This morning wouldnt be the first time I’m confused … Let me explain.

Here’s Bernanke circa 2010 explaining ‘the wealth effect’ and BOON to the consumer with LOWER INTEREST RATES, in a WaPO OpED

… Lower corporate bond rates will encourage investment. And higher stock prices will boost consumer wealth and help increase confidence, which can also spur spending. Increased spending will lead to higher incomes and profits that, in a virtuous circle, will further support economic expansion…

Here is Bernanke just yesterday on CNBC (via ZH — sorry, NOT sorry)

"It Was A Mistake" - Bernanke Says Fed's Fear Of 'Shocking' The Market Delayed Tightening Move

And to think we are to trust these folks running our global central banks? Hypocrisy? No good deeds going unpunished? I’m really not quite sure WHAT to think here and now other than to hope MY feelings are going to be as transitory as, well, TRANSITORY was(n’t)? Clearly I’ve got issues and as I struggle through them (my market-related struggle continues only until Thursday — OFF Friday for all good reasons discussed this past weekend!),

… here is a snapshot OF USTs as of 722a:

… HEREis what another shop says be behind the price action, you know,

WHILE YOU SLEPT USTs are cheaper and flatter following EGBs after ECB member Knot said he supports a quarter-point increase in interest rates in July and that a bigger move ‘may be justified’ if data show inflation pressures worsening. China restriction-easing also has risk-assets buoyant, DAX +2% and S&P fut’s +62pts here at 7am. 5s30s is -3bps, 2s5s10s +1.25bps, while real yields are leading the nominal cheapening. DXY weakening significantly -0.6%, energy markets responding as expected (CL +1%, NG +4%, HG +0.9%). Volumes running ~85-90% 30d average across the UST curve.

… 30y yield, weekly: 2017 range still holds court amid oversold conditions…3.25 to 2.70% range.

… TIC Flows: U.S. TIC report showed a net $149.2 bln inflows into securities in March following $160.3 (was $162.6) bln in February. A total of $23.1 bln in net long term securities were also bought after $141.7 bln previously. All of the increase on the month was via private accounts which purchased $172.4 bln, while official accounts sold -$23.3 bln. Of note, Japan was the biggest seller of Treasuries, dumping -$73.9 bln, followed by China's -$15.2bln, and -$13.2 bln from Luxembourg. The Cayman Islands was the largest purchaser in March at $18.0 bln, followed by Canada at $13.7 bln.

… and for some MORE of the news you can use » IGMs Press Picks for today (17 May) to help weed thru the noise (some of which can be found over here at Finviz).

Here are a few random thoughts ahead of this mornings ReSale TALES

UBSs Paul Donovan ASKS

Are US consumers still spending? The details of US April retail sales data will be monitored for evidence of demand destruction, and ongoing demand normalization. As US households spend more money fuelling the family fleet of SUVs, they have less money to spend elsewhere. In addition, areas where demand was exceptionally strong in 2021 have been moving towards normal or even below normal demand in 2022…

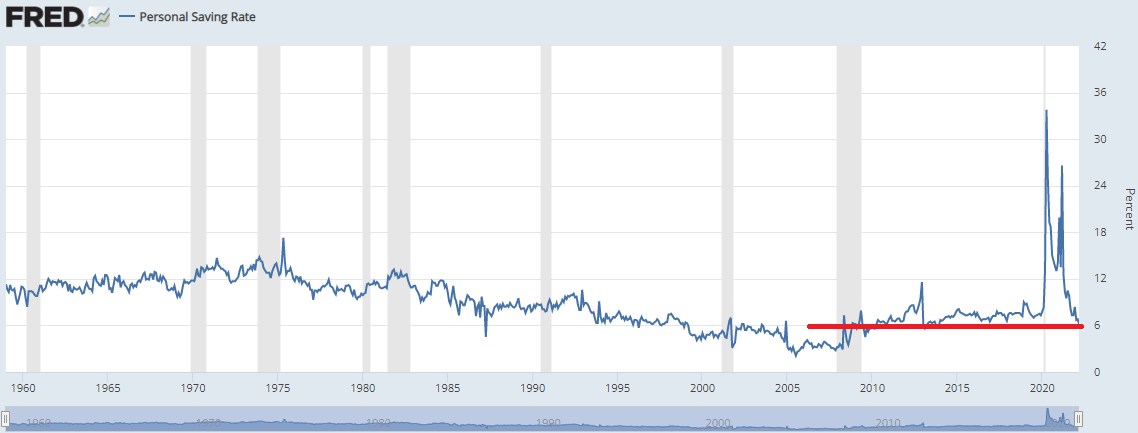

To the FRED, Batman

First is THIS VISUAL of the Personal Savings Rate which I believe speaks for itself

And then there’s THIS VISUAL which FRED offered to help as we are all

… Despite the sharp increase in gasoline prices in the first quarter of 2022, purchases of gasoline and other energy goods comprised just 2.7% of total consumer expenditures in that quarter, which is about average for the period since 2010. Additional energy price increases could drive the expenditure share higher than it was in the first quarter. But currently, the share of personal consumption expenditures has been well below the peak of 6% reached in 1980.

