Good morning … what did I miss? Am cutting some corners as I’m sifting through markets and inbox trying to make some sense of it all, likely falling short and so, leaning then on the expertise of ‘them’.

First up, a recap of past 24hrs by one of Global Walls fan favs …

… a brief review of the last 24 hours first. We saw a moderate risk-off move yesterday, with the S&P 500 (-0.43%) falling back from its all-time high, whilst gold prices closed at a record $2,939/oz. This morning Chinese risk is doing well on the back of Alibaba'a earnings. The main story in the US was a weaker-than-expected forecast from Walmart, which added to nerves about the health of the consumer right now, especially after a soft retail sales print last week. So that dented confidence, but some nervousness is also setting in ahead of a pivotal German election this Sunday, which could have significant implications for European markets and geopolitics for years to come…

…Away from the German election, the main story of the last 24 hours, as discussed at the top, was a pullback in US equities, though this decline did ease somewhat as the session went on. By the close, the S&P 500 was down -0.43%, having been -0.97% lower early on. The decline followed a weaker than expected profit forecast from Walmart (-6.53%), who were the worst performer in the Dow Jones (-1.01%) as a result. Moreover, that followed a worse-than-expected US retail sales number last week, which showed the biggest monthly contraction (-0.9%) since March 2023. So putting all that together, it added to fears that growth might be losing momentum into the new year. With this backdrop, bank stocks were the biggest decliners within the S&P 500 (-2.97%), giving up some of the outperformance that had propelled the sector to a +11.7% YTD gain prior to yesterday’s decline. Elsewhere in Europe, the STOXX 600 (-0.20%) also lost further ground, leaving the index on course to post its first weekly decline of 2025 so far.

On the rates side, the risk-off tone pushed yields lower on both sides of the Atlantic. But the main headlines came from US Treasury Secretary Scott Bessent, who said that moves to increase longer-term debt sales were “a long way off”. So that helped to push down longer-dated Treasury yields, with the 10yr Treasury yield down -2.8bps on the day to 4.51% and overnight trading at 4.49% (-1.95bps) . By contrast, the 2yr yield was little changed (+0.1bps to 4.27%), in part amid hawkish-leaning Fedspeak, as St Louis President Musalem said that policy should stay “modestly restrictive until inflation convergence is assured” He further added that “Around this baseline scenario, the risks of inflation stalling above 2% or moving higher seem skewed to the upside”…

AND a couple / few OTHER things

ZH: Soft 20Y Auction Tails As Foreign Buyers Shrink

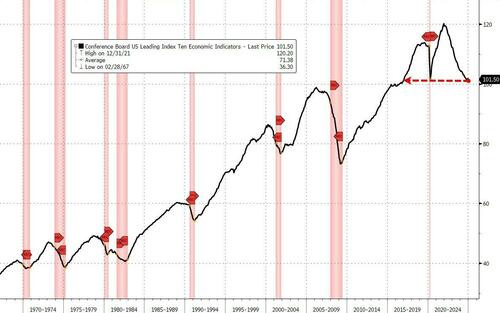

ZH: Dollar & Stocks Dumped, Bitcoin Pumped, Gold Stumped As LEI Hits 9-Year-Lows

… Jobless Claims were 'meh' except for the beginning of the surge in the unemployed in DC but it was the Leading Index that tumbled more than expected (back to its lowest since Dec 2016)...

…WMT was the standout name (though it didn't impact The Dow that much due to its 'low price')...

Treasury yields were lower across the curve with the long-end outperforming (30Y -4bps, 2Y -1bps). The short-end remains the outperformer on the week (unchanged)...

… here is a snapshot OF USTs as of 625a:

… for somewhat MORE of the news you might be able to use … a few more curated links for your dining and dancing pleasure …

NEWSQUAWK US Market Open: EUR weighed on by PMIs & JPY hit by Ueda remarks, Commodities are pressured by the firmer Dollar ahead of US PMI …USTs are marginally firmer but only posting gains of a handful of ticks in rangebound/choppy trade with US-specifics so far somewhat lighter than has been the case in recent sessions. Overnight, USTs caught a bid alongside the discussed move in JGBs. Specifically, at the upper-end of a 109-03+ to 109-11+ band, eyeing the 109-15 peak from Monday. Ahead, while we await updates to the tariff and geopolitical narratives we get data via US Flash PMIs and then an appearance from Fed’s Jefferson (Voter) on Fed Communication, from this we expect both a text release and a Q&A.

