Good morning … While not necessary the Fed pivot, worth noting overnight,

China cut their loan prime rates, the 1yr was lowered 5bp to 3.65% while the 5yr was cut more than expected by 15bp to 4.30%.

Now before we go any further, would you please join me in wishing a happy 45th birthday to the the long bond. Futures. That is …

HERE is a tribute TO the long bond (futures) I offered a couple years ago when the long bond celebrated it’s 43rd bday in 2020.

From the very TOP of the channel TO TLINE support … I’d highly recommend a point / click through what was note YESTERDAYand specifically the sage words from one who offered the ICE AGE theory long ago.

… HEREis what another shop says be behind the price action, you know,

WHILE YOU SLEPT Treasuries are lower and the curve flatter heading into this week's front-end loaded supply and Fed/PCE events this week. DXY is is higher (+0.18%) while front WTI futures are modestly higher (+0.5%) aftyer chopping around all morning. Asian stocks were mostly lower except in China after their 5y LPR cut, EU and UK share markets are all in the red (SX5E -1.4%, SX7E -2%) while ES futures are showing -1.1% here at 7am. Our overnight US rates flows saw a 'sleepy' Asian session where real$ bought 10's while joining fast$ in selling the long-end. Overnight Treasury volume was about average overall with 7's (148%) seeing some reltaively standout turnover overnight.

… What oil prices do this week will probably help to determine if 3.29% support for Treasury 2yrs will hold or give way... Grab your popcorn. Our next attachment shows that Treasury 5yr yields are also nearing tactical support at ~3.15; a level derived from a cluster of opening/closing highs for 5yrs seen last month. 5's do look short-term 'oversold' as we near that presumed support at ~3.15%...

… and for some MORE of the news you can use » IGMs Press Picks for today (22 Aug) to help weed thru the noise (some of which can be found over here at Finviz).

In addition TO what was noted HERE yesterday (a few sellside observations from Global Wall Street’s inbox) where I highlighted MS report on how CASH looks ‘relatively attractive’ right now (ZH must be a subscriber to this ‘stack ?), kindly note

As prospects of a sustainable recovery were fading amid the housing downturn, policymakers are now resuming the easing cycle with a more concerted (albeit still gradual) push for housing. We see subpar growth in Q3, but more aggressive easing is needed to arrest downside risks for Q4 and beyond.

Fed chair Powell is likely to emphasise that the fight against inflation is far from done … All eyes this week will be on the Jackson Hole Economic Symposium in Wyoming. Fed chair Powell (Fri) is likely to reinforce the FOMC's intention to guide policy to a restrictive position, amid lingering risks of sustained high inflation …

… China has cut its prime lending rates, with a 15bp reduction in the five-year rate. This move is more than was expected, and is being interpreted as another attempt to boost the flagging property market. Mortgage rates have fallen significantly over the past twelve months.

The US data calendar is quiet. Attention is focusing on the end of the week, and the central bank summer camp at Jackson Hole. Alongside the roasting of marshmallows and singing of campfire songs, Fed Chair Powell is expected to try and sound hawkish on policy. The problem is Powell has already trashed forward guidance …

For a view on RATES and specifically what is priced into the front end of the US curve,

… Fed officials, including Kashkari, Evans, and Daly, have been pitching a 'higher for longer' rate policy outcome, saying that while the pace of future rate increases may slow as economic activity eases, by no means does that imply that a peak in rates, or even a reversal, is in sight. On Thursday, Daly scolded that 'the markets have a lack of understanding, but consumers know that rates won't go down right after they go up.'

Meanwhile, over in the bond market, traders are betting that the Fed doesn't have the resolve to pull that off and will revert to cutting rates next year as a hard landing becomes evident.

Who is right and who is wrong remains to be seen…

Rareview: Demystifying the Pricing Of Interest Rate Cuts. Don't think of it in the absolute, think of the risk skew.

Many are confused about why the US fixed income market is pricing interest rate cuts in 2023, with inflation at a high level and the unemployment rate at a low level. The following commentary seeks to dispel the misconceptions surrounding why the pricing for these interest rate cuts exists.

Note that this commentary is not about inflation or employment. It is not a forecast. It is about probabilistic outcomes and historical precedent driving market pricing, regardless of the economic data or Federal Reserve messaging…

… CONCLUSION

We believe anyone’s view on portfolio construction beyond these facts is subjective and is not supported by the overwhelming evidence for central bank decision-making.

From a probabilistic outcome perspective and based on historical precedent, it is, therefore, logical to expect:

The Fed’s future interest rate cuts could be swift, mainly because the current interest rate hiking cycle can be measured in months rather than years.

If the last interest rate hike takes place in late 2022, the odds of an interest rate cut in 2023 are nearly certain.

