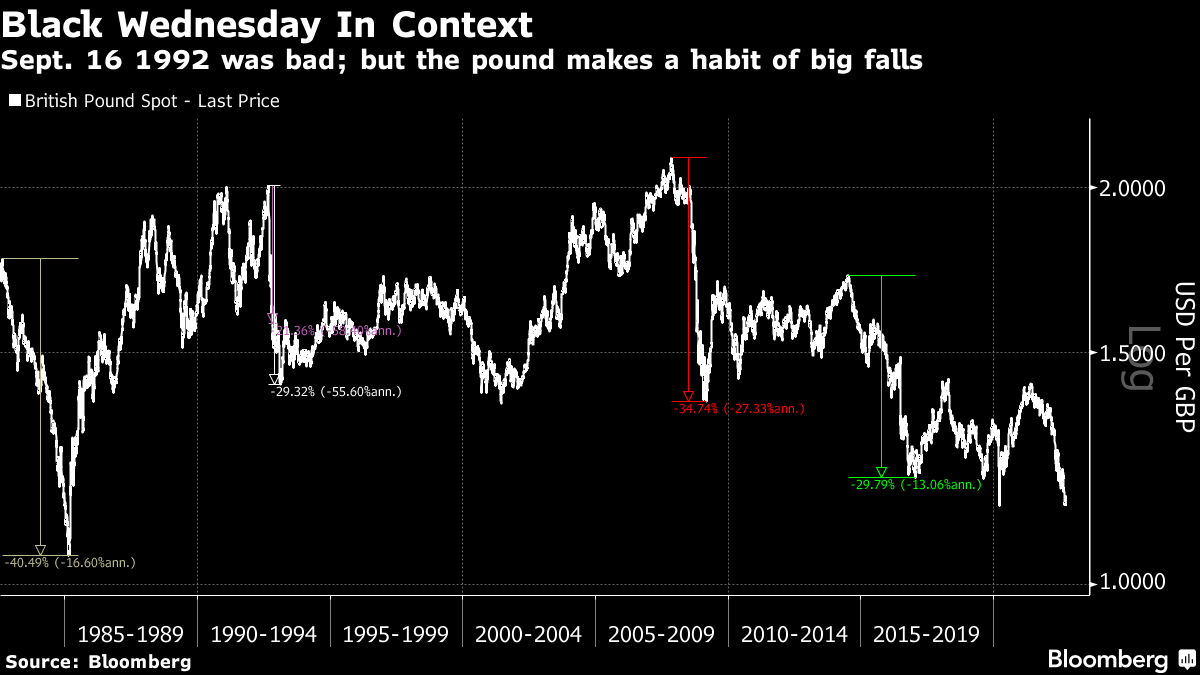

Margaret Thatcher always used to say that “you can’t buck the markets.” Having in 1990 been dragged very much against her will into joining the exchange rate mechanism of the European Monetary System (in which other EU currencies traded in a fixed band around the deutsche mark in what was intended as a precursor to the euro), she appeared to gain vindication 30 years ago today, when the UK government abandoned its attempt to keep the pound within the mechanism and let it float — which in practice meant that it let the currency collapse.

The events of “Black Wednesday” were a classic example of how economic actors can inadvertently display their weakness when they try to show strength. The pound had been overvalued when it entered the mechanism. Then the mark strengthened still further after the Federal Reserve in the US started to cut rates in an attempt to stimulate the economy. That briefly pushed the pound above $2.00, an infeasible level. The chart shows what happened next:

… It doesn’t have to be the government that takes the blame. In 1985, the pound tanked after the Fed raised the fed funds rate to 11.75% late in the previous year. It led to a speculative pile-on that took the pound as close as it has ever been to parity. And the biggest daily fall by far for the pound came on the night of the Brexit referendum in 2016. Black Wednesday saw the first ever fall of more than 4%; the British electorate managed to make it fall by 8%:

What lessons for today? Any intervention in foreign exchange markets must be credible to have any chance of working. And when the Fed takes a course that is out of sync with the rest of the world, stresses increase on the rest of the foreign exchange architecture.

