Good morning … (concessions are) easy come and easy go.

It would be hard to imagine a 5yr auction going as well as a 2yr auction (although one doesn’t have to imagine because it DID happen) so with THAT in mind,

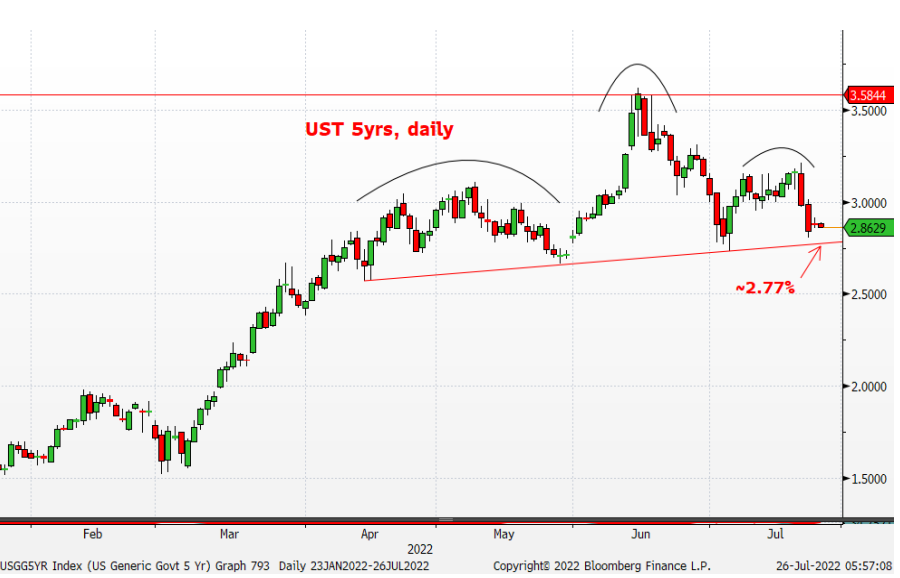

Yields appear to be at / near resistance (yellow) while a shocking hike (100bps tomorrow) would likely be needed to see 5yy up nearer 50dMA of 3.04. That seems like a stretch not unlike sentiment with momentum becoming overBOUGHT (red). For a somewhat healthier more robust look at / discussion of 5yy see just below. This afternoon’s liquidity event (5yr auction) sure could use a concession but then again, ZH (and global Wall St) reminds,

Perhaps things happening for a reason and by this I mean some sort of assistance to help Yellen and Treasury place 5yy with a somewhat more opportunistically LOW coupon? I dunno … here is a snapshot OF USTs as of 707a:

… HEREis what another shop says be behind the price action, you know,

WHILE YOU SLEPT Treasuries are higher and the belly's outperformingafter a major US retailer warned after yesterday's close while turbine 'issues' persist in Europe's gas pipeline from Russia. So 'risk-off' (XBT -5%) is the flavor of things this morning. DXY is higher (+0.55%) while front WTI futures (see attachment and discussion) are higher too (+1.55%). Asian stocks were mixed though Chinese markets all higher, EU and UK share markets are mostly lower (SX7E -1.2%) and ES futures are showing -0.35% here at 6:55am. Our overnight US rates flows saw a range trade in Asian hours with no discernible flow and little volume during their hours (~70% of ave). A block buy of 3k TYs was posted 15mins ago. Overnight Treasury volume was actually ~140% of average approaching 7am so Treasury turnover must have picked up markedly during London's AM hours- though we're too early for their flow update.

… US news: Inflation, the strong dollar and the fading pandemic ties retailer(s) in knots CNBC Some makers of 'luxury items' re-jigger tactics to appeal to cash-strapped shoppers RTRS With Omicron, reinfections are increasing MSN If Q2 GDP prints negative is the US in recession? Here's why it's hard to say: NYT US Treasury officials point to tax receipts and incomes as proof that the US economy remains in good shape RTRS The stock buyback blackout period is over ZH

… Our first attachment looks again at UST 5yr yields and how 5's appear to be in the final(?) throes of tracing out some form of a Head & Shoulders Top or Rounding Top in yields. If true , then the neckline or range resistance levels near 2.77% (neckline) and 2.71% (multi-month range resistance) will be critical resistance and perhaps a tell, if broken, that the move high in yields may be in. That bear trendline/neckline since the mid-April move low in yields looks like a 'good' line given that it is derived from three yield lows. As such, a daily close <2.77% today or tomorrow might be the sign that rates will shift to new, lower rate ranges?

