while WE slept: equity futures lower, bonds BID; #2025 dart-throwing exercise continues (BAML rates); "Option Traders Bet on Deep Treasury-Market Selloff Within Weeks"

First up and ahead of holiday shortened end of the week (defacto 4d weekend coming up — unsure as to ‘production schedule’ here’), I’ll lead with a look at today’s upcoming supply of $44bb 7yr notes …

7yy DAILY: middle of the (4.40 - 4.00%) range …

… with momentum (red circle) moving into overBOUGHT territory, not an ideal setup or concession …

… and so, before asking one / all to get those bids in early and often, I suppose the better question buyers may be contemplating is what, if any OTHER signals to be had might suggest DJT2.0 tariffs aren’t inflationary … on THAT note …

5y5y forward inflation expectation:

… somewhat more just below BUT does this speak TO December rate CUT and is Santa Pause being shown the door?

… AND back to here and now AND in as far as what, if anything one might like to infer from yesterday’s 5yr auction, well …

ZH: Solid 5Y Auction Sees Highest Direct Bid In A Decade

… a strong bid wasn’t enough as the market reflexed a touch lower and, as best in the biz put it, the bout of bond bearishness attributable TO DJTs recently announced tarrifs …

BMO RIP RRP Usage?: The Treasury market cheapened on Tuesday in a move that was consistent with the gains in Consumer Confidence and the strongest Labor Differential (jobs plentiful minus jobs hard to get) in five months. However, the durability of the bearishness was attributed to Trump’s social media posts regarding 10% additional tariffs on China and 25% levies on Canada and Mexico. It remains unclear how much of a ‘surprise’ Trump’s announcement was for investors; after all, tariffs were a key aspect of his platform and, therefore, it was a widely-anticipated move during early 2025. It is also worth highlighting that the bearishness was contained within the prevailing range; reinforcing the interpretation that the tariff revelations were well within the scope of expectations. Even the timing of the announcement seems consistent with what the market had anticipated – before Trump takes office which allows the groundwork to be established for an early implementation of the new levies.

The bulk of Tuesday’s data erred on the side of leaving the macro narrative largely unaltered…

… That in mind and in as far as the title of BMO note goes …

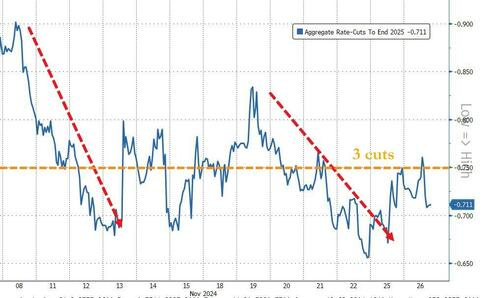

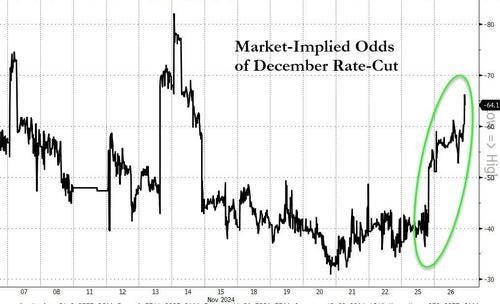

ZH: FOMC Minutes Show "Many" Members Suddenly Favor More Gradual Rate-Cutting-Cycle

… Rate-cut expectations have continued to slide since the last FOMC with less than three full cuts now priced in by the end of 2025...

But, the odds of a December cut have jumped in the last couple of days...

… and with the FOMC meeting minutes known, the day shall go down in history books as follows …

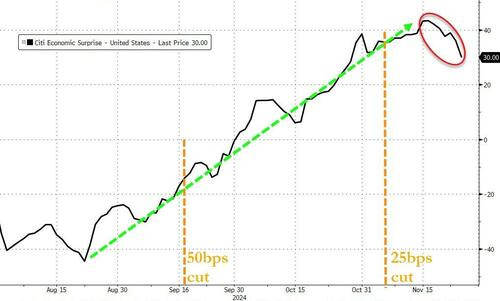

…The day was also dominated by a series of terrible macro data:

Philly Fed Services puked back into contraction,

Case-Shiller home-price growth slowed dramatically (with several cities seeing prices drop MoM),

New Home Sales collapsed (likely driven by the hurricanes but still not pretty), and the

Richmond Fed Manufacturing index disappointed, stuck in contraction.

