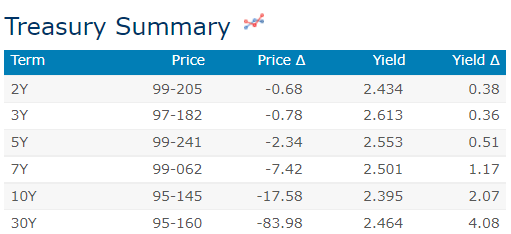

Here is a snapshot of UST rates, prices and moves as of 743a

… And HEREis what another shop says be behind the price action, you know,

WHILE YOU SLEPT Treasuries are mixed and the Tsy 2s30s curve has pivoted ~5bp steeper around a little changed belly overnight after the Fed warms toward consecutive 50bp hikes (Daly, Williams) while the EU and US noodle additional Russia sanctions. DXY is higher (+0.2%) while front WTI futures are UNCHD to open the week. Asian stocks were higher, EU and UK share markets are mixed while ES futures are showing +0.1% here at 7am. Our overnight US rates flows saw Asian real$ buy the front end and sell the back-end after 5s30s opened at -15bp and 2s10s curve at -9.5bp. Fast$ steepened the 5s30s curve and the Asian real$ selling appeared concentrated in 30's and off the run 20's. Overnight Treasury volume was about average with 20yrs (145%) and 2yrs (124%) seeing the highest relative average turnover overnight.

… > US News: San Fran Fed's Daly: Said the case for going 50bp in May has grown FT NY Fed's Williams: Must watch how the economy responds as the Fed presses toward the neutral rate RTRS Also: BBG US weighs tougher Russia sanctions after evidence of atrocities in Ukraine WaPo Inverting yield curve signals high stakes for Fed and investors BBG March's US corporate issuance was highest-ever outside of the pandemic RTRS

… and for some MORE of the news you can use » IGMs Press Picks for today (4 April) to help weed thru the noise (some of which can be found over here at Finviz).

In as far as what’s hit the inbox SINCE YESTERDAY, well not much (thankfully)

Umm … got flatteners? Speaking of the risk of recession … both literally and figuratively, Barclays Macro House View Weekly: The risk of recession

From fan-fav equity bear who’s still keeping residence with MS,

Weekly Warm-up: Boring Is Beautiful with Bear Market Rally Over; Stay Defensively Biased … After one of the roughest quarters in history for stocks and bonds collectively, the markets better reflects the "Fire" part of our narrative; but now it's about the "Ice," and that's decidedly worse for stocks relative to bonds. We are doubling down on defensives, with the bear market rally now over…

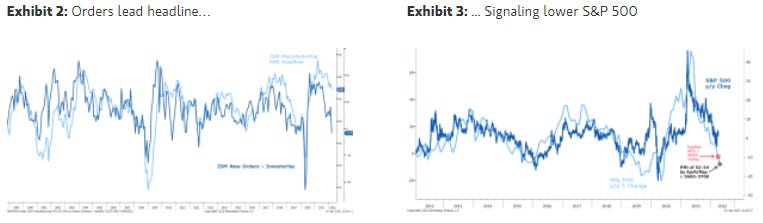

… On that score, Friday's ISM release showed a sharp deterioration in the orders component. Relative to inventories, it looks even worse, with the inventory component of the index now below orders for the first time since the recovery began. Think of this as a book to bill for the broader manufacturing economy. Based on our Ice and over-ordering thesis, we have been expecting this and now it is here. As we have shown in prior notes, this differential between the orders and inventories components leads the headline index (Exhibit 2). Importantly for investors, it suggests the S&P 500 has another rough month(s) ahead (Exhibit 3). Bottom line, the rally in stocks over the past few weeks has been remarkable, but in our view it has all the characteristics of a bear market rally, and we view month/quarter end as the perfect spot for it to come to an end.