… and for some MORE of the news you can use » IGMs Press Picks for today (26 July) to help weed thru the noise (some of which can be found over here at Finviz).

RUSSIA GAS CUT to EZ (RTRS HERE) + GM news + WMT= X … still trying to solve for X and so, here are a couple things from Global Wall Streets inbox which caught my eyes …

Risk assets have bounced despite bad news, mainly because longer real rates rallied. But the data has worsened again, the Fed is unlikely to sound dovish this week, and we expect a sharp widening in US credit spreads. We turned tactically Neutral on risk last week; we are now back to being Underweight.

Nothing without consequence … and speaking of consequences, Wells attempts to answer ALL the questions on rates traders / investors minds related TO …

The Fed's Balance Sheet: Your Questions Answered In this first installment of a three-part series on the balance sheet of the Federal Reserve, we start by answering some of the more basic questions about the central bank's balance sheet, such as what are its main assets and liabilities and what makes them grow/shrink. In the final two installments of this series, we will use a similar framework to discuss what effects quantitative tightening may have on financial conditions and the real economy as well as whether the Fed's balance sheet will ever return to a “normal” size.

Here’s an excerpt and visual which strikes ME as interesting

… With a chronic excess supply of reserves, the Federal Reserve would not be able to lift the fed funds rate from 0% using its pre-2008 operational framework. So the Federal Reserve solved this problem, which required enabling legislation from Congress, by paying interest to banks on their reserves.5 Because banks were now being paid interest to essentially make a risk-free overnight "loan" to the central bank, they did not have much incentive to loan excess reserves to each other below the rate they could earn from the Fed. When the FOMC wanted to tighten policy, it would raise the interest rate that it paid to banks on their reserves, putting a "floor" under short-term interest rates. Overnight reverse repurchase agreements also helped to put a floor under short-term interest rates by offering some non-bank cash holders, such as money market funds, a guaranteed rate on overnight loans made to the central bank.6 This new operational framework, which can be seen in the following illustration, allowed the Committee to increase the fed funds rate and, by extension, other market-determined short-term interest rates.

Figure 9

Part 1 concludes with classic cliff-hanger,

… In Parts II and III, we turn to a different set of questions. Why should we care about the Fed's balance sheet? What impact do QE and QT have on financial conditions and the real economy? And will the Fed's balance sheet ever return to a “normal” size?

Chart of the Day: As we noted in our recent spotlight, core yields are threatening major tops, which also extends to the US 5yr Bond Yield, which saw two high volume falls on Thursday and Friday. This has sharply increased the risk of a “head and shoulders” top, but only a closing break below 2.73% would confirm. If the top is confirmed, next resistances are seen at 2.57%, then the 38.2% retracement of the entire 2020/22 upmove at 2.30%. In contrast, a hold above 2.73% would keep alive the prospect of further ranging, with a move above 3.21% needed to lessen the risk of a top.

The firm goes on to suggest they will

… turn tactically bullish, expecting a move to resistance at 2.465% initially, whilst support is seen at 3.06%, above which we would turn tactically neutral.

And has recently gotten stopped OUT of short 10s. Finally, she’s baaaaaaaack? Who, you might ask? The Widowmaker, Bloomberg asks overnight

Could the Widowmaker have claimed a fresh round of victims? Betting against the Japanese bond market has long been an attractive on paper, but ultimately losing trade and this year's global debt selloff unearthed a new cohort of funds willing to risk a few yen. But what looked promising a month ago when 10-year yields threatened to climb above the Bank of Japan's 0.25% yield cap now looks like being another loser as they have since reversed the move and gone into a rapid retreat. The current benchmark fell to as low as 0.18% Monday, while the previous one fell below 0.10%, levels that suggest some stop-losses may have been triggered. Meanwhile, 10-year yen swap rates -- which are popular with international funds -- have collapsed from their mid-June highs, suggesting a paring of the most speculative bets against Japan’s bonds amid increased concern about a global recession. Swaps are now around five basis points off the central bank’s 0.25% line in the sand, having been more than double the yield at their peak last month.

From The (original) Widowmaker to earnings … an idea of what should be sent out to investors with quarterly reports and statements …

Good stuff Steve! Thank you for your insights