The only bright sigh was an improvement in consumer confidence post-election (Conference Board).

...interesting that US macro data has suddenly started serially disappointing right after Trump's Red Sweep (after mysteriously surging days after day for the months ahead of the election)...

...and on top of all that the FOMC Minutes showed a suddenly much more hawkish Fed with regards to the rate-cutting cycl but the odds of a December rate-cut are rising...

… here is a snapshot OF USTs as of 655a:

… and for some MORE of the news you might be able to use…

NEWSQUAWK: US futs mostly lower (RTY leads), USD outmuscled by JPY … Fixed benchmarks in the green and towards highs though Bunds were dented by ECB speak, OAT-Bund yield spread at its highest since 2012 … USTs towards their 110-21+ peak, pulled back modestly on Schnabel but only briefly. Docket ahead is packed with PCE the highlight, and will help to inform the view into December’s FOMC, with markets leaning towards a 25bps cut (60% chance) vs unchanged (40% chance) into the releases.

Reuters Morning Bid: Holiday-bound US turns focus to inflation, France tense

Finviz (for everything else I might have overlooked …)

Moving from some of my views and the news to some of THE Global Wall VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ …

First up a note on the relationship (obvious to many) of interest rates and prices and the housing market …

BARCAP: Housing market data imply weakness amid higher mortgage rates and prices

Housing market data today provided a fuller picture of the effects of hurricanes and increased mortgage rates, as October new home sales fell 17.3% m/m. Coupled with increasing house price indexes, this implies overall weakness in the housing market until easier financial conditions persist.

… but never fear, DJT is here …

BARCAP: Consumer confidence increases in November amid broader optimism

The Conference Board's index of consumer confidence increased to 111.7 in November, as the assessments of future economic conditions and the present situation became more optimistic. This comes alongside a 0.3 pp decline in average inflation expectations to 4.9%.

… ok that may NOT have been mentioned but uncanny or coincidental that confidence popped as election has been decided? maybe it is just me or, maybe it’s payback time …

We expect the November employment report to show a 275k job gain, propelled by payback effects from October's Boeing strike and hurricanes. We expect the unemployment rate to be unchanged, to rounding, at 4.1% and hourly earnings to decelerate to +0.2% m/m (3.8% y/y)…

… There are many risks around this report—particularly, the potential for revisions to October's data. The Bureau of Labor Statistics noted a lower than normal response rate to the payroll survey in their October press release, although they did not attribute this to the hurricanes, but to late-arriving responses during the unusually rapid turnover time between the reference week and the report. Due to the nature of this distortion, we do not have a view about the likely direction of revisions, but we do caution that these will be relevant for the FOMC's thinking as it considers whether to pause its cutting cycle in December. In making its determination, the FOMC is likely to look more closely at the 3mma of monthly payroll gains, after accounting for revisions, rather than the magnitude of the incoming November print …

… and with NFP already in mind, this shop does finally talk of POSITIONS, which you know I think matters dearly …

BARCAP: Who Owns What: US takes it all, Europe scorned

Inflows into US equities surged post election and retail frenzy is back. But limited HF/systematic re-grossing leaves dry powder. In contrast, selling of Europe continues unabated. Positioning on exporters/tariff plays/Germany is arguably depressed now. Banks are well owned despite recent outflows.

