while WE slept: FI contained, Gilts hit on data, EGBs & USTs attempt to move higher; ReSale's TALL Tales; 10yy WEEKLY near support (will shorts cover?); ample reserve regime ... and the curve

Good morning … sorry for missing a day (or your welcome :)) … I had to attend some meetings in NYC ... don’t miss it, gotta say.

A couple / few things which I missed and caught my attention overnight (and then yesterday) …

ZH: China Macro Data Dump "Unexpectedly" Beats Across The Board

WolfST: Landing Cancelled? Retail Sales Jump, Prior Months Revised Up, Boost Atlanta Fed GDPNow to +3.4% Inflation-Adjusted GDP Growth

This demand growth is adding to renewed inflation concerns. The huge waves of immigrants in 2022-2024 are part of this demand growth.

ZH: Retail Sales 'Reality Check': This Was The Biggest Positive September Seasonal-Adjustment Ever!

… so while the headline certainly might fool innocent bystanders (ahem, I’m now clearly in this group), it would appear the bond market was also fooled — please don’t fault me for attempting to garner signal over the noise from the charts like this …

10yy WEEKLY: support in / around 4.10% - 4.20% is near …

… momentum would suggest there’s still somewhat more upwards adjustment to come and begs the question if / when shorts will cover and / or others might very well buy the dip …

… Time will tell but speaking of shorts … Druck confirmed he is short bonds on the day the Fed CUT rates (BBG interview). For reference, here’s a story on topic …

MarketWatch: Stanley Druckenmiller says he’s shorting U.S. bonds and staying out of China

AND … here is a snapshot OF USTs as of 651a:

… and for some MORE of the news you might be able to use…

NEWSQUAWK: Chinese sentiment lifted overnight whilst European markets are tentative and choppy thus far … Fixed benchmarks relatively contained, Gilts initially hit on data while EGBs & USTs attempt to move higher … USTs are in-fitting with EGBs/Gilts, pivoting the unchanged mark in a slim range into data and Fed speak. Yields are mixed but with overall action modest as the curve steepens a touch.

Reuters Morning Bid: Trump trades shine, China data darkens … So-called Trump trades focus on those parts of the global economy likely to feel the force of tariff hikes, deregulation, and bigger deficits. The Mexican peso , for example, is down 4% from its September high as investors fret about tariffs. Shares in Trump Media & Technology Group (DJT.O) …

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ …

First up a bit of GOOD news (unless yer Team Rate CUT) …

BARCAP: September retail sales: Plenty of momentum entering Q4

Retail sales surprised with a broad-based 0.4% m/m gain, including a robust gain in the control group. Today's estimates position PCE for an increase in the vicinity of 3.5% q/q saar in Q3, and imply very solid carryover for Q4. The FOMC will likely see this as another indication that downside risks have been exaggerated.

… IF you wanna focus on the negatives and so, rate CUTS …

Industrial production fell 0.3% in September on the heels of a downgraded August print, reflecting declines in the manufacturing and mining components. However, disruptions from Hurricane Helene and the Boeing strike are plainly evident, and more than explain these declines.

… undeniably weak, to be sure … A brief departure from weak (IP) to more of a CHOP …

BARCAP: U.S. Equity Strategy: Food for Thought: A Choppy Month for Stocks?

October typically brings larger SPX drawdowns than other months; while elections loom, our Derivatives Strategists' analysis of election years vs. non-election years indicates that seasonality is still the bigger concern; with 3Q24 earnings kicking into high gear, equities could be choppy over next few weeks.

what is NOT so weak is front-end of the bond market … and the amount reserves …

BNP: Front-end center: Money fund backdrop into ample-reserves regime

KEY MESSAGES

Money market fund assets under management continue to rise thanks to elevated short-term interest rates, while weighted average maturities have come down due to T-bill paydowns and Fed uncertainty.

Our baseline is for inflows to continue at a similar pace as seen so far in 2024, while funds progressively extend duration due to positive T-bill issuance and a gradual Fed cutting cycle.

As overnight funding rates face upward pressure and volatility, we continue to see money market funds acting as a meaningful backstop to elevated Treasury supply.

