while we slept; 'Getting the price of oil down is really the whole ballgame here...'; Bonds > Stocks, No-Growth Q2, Fund Flows -DataTrek; a 'memo' from inside the Fed?

Good morning … SNB surprised with 50bps HIKE and just now, BoE surprising with ‘only’ 25bps? This goes to show when you think you’ve got it figured out, hawks at the Fed voting for somewhat LESS hawkish outcomes which were actually produced?? Did you catch the dissent in the press release?

Okie dokie … I couldn’t resist passing this one along as it stopped me in my tracks

ZH: Stocks, Bonds, & Bullion Rally After Powell's Perjury-Prone Presser

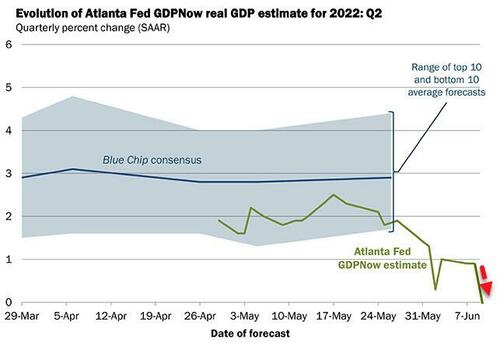

…He then shifted from prevarication to total perjury when - on the day that retail sales printed negative and the Atlanta Fed GDPNOW model forecast tumbled to 0.0% - he dared to utter the following words:

“There is no sign of a broader slowdown in the economy that I can see.”

Then, Atlanta Fed GDP cutting GDP f’cast to ZERO, "…Confirming Technical Recession” -ZH HERE

I’m sure it’s nothing … fastest economy in the world. world. world…or something like that …

And we were just then getting started? Yep

ZH: Fed Hikes Rates By The Most In 28 Years, Signals Volcker-Era Is Back

And then as ZH has had time to compile (and I no longer am paid to help do so),

ZH: "Don't Panic": Wall Street Reacts To Fed's Biggest Rate Hike In 28 Years

The GOOD NEWS is in, well, the BAD NEWS as Barclays detailing why they now see only 50bps hike next. Again from ZH

ZH: Bank Which First Correctly Called 75bps Hike Now Sees 50bps In July Due To Economic Slowdown

One week ago, well before the WSJ's leaked flipflop on what the Fed will do, Barclays rates strategists Jonathan Millar and Ajay Rajadhyaksha were the first to correctly call a 75bps rate hike when 50bps was still the broad consensus. Well, moments after Powell proved them right, the Barclays duo came out with another report which maybe while not as remarkable is still quite noteworthy in its break from consensus. Indeed, with most banks now expecting the Fed's autopilot to kick in and for the Fed to keep hiking 75bps (even though Powell said not to expect 75bps moves to be common) with Goldman now calling for another 75bps in July, Barclays is once again taking the other side, and writes that "the Fed will go back to a 50bp hike in July, amid signs that consumption and the US housing market are slowing." …

More on this in a moment. And NOW back to our regularly scheduled programing … here is a snapshot OF USTs as of 713a:

… HEREis what another shop says be behind the price action, you know,

WHILE YOU SLEPT Treasuries have seen a very lively bear-flattening after Wednesday’s relief rally. Block activity dominated the Tokyo session (at least 9 blocks, focused on flattening FV-TY), while risk-assets have given back all of the Powell presser-inspired gains (SPX futures -90pts at 6:30am). The surprise 50bp hike from the SNB has only accelerated the retracement from yesterday’s moves, CHF +2% (on a drop of FX language in the Statement), while 5y bunds are +18bps, 10y US real rates +13bps, US 5s30s -5.5bps so far. Flows from our desks have been reportedly light, futures leading activity ~115% of the 30d average, some listed downside going through in TY during the London morning (TYN2 113/112 put-spreads).

… and for some MORE of the news you can use » IGMs Press Picks for today (16 June) to help weed thru the noise (some of which can be found over here at Finviz).