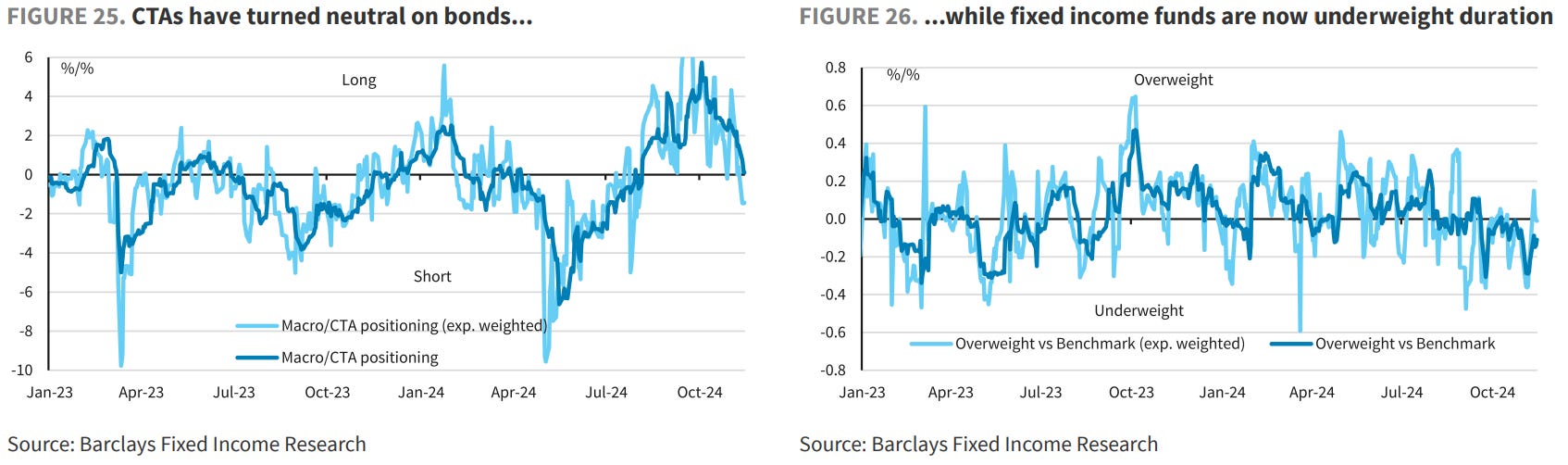

… Of course, bond market jitters will not go away fully until investors digest the ramifications of the policies from the new regime. However, the potential risk to equities from rising rates looks to have eased somewhat, at least for now, with yields stabilising recently. Moreover, fixed income positioning has been cut sharply among both LOs and CTAs. Our fixed income colleagues are now neutral on duration, arguing that US 10y yields are pricing in an appropriate term premium for the uncertain macro backdrop (see US rates: Slowly slowing, Nov 21). So the risk to equity valuations from higher yields should be limited at least until the new administration and its policies are in place, in our view…

… a few words on the front-end of the US curve as it relates TO the US debt limit given the current landscape in DC …

BNP: Front-end center: US debt limit risks under a Republican sweep

KEY MESSAGES

US Treasury will invoke extraordinary measures and limit net debt issuance once the debt ceiling is reinstated on 2 January 2025.

A Republican sweep reduces the risk of debt ceiling brinkmanship, but a resolution by January is unlikely. As a result, typical dynamics related to a debt limit impasse should persist into next spring.

This may see temporary injection of liquidity into the system, and it skews risks to our baseline of the Fed stopping QT to later. However, tailwinds are likely to be marginal as we remain biased to higher funding pressure and cheaper swap spreads.

… AND as the #2025 dart-throwing contest continues, this next one comes from THE bank of the land …

BAML: Global Rates Year Ahead 2025: Continental drift

The View: not all longs are equal We think that 2025 will force investors to differentiate across rate markets. Synchronized cutting cycles are being challenged by diverging fundamentals, US trade policy. We are outright bullish EUR rates and AU cross market versus Japan and short CAD cross market versus US.

Rates: bullish EUR rates, steeper US and UK curves In 2025, we see the 10y at 4.50%, 4.25%, 1.85%, and 1.40% in the UK, US, EA and Japan, respectively. We expect steeper curves in the US and UK. In EUR, the curve call is complicated by potential receiving needs. In Japan, we believe that 2s10s will bear flatten…

…In 2024, UST 10y held a relatively tight range of 3.6-4.7%. In 2025, we expect more of the same, with a 10y rate forecast of 4.25%. Our forecast is built from relatively robust macro projections from our US economists (Exhibit 4, Exhibit 5). Our forecasts slightly overweight downside risks versus the market. In 2025, we expect to trade the 10y range around 4-4.5% tactically and fade large moves in either direction.