That’s unfortunate because US bond yields are in an upswing again. As of late Thursday trading, 10-year real yields (which offer inflation compensation) had topped 1%. This landmark was last reached for a few weeks in late 2018, and helped to precipitate a stock selloff and a “pivot” toward easy money by the Fed. That seems very, very unlikely in the immediate future. Before 2018, real yields had been below 1% uninterruptedly for seven years:

And John continues, eventually turning TO the JPY …

But first, BEFORE we get TO the weekend … a few items from ZH and it’s hard NOT to begin here

In a surprise pre-announcement, FedEx said it’s withdrawing its fiscal year 2023 earnings forecast as a result of the preliminary 1Q financial performance and expectations for a continued volatile operating environment.

First quarter results were adversely impacted by global volume softness that accelerated in the final weeks of the quarter. FedEx Express results were particularly impacted by macroeconomic weakness in Asia and service challenges in Europe, leading to a revenue shortfall in this segment of approximately $500 million relative to company forecasts. FedEx Ground revenue was approximately $300 million below company forecasts.

Specifically for Q1:

FedEx prelim 1Q adj EPS $3.44, est. $5.10

FedEx prelim 1Q Rev. $23.2B, est. $23.54B

FedEx prelim 1Q Adj. oper income $1.23B, est. $1.74B

As a result of the preliminary first quarter financial performance and expectations for a continued volatile operating environment, FedEx is withdrawing its fiscal year 2023 earnings forecast provided on June 23, 2022…

… HEREis what another shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are modestly bear-flattening, outperforming weaker EGBs on hawkish ECB comments and a firmed-up data slate overnight in China (AUG IP +4.2%YoY vs +3.8%YoY exp). There was a 5k FV seller in early London hours alongside more listed FV downside going through (on the back of the trend in SOFR listed downside y’day, chart attached). Volumes are running at a healthy 110% clip for a Friday morning, 2s flirting with 3.90% as we speak. Risk-parity underperformance is continuing, SPX futures showing -31pts here at 7am, while the DAX is -1.4% on the session. Oil is a bit firmer at +0.6%, but the rest of the commodity complex is weaker (BCOM -0.6%, NG -2.3%, XAG -0.9%, HG -1.5%). The 2s10s curve is further inverting as well, -2bps to -44bps (cycle lows at -56bps). Flow-wise, our desk in London noted screens heavily biased to client sales, while there was some fingerprints of CB sales involved (to defend FX?). OFTRs were noted as 'well-behaved', but liquidity in OTR has certainly deteriorated in recent days.

… and for some MORE of the news you can use » IGMs Press Picks for today (16Sep) to help weed thru the noise (some of which can be found over here at Finviz).

Now as strategists / economists alike playing pin the tail on the forecast, Global Wall Street has offered couple of ‘insights’ which may be of interest SO I’ll pass them right along.

First up, a rather large German bank offering ITS guess as to where terminal rate will be (so, price 2s through bonds accordingly)

… Both approaches – comparing the nominal fed funds rate to inflation and a suite of common policy rules – suggest that a fed funds rate at or above 4.5% is likely to be required by early next year. Accounting for risk management considerations, a rate near 5% is more likely to be appropriate, an outcome that our colleagues flagged earlier this year (see "What's in the tails?: Why the coming recession will be worse than expected" ). As such, we now expect the Fed's policy rate to peak at 4.9% in Q1 2023. Despite the recent jump in market pricing for the fed funds rate, this analysis therefore points to further upside risk to terminal rate expectations.

The ultimate path for the Fed will be determined primarily by the evolution of inflation and financial conditions. Continued upside surprises in the former could lead to a peak fed funds rate exceeding 5%, particularly if it occurs in conjunction with easier financial conditions and a persistently tight labor market. Conversely, a faster decline in inflation coupled with tighter financial conditions and some loosening in the labor market, could beget a terminal rate closer to 4%. At this point, we see risks skewed in the hawkish direction….