Here are a couple OTHER items YOU may (also) want to consider as the apocalypses arrives (joking … i think // i hope) …

BBG detailing what Fed watchers will be watcher’ing in coming months

… Then on Monday, word started leaking out that instead of the expected 50 bps hike, the Fed would likely go 75 bps. On one hand, that makes sense. If CPI comes in hotter than you think, you gotta do more. On the other hand, the CPI miss came largely from oil, and the oil shock stems from the war, so what do rate hikes accomplish? Why would inflation that is a result of some outside shock, not related to underlying demand, be a reason to hike even further?

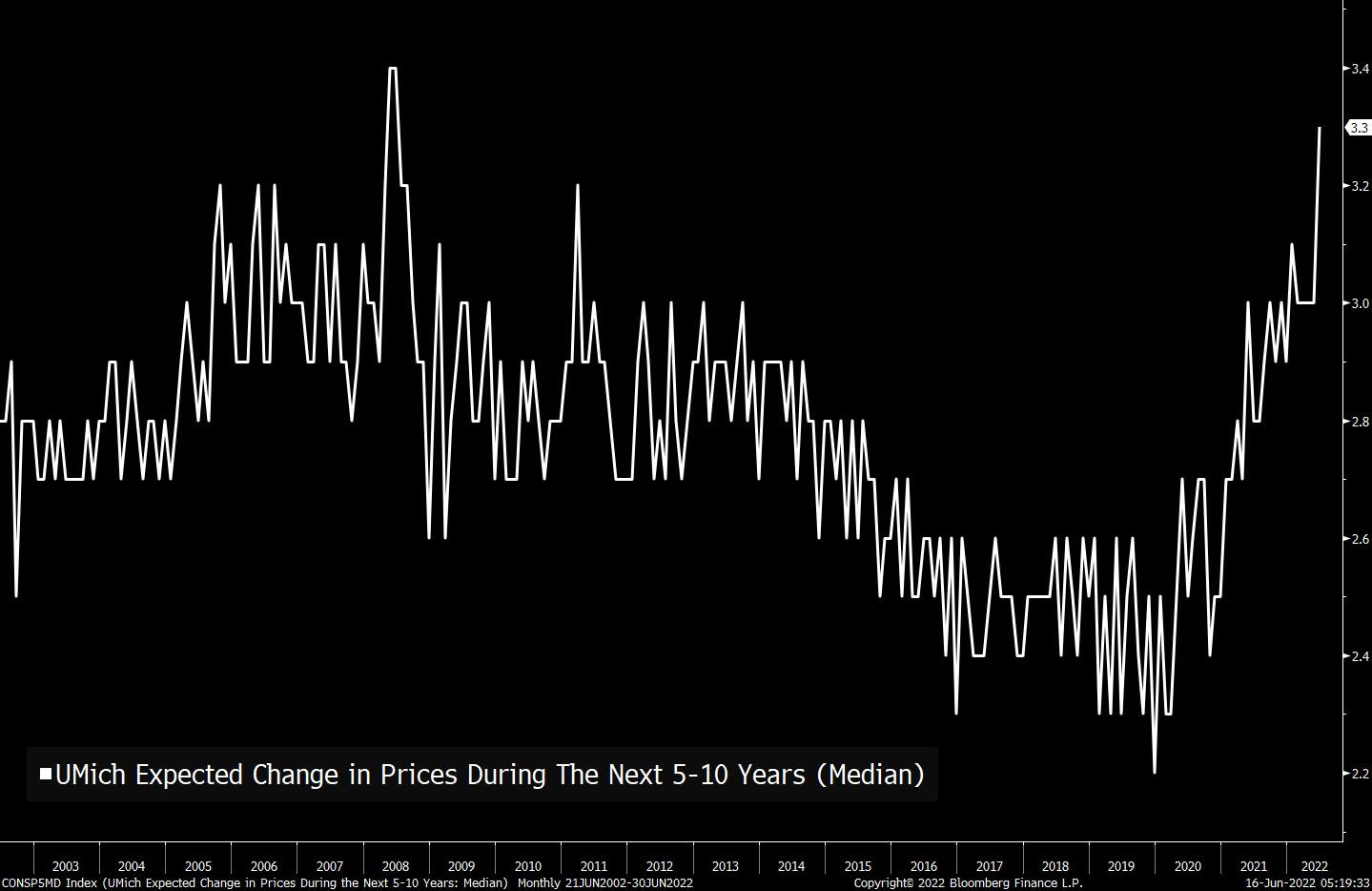

Powell answered that question clearly yesterday, by pointing out that there was another datapoint released on Friday as well, beyond just CPI, and that was the University of Michigan Sentiment survey, which among other things asks respondents about their own inflation expectations. That number jumped from 3% to 3.3% in the month.

Here's Powell:

"We also noticed that the index of common inflation expectations at the board has moved up after being pretty flat for a long time. So, we're watching that, and we're thinking, "this is something we need to take seriously." And that is one of the factors, as I mentioned, one of the factors in our deciding to move ahead with 75 basis points. Today is was what we saw in inflation expectations."

He also said something else which is key, which is that while central bankers typically like to look at "core" measures of inflation (which strip out volatile, global prices) that for the public, it's headline inflation that actually shapes expectations. That makes sense. People don't distinguish personally between core/non-core, and of course the price of gasoline is so publicly visible to everyone.

Here's Powell again:

But all over the world, you are seeing these effects. And so -- and we're seeing them here, gas prices at, you know, all-time highs and things like that. That's not -- that's not something we can do something about. So that is really -- and by the way, headline inflation, headline inflation is important for expectations. People have -- the public's expectations; why would they be distinguishing between core inflation and headline inflation?

Core inflation is something we think about because it is a better predictor of future inflation. But headline inflation is what people experienced. They don't know what core is; why would they? They have no reason to. So, that's -- expectations are very much at risk due to high headline inflation.

