Good morning … what did I miss? Catching up after quite a day on Global Wall, from what I can tell, and so I’ll begin with a quick look at 10s …

10yy DAILY: sittin’ on ‘the fence’ (TLINE ~4.27%) ahead of the data …

… bearish momentum now off overBOUGHT conditions, middlin’ and awaiting this mornings data and reports of the NEXT legendary / record-sized trade …

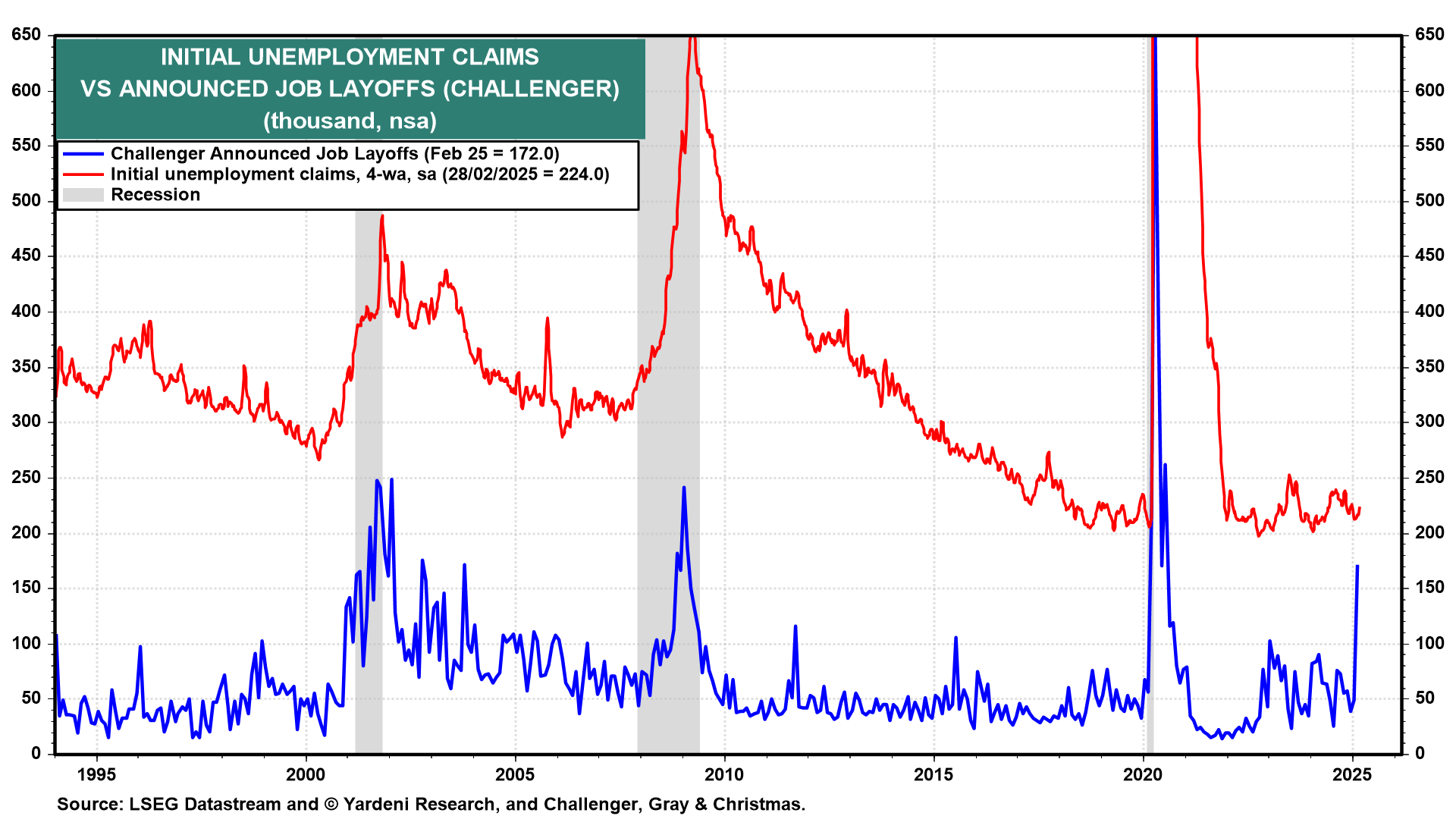

… Moving right along to what SHOULD be a short note ahead of today’s data. The weekend note will be filled with further recapAthon and I told ya so, but first, a quick look back at what it was that drove price action Thursday … Challenger …

ZH: DOGE Deep-State Demolition Sparks Surge In Layoffs

… In a sign that policies from the new White House Administration are starting to hit the labor market, Challenger layoff announcements spiked 245% m/m in February to 172,017, more than double what they were a year ago and the highest monthly total since July 2020 (262,649).

The year-to-date total of nearly 222,000 planned job cuts is the highest since 2009, when the economy was still amidst the Great Recession.

The surge was led by the government sector, with 17 different agencies announcing cuts last month.

