Good morning … today’s dance card is highlighted by $70bb 5yr USTsand so …

5yy DAILY:

momentum (stochastics) is bearish and ahead of this afternoons supply, a concession might NOT be a bad thing and finally, would note that the middle of this years range (5.00 - 3.75) appears to ME to be just about 4.375% and so … a level to buy / cover?

#Got5s?

… these developments come fresh on heels of some data (allowing one / all to see whatever they wanna see ) …

ZH: US Home Prices Hit New Record High, But YoY Appreciation Slows... ZH: Conference Board Confidence 'Hope' Hovers Near Decade-Lows ZH: Dallas Fed Respondents Blast "Poor National Leadership" As Stagflation 'Erodes Business Confidence'

… which then set the table for the 2yr auction …

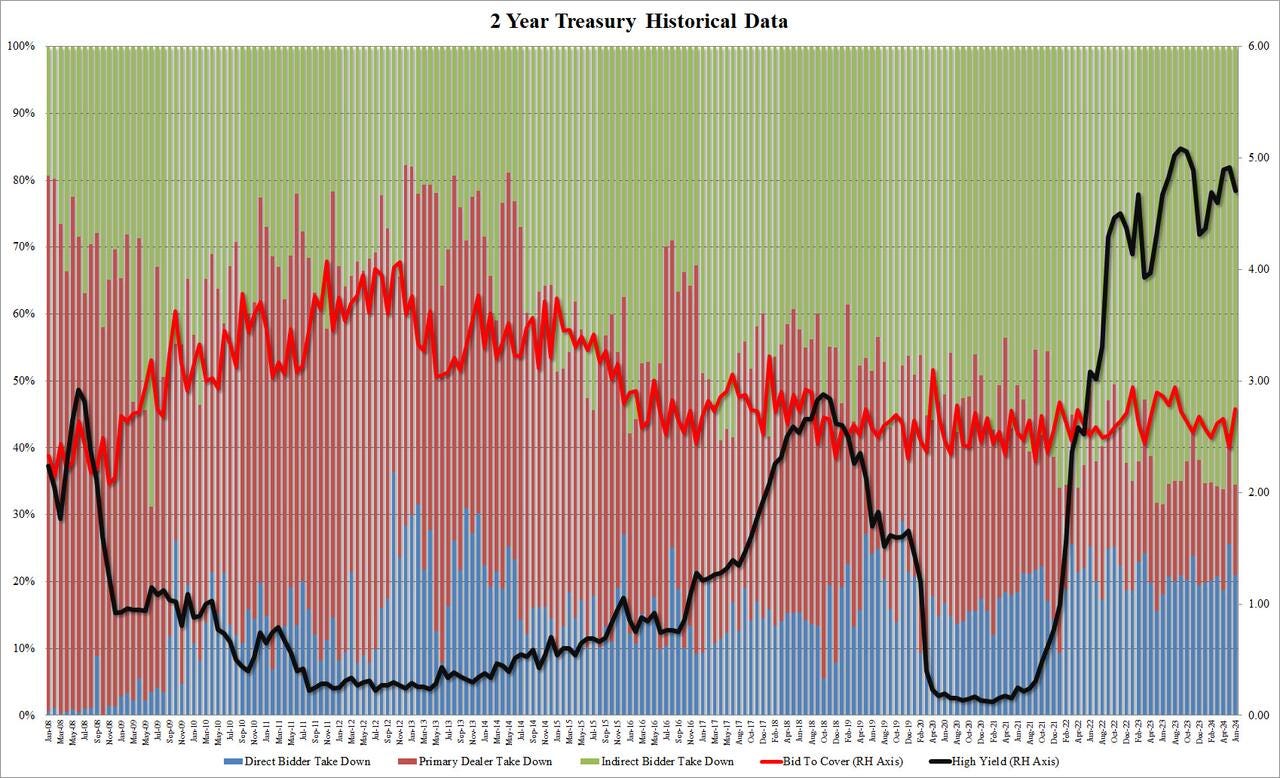

ZH: Solid 2Y Auction Stops 'On The Screws', Highest Bid To Cover In A Year (red line)

… The bid to cover jumped from last month's 2.406% (which was the lowest since Nov 2021) to 2.751%, well above the six-auction average of 2.57% and the highest since last July…