The precedent of the Fed cutting interest rates back to zero in the next two years is very high. Ironically, per the table above, the market is only pricing in a 1% probability of that outcome.

This explains why the interest rate market is priced for the relatively higher risk of substantial interest rate cuts over the next two years.

Is the US at full employment and we just don’t know it yet?

The ratio of full-time workers to part-time workers is at a near 20-year high. It may be turning, and a drop in the ratio may spell peak inflation as companies adjust to cut costs. That’d mean a better environment for stocks and bonds going forward.

If the ratio falls, it likely means companies are either looking to replace higher paid full-time workers with less expensive part-time employees or they are seeing declining sales. Either way, it is a sign of rising costs and an attempt to lower them or a slowing economy.

Both scenarios could prompt a Fed pivot. A slowing economy and peaking inflation are the signs the Fed needs to see in order to pause rate hikes.

Another angle on inflation rolling over (or perhaps NOT) can be seen HEREoffered by WFC,

Tackling Inflation This Tailgating Season With the end of summer in sight, football fans have begun to get excited for the start of a new season. But this year, fans will not just be coping with the usual parking lot traffic and last second heartbreak. They will also be dealing with some of the fastest inflation seen in decades. Prices have surged over the past year for gasoline, flights and many of the staple foods found at tailgates and watch parties. That said, consumers remain eager to get out and partake in experiences missed over the past couple years, and not all parts of the gameday experience have seen surging costs. Prices for televisions, beer, hot dogs and hotel accommodations have all increased by less than the total consumer price index over the past year. But even if inflation keeps some football fans on the sidelines this season, as any sports fan can tell you, at least there's always next year.

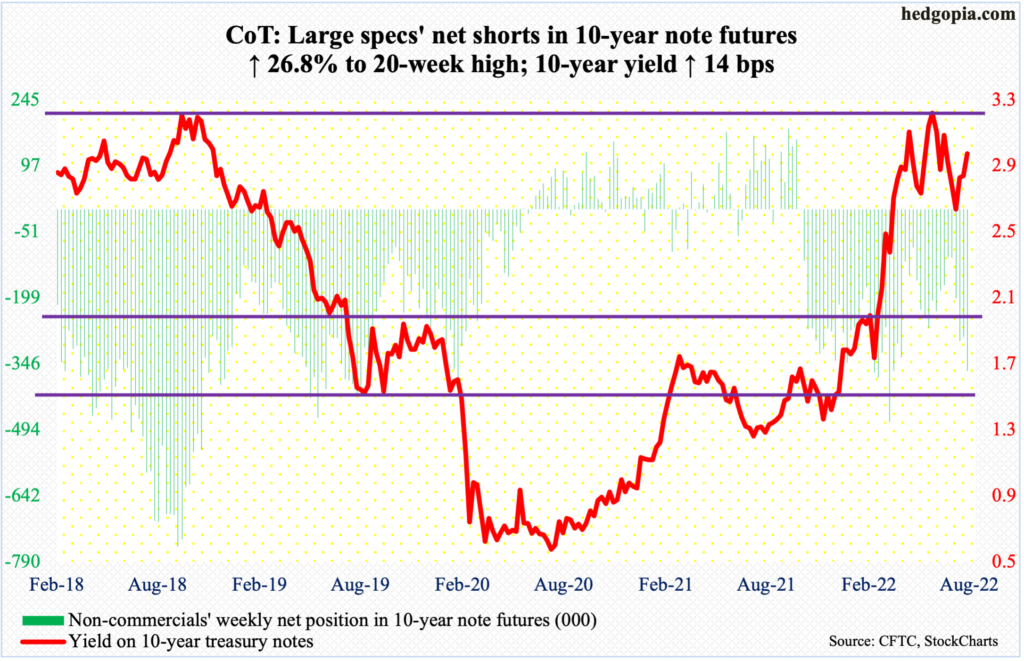

Giant investment funds may be ready to pile back into Treasuries but their bearish fast money counterparts are also growing in confidence, taking heed of the relentless message from Federal Reserve officials that the fight against inflation is nowhere near done. An aggregate gauge of net-short non-commercial positions across all Treasury maturities shows bearish bets have grown to the most since 2018, according to the latest data from the Commodity Futures Trading Commission. Last week saw a spike in bets against five-year Treasuries, which are particularly sensitive to Fed policy. Meanwhile, the 10-year Treasury yield is on the cusp of rising past the closely-watched 3% level once more as investors await Fed Chair Jerome Powell’s speech at the annual Jackson Hole symposium this week. Bets on the benchmark note are diverging once again with asset managers net long and leveraged funds net short — reminiscent of the sizeable opposite positions both had in 2019. It would be churlish not to acknowledge that hedge funds won that round.

{kind=link}