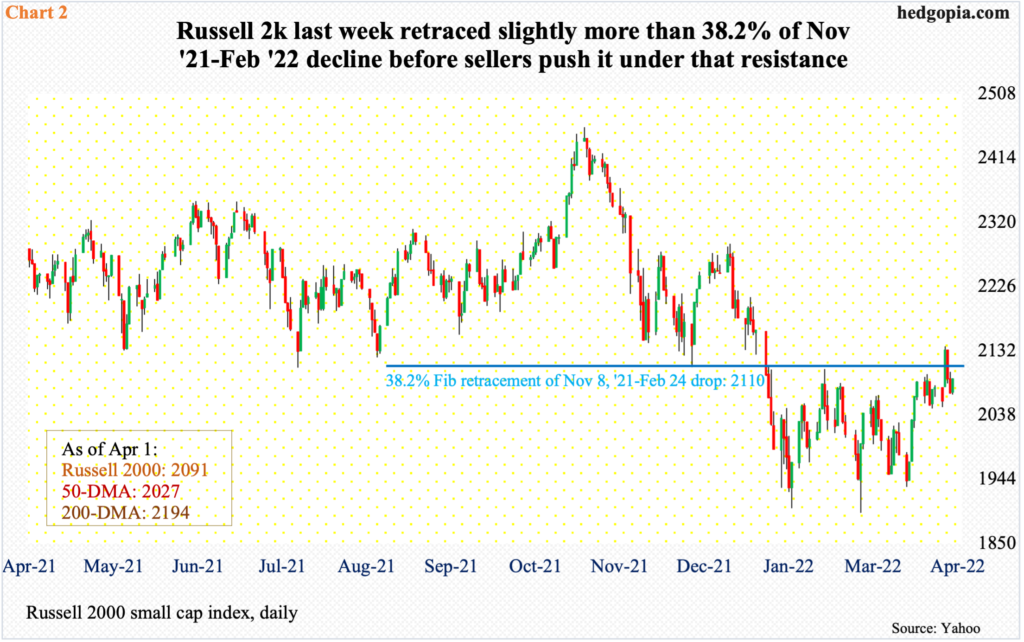

For something completely different, HEREis a bit of detail in / around longer-term R2k TREND:

For a somewhat shorter-term and technical look at FIBO RETRACEMENTS,

Hedgopia: R2k last week retraced slightly MORE than 38.2% of Nov 21-Feb 22 decline B4 sellers push it under …