AND with that in mind (#Got5s?), here is a snapshot OF USTs as of 630a:

… and for some MORE of the news you might be able to use…

NEWSQUAWK: US Market Open: USD/JPY breached 160.00; US equity futures firmer awaiting MU after-hours … USTs also have a thin docket ahead with no Fed speak due and the main highlight being the 5yr auction, a tap which follows a better-than-average 2yr sale; USTs at a 110-09 fresh WTD base and holding just above last week's 110-06+ low.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ …

BARCAP: April house prices continue to climb higher (hmmm … a rate CUT might not be ‘position A’ for at least this sector of the economy … depending then on the multiplier of said CUT … this could really be funTERtaining…?)

The FHFA and S&P CoreLogic CS 20-City indexes increased in April, growing 0.2% and 0.38% m/m, respectively. Both indexes continue to show annual growth albeit at a slightly slower rate than the prior month.

BARCAP: June consumer confidence declines on more pessimistic expectations

The Conference Board's index of consumer confidence declined to 100.4 in June, on a weaker assessment of future economic conditions, while the assessment of the present situation slightly increased. This comes after a slightly more optimistic view in the May report.

DB: Early Morning Reid (lifting description of US RATES action yest)

…US Treasuries are also edging up around +1.5bps across the board after the Aussie CPI print after rising yesterday on the Canadian CPI beat. By last night’s close, 2yr Treasury yields were up +1.7bps to 4.74%, and the 10yr yield was up +1.6bps to 4.25%. Treasury yields did come slightly off their intra-day high seen around the European close following a solid 2yr auction which saw the highest bid-to-cover ratio since September. There was also some hawkish Fedspeak though, with Governor Bowman warning that “we are still not yet at the point where it is appropriate to lower the policy rate.” In addition, she said that cutting rates “too soon or too quickly could result in a rebound of inflation, requiring further future policy rate increases to return inflation to 2 percent over the longer run.” Meanwhile, Fed Governor Cook maintained patience on rate cut prospects, saying these will be appropriate “at some point”…

Fed rate path: first cut in Dec; 175bp of total easing through 2026

Neutral rate: 3.5-3.75% nominal; well above the Fed and consensus

QT: to continue until reserves near ample in 2025q2

Term premia: too low; tradable

Forecast/trades:

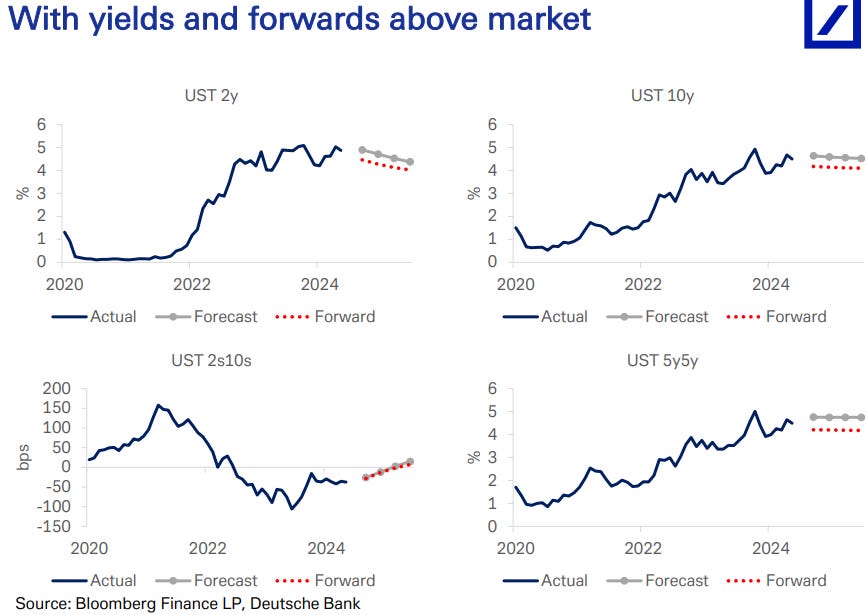

Duration – forecast (modal) is moderately bearish; year-end 10y UST at 4.6%

Curve – long term premium and far-forward steepeners (e.g., 2y3y-5y5y)

Inflation – long 5y5y inflation swaps

MS: Global Macro Strategy: June Index Extensions (Fri, 4pm, be there or be square)

Eurogovies extend by 0.047y, lower than avg; USTs 0.043y, lower than avg; UKTs 0.206y, higher than average; eurolinkers to extend by 0.009y, lower than avg; TIPS and UKTis to contract.

