… The internals were also solid, with Indirects taking down 69.0%, in line with recent auctions but above the six-auction average of 66.7%. And with Directs taking down 16.9% (also above the 13.2% average), Dealers were left holding just 14.08%, which wasn't a record low but wasn't too far from it (the all time low for the series was 12.1% in March).

Well if THAT didn’t prove a point — what happens in the ECB does not STAY in the ECB and EZ govy moves matter — well, said another way, UST auction players got a concession … ZH noted

The reason this is worrisome is clear - markets are once again pricing in non-negligible possibility of 'Italeave'...

And like that, EZ govies made a YUGE moves higher, dragging USTs along with them before someone somewhere realized there might be a reasonable level to (cover short, see value of WI30y) … Stellar 30Y Auction Sees Buyers Emerge Ahead Of Friday's CPI

But hey, maybe the EZ govy selloff (ie concession for USTs) combined WITH state of US labor market actually helped some see value in duration as ZH noted

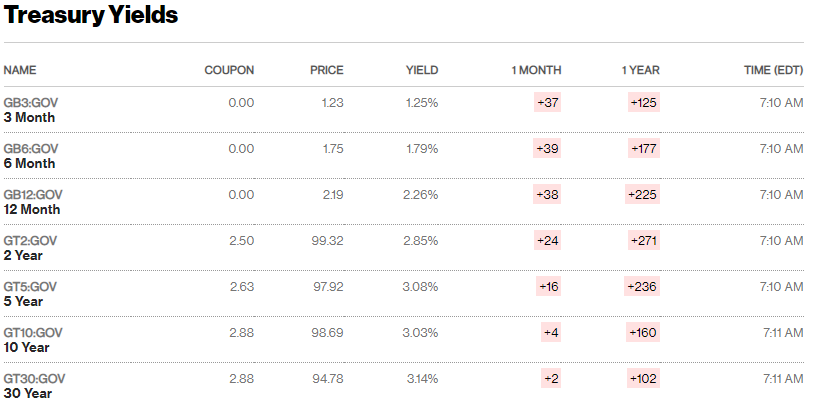

… here is a snapshot OF USTs as of 710a (via BBG.com)

… HEREis what another shop says be behind the price action, you know,

WHILE YOU SLEPT Treasuries are mixed with the curve pivoting notably flatter (2s30s -4.3bp) around a little-changed 7y point ahead of CPI. DXY is higher (+0.25%) while front WTI futures are again too (+0.75%). Asian stocks were mixed (SHCOMP +1.4%, NKY -1.5%), EU and UK share markets are all lower (SX5E -1.9%, SX7E -4.3%) while ES futures are showing -0.13% here at 7am. Our overnight US rates flows saw an 'uninspiring' Asian session that was somewhat stuck between acronyms (ECB and CPI). Our flow did see better selling in intermediates and the long-end from real$ names though another 3 block buys in FVs (4k each) were a buffer of sorts. Overnight Treasury volume was actually pretty solid at ~140% of average overall.

… and for some MORE of the news you can use » IGMs Press Picks for today (10 June) to help weed thru the noise (some of which can be found over here at Finviz).

That in mind, a couple things from the inbox which caught MY attention and getting / keeping me thinking about RATES.

First couple are from the CHARTS department where CitiFX noting it is time.

… As a consequence, the print tomorrow is hugely important from our point of view as if it is a .5 or .6 it puts the Fed in “Strike 3” territory.

One more strike and they will know in their hearts and minds that they are in trouble.

Therefore, on the back of that eventuality it could even drive them to start preparing the way for that possibility as early as next week in their guidance. Although they could “kick the baseball” to July knowing they still have some cover left in the June print. They might even wait until Jackson hole in August (although at 25-27 August that is a long way away so doubtful as that would be very late in the day)

Our bias, therefore, is, that we are on the cusp of breaking this big 3.10% on the 5-year yield (at least weekly close) which we think is now a pivotal and possibly “accelerative” level around (as repeated below)

US 5-year yield long-term chart- Why is 3.10% so important?

… Finally, and most importantly IF we decisively break above 3.10% it will be the first time in the history of the 41-year bull market in Fixed Income that a cyclical bear market high has broken above the prior cyclical high therefore by definition suggesting that we are in a structural bear market.