… For the year, 2024, the blended performance (as some bonds were purchased during the year) was 6.7%. It had been as high as 7.4% in September until rates pushed higher.

You can see how that compares to the passive Bloomberg Barclay's US Aggregate bond index (AGG) and the iShares iBoxx Investment Grade Corp Bond ETF (LQD).

Resilient growth and rising inflation expectations are weighing on the global macro setup, with rates positioning moving into neutral, the consensus long dollar unwinding into weakness and equity longs being trimmed as they touch highs - our analysis suggests that these position unwinds are driven by profit-taking rather than stop-loss.

This setup aligns with macro indicators, where underlying inflation data is accelerating and surprising to the upside, while growth data is more neutral. This is creating uncertainty in the speed and size of FED rate cuts, with the market gyrating between x1 to x2 rates by the end of the year. Meanwhile, as inflation expectations rise, curves have been flattening (inflation pressures are assumed to be short term dynamic) and equity/bond correlation has been moving higher (in the top quantile)…

…In USTs 4.50% remains the sticking point in 10s, which is where we see long / short risk is concentrated (positioning and systematica). As roll activity picks-up, we find there is little change in the positioning setup, with the market mildly short both tactically (at $10m) and structurally (at $35m), but no profits. A similar dynamics is also playing out in systematics, where the market has trimmed short (at 108-28 in 10s) but larger moves are required for models flip long at 110-00.

DB: Debt ceiling and balance sheet strategy: Key takeaways from the FOMC minutes

DB US Economic Chartbook: Trump 2 month 1: Fed on hold with inflation still too fast, tariffs more furious

…Accommodative financial conditions suggest r-star may be higher / policy not as restrictive

In light of discussion in its January minutes (released yesterday), we now expect the FOMC to announce a pause to QT at its March meeting, to be implemented in April, alongside forward guidance that QT will resume at the current caps ($25bn on USTs; $35bn on MBS) once Fed liabilities have normalized following resolution of the debt limit. Given our debt limit baseline, we project QT will resume in October.

We also take the occasion to modestly revise our assumption of the level of ample reserves – from $3tn to $2.75tn – in line with the calibrations discussed in our earlier note on market expectations for QT. With this change, and the assumption that the FOMC will stop QT with reserves “somewhat above ample” (per the 2022 balance sheet runoff plans), we now expect QT to end altogether in Q1’2026.

Once overall QT ends, we expect MBS prepayments to be invested into USTs to facilitate further reduction in the share of MBS in the SOMA portfolio. And, in early 2027, balance sheet growth will restart to accommodate growth in non-reserve liabilities that would otherwise lead reserves to decline. We discussed guidance in yesterday’s minutes on the structure of these purchases here.

ING: Eurozone PMI shows little relief from stagnation just yet

MS: U.S. Economics: Immigration and the macroeconomy

Investors are focused on the twists and turns of tariffs, but we think immigration policy deserves more attention. The macro effects of immigration restriction could be just as consequential.

Key takeaways

Immigration averaged about 3mn per year in 2022-24, about twice the historical run rate. We think immigration falls to 1mn this year and only 500,000 next year.

Less immigration could lower real GDP by 0.4-0.6pp this year and next and put upward pressure on inflation, particularly in services, and to some extent wages.

Slower immigration could pull short-run potential GDP growth down from 2.5-3.0% in 2022-24 to 2.0% this year and 1-1.5% next. Trend hours should slow markedly.

The Fed leans against the new inflation pressure, supporting our expectation of just one cut this year and further cuts only late next year after growth slows.

MS: U.S. Economics: History may not repeat, but it should rhyme: what the 2018-19 tariffs can tell us about tariffs today

The 2018-19 tariffs caused manufacturing output to fall after a delay. This time around, the hit to growth could materialize faster. Either way, we think the Fed will be inclined to ease in support of activity so long as inflation pressures prove temporary, as we expect.