Where then will 2yy be? Step right up and place your bets … SOME have already, based on YESTERDAYShit where rate CUTS remain priced … and SOME have suggested 2yy MAY BE heading up NORTH of 4% …

Speaking of things being NORTH of 4%, another update which will likely be the talk ‘round the water coolers today comes from Goldilocks,

G10 sovereign yields have continued to reprice higher following an historic first half of the year as inflation appears slow to normalize. Given this backdrop and substantial revisions to our economists’ terminal rates projections, we now project 10y USTs, Bunds and Gilts will end the year at 3.75%, 2%, and 3.5%, and see these yields peaking next year at 4%, 2.25%, and 4% respectively

… Our longer maturity forecast changes reflect not only revisions to our expectations for the terminal rate, but also an anticipation that investors will update their priors on “long run” or neutral rates … we note that market pricing is roughly aligned with our Fed policy rate baseline through year-end, though 10y USTs are only modestly above our previous 3.3% year-end target. Nonetheless, as we noted in a recent report, we expect higher longer maturity yields as well. This upward pressure will come from a few sources. First, investors appear to be placing material odds on scenarios that involve significant easing from the peak, to a degree that is incongruent with Fed commentary given current inflation pricing … despite a long period of elevated inflation, medium term expectations in the US remain anchored, which means the Fed is less likely to want to engineer a deeply inverted (and restrictive) real yield curve as it did in the early 1980s, a period when yield curves were substantially more inverted.

And from the CHARTS department and the basement of Kimble & Co comes a hopeful and optimistic / useful reminder of one (more)thing to watch

10yr US Bond Yields are approaching their 3.50% prior 2022 high, however we would not chase a breakout beyond here.

… 10yr US Bond Yields have continued to edge higher over the past week, helped by the strong beat in CPI earlier this week. The market is now very close to the 3.50% highs, however we would certainly not chase weakness beyond here, as our broader medium-term view remains unchanged that the market is set to stay trapped in a broad mean-reverting phase. If the market breaks above 3.50%, this is likely to trigger an initial short-term burst higher as momentum players chase the move and/or investors step out of long positioning, with first minor support at 3.62% (then 3.77% at a real stretch). However, such a break is highly likely to set up a large weekly momentum divergence on both weekly RSI and MACD, which has characterized 4 out of the previous 5 major peaks in yields. Therefore, we believe a breakout is highly unlikely to lead to another sustained trending phase higher in yields and our attention would instead turn to any signs of exhaustion in order to turn bullish…

And as one shop reads the inkblot and sees it one way, another (techAmentalist) would look at very same yield and note 10yy are pushing higher, and say its only a matter of time until …

US10YR: Is trading higher and approaching horizontal resistance at 3.50% (2022 high). The US2YR, 5YR, & 30YR have all set new highs for 2022, suggesting that it is only a matter of time before the US10YR breaches 3.50%. Resistance to watch above there is 3.77% (2011 high).

But these words and visuals from the pros aside, you don’t really need to listen to anyone — not ME or the pros — other than those who call themselves the allstars of charting, right?

Higher rates mean downside pressure for long-duration assets in general, not just bonds. This also includes growth stocks!

Check out the chart of the US T-Bond ETF $TLT overlaid with the growth vs. value ratio:

… It’s possible. These fresh lows for bonds not only suggest further underperformance for growth stocks but also continued weakness on absolute terms. If this key ratio undercuts its May lows, it’s probably because the weakest names are leading the market lower.

The Ark Innovation ETF $ARKK is an excellent example. Here’s a chart overlaying it with TLT:

In other words, bonds matter … and as a former card carrying member of the RATES world, I can verify that bond jockeys remain to this day to be some of the smarter ones in the room. And most of them don’t refer to themselves as allstars (even though, they truly are).

For more, refer TO ZH HERE for words / thoughts / BUY BONDS ideas from the likes of Gundlach. Please head there, read / listen to / watch GUNDLACH and then race out to BUY USTs because, as this weekly newsletter from BBG highlights, UST liquidity remains impaired and even The BeachBoys want YOU to trade with them.

The weekly fix: an unlikely trio; Pimco wants to trade with you

… “We would like the entire Treasury market to move to all-to-all trading -- a platform where asset managers, dealers, and non-bank liquidity providers are able to trade on a level playing field, with equal access to information,” wrote Pimco’s Libby Cantrill, Tim Crowley, Jerry Woytash, Jerome Schneider and Rick Chan. “The vast majority of the bond market, including most parts of the Treasury market, liquidity remains intermediated, making the market more fragile, less liquid, and more susceptible to shocks.”

I really HATE whoever / however it is that PIMCO has become a proper name. It’s an abbreviation of a firm and so I realize it’s just me, but it bothers me that nobody capitalizes the entire abbreviation … Be that as it may, go and TRADE USTs (even with PIMCO)

I’m done venting and so, THAT is all for now. Off to the day job…unsure about weekend post given football related travel schedule …