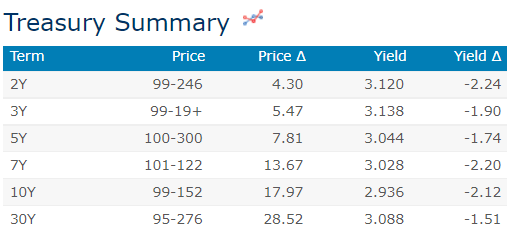

while we slept; China GDP weak; US rates f'cast REVISIONS; cross-asset proxy SAYS (yields gonna drop); 10yy 'threatening a "head and shoulders" top, but...'

Good morning … Here is a visual of 30yy, WEEKLY dating back TO the modern era lows (70bps)

I’d note weekly momentum (stochastics, bottom pane) REMAINS a BULLISH impulse. I’d imagine weaker economic data leading to recession calls (not unlike HIMCo’s latest update) and lower rate foe casts will FOLLOW, not lead, market pricing…

That in mind, here are a few things to consider ahead of this mornings ReSale TALES data and the weekend.

On the heels of overnights China GDP report and economic ‘Rorschach test’ where we’ll all see the data however we want (bad or better than expected), ZH

… HEREis what another shop says be behind the price action, you know,

WHILE YOU SLEPT Treasuries are modestly higher led by intermediates (2s10s30s -1.5bps) after a very quiet overnight session (volumes at 58-62% 30d ave). Flows showed very light receiving in 30y rate, EGBs outperforming in some catch-up to US yesterday. Chinese data overnight proved rather poor, Q2 GDP missing estimates, though June Retail Sales proved a silver-lining. Asia equities underwhelmed (SHCOMP -1.6%, SHPROP -4%, KOSPI +0.4%, NKY +0.5%), while DAX futures are +1.5% here at 6:30am, SPX futures flat. The USD is also mixed with FX generally quiet (EUR +0.2%, CHF +0.4%). Crude is also unmoved, Copper still under quite a bit of pressure -1.7% this morning.

… US news | Fed’s Waller Backs 75 Basis-Point Rate Hike, Says Bigger Move Hangs on Data (Yahoo) Ecommerce Giant Slashing Private-Label Goods Amid Weakening Sales (WSJ) The Recession in Confidence (WSJ)

… and for some MORE of the news you can use » IGMs Press Picks for today (15 July) to help weed thru the noise (some of which can be found over here at Finviz).

Now as the data has evolved over the past few days and rate hikes and cuts are BOTH apparently on the table, Global Wall St has plenty on its mind. Here are a few items which stood out to ME — unfortunately they are mostly about the coming growth slowdown …

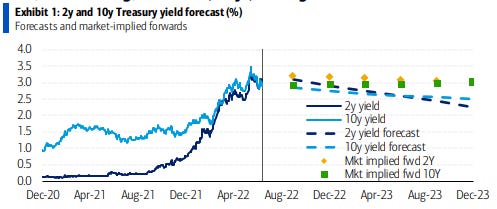

We revise US rate forecasts lower following shift to recession call; 10yT end '22 = 2.75%, end '23 = 2.50%

Our core trade recommendations remain:(1) flatter UST curve, (2) constructive back-end duration, (3) hold LR real curve longs

QT likely to end early with Fed cuts and support wider UST-SOFR spreads; close 2Y UST vs OIS cheapening trade

Wow, thats funny because, you know, when Lacy HUNT says stuff like that — recession and lower yields — he usually gets laughed at or ridden outta town as some sort of village idiot. For more with all the snark b(and without the HIMCo link), ZH HERE.

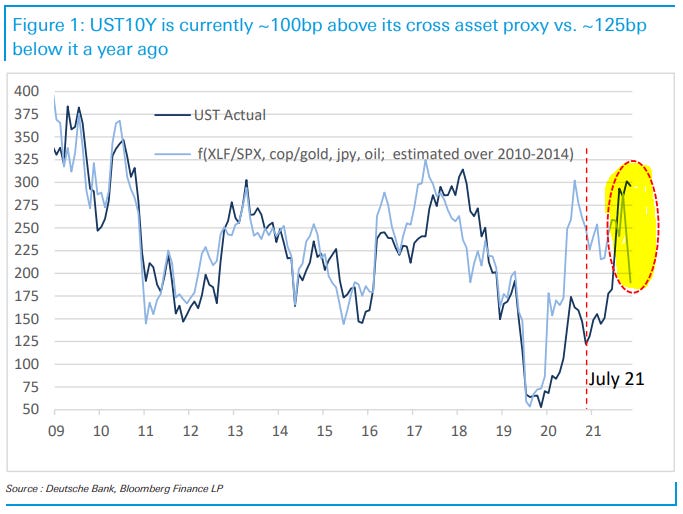

HERE, a large German operation talks about cross market valuations and how 10yy is now ABOVE where it ‘should’ be based on other markets,

Night and day A year ago, after the (seasonal) summer rally, UST10y stood at ~1.25% vs. ~2.50% for our cross asset proxy (financials/S&P 500, copper/gold, the yen and oil). The roles are reversed today, as the cross asset proxy declined to ~2% vs. ~3% for UST10y.

