On the heels of JPOWS late-day interview yesterday (ZH snark and link thru to transcript HERE, Powell Sees More “Pain” Ahead, Admits ‘Soft Landing’ Is ‘Out Of Fed’s Control’”. Or as another pundit put it on BBG earlier, the Fed trying to achieve a soft landing is like trying to thread a needle wearing oven mitts while blindfolded.

With THAT image in mind, I’d like to wish you a very pleasant and hopefully NOT too scary a good FRIDAY THE 13th morning!

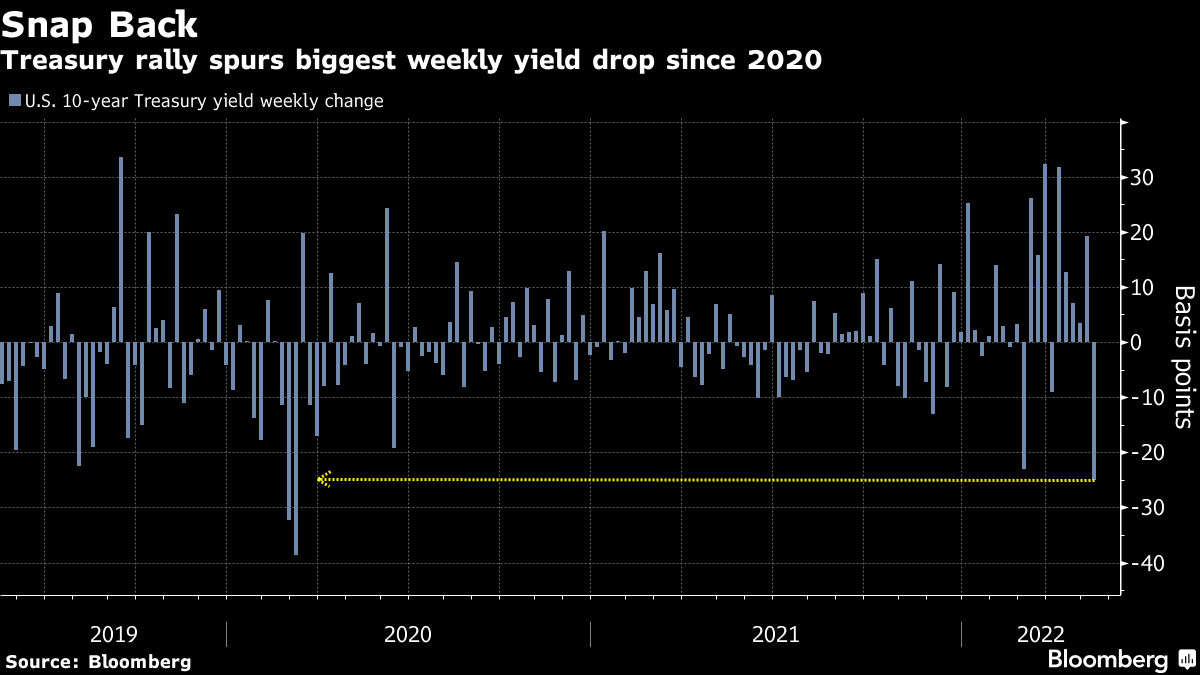

After months of a seemingly one-way trade, people finally started buying bonds. As of writing, 10-year Treasury yields are on track to drop nearly 25 basis points this week. The ‘why’ isn’t crystal clear. …

… “Short-covering likely exacerbated the rally,” said Subadra Rajappa, head of U.S. rates strategy at Societe Generale SA. “It’s been a relentless sell-off in bonds since early-March. The market seems to have gotten a little ahead of itself in pricing in for the fed funds rate to get to 3.5% by mid-2023.”

While Wednesday’s consumer-price index reading suggested that price pressures have yet to peak, perhaps inflation expectations have. After breaking above 3% in late April, 10-year breakevens have dropped to 2.63%, dragging nominal yields lower as real rates hold relatively steady.

Whatever the reason, Treasuries are finally behaving like haven assets again. But many investors are still gravitating towards the safety of cash. The $18 billion SPDR Bloomberg Barclays 1-3 Month T-Bill exchange-traded fund (ticker BIL) is on track for a sixth straight week of inflows totaling roughly $4.2 billion. Roughly $645 million poured into the ETF on Tuesday -- the second biggest one-day influx since the pandemic’s onset…

Okie dokie. As global markets and macro continue to try and adjust TO whatever it is perceived to be today’s version of the new normal, it’s good to know that on this Friday the 13th, there has been some sense of normality restored with this weeks risk OFF move accompanied BY a bond BID as with today’s move towards risk and away from bonds.