Assets under management (AUM) for MMFs continue to breach record highs: Back in February, we published our second "Frontend Center" where we looked into the drivers behind money market fund (MMF) flows and average maturities (see Front-end Center: Money fund assets and WAM outlook, dated 22 February). Our expectation was for money fund inflows to continue at a slower pace than 2023. For assets under management (AUM), money funds drew in USD1.15trn in 2023, while year-to-date in 2024 inflows have totaled USD588bn as of 9 October. Inflows likely continued as interest payments to investors remain high and the yield curve (i.e. 10y – 3m or 2y – 3m) was unlikely to turn positive. But inflows have been slower than last year, mainly because of the absence of a deposit run experienced during the regional banking turmoil in March 2023, which made MMFs the product of choice for cash investors. Deposits have since recovered and continue to grow at a decent pace. H8 Fed data show bank deposits have grown USD406bn so far this year (as of 2 October) versus USD299bn in deposit outflows in 2023…

… from a French view of the front-end view to a German view of rate cuts / pricing in wake of the good / bad news yesterday …

… In terms of near-term Fed expectations, futures are now only pricing in 84bps of cuts by the March 2025 meeting, down -4.9bps from the previous day. That’s equivalent to 3.3 cuts at the upcoming four meetings, so market pricing suggests it’s more likely than not that the Fed will pause their cuts for at least one meeting over the next six months. And with investors dialling back the likelihood of rate cuts, Treasury yields moved significantly higher, with the 10yr yield up +7.8bps on the day to 4.09%. Higher yields saw the dollar index (+0.23%) rise for the 12th time in 14 sessions, to its highest level since August 1 …

Consumers may be feeling less confident on the economic outlook amidst job worries, but for now are happy to continue spending. Financial pressures are building for many households, but strength in consumption from those at the top of the income spectrum is more than offsetting that story. This suggests the Fed will tread carefully with 25bp cuts

Retail sales rose 0.4% (consensus +0.3%, Morgan Stanley +0.1%) and control group sales increased 0.7% (consensus +0.3%, Morgan Stanley +0.1%), well above our forecasts. Revisions were small but slightly positive for both headline and control. The strong data raise our 3Q real consumption growth tracking to 3.6%a.r. from 3.1% previously and 3Q GDP to 2¾% from 2.5% previously.

Real spending is now trending in-line with last year, at an estimated 2.8%a.r. year-to-date through September. Real spending has been strong in both goods and services, with goods rebounding in 3Q. Real goods spending is trending at a 2.6% year to date pace, with 3Q at 6.1%a.r. Real services spending is trending at a 2.9% year to date pace, with 3Q at 2.5%a.r.

On a monthly basis, we are tracking real consumption growth up 0.4%.

In today's retail report, the strength was widespread. Restaurant spending increased 1.1%M. Recent months had suggested softening but were revised up and no longer suggest a slowdown.

Back to school categories - including electronics, clothing stores, shoe stores, sporting goods stores, book stores, and general merchandise stores - rebounded, coming in at +0.5%M in September versus -0.5%M in August.

Storefront sales showed more strength this month compared to online. Online was up +0.4%M in September after a strong August. Miscellaneous stores and health and personal care stores contributed to the strength in control.

Furniture and gas both fell for a second month. Building materials showed only a slight increase; hurricane effects could raise October retail sales more.

Consumer spending is strong, and somewhat stronger than we knew. We continue to expect that the Fed will cut in a string of 25bp moves. September payrolls rebounded, keeping labor income growth solid, and household purchasing power is further helped by disinflation…

… and while dated, this note caught my attention …

NatWEST: JPY investor flows: Significant buyers of US sovereign bonds in August

… Japanese investors bought US sovereign bonds in large quantity, the highest since March 2020. They bought €34.6bn of US sovereign long-term bonds in August, remaining buyers for a second consecutive month. JPY investors may have grabbed US sovereign bonds over August given expectations for significant Fed easing at the time. On an FX-hedged basis JGBs are still more attractive than USTs, Gilts and Euro Area bonds. A rise in domestic yields will likely keep more Japanese investment at home in our view …

… and a view of the US … I mean GLOBAL … consumer, from the UK POV …

US data once again reminded investors of the wisdom of never underestimating the hedonism of the US consumer. September retail sales were strong (the data do include the effect of inflation). Consumers are often disbelieving of the data, but the value of US retail sales are up over 25% from the start of 2021 while goods inflation is up a little more than 17% over the same period. That suggests a rising living standard, at least when measured by material possessions.

