively little economic news today—although inflation data is likely to be significant this week.

The US and the UK both release consumer price inflation figures on Wednesday. The US data will overstate the inflation experience of middle-income consumers because of the fantasy of OER. Middle-income consumers’ better spending power is a reason to be wary of too much pessimism on the economic outlook.

US Vice-President Harris has said she would not interfere in the independence of monetary policy— a response to contrary suggestions from former US President Trump. Markets have not priced in any threat to US central bank independence, seeming to regard this as campaign rhetoric rather than a serious risk.

The New York Fed survey of inflation expectations is due and should not be taken seriously. Registered Republicans will declare inflation is mimicking that of Weimar Germany. Registered Democrats will deny inflation exists. Frequency bias and loss aversion will distort the data. Inflation expectations only matter if consumers change behavior in consequence (which they are not doing).

… And from Global Wall Street inbox TO the WWW,

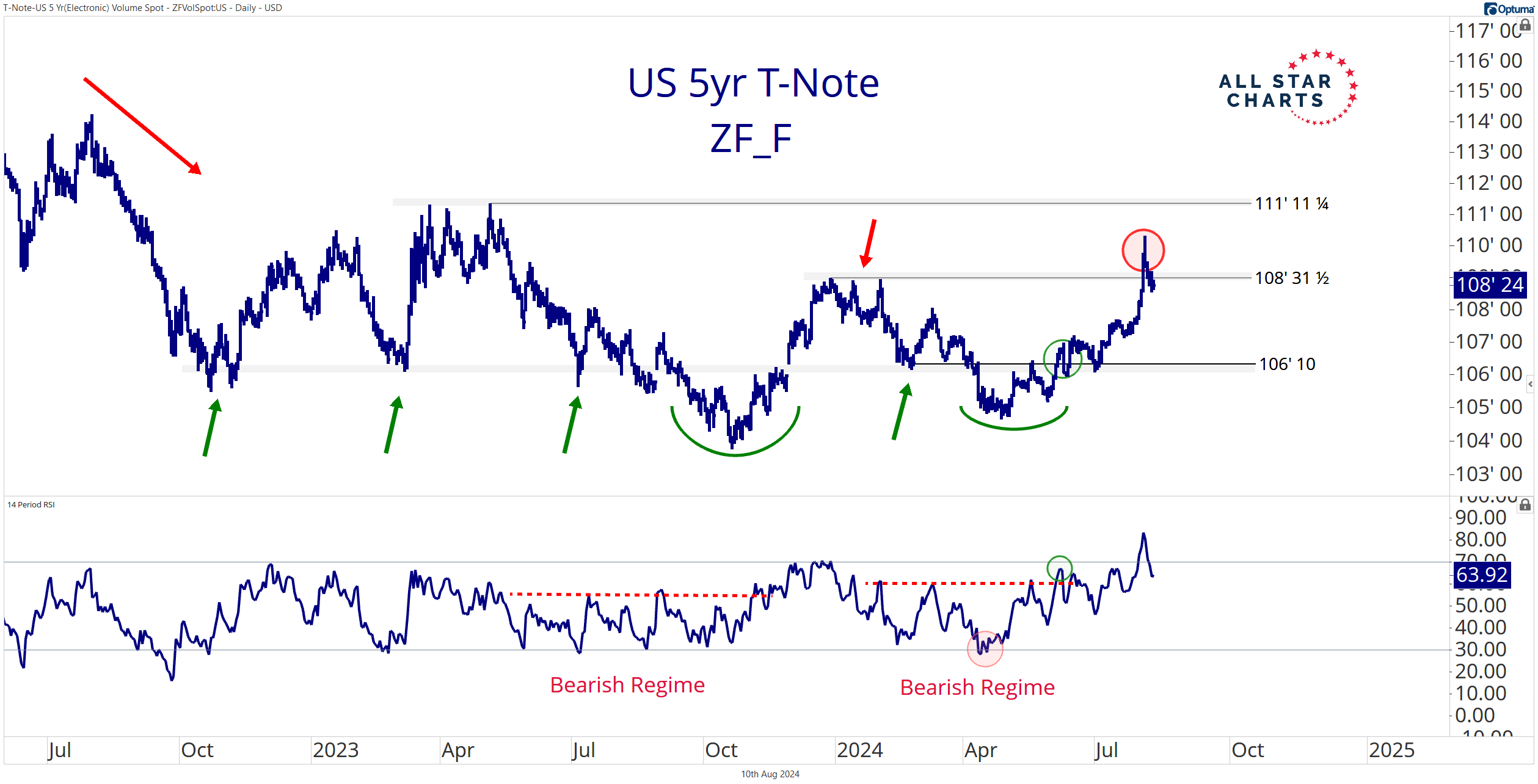

AllStarCharts: The Dust Has Settled. What’s Next for Bonds? (victory lappin’)

…Credit Spreads Had it Right

… Structural Trend Reversal Lacks Confirmation

Bonds might be back, but a shift in the structural downtrend is up in the air.

I noted that the T-bond ETF $TLT showed early signs of a bullish reversal at the beginning of the month (a trendline break and rising long-term moving average):

TLT continues to hold above a multi-year downtrend line and an upward-sloping 200-day moving average, but momentum has yet to confirm a bullish reversal.

The 14-week RSI must break free from a bearish momentum regime before we can add conviction to the long bond trade over extended time frames.

If we zoom out, 30-year T-bond futures are still trading within a structural downtrend:

A four-year downtrend line remains intact despite the most significant one-week rate of change since March 2020.

The recent initiation thrust may lead US Treasuries to a sustained rally. But structural trend reversals take time, especially following historic selloffs.

Meanwhile, bond bulls contend with selling pressure at logical resistance levels…

US Treasuries Hit Our Initial Targets

No matter where you look across the curve, overhead supply looms large.