Said another way, 60/40 not dead yet

Well, supply out in The Land of the BIG 01s came and went. It was NOT a 3% coupon but it was, as ZH NOTES, a,

Solid 30y Auction Stops Through, Concludes ReFUNding Week On A High Note … Internals were also in line, with Indirects taking down 69.7%, also above last month's 65.23% and the six-auction average of 64.9%, if below March's 71.52%. And with Directs awarded a solid 16.6%, Dealers were left holding the smallest bag at just 13.7%, which is to be expected in a world where they have to wait at least a few months before the Fed's upcoming QE episode will allow them to promptly flip this paper back to the Fed.

… here is a snapshot OF USTs as of 719a:

… HEREis what another shop says be behind the price action in their morning commentary, Give Superstition its Due

… Overnight Flows Treasuries retraced into the range with 10-year yields ~5 bp higher at 2.90%. Overnight volumes were near the norms with cash trading at 97% of the 10-day moving-average. 10s were the most active issue, taking a 31% marketshare while 5s were second at 27%. 2s and 3s combined to take 29% at 19% and 10%, respectively. 7s managed 7%, 20s 2%, and 30s 4%. We have seen better buying in the long end.

Same firm points out,

… There are now two key points of support in Treasuries, this cycle’s high yield mark at 3.20% and last cycle’s peak of 3.26%. In the event of another attempt to establish a higher rate plateau, those will represent the most compelling hurdles – although we’re increasingly of the mind that 3.20% will hold for the foreseeable future. Conviction behind this stance will be tested as the market continues to build a volume bulge and 10s retest 3.0% in the week ahead. With the establishment of at least a temporary upper-bound for yields, the most relevant test will be the degree to which dip-buyers are active in another backup in yields. All else being equal, this week’s rally is sure to offer solace to market participants who have been waiting for the bottom in Treasuries to add duration exposure. Suffice it to say, there is a long and winding road on the Fed’s path of policy recalibration; as Powell commented the process will be “quite challenging” and “will include some pain.” So kinda like parallel parking?

… and for some MORE of the news you can use » IGMs Press Picks for today (13 May) to help weed thru the noise (some of which can be found over here at Finviz).

With these prices and overnight factoids in mind, here are a few words from Global Wall St sponsors (ie the sellside).

… What deviates from this pattern is the sharp spike of real rates in 2022: Since the beginning of March, 10Y reals have risen by 140bp. In fact, it is the anticipation of a continued rise of real rates that the stock market sees as particularly toxic. If we look at this relationship at higher resolution, then 2022 behavior gets another dimension. The Figure shows the last 12M of interplay between S&P (on inverted axis) and 1M-lagged 10Y real rate. It looks as if the real rates selloff is overwhelming all other considerations.

… If equity prices continue to follow this trajectory of rebellion, they are unlikely to extort the Fed’s concession as they did four years ago, and the S&P will have another leg of decline ahead of itself. Taken at face value, it’s current interaction with real rates could push stocks close to 3700 and possibly lower if reals continue to rise further.

Recent market volatility does not necessarily reflect economic reality. There is nothing in economic data or policy pronouncements that suggests the global economy will do anything wildly unexpected —but markets have been unwilling to look at the bigger picture

While in the short term markets can do their own thing, in the long term economics dictate market direction. Economists suggest inflation will slow, and the growth slowdown should not be alarming. We should be wary of relying on past correlations to forecast the future (too much structural change). The latest crypto-hyperinflation should not cause market contagion. While the media may refer to crypto bros as “investors”, they are in reality gamblers; we do not worry about equity contagion when someone loses money playing roulette at Monte Carlo. The same applies to cryptos….

… The simple equities signal has a much shorter 3 to 6 month lead time (see Figure 6), relative to growth, and is fairly consistent with the longer-term yield curve signal of a marked slowdown but no confirming early recession signal as yet.

… the Fed has to validate much of the bond market tightening. There will be no retreat from lifting the funds rate to a 2 handle at least, BUT, it is a timely reminder that the peak in the funds rate will be less determined by notions of neutral and real funds relative to past history, and more by the extent to which funds rate impacts financial conditions, and the judgment on inflation's elasticity to FCI tightening….