Our favorite 2025 year-ahead trades: (1) duration: constructive bias; we favor owning 1y2y risk reversals given asymmetric macro outlook; (2) curve: slow steepening bias in nominal 5s30s; (3) front end: Mar / Sept ’25 SOFR/FF curve flattener; (4) inflation: long 1y4y inflation swap; (5) spreads: short 30y spreads with UST supply / demand risk; (6) vol: 1y fwd 5s30s bear steepeners, 1y10y versus 3m10y payer calendars, 1y1y strangles versus straddles, 6m5y payer ladders and long right-side vega versus intermediate expiries.

…Economics: no landing, rates: > consensus, < forwards…

…Bottom line: our US rate views are bullish versus forwards but bearish versus consensus. Solid US growth outcomes are well priced, in our view, but downside risks / macro uncertainty is not. Core views: own 1y2y risk reversals given asymmetric macro outlook, hold 5s30s steepeners, hold short 30y spreads, hold March / September 2025 SOFR/FF flatteners, own 1y4y inflation, position for higher sustained vol (long forward vol on the right and vol of vol on the left).

…Technicals: diverging 10y yield patterns Conviction in a steeper US 5s30 curve. An uptrend channel, wave III up and oscillators support this. Into year-end 2024, US10y yield is turning lower toward 4.15-4.05% and Bunds 2.10%.

…US 10y yield: We see yield turning lower into year-end 2024 to the 4.15-4.05% area while below 4.50%. While a declining wedge pattern has implied lower toward 3.75-3.50%, the impulsivity of September-November raises risk of a new pattern toward 5% in 1H25.

Down into year-end 2024, then assess if wave Alt (B) up replaces E down

…New trade: Enter US 5s30s steepener We open a 5s30s steepener at 30bps, target 60 and 85bps in 2025 while above 0. Risk to this trade is a loss if the stop is reached (Exhibit 115).

… a large German institution pontificates on the FOMC minutes AND offers some reason for pause (of the equity rally) …

…The FOMC minutes from the November 6-7 meeting showed that committee members thought that “ with inflation continuing to move down sustainably to 2% and the economy remaining near maximum employment, it would likely be appropriate to move gradually toward a more neutral stance of policy over time.” “Many” officials noted that ongoing uncertainty around what the neutral rate should be, "made it appropriate to reduce policy restraint gradually.” That represented an increase after the previous minutes referenced “some” officials. The staff upgraded both growth and inflation forecasts from the prior meeting, this can also be seen from fewer members being concerned with the risk of growth slowing. Last meeting, “most remarked that the downside risks to employment had increased,” but this meeting, “some participants judged that downside risks to economic activity or the labor market had diminished.”

Overall, the minutes gave slightly more credence to a rate cut next month with fed futures now pricing a 63% chance. That’s the most in nearly two weeks. The 2yr yield fell (-3.7bps) into the close from an intraday high of 4.2932% just four minutes before the Fed minutes were released to close -1.2bps lower on the day. 10yr yields were less impacted by the Fed minutes, and finished +3.3bps higher on the day at 4.306% but are back around 4.29% in Asia this morning…

DB: Mapping Markets: 3 factors that could stop the market rally, and almost did

2024 has been a very strong year for risk assets. But whilst markets might look invulnerable right now, it’s worth remembering there’ve been several wobbles this year. It’s just that each time the driver behind the selloff subsided again, whether that was geopolitical tensions, weak data, or inflation risks. Hence, markets recovered quickly and the narrative moved on.

The point is that markets are still vulnerable to several risks – it’s just that none have actually materialized in a significant way this year. For instance, markets slumped in the summer as fears of a US recession mounted, but when the data improved again, they bounced back. Similarly in April, geopolitical tensions and upside inflation surprises helped to drive another selloff. But then tensions eased and the inflation numbers fell back again, so markets recovered then as well.

