Good morning, FRED. 10yr TIPS (aka REALZ) up to ZERO POINT ZERO … context

As far as nominals go, with my now somewhat limited capabilities, a monthly of 30yy where I take artistic liberty with the crayon in effort to find a level of interest …

Time at a price OR a retreat in yields — either / both would alleviate what appears to ME to be an oversold bond market.

Meanwhile, the price action of April continued yesterday and then, last night, the Supreme Court draft leak happened. While I’m NOT yet sure exactly how this fits into the global markets landscape, I’m certain it won’t take long until someone out there connects dots.

In the meanwhile, RBA jacked rates 25bp, more than expected and signals more to come, as

The economy has proven to be resilient and inflation has picked up more quickly, and to a higher level, than was expected. There is also evidence that wages growth is picking up”. They will not reinvest proceeds from QE and they are “not currently planning to sell the government bonds that the Bank purchased during the pandemic.

Meanwhile, back here at home, the US FOMC this Wednesday is to begin

Hiking into weakness -Barclays Macro House View Central banks have no choice but to raise rates to tackle inflation, even as threats to growth mount

Central bankers arefacing uncomfortable stagflationary trends. Uncertainty over China's lockdowns and Russian energy supplies to Europe cloud the global growth outlook, while CPI prints remain very high. Policy options are complicated, in many cases. We expect the Fed to lift the funds rate by 50bp (Wed), amid resilient data on activity, and reiterate its intention to raise it "expeditiously" to neutral by the end of the year…

While there will be many impacts OF hikin’ into weakness, Bloomberg helps flesh out visually, one,

… As rough as this year has been for stocks and bonds, there’s a strong chance things will get worse before they get better. Wednesday’s Federal Reserve meeting will be momentous not only because it is all but certain to bring the first half-point rate hike since 2000, but because policy makers are likely to announce plans to trim a $9 trillion balance sheet.

That’s got to be a major worry for investors considering that bonds and stocks shot up on pandemic-era stimulus. Bloomberg Economics estimates major central banks will shed about $410 billion in assets this year. The value of the combined balance sheets of the central banks for the U.S., Europe and Japan has edged down in 2022, but that’s mostly because the Fed-driven dollar spike cut the value of peers’ assets. The outlook is darkening now the Fed is ready to start quantitative tightening.

… here is a snapshot OF USTs as of 710a:

… HEREis what another shop says be behind the price action, you know,

Treasuries are mixed with the curve pivoting flatter around a little changed 5yr benchmark after Australia's RBA kicked off a big week for central banks with a 25bp hike (see above). DXY is lower (-0.2%) while front WTI futures are too (-1.3%). Asian stocks were mixed with China and now Japan out, EU and UK share markets are mixed (SX5E UNCHD, FTSE 100 -0.75%) and ES futures are showing -0.4% here at 6:55am. With much of Asia out we got no overnight flow color and overnight Treasury volume was ~60% of average.

… and for some MORE of the news you can use » IGMs Press Picks for today (2 May) to help weed thru the noise (some of which can be found over here at Finviz).

For somewhat MORE from the inbox, John Authers of BBG

…Tightening Is Already Working Look at broad measures of money in the system, and growth has already plummeted in spectacular fashion. After an extraordinary expansion in 2020, year-on-year changes in both the euro zone and the U.S. are back to normal ranges, though still toward the top. Extreme growth is over, and will continue to slow from here:

Chris Watling of Longview Economics Ltd. in London suggests that falling monetary aggregates in combination with rising rates mean that the steps to crush inflation have already been taken. For him the real question is: “Did Powell and the Fed have their `U.S. Treasury Accord' moment earlier this year when they switched to a hawkish stance and started aggressively to bring money supply growth under control? And, with that, have they already been somewhat successful?” His answer is yes, and he adds:

“Typically, a central bank has two jobs: i) To control the money supply (and therefore inflation); and ii) to act as lender of last resort. The history (of wars, pandemics, and multiple monetary systems) shows that, if the central bank chooses to control inflation, it’s more than capable.”

Meanwhile, a buyers strike noted by BMOs Ben Jeffrey via ZH

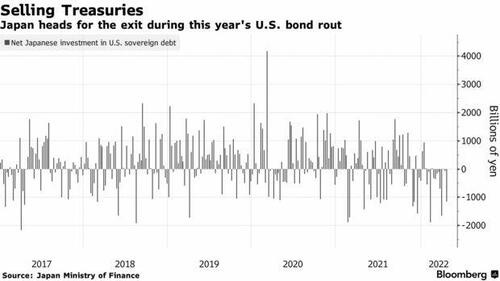

It was about a year ago, when the calendar was moving from the end of the first quarter of 2021 and into the second quarter, when we first observed something unexpected about the single biggest catalyst behind the forceful emergence of the "reflation trade" in the first quarter, which many interpreted as markets pricing in higher long-term inflation and strong growth. Yet in reality as we reported last year, the move which coincided perfectly with the end of Japan's fiscal year on March 31..

... was largely, if not exclusively, a byproduct of Japan's giant pension fund, the GPIF, drastically shifting out of treasuries as it slashed its US Treasury exposure by a record amount.

… Validating our hypothesis that Japan is behind the great Treasury rout for the second year in a row, the latest data from BMO Capital Markets shows the largest overseas holder of Treasuries offloaded almost $60 billion over the past three months! And while that may be small change relative to the Japan’s $1.3 trillion stockpile, its effect is magnified by the near record illiquidity in the Treasury market.

"It’s a significant amount of selling and on par with what we saw in early 2017 from Japan,” said BMO rates strategist Ben Jeffery…