The 30-year T-bond is finding resistance at its December 2023 peak:

The 10-year T-note is slipping below a shelf of former highs after hitting our initial target:

The 5-year T-note is turning lower at a logical supply zone following fresh 52-week highs:

And the 2-year T-note is running into stiff selling pressure at a critical polarity zone marked by the June 2022 pivot lows and last year’s highs:

When a US government bond auction is announced, a new when-issued bond starts trading, which allows the market to trade the new Treasury bond before the auction has completed. Such trading activity promotes price discovery and allows the market to trade the government bond before it is available for sale.

When the auction is complete, the yield difference between the when-issued bond and the new bond is generally called the tail. Specifically, a one basis point tail means that the auction result was one basis point higher than where the when-issued yield was trading minutes before the auction was completed, normally at 1 p.m.

This past week, there were auctions for 10-year and 30-year Treasuries, and they both tailed three basis points, which signals that demand for Treasuries was significantly weaker than the market expected. The chart below shows tails for 10-year auctions since January 2020, and the chart shows that a three basis point tail is very significant.

The bottom line is that the trend of larger and more frequent tails since the Fed started raising interest rates in March 2022 underscores the importance of investors closely monitoring Treasury auction metrics. These metrics can provide early indications of weakening demand for Treasuries.

It is possible to track tails in Bloomberg using the tickers USN10YTL and USBD30TL.

Bloomberg: Chinese Brokers Curb Bond Trading Amid Warnings on Rally

At least four brokers reduced bond trading since last week

China bonds and futures slip amid efforts to rein in bulls

At least four Chinese brokerages have started fresh measures to cut back trading of domestic government bonds since last week, people familiar with the matter said.

The brokers are reducing the trading of sovereign notes with one of them even suspending the trading of some tenors, the people said, requesting not to be named discussing private matters. While most of the firms called it a voluntary move, one person said the change came after authorities’ guidance…