So given how markets have already reacted to various shocks this year, it’s clear that any one of these factors could drive a fresh selloff, particularly if they became a more persistent and longer-lasting problem. And since valuations are more elevated now relative to the last couple of years, that means on paper, the scope for further gains is now more limited.

Risk #1: An economic downturn…

Risk #2: Mounting geopolitical tensions…

Risk #3: An inflation shock

It feels a long time ago now, but back in Q1 there were growing fears that inflation was becoming more persistent. Indeed, US core CPI came in at +0.4% for three consecutive months, which pushed up the 3m annualised rate of core CPI to +4.5%. Investors pushed out the timing of likely rate cuts from the Fed, and by the end of April the 2yr Treasury yield had closed above 5% again.

Fortunately from a market perspective, inflation subsided again into Q2, paving the way for the Fed to cut rates for the first time of this cycle in September. Other central banks have also started to cut, including the ECB. So there was a strong rally for fixed income over Q3. But if inflation had remained at those higher levels, and not come down again, that would have brought into play the sort of outcomes we saw in 2022, when both equities and bonds sold off together as central banks pursued much more hawkish policy.

This is becoming an increasing risk as we head into 2025. Fortunately, we have avoided the sort of inflation persistence that happened in the 1970s. But in the US, inflation is still above target even now, and our economists forecast that headline and core PCE should remain above 2% throughout 2025 and 2026. Neither have been beneath 2% since early 2021, so if those forecasts are realized, that would mean there was a period where inflation was above target for more than 5 years.

DB: What tariffs on Canada and Mexico could mean for our inflation forecast

On Monday night (Nov 25), President-elect Trump proposed steep tariffs on Canada and Mexico as well as a more modest increase in tariffs on China. Specifically, he said that on the first day of his presidency he would implement a 25% tariff on imported goods from Canada and Mexico and 10% on imports from China.

While the China tariffs are broadly consistent with what we outlined in our latest outlook publication, we have not factored in additional tariffs on Canada and Mexico (see “Trump II: Growth too fast, inflation too furious for Fed cuts”). This piece quantifies the potential impact of the latter if they were to be implemented.

Using the same methods to ballpark the inflation impact of other tariffs in our recent outlook update, we find that adding the tariffs on Canada and Mexico would likely lift core PCE inflation above 3% in 2025, with more marginal effects beyond.

… everyones fav Swiss stratEgerist talking of a gradual FOMC (via minutes) …

The Federal Reserve meeting minutes signalled a gradual series of rate reductions next year (a quarter point each quarter seems reasonable). A December rate cut is also plausible, bringing interest rate reductions in line with the decline in the inflation rate.

US trade representative nominee Greer has supported higher US consumer taxes, but his power in the incoming administration is unclear. US President-elect Trump’s trade tax plans provoked warnings of higher US gasoline prices. The auto sector has also highlighted how often cars cross the Mexico-US border during the manufacturing process. US tech companies are reportedly trying to stockpile components, knowing that they will be liable for any new taxes.

With the US taking tomorrow off to prepare for the Black Friday consumption festival, there is a data dump today. Revised third quarter GDP is unlikely to move markets. October consumer spending and price data are important—inflation-adjusted spending has risen consistently since the end of the pandemic, with the recent focus skewed to services…

… and those in the covered wagons look to confidence with confidence …

Summary After a jolt to consumer confidence in October, consumer moods continued to perk up in November. If history is any guide, confidence may receive a jolt in coming months now that the election is behind us. But just as the economy mattered more for consumers pre-election, the labor market and still-high prices act as an anchor on the moods of consumers.

… and on housing news (blaming Mother Nature) …

Wells Fargo: New Home Sales Fell Sharply in October Hurricanes Mostly Explain the Surprisingly Acute Decline

Summary Elevated Mortgage Rates and Policy Changes Headwinds for Home Builders

New home sales dropped 17.3% to a 610K unit pace during October. A sharp pull-back in sales in the South region suggests recent hurricanes negatively impacted home buying during the month. The bounce in November's NAHB housing market index points to sales bouncing back in coming months as scarce resale supply and pricing incentives from builders continue to support new home demand. A material step-up in sales seems unlikely, however, given the elevated stance of mortgage rates. Although a more friendly regulatory environment could prove beneficial, changes in tariff and immigration policy stand to reintroduce supply chain uncertainty and could potentially constrain new residential construction moving forward.