Meanwhile, growth is slowing, THEY SAY. BUT …

US growth is slowing, but not (yet) enough The Fed is approaching its dual mandate from "above": inflation exceeds the 2% target and the labour market is through full employment. Thus, in order to fulfill its dual mandate, the Fed should aim to raise the unemployment rate. This will require slowing growth below potential.

The Fed's Senior Loan Officer (SLO) survey has historically been a good indicator of underlying growth relative to potential. The latest SLO released earlier this month indicates that growth is slowing down, but remains above potential. This should lead the Fed to deliver more tightening than what is currently priced in.

And in the department of DEFENSE winning games — here, one of Global Wall Streets most popular kids — Goldilocks — out defending their recent downgraded econ call,

Our US Financial Conditions Index (FCI) has tightened by 80bp since Fed officials forecasted 2.8% growth for 2022 (Q4/Q4) in the March Summary of Economic Projections (SEP). How large a growth downgrade should we expect from the Fed if the recent FCI tightening is sustained?

Historically, we find that a 100bp FCI tightening leads to a 0.7pp downgrade in year-ahead SEP growth forecasts. Combined with the 2.7% year-ahead growth forecast in the March SEP, this suggests that the recent FCI tightening alone would push the June SEP year-ahead forecast down to roughly 2% and thus much closer to potential.

Alongside the much lower than expected Q1 GDP print and the negative turn in growth news so far this year, our analysis points to significant downgrades to Fed growth forecasts in June.

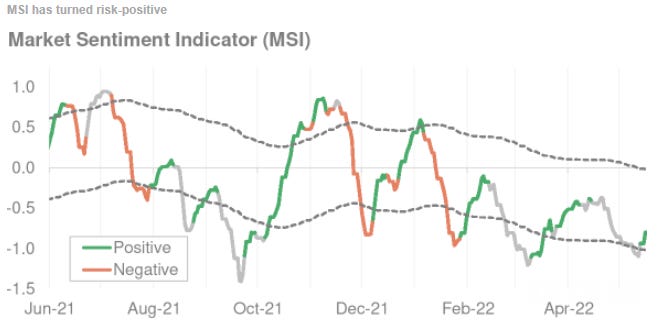

More MARKET-related DEFENSE in the form of some good news from MSs NOT stock jockey (Sheets)

MSI Turns Positive We recently introduced our Market Sentiment Indicator (MSI). We highlight the indicator's latest signal change, and run through a brief set of FAQs.

MSI signal has turned positive: The MSI generates risk-on/risk-off signals based on two conditions – the level andthe change of our MSI – both of which are currently satisfied. Sentiment that is improving from extreme negative levels leads to a positive signal.

What could change this signal? While the 'level' condition should remain satisfied for some time, the 'change' condition is more fragile. Any further deterioration in sentiment data would cause the signal to return back to neutral.

Tracking the MSI on Bloomberg: We track the data daily, posting updates of the indicator's level (MSXAMSIL Index) and signal (MSXAMSIS Index) to Bloomberg. A weekly summary is published in our Cross-Asset Spotlight.

Who cares WHAT it is, at least it’s turned POSITIVE, amIright?

Global Bond Yields look likely to enter a short-term consolidation phase over the next 1-2 weeks after rejecting major long-term supports, however for the US at least, we stay biased towards eventual clear breakouts above the 2018 highs.

And finally, in the department of WHO CARES or WHAT TO DO with all this (and more)knowledge, is BLACKROCKS LATEST

• We recently cut risk, but stick with stocks over bonds for now. Equity prices now reflect much of the worsening macro outlook and hawkish Fed, in our view. • Markets came to grips last week with the trade-off central banks face: choke off growth or live with inflation. Yields fell and stocks bounced off new 2022 lows. • U.S. retail sales and other activity data will give investors a read on growth momentum. We believe the restart from pandemic lockdowns has room to run.

Of course they prefer anything over bonds. Who doesn’t? They’ll ONLY come running if when things get really bad and by then, it’s usually too late and the smarter money had already positioned for the move (lower in yields). It’s not to say / suggest it’s a foregone conclusion BUT the warning signs have been discussed before. IF the Fed becomes soft on fighting inflation, well THAT might be something that turns bond bulls to bears.