Over the past decade, the cross asset proxy has proven to be a good leading indicator of the subsequent move in UST10y. Will it be right again? As we argued in our recent valuation update, this time may be different. Over the past 25 years, core PCE only briefly and marginally exceeded 2.5%. As a result, slowing growth was a good leading indicator that inflation will soon be below target and that the Fed will ease monetary policy accordingly. This time, core PCE peaked more than 3% above target. Thus, the link between slower growth (as captured by the cross asset proxy) and a dovish Fed pivot may be weaker, or at least delayed.

Hey, if they’ve built the better mousetrap (10yy model) who am I to argue … Perhaps they should go TO Shark Tank with it?

Now to be sure, USAs not the only country about to face cost of living crisis (HIMCo term) as this same large German operation WRITES on Germany,

Moving into recession … A likely further decline in Russian gas supply after the maintenance of NS1 will necessitate additional savings. While we do not expect a full rationing, we believe the economic consequences will together with a US recession and other headwinds push Germany into a recession in H2 2022. Given that prospects for Russian gas deliveries have darkened since February, this energy shock will not hit Germany by surprise or unprepared. Hence, we expect a modest but rather drawn-out GDP decline, as the economy gradually adjusts. After a 1 ¼% expansion in 2022, we forecast German GDP will shrink by around 1% in 2023, largely because consumers will not be able to offset the real income loss by further dissaving. In a “tap remains turned off” scenario, we expect a rationing of gas leading to a GDP slump between 5% and 6% in 2023.

MSs Seth Carpenter on a global aspect of this recovery,

Global Tourism: A Slow and Uneven Recovery. The Covid-19 pandemic led to a collapse in global tourism. Since then, activity has recovered in some regions, but has lagged in others. As travel restrictions are lifted and travel picks up, the recovery is poised to slow amid high inflation and lower consumer confidence.

And with all the slowdown, recession and lowered rates f’casts in mind, HERE is something from the CHARTS department and 1stBOS

…Core Themes …Outside of FX markets, our outlook for Bond Yields is still unchanged – we are looking for a range to develop over the summer for most core yields. There is however the growing risk of some yield tops and although this is not our base case, it is a risk we are monitoring carefully as recession concerns continue to grow.

The US 2s10s Bond Curve has flattened aggressively over the past week and has reached our long-held objective at -16.5/20bps. We reduce conviction in our flattening bias and would par back flattening exposure, however we are not ready to call for a low.

Finally, from BBG and its Weekly FIX (FI weekly letter),

In the span of 90 minutes on Wednesday morning, the most aggressive Federal Reserve move in modern history became a very real possibility.

Data at 8:30 a.m. Eastern showed that inflation surged by 9.1% in June from a year earlier, the biggest jump since 1981 and higher than every estimate in a Bloomberg survey of economists. An hour and a half later, the Bank of Canada shocked markets with a 100 basis point hike to fight back fears of entrenched inflation -- opening the door for the US central bank to follow.

An intense repricing of Fed expectations followed. At one point on Wednesday afternoon, swap-market bets showed traders were bracing for a 3-in-4 chance of a full percentage-point hike at this month’s meeting -- something that’s never been done since Fed started directly using overnight interest rates to conduct monetary policy in the early 1990s. Meanwhile, Nomura economists said their base case is now a 100-basis point move this month.

But if the Fed is really going to unleash the biggest rate hike ever in less than two weeks, they better start talking, given that the quiet period is quickly approaching.

“I think they have time, if they want, to change that expectation to 100. I don’t think they’ve given us a great reason why they should be going slow here, or being gradual,” said Michael Feroli, chief US economist at JP Morgan Chase & Co. …

… Word of the Week

Against that backdrop, Treasury yields have been all over the place. But similar to last week, there’s one clear theme: curve inversion. Benchmark 10-year Treasury yields fell as much as 28 basis points below those on 2-year bonds, the most since 2000.

Picking apart what’s driving the latest leg of curve flattening is telling. Two-year yields are on track to climb again this week, following a 27 basis point rise last week. Meanwhile, 10-year yields are lower by 12 basis points so far this week to hover below 3%.

That dynamic suggests a clear pretty linear chain of events: the Fed is going to raise rates a lot, which will hopefully stamp out inflation but will definitely kneecap economic growth.

With that in mind, it’s no surprise to see that a US recession is morphing into the base-case for sell-side economists. Wells Fargo Investment Institute and Nomura Holdings Inc. see a contraction this year, while Deutsche Bank AG thinks the downturn will begin in mid-2023. Bank of America now forecasts a “mild recession this year,” with higher food and energy costs leaving Americans with less cash to spend on everything else…

Recessions. Stag’flation. Rate forecasts. There is, as always, much to consider as you step up to the table and place your chips … Looking at things in a somewhat bigger picture (SECULAR) context as only HIMCo can do, what matters most is how the Fed reacts. Will economic hard times and lower yields as a result, lead to a 2018 Fed pivot (leading to another cost-of-living crisis OR will the Fed remain committed TO its current ‘flation fight? To know this answer (or at least have a view) might help you you choose where/how to place those chips…

Finally, why you should take any / all of the above and this spot on the web with a large grain of salt, my investing / trading prowess summarized in a single picture,

Anyone else who can relate? … THAT is all for now. Off to the day job…have a nice weekend.