… And from Global Wall Street inbox TO the WWW …

… Positions matter and nobody details them better than Bolingbroke …

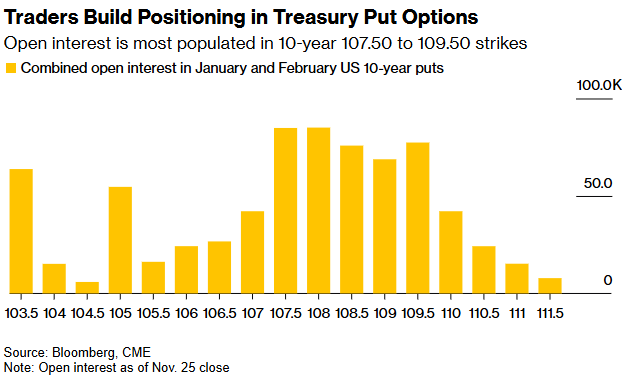

Bloomberg: Option Traders Bet on Deep Treasury-Market Selloff Within Weeks

Bets include 10-year rate possibly eclipsing YTD high of 4.74%

JPMorgan Treasury client short positions rise to most in month

… There has been steady demand for bearish hedges using Treasury-option put structures in January contracts on 10-year notes, which expire Dec. 27. Positioning has also been building over the past couple of days in the February options, which expire Jan. 24, the week of President-elect Donald Trump’s inauguration.

…Open interest, or the amount of outstanding positions held by traders, has been building specifically between the 107.50 and 109.50 put strikes in the January and February options. Those levels target a 10-year yield range of approximately 4.45% to 4.75%, relative to roughly 4.3% now. The upper bound of that span would push the yield above its 2024 high of about 4.74%, touched in April.

On Tuesday, an even more bearish position traded, targeting a yield as high as 4.9%, for a premium of $2.5 million. The benchmark yield hasn’t been that high in more than a year.

The wagers are a reminder that even though yields have surrendered the brunt of their post-election advance, investors are well aware of the potential for the so-called Trump trade to gain traction again. The premise of that trade for months has been that his policies including steeper tariffs would quicken inflation and push yields higher. Treasuries fell modestly on Tuesday, bumping up 10-year yields slightly, after Trump threatened to place additional tariffs on US trade partners.

Along with Trump’s first few day’s in office next month, a couple of other events ahead will be key for these options bets. First off, next week’s report on November job figures is projected to show a big jump in employment from the prior month.

Then there’s the Dec. 18 Federal Reserve policy announcement. Traders see it as a coin toss as far as whether officials will cut interest rates by another quarter-point or stand pat amid signs of economic resilience.

… this next note via Informa strategerist asks a good question … are tariffs disinflationary? and attempts to answer by visual …

President-elect Trump fired the first shot in the tariff war late Monday with threats of a 25% tax on imports from Canada and Mexico if they didn’t help crack down on the flow of immigrants and drugs over their respective borders.

As if on cue, the leaders of both countries responded almost immediately, which means we should expect similar salvos in the weeks ahead as Trump begins exerting US leverage over trade and foreign policies.

The natural reflex in the bond market sees tariffs as inherently inflationary. But that assumes the tariffs are actually implemented, which in the case of Canada and Mex is probably pretty low.

To us, a bigger unknown heading into 2025 is what happens with fiscal policy and the budget.

If Bessent and the DOGE crew are remotely successful in cutting spending, the economy will almost certainly go through a period of withdrawal.

Not only would that outcome be disinflationary, as forward breakevens are beginning to suggest, it may also undercut the case for gold and crypto.

While gold and crypto are too dangerous to short, we are growing more comfortable owning bonds here.

AND in the case I don’t write anything for couple days — yer welcome — wishing you all a happy thanksgiving …

Yes Happy Thanksgiving!

Happy Thanksgiving to all !!!