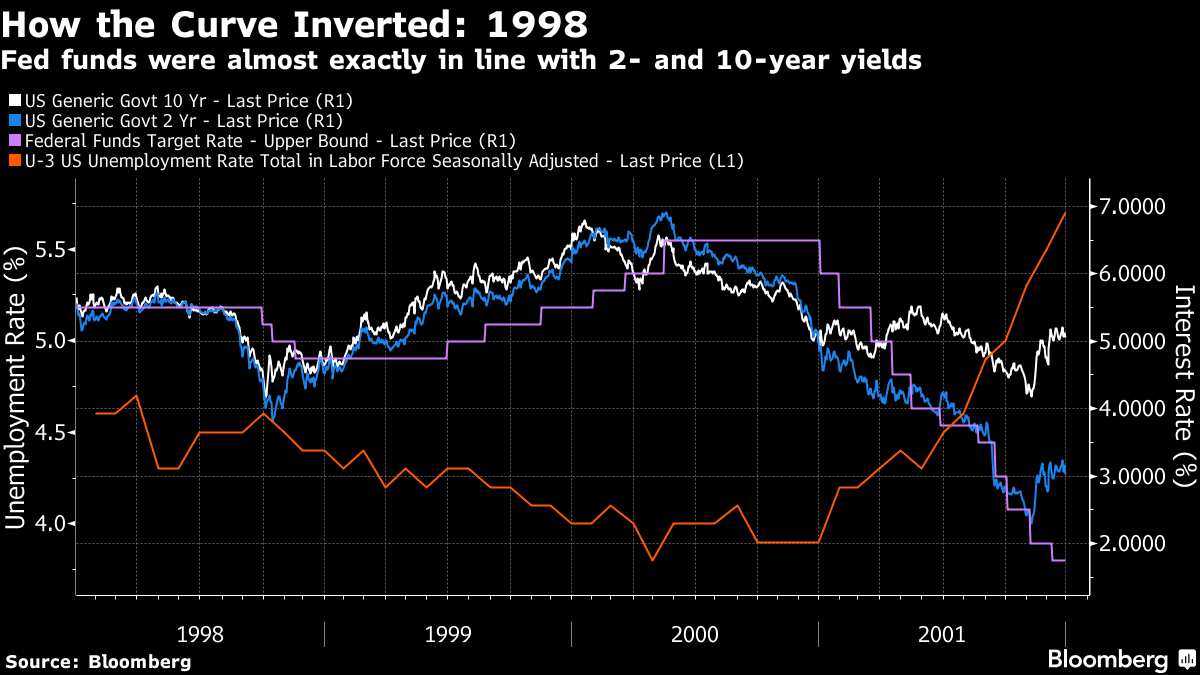

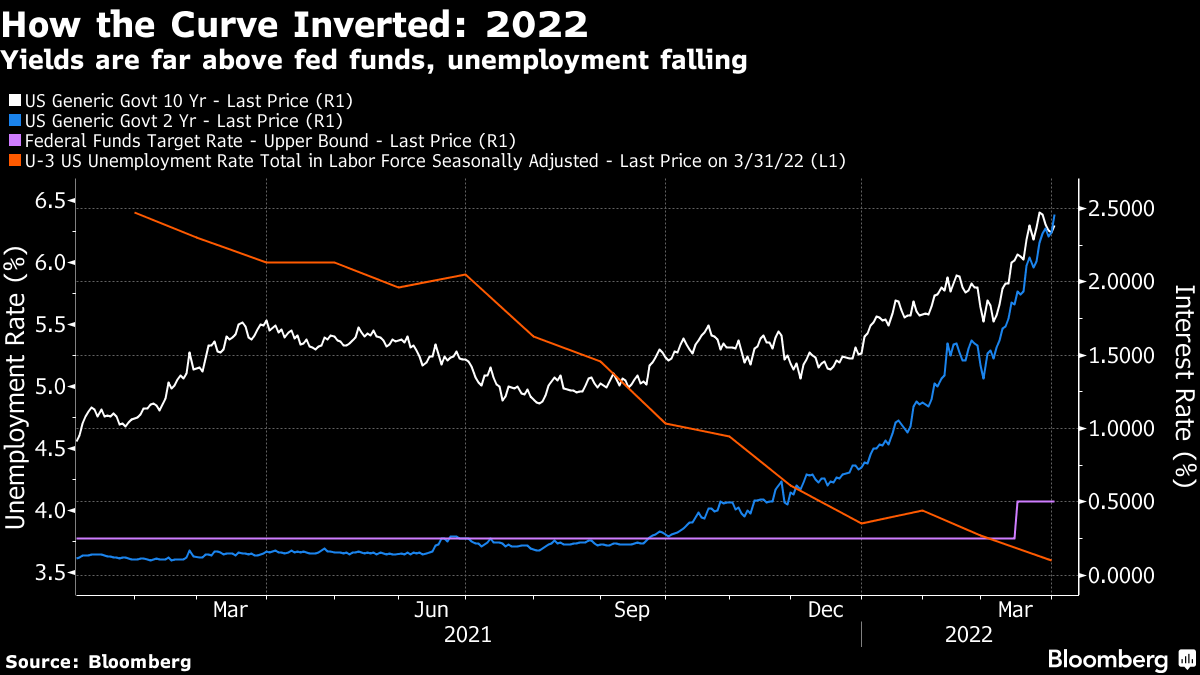

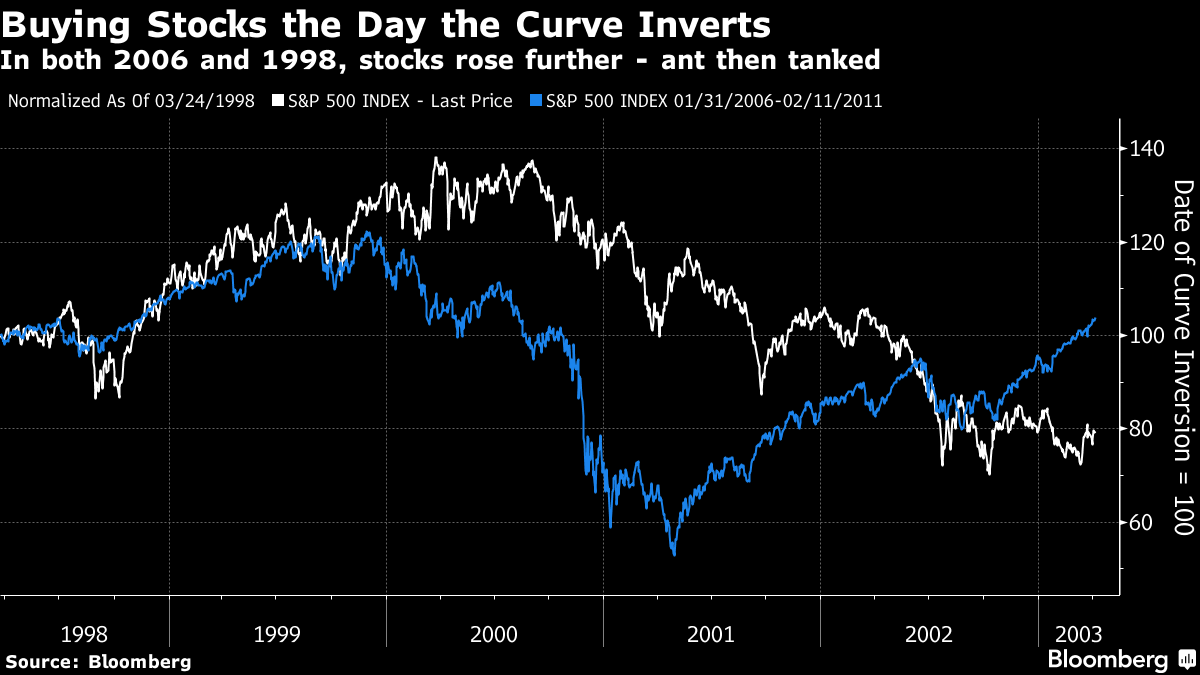

And back in the flattening yield curve obsession department, John Authers’ latest

Along with several visuals and explanations of HOW curve inverted in prior instances,

AND what one is supposed to do, always and forever

It is the conclusion which I can agree with and continue to think,

… Unlike the previous incidents, the two-year and 10-year lines have crossed when both are still far higher than fed funds, and when the unemployment picture is still improving impressively. It really is very different this time in important respects.

The difference is that the Fed is “behind the curve,” and its successful attempt to persuade the market that it will catch up has prompted a huge move for the two-year compared to overnight rates. The market is saying that the Fed is going to hike a lot in the short term (doubtless correct), and that will slow down the economy to an extent in the longer term. However, 10-year yields are still rising, implying both confidence about growth and a danger that long-term rates will eventually crimp growth and equity valuations (which is what happened in 2007.)

What next? It’s possible the yield curve will soon move out of inversion, because 10-year yields will rise. Wednesday’s publication of the minutes to the last Federal Open Market Committee meeting is expected to give details of “quantitative tightening” — the process by which the Fed will sell the bonds on its balance sheet. That might well push up 10-year yields, and may ultimately lead to the denouement many have feared for years, when longer yields finally settle into a rising trend and bring down the multiples that people will pay for stock.

But this is far from inevitable. Pension funds, which benefit from higher long-term yields making it easier for them to guarantee an income for the future, might well take the opportunity to buy longer bonds while they can. That would keep yields lower. There are plenty of such factors to watch. As I said last week, the yield curve isn’t foolproof, and a lot of things are different this time.

But it’s best to work on the assumption that as the Fed catches up, something similar to the last two big inversions will play out. Make contingency plans for something somewhere in the financial system to break in the next year or so that forces the Fed to cut rates, and to brace for a recession to arrive by the end of 2023. Can we be certain about any of this? Of course not. But it’s just as well to have that scenario as a “base case.” That would be much safer than ignoring the bond market altogether.

More on recessions and curves some other time … THAT is all (I can take) for now. Off to the day job…