If that is the case, then when we look at the chart below, we see no reason why we could not see this yield head back towards the 5%+ area. In fact, it would complete a double bottom that would suggest as high as 5.5%-6.0% eventually.

Do I think we will go that high?

Probably not. However, leading into the financial crisis in 2006 our long-term US 10-year yield chart suggested we could go as low as 2% by late 2008 (The low was 2.03% in December 2008).

… If I were a betting man �� I would anticipate the Fed having to revise it’s 2023 inflation rate forecast up to 3.5% thereby suggesting the likelihood of a terminal rate closer to 3.5-3.75%

…Our “Financial Bible” (2’s 5’s curve) is NOT signaling that recession is around the corner

Right now, that curve is at +24 basis points, and we suspect could go even higher still if we make that decisive break of 3.10% on the 5-year yield resulting in curve steepening. Although the Fed is raising rates it remains well behind the curve and will not look to take rates above the level of inflation anytime soon…

The group ends noting, “It’s about to get real” and clearly these techAmentalists been around far longer than ME and have lots more details to add for those with permission to read full note.

ALSO from the CHARTS department is updated FI technical / tactical take

1stBOS Chart of the Day: With the ECB opening the door to 50bps hikes, further flattening in European curves looks likely in our view. The German 2s10s Bond Curve has reversed sharply flatter since we neutralised our long-held steepening bias at 87/87.5bps back in April and the market is now threatening a large and clear top. A close below 59.5/58bps would confirm, with scope for at least a move to the 41.5bps potential uptrend.

The firm details how it is remaining tactically bearish 30s (from 3.085%) and looking to sell both 10s should they ever rally again down to 2.885% (OR if 5s if they were to bearishly break ABOVE 3.105%).

All bases are covered and only ONE activity need apply. BEARS (kindly see government notice re BEAR SIGHTINGS in next town over just yesterday).

Moving away from bear sightings and CHARTS for a moment, a couple OTHER items worth knowing / thinking about.

First, what some of Global Wall Street is thinking in as far as curves and rates ahead of CPI — don’t tell me lemme guess — CPI related flattners? Barclays (with what I thought was a BEAR SIGHTINGS reference),

Not out of the woods In the US, headline inflation persisting at elevated levels is likely to tilt Fed communication in the hawkish direction even as the growth outlook worsens; we recommend 2s10s Treasury curve flatteners. In Europe, we maintain long EUR 2s10s30s. In Japan, we maintain our bear steepener view and long JGB ASW recommendation.

… We believe markets are not fully on board with the Fed’s messaging and recent developments and recommend 2s10s Treasury curve flatteners.

Figure 8 shows that 1y1y real rates (nominal OIS rate minus CPI swap rate) are still priced to be somewhat negative even as 5y5y real rates are slightly positive. This is in sharp contrast to historical hiking cycles, which have typically ended with a well above neutral real rate (Figure 9). Likely as a result of this relatively benign peak real rate that is priced in, markets are pricing in inflation to persist above the target level for long. Figure 10 shows 5y5y CPI swap rates are still hovering around 2.75%. We believe the Fed’s updated forecasts are likely to show not only a positive real rate but an above neutral real rate as well, which should convey the Fed’s intention to bring inflation to its 2% target over time.

We therefore find that curves such as 2s10s (or 1y1y-5y5y) are still too steep and recommend 2s10s Treasury curve flatteners (entry: 23bp).

Curve FLATTNER then it may be? As far as directionality or peak anything, goes, what IF we considered possibility rates were near peaking? Said differently,

Finding the terminal rate for the current hiking cycle is a joint discovery process for central banks and the market. We argued a couple of months ago that a rough calculation would suggest a terminal rate in a 3.25-4.25% range for the Fed and a 1.75-2.75% range for the ECB. Ahead of today's ECB meeting, market pricing was in line with the bottom end of the proposed range. Does that mean that the repricing is complete? As we suggested a month ago, probably not.