US Treasury Secretary Bessent signaled that former US Treasury Secretary Yellen’s debt issuance plan would continue, implying no increase in longer-dated Treasury bonds and lowering 10-year yields. This support is threatened by talk of a “DOGE dividend” to taxpayers. There is a considerable gulf between claimed government savings and economists’ view of reality. Refunding illusionary savings would be a deficit-financed stimulus check….

Wells Fargo: Soft-Landing, or No Soft-Landing, That is the Question

… And from the Global Wall Street inbox TO the intertubes, a few curated links …

From The Terminal, a view on FI POSITIONS and flows …

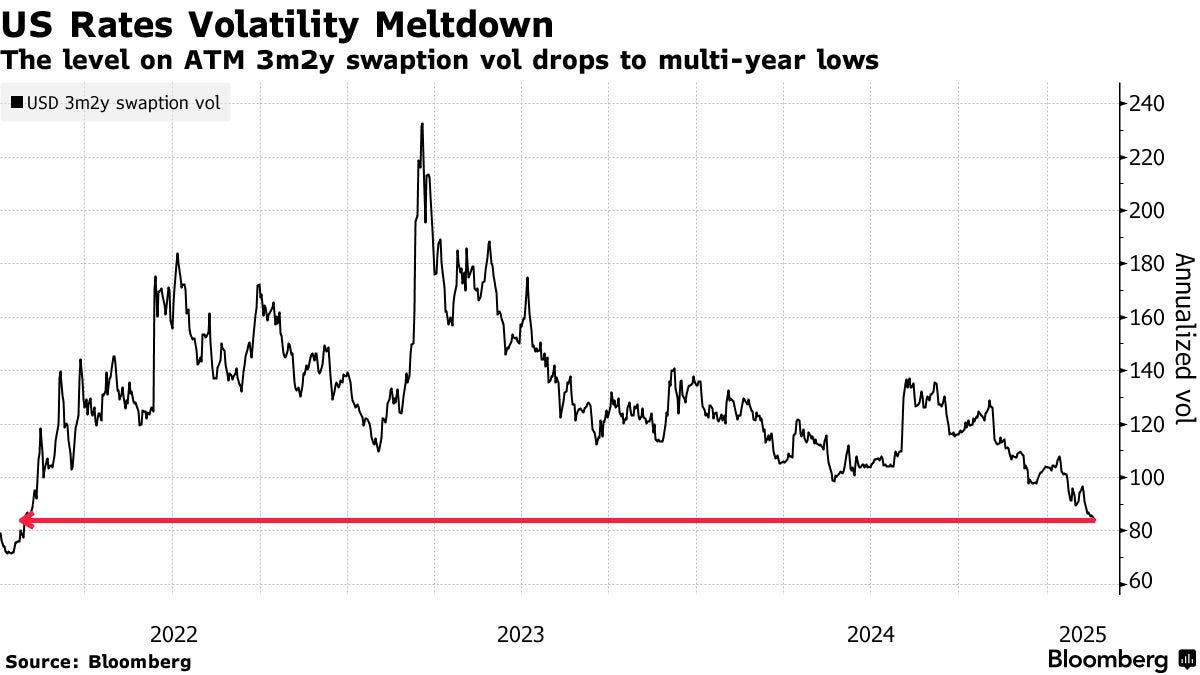

Bloomberg: US Rate Volatility Craters as Tariff-Wary Bond Traders Pull Back

Traders turn to short vol plays in Treasury and SOFR options

JPMorgan clients flip to biggest neutral positioning this year

…Traders taking directional bets off the table have helped keep US yields in a tight range in recent weeks. The benchmark US 10-year Treasury yield continues to straddle a 4.5% handle, near the middle of this year’s 4.38% to 4.81% range. At the same time, one measure of rates volatility - the 3-month/2-year swaption, which reflects implied volatility via option prices - has dropped to its lowest levels since January 2022.

A narrower range of Fed policy outcomes may also be keeping yields in a tighter range. Front-end Fed swaps continue to trend toward just one more full quarter-point of central bank easing for this year.

In listed options, the short volatility theme has also been well represented, with trades this week focusing on sellers of strangle and straddle positions across both SOFR and Treasury options, as traders look to take advantage of the current low volatility backdrop. The theme continued Wednesday with a $3 million short volatility trade.

Here’s a rundown of the latest positioning indicators across the rates market…

MORE (catchup) over the weekend but … THAT is all for now. Off to the day job…