The picture in China is more complicated. There were several data items today; and if one believes the official numbers, economic growth slowed a little during the third quarter. Official retail sales were stronger (as with the US, these figures include the effects of inflation). There was a spike in sales of home appliances, but food prices may have been more important in raising the value of retail sales.

UK retail sales lie ahead of us. These numbers do not include inflation, and the volume of goods sold suggest a solid growth in consumption by UK households. A growing population, being paid more money, provides a basis for this growth.

Japan’s September consumer price inflation slowed with lower energy prices. Excluding energy, inflation rates were more stable.

… more on ReSale TALES and IP in case you hadn’t had yer fill …

Wells Fargo: Retail Sales Post Broad Advance in September

Summary Despite worries about the financial health of the consumer and potential weakening in the labor market, U.S. retailers had a solid month in September. Control group sales rose more than twice the expected amount, pointing to stronger Q3 consumer spending.

Wells Fargo: Industrial Production Whiffs in September, Down for Q3 as a Whole

Summary Industrial production fell in September as capacity utilization dropped to a three-year low. There were mitigating factors at play, but it is emblematic of the dire straits in the manufacturing sector today that one-off factors can derail output rather than just slow it.

… finally, in case you thought I missed the theme of yesterday …

Today, the Atlanta Fed's GDPNow tracking model raised Q3's real GDP growth rate from 3.2% to 3.4% (saar) following a roaring September retail sales report (chart). Real consumer spending was revised up from 3.3% to 3.6%! Jobless claims fell despite worker strikes and hurricanes. Manufacturing also held up well notwithstanding Boeing layoffs and bad weather.

Today's data further confirm our assessment that the Fed was too dovish when it cut the federal funds rate by 50bps on September 18. We immediately responded by raising the odds of a stock market meltup and forecasting a counterintuitive backup in bond yields. Sure enough: Stocks are climbing to new record highs and the 10-year US Treasury yield is up almost 50bps to 4.10% since September 18.

