Good morning. I’ve NO idea why I’m still doing this other than I can’t help myself. Watching the bond market over the years has been a tougher habit to break than I ever imagined. Now even more so after last weeks historic bad year!

That said, here are a few things that I’m told occurred overnight. First an HOURLY visual of 5yy and again I ask, who you gonna believe, ME (or ‘them’) or your own lyin’ eyes.

Clearly some impact from hawk talk overnight … AND some markets as of 650a,

Here, from the authors OF what happened while we slept,

US News: Fed Governor Brainard will call inflation 'too high' at nomination hearing today NYT San Fran Fed President Daly the latest FOMC participant to set sights on a March hikeRTRS Philly Fed President Harker open to the March hike idea too FT Manhattan rents hit their highest levels ever in December CNBC The average price of a new car went up $6000 in one year Jalopnik Cass freight expenditures (trucking) rose 44% YoY in December to a record Cass Reality bites: California tells virus-positive workers to stay on the job Yahoo Canada drops vaccine mandate for truckers under pressure from industry RTRS Government losses on student loans top $100bn amid pause on payments WSJ What inflation will do for your 2022 taxes WSJ French Dressing finally deregulated after 72 years WSJ

AND,

WHILE YOU SLEPT

Treasuries are sharply mixed and the curve a hair steeper ahead of this afternoon's 30-year reopening. DXY has extended yesterday's losses (-0.11%, see attachments) while front WTI futures are UNCHD. Asian stocks were mixed to lower (China), EU and UK share markets are aggressively mixed this morning while ES futures are showing UNCHD here at 7am. Our overnight US rates flows saw a quiet Asian session with hedging flow taking a breather after an active start of the year.In London swaps, 2-way activity seen in the belly with the desk noting that spreads feel heavy ahead of widely-expected financial/swapped issuance. Overnight Treasury volume was ~65% of average with 30yr bonds seeing about 1/2 their average turnover this morning- surprisingly low for an auction day.

So, in short, NOT MUCH OVERNIGHT despite / because all the hawk talkin.

From today’s FIVE THINGS (from BBG.com), on Fed Policy,

In the wake of yesterday’s highest annual U.S. inflation reading since 1982, more Federal Reserve officials are signalling support for a hike as soon as March. San Francisco Fed President Mary Daly and her Philadelphia peer Patrick Harker added their voices to the chorus in interviews published yesterday evening and this morning. Investors have been listening, with markets now pricing a 90% chance of a hike in March. Attention today will be on the confirmation hearing of Lael Brainard in the Senate. The vice-chair nominee, who last publicly commented on the economic outlook in September, said in prepared remarks that tackling inflation is the bank’s “most important task.”

BBGs Macro Squawk (554a) where I’ve taken the liberty to add FT LINK thru to HARKER interview and I’ll also state upfront, he’s in a ‘non-voting’ district (as per WFCs FOMC 101)

Fed Hawks Steepen Eurodollar Strip; Stocks Steady

European equities trade little changed with modest gains in tech, autos and utilities offset by softness elsewhere. CAC 40 underperforms, dropping as much as 0.6%. U.S. equity futures hold in small positive territory. Fixed income is relatively quiet, with changes across major curves limited to less than a basis point so far. 10y Treasuries stall near 1.75%. Eurodollar futures bear steepen a touch after a round of hawkish Fedspeak during Asian hours. In FX, Bloomberg Dollar Spot dips into the red pushing most majors to best levels of the session. NZD, AUD and GBP are the best G-10 performers. Crude futures maintain a relatively narrow range. WTI is flat near $82.70, Brent stalls near $84.84. Spot gold dips before finding support near $1,820/oz. Most base metals are in the red with LME zinc lagging peers. KEY HEADLINES:

Omicron spreads in China; France eases border curb: Virus Update

China banks curb property loans to local Government Firms

U.K. says 3% of workforce absent in late December due to Covid

Daly joins camp that sees Fed rate liftoff as early as March

U.S. to propose UN sanctions after North Korea missile launches

Now in as far as yesterday’s CPI and today’s PPI goes, and while rents and AUTOS helped drive yesterday’s CPI, today’s PPI shouldn’t be ignored. For somewhat more, see UBSs Paul Donovan morning note,

Yesterday’s US consumer price inflation attracted economists’ curses, as it means we will spend 2022 forecasting used car prices. These are pushing inflation up today, and how far used car prices fall in 2022 will determine how much headline consumer inflation falls. The millions of US consumers who do not drive a car are experiencing an inflation rate about half the headline number.