… The possible range on the funds terminal rate is unusually wide that will itself be a source of asset market volatility. This is also a timely reminder that the Fed is going to have to make some very tough decisions as early as H2 2022, about whether the slowing in growth is sufficient to drive inflation to near target. The Fed having badly erred on the side of excess inflation in 2020/21, cannot afford to make the same mistake twice - which favors more financial conditions tightening, and ongoing high vol panicky markets.

This ‘debate’ about whether or not REALZ matter and the Fed Put — which moves first — economies or markets — ultimately produces confusion and Global Wall Street always left to catch up (or down) to the markets, ultimately modifying prognostications.

G10 rates markets have repriced significantly due to the combination of front-loading of hikes, higher terminal rate pricing, and rebuilding bond risk premia. We have revised our yield forecasts to reflect these shifts, and now look for 10y USTs to end the year at 3.3%, 10y Bunds at 1.25%, and 10y Gilts at 2.25%.

Where we had previously characterized risks to our forecasts as being skewed to the upside, the recent tightening of financial conditions and expected growth deceleration in certain markets leaves risks somewhat more balanced (and even skewed to the downside for certain markets). With markets in many cases already pricing close to our baseline for policy rates, we expect yields can move higher, but not necessarily significantly beyond what the forwards imply.

Reduced asymmetry does not mean reduced uncertainty. While markets seem reasonably priced versus our central view, the tails of the distribution for rates over the coming years are fat. To the upside, a slower moderation in inflation could translate to more policy tightening, taking yields higher across the curve, with increased flattening pressure. On the downside, a larger slowdown in growth (and inflation) would likely warrant lower yields and steeper curves.

To be clear, the revision of UST was HIGHER, not lower BUT

… For YE22 we now expect 10y USTs at 3.3% (up from 2.7% previously) … Firming inflation risk premium should maintain upward pressure on longer-maturity yields as well (Exhibit 3), though we see risk-reward as more balanced here. Downside growth risks from the energy repercussions of the conflict in Ukraine alongside fragmentation risk could be headwinds to a material extension of the selloff at the 10y point …

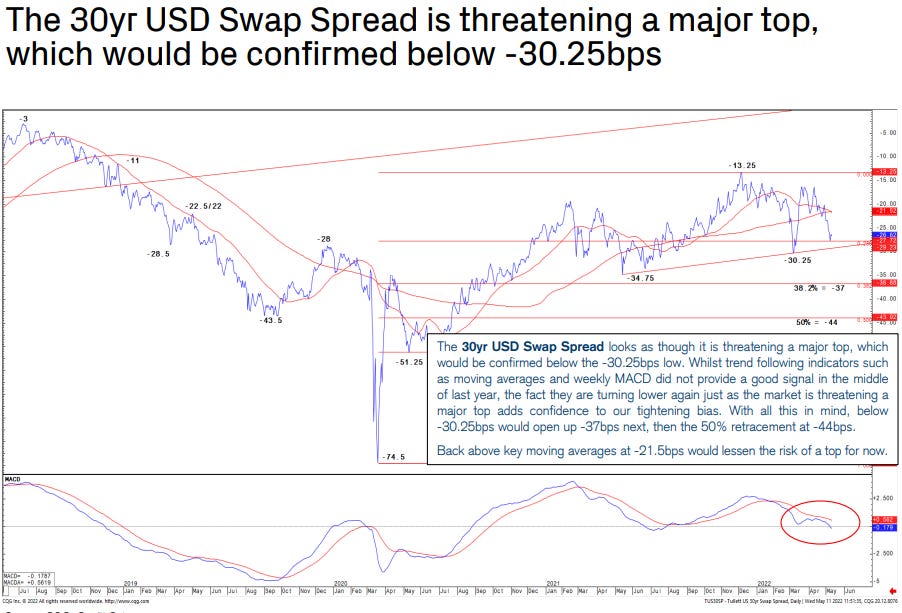

And from the bowels of the CHARTS DEPARTMENT — for those interested in global swap spreads technical outlook

Lets HOPE not (but then, hope is not a strategy …).

With that little in mind, I’m OUT and unsure IF updates possible this coming weekend. ‘Thing 3s’ bar mitzvah only 7d away (his mitzvah project — raising $$ for kids with cancer — can be view HERE) and there’s lots to do as family starting to arrive soon! Thanks in advance for your patience!!