Here's more on today's economic indicators and developments:…

… And from Global Wall Street inbox TO the WWW,

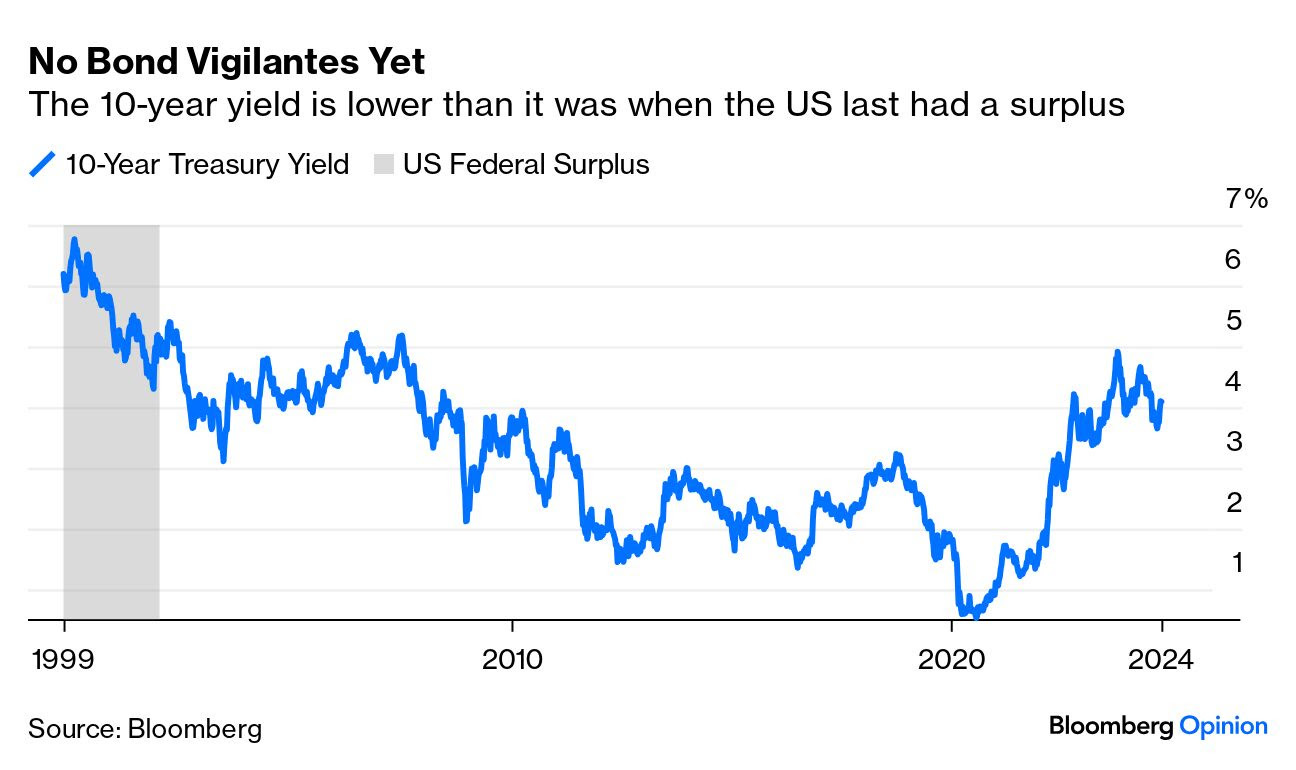

… Authers’ writes on bond vigilantes …

Bloomberg: That snapping sound is euro-inflation's neck Lagarde shows she has a way with triumphal declarations, followed by a celebratory rate cut.

… Should Americans be concerned about this mounting debt? Definitely. Powell, the Federal Reserve chair, describes it as an “adult conversation” that elected officials need to have. Myriad reasons might justify a Clinton-style bipartisan approach. But it might require the intervention of bond vigilantes to make this happen. Incessant borrowing to fill the revenue shortfall should theoretically push up the interest rates that lenders demand. That means higher interest payments for the government (and hence for taxpayers), and also for corporations and individuals. But even if bond yields have been jolted out of their long-term declining trend in recent years, they remain lower than in 2001, when the US had a surplus. The much feared bond buyers’ strike is still not happening:

What explains this? PGIM’s Tom Porcelli argues that the US gets away with such an avalanche in new debt issuance due to what Giscard would have called “exorbitant privilege” — the dollar’s position as the world’s reserve currency:

When you’re the world’s reserve currency, it’s difficult for investors to walk away. That’s the interesting push-pull in this whole debate that’s going on about where yields should be on the back of a fiscal deficit that’s deteriorating.

However, a strong relationship exists between fiscal deficits and inflation, as shown in this study by Michael Bordo and Mickey Levy. All else equal, the researchers concluded that bond-financed fiscal deficits, unbacked by future taxes, may have contributed to inflation. This lends credence to Powell’s calls for fiscal authorities to get their house in order; otherwise, the Fed’s fight could be in vain.

While it’s helpful that lower fed funds rates will reduce the interest burden, savings won’t be great if revenues continue to lag expenditure. The annual net interest costs would total $892 billion in 2024 and almost double over the upcoming decade — rising to $1.7 trillion in 2034 from $1 trillion next year, according to the Congressional Budget Office. This assumes that short-term rates fall to 2.8% — which is contentious given the evidence that the neutral rate of interest is rising. The Peter G. Peterson Foundation notes that should interest rates turn out to be higher than that, costs would rise even faster than in its already alarming projection:

Rising interest bills may not be at the top of voters’ minds compared to the more direct rates they pay for mortgages or auto loans. But more interest expense squeezes out government expenditure in other areas. It will hurt …

…surprise surprise surprise …

LPL: Surprise! Economic Data Has Been Better Than Expected Lately

…Treasury Yields are Higher on Better-Than-Expected Economic Data

…So, what’s next? History shows that without signs of recession, intermediate and longer-term yields tend to drift higher, particularly as the Treasury yield curve further steepens. Our base case remains no recession this year and our year-end target for the 10-year Treasury yield is 3.75%–4.25%. So, while yields may move slightly higher from current levels, we still think we are past peak Treasury yields for this cycle.

But, if the economy, particularly the labor market, cools more than expected or if geopolitical events cause the Fed to accelerate rate cuts more than what is priced in, Treasury yields will likely fall. Historically, fixed income returns have come primarily from the income component, and with income levels still relatively attractive, we think clipping coupons is still an attractive strategy, especially versus cash.

… THAT is all for now and HOPE to have somewhat more over weekend BUT ... Off to the day job…