Today’s US producer price inflation ultimately matters more to markets. First, most companies sell to other companies, so this drives revenue growth. Second, producer prices signal corporate pricing power and thus inflation pressures. Corporate pricing power (measured by the monthly change in core producer prices) peaked in the second quarter of 2021 and should continue to decline…

Continuing along the ‘flationary theme after CPI and ahead of PPI, John Authers of BBG talks about how broad based inflation was (is) BUT ALSO NOTES this morning,

Breaking inflation down into its main components, again using the ECAN function, we find that shelter’s importance is increasing, while the resurgence in higher sticker tabs for used cars and trucks also drove prices higher. The former will likely continue to push inflation upward; the latter should almost certainly begin to drag it down before long. Gasoline remains a huge contributor to year-on-year inflation, but this should begin to fall thanks to the increase in oil prices at the beginning of 2021. Year-on-year increases should diminish or even reverse:

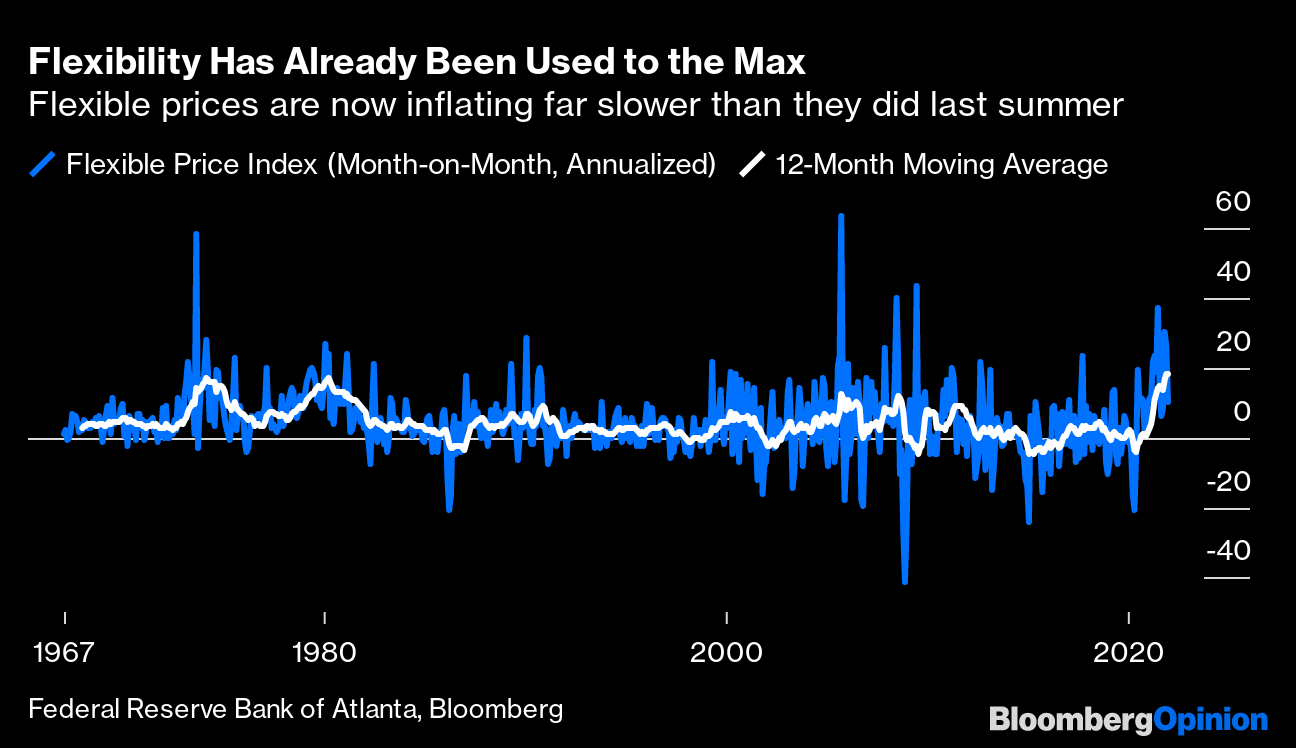

Meanwhile, the Atlanta Fed’s data on flexible prices that can easily be changed in a hurry also gives reason for hope. Last year saw the greatest-ever rise in flexible prices, a series that the bank had been following since 1967:

Even amid the far greater inflationary psychology of the 1970s and early 1980s, spikes this high in flexible inflation were soon followed by a decline. There is every reason to expect that rises cannot continue like this for much longer. If we look at month-on-month figures for flexible prices (which the Atlanta Fed shows on an annualized basis), we can see that the rate of increase of prices that can most easily be moved is already dropping substantially. It's reasonable to think that the first wave of price rises in response to the pandemic is over. The two big spikes in the past, incidentally, came during the oil embargo of 1973 and in the month after Hurricane Katrina in 2005:

There are also glimmers of light when we look at broader inflation indicators. Last year, we tracked a group of different indicators weekly (explained here), in an attempt to see if inflation was breaking decisively out of the disinflationary norm of the post-crisis decade. By year-end, they had done their job by showing inflation had indeed moved up a level and that the picture is far more subtle than people on either side of the debate tended to admit. However, I thought it was interesting to update them one last time, below, to cover the final official data of the year …

More from BBG.com — an interesting story earlier this morning detailing some strategy from GS,

Valuations less demanding today than 2000, according to note

Strategists say slowing economy will hurt cyclical value most

… Following a recent selloff spurred by soaring Treasury rates, “only a modest further move in longer-term yields” is now expected, the strategists led by Ben Snider wrote in a note to clients. This means “limited further risk to growth stock valuations from the discount rate.”

… “Bond markets point to further upside for value versus growth,” Morgan Stanley strategists led by Ross MacDonald wrote in a note to clients on Thursday. While a growth scare would be a major risk for value stocks, the strategists “see few signs of this fear yet.”

Goldman strategists, on the other hand, see the backdrop favoring growth.

“The likelihood of slowing economic growth in 2022 is an argument in favor of growth stocks,” the strategists said, adding that comparisons with the tech bubble at the turn of the century may not be entirely appropriate. “Adjusting for the interest rate environment, growth stock valuations look much less demanding today than they did in 2000.”

Is there ANY ‘perfect hedge’ for high/rising rates (nominally and of inflation)?

… On Wednesday, we learned something remarkable: the price of a basket of goods bought in the U.S. cost 50 basis points more in December than it would have a month earlier. Year on year, inflation is running at 7%. Given that information in advance, many investors would have opted for gold, a metal celebrated for its ability to hedge inflation through history. And yet, since the end of 2020, gold has done less than nothing in nominal terms. It dropped about 4%. In real terms, it’s down double digits.

Maintaining purchasing power is one of the most basic goals of money management. But in periods of rapid price rises, particularly when real bond yields are below zero, this is hard. Energy stocks have generally done well, but that may just be because our experience of such events is associated with high oil prices. This time may be different. Instead, investors might favor companies that make products with low price elasticity of demand. In other words, companies that can raise prices without losing customers. And that suggests we’re entering a period where active management will beat broad-market ETFs. Time will tell.

Since I was on the site, I also thought one truly final link offering something to consider in as far as global markets, macro and impacting direction of RATES, was worth note.

Bye-Bye, Stimulus: Where Budget Cuts Threaten Growth Around the World

A pivot away from government intervention will weigh on some economies, while others shrug it off.

The world economy bounced back from the Covid-19 slump faster than most forecasters reckoned was possible a year ago—thanks largely to record injections of government money. Now those aid programs are getting trimmed or wound down.

What that means for global growth is one of the key questions for 2022. Financial markets are fixated on how fast central banks will raise interest rates to counter surging inflation. But how governments adjust their budgets will likely have a bigger impact on economies than anything monetary authorities do, at least in the developed world.

Belt-tightening is under way at various speeds in different parts of the world, and much of it is provisional. The omicron variant could yet upend governments’ plans.

In the U.S., President Joe Biden’s proposals to ramp up spending on child care and clean energy have hit a wall in Congress, though they’re not dead yet. Offsetting that is the prospect of more stimulus in Japan and China—and perhaps in Europe, where Germany’s new government is keen to make green investments. Here’s a roundup of where fiscal policy is headed in some of the world’s biggest economies.

U.S.

After the biggest stimulus program in history, budget policy swung from being a support for growth to becoming a drag in the second quarter of last year, according to the Brookings Institution’s gauge of fiscal impact.

Biden has been pushing a spending bill worth $1.75 trillion over a decade, with the biggest dollop coming this year. It includes an extension of the child tax credit and support for clean power and electric vehicles. The president has been unable to win backing from West Virginia Democratic Senator Joe Manchin, whose vote is needed to pass the measure, so it’s on hold for now.

If the so-called Build Back Better legislation collapses, it would likely shave about 0.75 percentage point off 2022 growth, according to Moody’s Analytics, which currently forecasts a 4% expansion. Passing a Manchin-approved version of the bill could add 0.5% to growth, Moody’s says. Meanwhile, Biden has acted to prolong one kind of stimulus that doesn’t require a Senate vote: extending a freeze on student-debt repayments until May…

And they’ve got more from around the globe in as far as belt tightening — who, what, when and where…

That’s all for now. Off to the day job…updates when possible…