while we slept; MATH of 'historically high' inflation rate & the student loan fiasco; "Overall, quits remain near record highs."; yield curve 'analysis' (circa 2005)

Good morning … China official manufacturing PMI contracted for a second month, coming in at 49.4, slightly higher than the forecast of 49.2 …

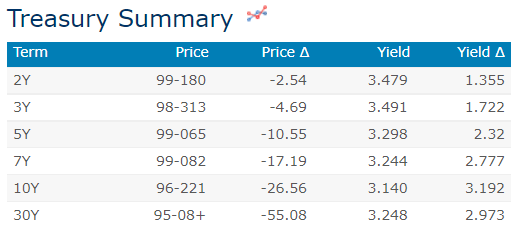

… here is a snapshot OF USTs as of 712a:

… HEREis what another shop says be behind the price action overnight,

… WHILE YOU SLEPT Treasuries have moved lower with the curve little changed as UK Gilts continue to lead G-3 bond prices into the gutter. ADP employment will return after a re-vamp for the first time since May and we discuss the changes below. DXY is higher (+0.25%) while front WTI futures have extended recent losses this morning (-3%). Asian stocks were mixed, EU and UK share markets are all modestly lower while ES futures are showing +0.25% here at 6:45am. Our overnight US rates flows saw a quiet Asian session pock-marked by some TY and FV block buys. We saw 2-way flows in 10's from real$ while fast$ added front-end flatteners. It was the same low-volume, choppy trade in London's AM hours with all eyes on Germany's record CPI print. We saw 'decent' demand in the front end this morning while the desk added that with curves so flat again, foreign real$ demand has evaporated (US real$ WAS an active buyer in the long-end yesterday, as below). Overnight Treasury volume still showed ~125% of average volume so the guess would be a lot of the flow was screen/algo based overnight?

… Our last picture this morning is an updated look at the US-German 10yr rate differential. The spread is now back to a range support level that has loosely supported this spread since early 2021. We'd spot range support near 155bp, as illustrated, and note in the lower panel that medium-term momentum is flipping down again.

… and for some MORE of the news you can use » IGMs Press Picks for today (31 Aug) to help weed thru the noise (some of which can be found over here at Finviz).

And having reached that part of the programming where I’ll note just a couple things from the Global Wall St. Inbox … Starting with what seems to be a bit of common sense from a large German bank, from the ‘MATH’ department

The 4.8% drop in energy prices in July resulted in the first monthly decline in headline PCE (-0.1%) since the depths of the pandemic in April 2020. Though core PCE prices increased just 0.1% in July -- the slowest monthly pace since November 2020 (0.0%) – some of the weakness was due to portfolio management (-7.8%), a sector that is likely to reverse in August. With respect to our suite of underlying inflation models, the upshot of the latest data is that our monthly median estimate remained unchanged at 3.1%, while the mean estimate ticked down 4bps to 3.3%. To be sure, both measures remain at historically high levels going back to the early 1990s.

Despite no further deterioration in underlying inflation in July, it remains far too high. Indeed, firmer monthly readings for some measures of trend inflation, such as trimmed mean, support Chair Powell’s recent assessment that it is “too soon to declare victory” on inflation. Our latest analysis supports the Chair’s call for continued “forceful” action to tame inflation pressures. With demand factors accounting for more than half of the rise in core inflation – the mirror image of the 1970s Great Inflation period -- monetary policy has a clear role to play in achieving price stability, even if that requires some economic pain (see Inflation: Stayin' alive on supply in the 70s, dancing to demand today).

Sure the price of gasoline is down but again, it’s from absurd levels. Yea, inflation is lower but, well, from UNACCEPTABLY HIGH levels. Levels that will FORCE choices to continue to be made. Consumers do NOT live in ivory towers but in the real world where a paycheck is finite.

… The index declined 3.6% from July in the first 15 days of August but is still up 8.8% from August 2021. The monthly slump was the most significant drop since April 2020.

Choices between things will have to be made. The choices of those running policy (from their ivory towers) are far more apparent in the EZ as winter approaches.

Watching Schatz, Bobls, Bunds and GILTS might become even MORE important part of ‘the game’ …

30yr US Bond Yields are likely to stay trapped within their ran

… We see support at 3.395/40%, where we would turn tactically bullish, with scope for a move to resistance at 3.05%, where we would turn tactically neutral. Next support above 3.40% is seen at 3.50%, above which we would also turn tactically neutral.

Plan your trades and trade your plans, accordingly.

Speaking of HISTORICALLY HIGH, this mornings brief by Yahoo

…The latest JOLTS data did show, however, a moderation in the amount of quitting American workers have been doing in recent months. While trend stories continue to pop up about the semi-mythical trend of "quiet quitting," data shows actual quits are leveling out.

In July, some 2.7% of the U.S. workforce quit their job, down from 2.8% in June and a record 3% seen in November and December 2021.

"The quit rate fell to a 14-month low, which should help restrain wage pressures as businesses feel less threat that current employees will depart," economists at Wells Fargo led by Sarah House wrote in a note on Tuesday, "but is unlikely to completely quell the inflationary pressures stemming from the labor market."