First, one should expect the market to build some risk premium as sticky inflation is likely to be bad news for growth. This implies that bonds are no longer a good hedge for equities and that they should therefore commend a positive risk premium. Second, the risks in Europe are tilted to the upside because of clearer upside risks to fiscal policy. On the other hand, a significant fiscal tightening after the US midterm elections remains the main downside risk to these terminal rate estimates.

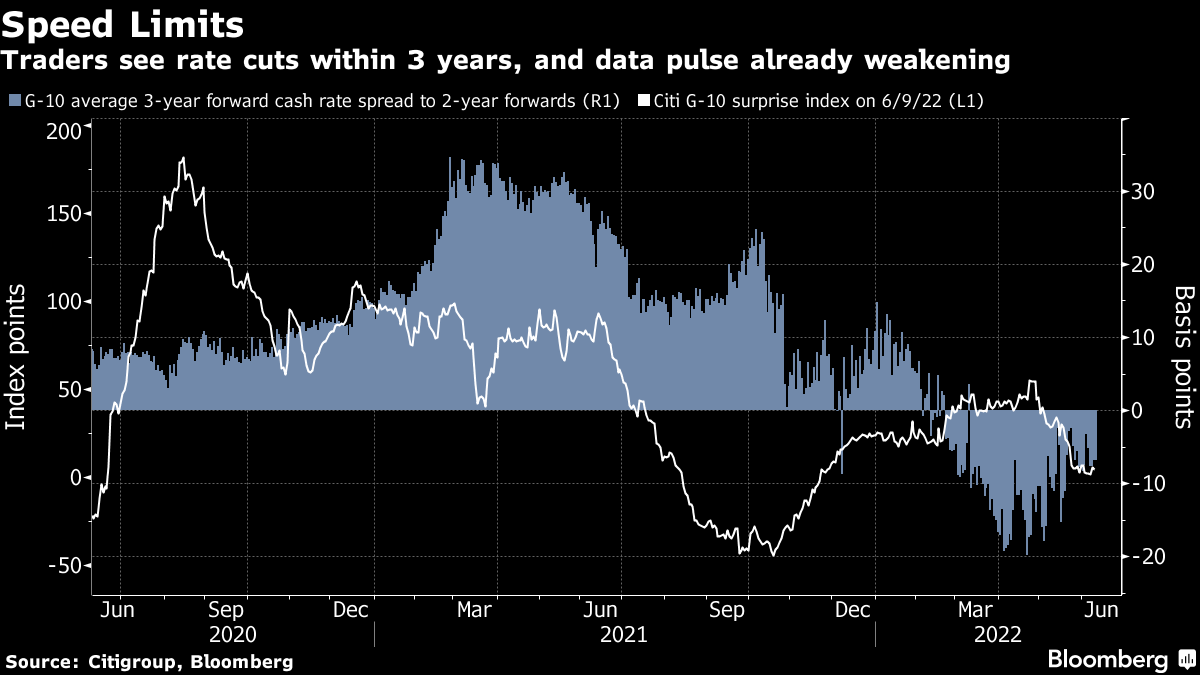

Interestingly enough, no matter how bearish you may/may NOT be at the moment, or how high you believe rates will or can ultimately go (watch 5yy), another thing has been made clear by Bloomberg, tracking rate hike / cut bets.

…Recession fears are plaguing equities once more, with a late swoon in US stocks overnight putting the S&P 500 within a whisker of entering a bear market. Alarm bells for the economic outlook have already been ringing loudly for at least three months in the rates market, with traders signaling global rate cuts are coming within three years on expectations central banks will hike hard enough to risk recession.

The picture is gloomier for countries where policymakers are already front-loading tightening moves, with rate reversals priced within two years for the US, UK, Canada and Australia. With most of the rate hikes expected in the next 12 months, the impact is apparent in the way economic data are looking much less robust. With elevated inflation set to keep policymakers’ pedals to the metal, there’s plenty of scope for equities to extend declines.

Lets see whatever the data and market reflex is and will attempt to connect some more dots over the weekend.

For NOW, while this runs the risk of appearing to be taking sides — truthfully NOT my objective — am going to copy / paste this from comedy site (The Burning Platform) because, well, satire is just that.

Sooner or later, we’ll ALL get offended (even those of us like myself, with extremely thick skin) … THAT is all for now. Off to the day job…