This is a very clear expression of the Fed's thinking -- why it will get more hawkish in response to higher oil. Regardless of the cause, it's headline inflation that shapes expectations. And the survey shows expectations are on the rise. And the genie that the Fed is determined to not let out of the bottle is anchored inflation expectations. The Fed takes tremendous pride in the Volcker era, and its aftermath, in keeping expectations so tamed and stable for so long. And it sees what's going now with oil as a threat to those expectations.

Getting the price of oil down is really the whole ballgame here. If it doesn't go down, then the Fed will only go harder on the rate hikes to crimp demand.

Game on. And speaking of OIL …

ZH: 'Big Oil' Responds To Biden's Threats: Here's 10 Things You Can Do To Ease Gas Prices

Pop the corn, there, cornpop … this all about to get good…

DB chart: Volckerian expectations from a non-Volckerian Fed …

This, in our opinion, is the basic inconsistency of the present market/Fed dialogue. Both current flatness of the 2s/10s and the shape at the front end of the curve are the result of curve’s adjustment to the near-term Fed expectation. It is largely the doings of the 2Y sector which is currently pricing aggressive rate hikes, against the background of what by Volckerian standards is an uber-dovish Fed.

Paul Donovan of UBS thinking more BURNS than Volcker in HIS latest

More Burns Bumble than Volcker Shock The US Federal Reserve raised rates 0.75%. This was not a "Volcker Shock" (taking control with a clear strategy). It was more a “Burns Bumble” with external pressures undermining credibility and coherence. For investors, it likely signals volatility…

Barclays — leading the way to 75bps call in June and now back to ‘just’ 50bp

June FOMC: A big statement about price stability The FOMC made a strong statement in today's meeting, boosting the target range for the funds rate by 75bp and sending a resounding message in its projections that price stability is being prioritized over full employment. We expect 50bp hikes in July and September, and a terminal range for the funds rate of 3.25-3.50%.

DataTrek with an interesting email (at least subj line),

June FOMC Recap: On Track for 75bp in July and 3.25-3.5% by End-2022

Finally while running the risk of perceived offensiveness by copying / pasting anything from Burning Platform, well, this one seemed like it had to be relayed. Because. You know. Higher rates.