… We expect the 1y+ UST index to extend by ~0.043y, compared to an average June (0.076y) and an average month (0.09y) – Exhibit 8 . A total of about US$315 billion of supply (offered amount) will affect the extension, and US$173 billion market value of bonds will fall out of the index. The monthly issuance of 2y, 3y, 5y, 7y, 10y, 20y and 30y will affect the respective maturity-wise indices.

Wells Fargo: June Consumer Doesn't Say Much With Confidence

Summary Consumer Confidence edged modestly lower in June, keeping the index within its narrow recent range. The details continue to demonstrate a hesitant, but not overly concerned, consumer.

… And from Global Wall Street inbox TO the WWW,

ABNAmro: Global Monthly - Five themes to watch over the summer | Insights newsletter

As we approach the summer holiday period, we preview five major themes to watch

We start with the repricing of central bank rate cuts, which we think has further to run. This will likely be helped along by our second theme – the US economic slowdown

We also preview upcoming elections, explore the drivers of the recent rise in shipping freight tariffs, and finally, we flag the potential for eurozone services activity to see a boost from summer cultural events

As is customary in summer, we will take a break in July, resuming publication in late August

Regional updates: The ECB is waiting to gain further confidence in the eurozone inflation outlook, while in the Netherlands, tax cuts and rising real incomes are expected to support consumption

In the US, disinflation and a weaker labour market are strengthening the case for rate cuts

Proposed EU tariffs on China’s EV exports could yet be watered down

ABNAmro: US - The tide is turning | Insights newsletter

The US disinflationary process has resumed with a bang. There are increasing signs of weakness in the labor market, raising the likelihood of a Fed rate cut in September.

Bloomberg: Bond Traders Boldly Bet on 300 Basis Points of Fed Cuts by March (it’s getting to the point that whenever EBB writes you gotta slow down and absorb the description of price action intertwined with narratives as he illustrates just how those out there are putting their money where their mouths are …)

Standout play in options targets policy rate as low as 2.25%

Fed officials forecast just one quarter-point cut this year

Traders in the US rates options market are embracing a nascent wager on the Federal Reserve’s interest-rate path: a whopping 3 percentage points worth of cuts in the next nine months.

Over the past three sessions, positioning in the options market linked to the Secured Overnight Financing Rate shows an increase in bets that stand to benefit if the central bank reduces its key rate to as low as 2.25% by the first quarter of 2025.

Such an outcome — which appears unlikely unless the US economy tumbles into a sudden recession — would mean at least 300 basis points of easing from current levels. This type of wager could be used to hedge another investment.

It’s an aggressive position given that market participants are pricing in some 75 basis points of easing in that period. Fed officials recently forecast just 25 basis points of reductions by the end of this year and a total of 125 basis points by end-2025…

Bloomberg: Fed’s Bowman Warns of Upside Risks to Inflation, Not Time to Cut (VOTER)

Flagged risks of immigration policy on labor market, rents

Bowman outlines why Fed was slow to hike rates post-Covid

Bloomberg: Fed’s Cook Says Rate Cut Needed at Some Point But Timing Unclear (VOTER)

Inflation expected to slow more sharply next year, Cook says

Official says policy moves will depend on how economy evolves

MarketWatch: Why inflation could take several years to get back to 2%

‘Left to its own devices without shocks, how fast does inflation move to 2%?’ Cleveland Fed economist Randal Verbrugge asks. ‘Not very fast.’

… AND before signing off, here’s a live look in at those driving the 300bps of CUTS bus, so to speak …

Would love to read/hear Bowman's rational for lagged rate hiking by the Fed. I'd vote Denial, Delusion, and Dishonesty. Good thing I'm no voter right :) or else I might be Sleeping w/the fishes at the bottom of the Hudson

Would love to read/hear Bowman's rational for lagged rate hiking by the Fed. I'd vote Denial, Delusion, and Dishonesty. Good thing I'm no voter right :) or else I might be Sleeping w/the fishes at the bottom of the Hudson