Overall, quits remain near record highs…

Finally, from 1stTRUST — Brian Wesbury & Co — is this one which made ME stop and think … and it’s more from the MATH department,

… The Biden Administration says the changes would cost $240 billion in the next ten years. The Committee for a Responsible Federal Budget says $440 - 600 billion. A budget model from Wharton says $1 trillion. But even that $1 trillion figure might be way too low.

he key is that, as bad as it is, the cancellation of some student debt that already exists is only a small part of the policy change. The much bigger change, and the one that the market has finally begun to absorb, is limiting future payments on debts to 5% of income, but only after the borrower’s income rises above roughly $30,000 per year. For example, if someone makes $70,000 per year, then no matter how much they borrow they’re limited to paying $2,000 per year (5% of the extra $40,000). After twenty years, any remaining debt would simply disappear.

Think about the perverse incentives!

For the vast majority of students, choosing this “incomebased repayment” system would be a no-brainer. And once they pick it, they wouldn’t care at all whether their college charges $35,000 per year (tuition, room, board, and fees), $85,000, or even $150,000. In fact, students would have an incentive to pick the priciest college with the best amenities they could find and pay for it all with federal loan money, because their repayments are capped. If you always wanted Rodney Dangerfield’s dorm room from the movie Back to School, you’re in luck!

Meanwhile, students would have the incentive to take out loans greater than what they need because they can turn the excess into cash for “living expenses.” Then they could use it to buy crypto, throw parties, or pretty much anything else. Who cares?!? The government would limit their future repayments.

And here’s what might be the worst part: colleges would have an incentive to enroll students even if they have horrible future job and earning prospects. By enrolling people no matter how poorly prepared they are, a college can charge whatever they want and get huge checks from the federal government. And the unprepared students won’t care because they really don’t have to pay it back. In effect, colleges could create massive and perfectly legal money-laundering schemes…

Emphasis MINE … I haven’t always agreed with or seen eye-to-eye with Mr. Wesbury BUT … in THIS CASE, I’m having a tough time with the Biden admin ideas generally speaking … and now this FIASCO?

Said another way,

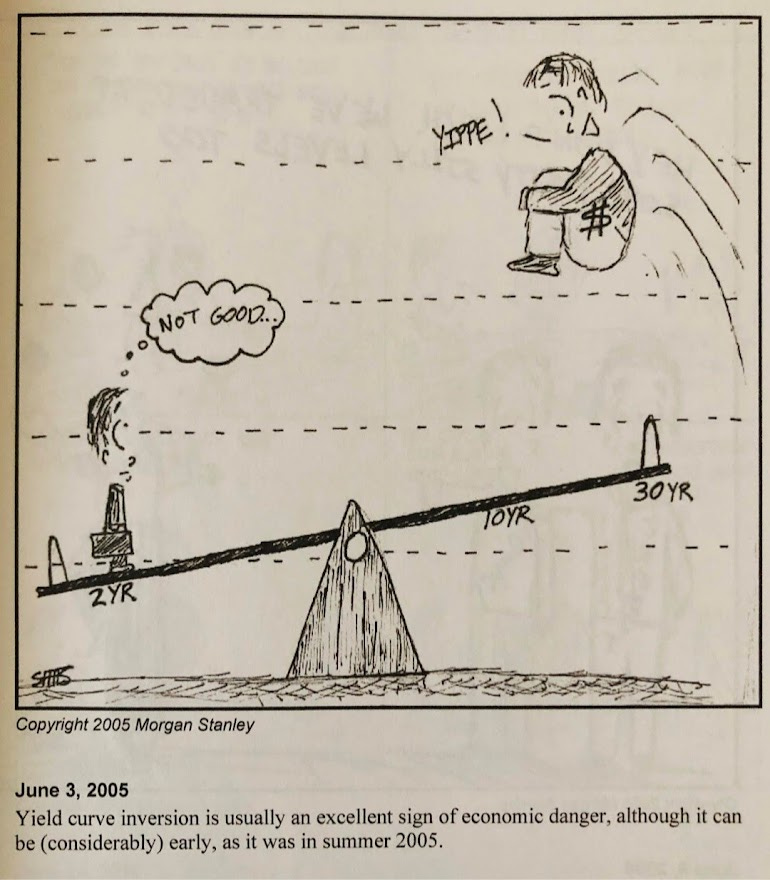

Finally, in as far as the yield curve remains a conversation, I thought a clear and concise look at my view may be overdue and in order … Unfortunately that will have to wait for another post but in the meanwhile, here’s something from MS circa 2005 and is as good a representation of what I think I think as any,

As you consider this rude and crude curve ‘analysis’, perhaps you’ll prefer ending with something a bit more cerebral. Straight from The Ivory Tower and Bernanke on 31 August 2012 on the portfolio balance channel

At the Federal Reserve Bank of Kansas City Economic Symposium, Jackson Hole, Wyoming

The point of all this is to highlight that, despite investor frustrations over the ascent in stocks amid the pandemic, the Bernanke-an Portfolio Balance Channel remains alive and quite well thank you! Simply, Fed actions … have made USTs/real yields and MBS ‘imperfect substitutes’ for other, risker asset classes- driving flows and upward trends into/in those markets, as we well know.

It is the WHAT NEXT which should concern each and every one of us, no matter WHAT asset class … THAT is all for now. I’m BACK and off to the day job…