Challenger said the purging of the federal workforce by DOGE was cited as the main reason for layoffs.

Despite the jump in job cutting plans, initial claims for unemployment insurance have yet to show a meaningful increase…

… The ECB …

ZH: ECB Cuts Rates, Says Policy Becoming "Meaningfully Less Restrictive"

… all told, seems to many (some) stocks sticking to ‘the script’ (‘45 vs ‘47) …

ZH: Stocks Puke Despite 'Easing' Tariffs As Trifecta Of Trouble Hits Markets

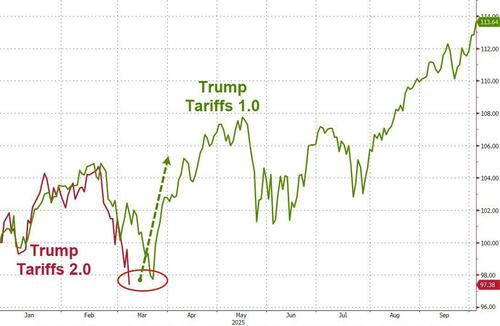

…And if we are still focusing on Trump Tariffs 1.0 as an analog, we are a critical level here...

… and so it goes. Tariffs ON, walked back (not OFF!, not yet) and back on … certainly hard to skate to where the puck is gonna be.

That in mind, before I hit send, one last statement of the obvious …

… After a frenzied week in global markets, investor attention today turns to the US jobs report at 8:30 a.m. Washington time. They’ll be looking for signs of weakness in the economy to determine whether the rally in Treasuries has more room to run.

Treasuries have already returned 2.2% this year as traders bet that a slowing economy and US tariff turmoil will force the Fed to cut interest rates.

“The economy is obviously slowing,” said Gang Hu, managing partner at Winshore Capital Partners. “If the payroll comes out on the weak side, markets will bet that the Fed will cut rates in May. There’s still room for yields to go down.”

Bloomberg Economics has one of the lowest forecasts, seeing a subdued 65,000 increase in payrolls, in part because the withdrawal of Biden-era fiscal support was amplified by Trump’s temporary funding freeze.

“We expect a tepid pace of job growth in February due to a combination of fiscal withdrawal and bad weather. A reversal of those factors should support payroll growth in March, but DOGE layoffs and spillovers to the private sector from cancelled federal contracts will also begin to show up in the data.” —Anna Wong, Estelle Ou and Chris G. Collins, Bloomberg Economics

Of course, some on Wall Street have grown concerned the rally in bonds is overdone. JPMorgan Chase is recommending clients go short two-year notes, in part because of “stretched” bullish positions.

Two-year yields, which are most sensitive to Fed policy, hit a five-month low of 3.84% this week before rebounding to 3.94% now.

“If the job market shows material weakness, people will get much more worried about recession risks,’’ said Priya Misra, portfolio manager at JPMorgan Asset Management. —Ye Xie and Liz Capo McCormick

… here is a snapshot OF USTs as of 655a:

… for somewhat MORE of the news you might be able to use … a few more curated links for your dining and dancing pleasure …

NEWSQUAWK: US Market Open: US equity futures trade modestly higher whilst the Dollar slips ahead of US NFP … USTs are firmer but in a narrower 110-25 to 111-03 band. Benchmarks benefitting from the uptick in Bunds as discussed above, more sources pointing to the BoJ potentially remaining on hold in March (pricing has a 96% chance of no move implied) and mainly waiting for Payrolls & Powell. That aside, following the concessions on tariffs by Trump on Thursday we are keenly awaiting any fresh updates to this for/from Canada and Mexico in addition to and perhaps more pertinently anything relating to China.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s some of what Global Wall St is sayin’ …

First up, one of many ECB recaps …

ABNAmro: ECB building to an April pause, but shocks will determine outlook

The ECB cut its key policy rates by another 25bp as was widely expected, taking the key deposit rate to 2.5%. In a sign that the Governing Council judges that interest rates are closer to neutral it noted that ‘monetary policy is becoming meaningfully less restrictive, as the interest rate cuts are making new borrowing less expensive for firms and households and loan growth is picking up’. However, there were also clear signs that it does not see the job done quite yet.

The ECB trimmed the deposit rate by 25bp and maintained that policy remains restrictive, although meaningfully less so, while remaining noncommittal on future rate decisions. We continue to expect consecutive 25bp cuts in April and June. We do not see an end to QT for now.

… same firm w/a CPI precap / victory lap …

Barclays: Core inflation to retrench after January surge

We forecast core CPI inflation eased 14bp, to 0.31% m/m, following beginning-of-year price increases in January. We foresee elevated food inflation to be partly offset by lower energy inflation, with headline CPI rising 0.3% m/m SA (2.9% y/y), and the NSA index at 319.356.…

Following a strong Q4 print, China's exports weakened significantly, with slumping shipment to the US. This reflects the payback from earlier exports front-loading and Trump's faster and broad-based tariff hikes, in our view. The deep imports contraction pointed to weakened domestic demand in Q1.

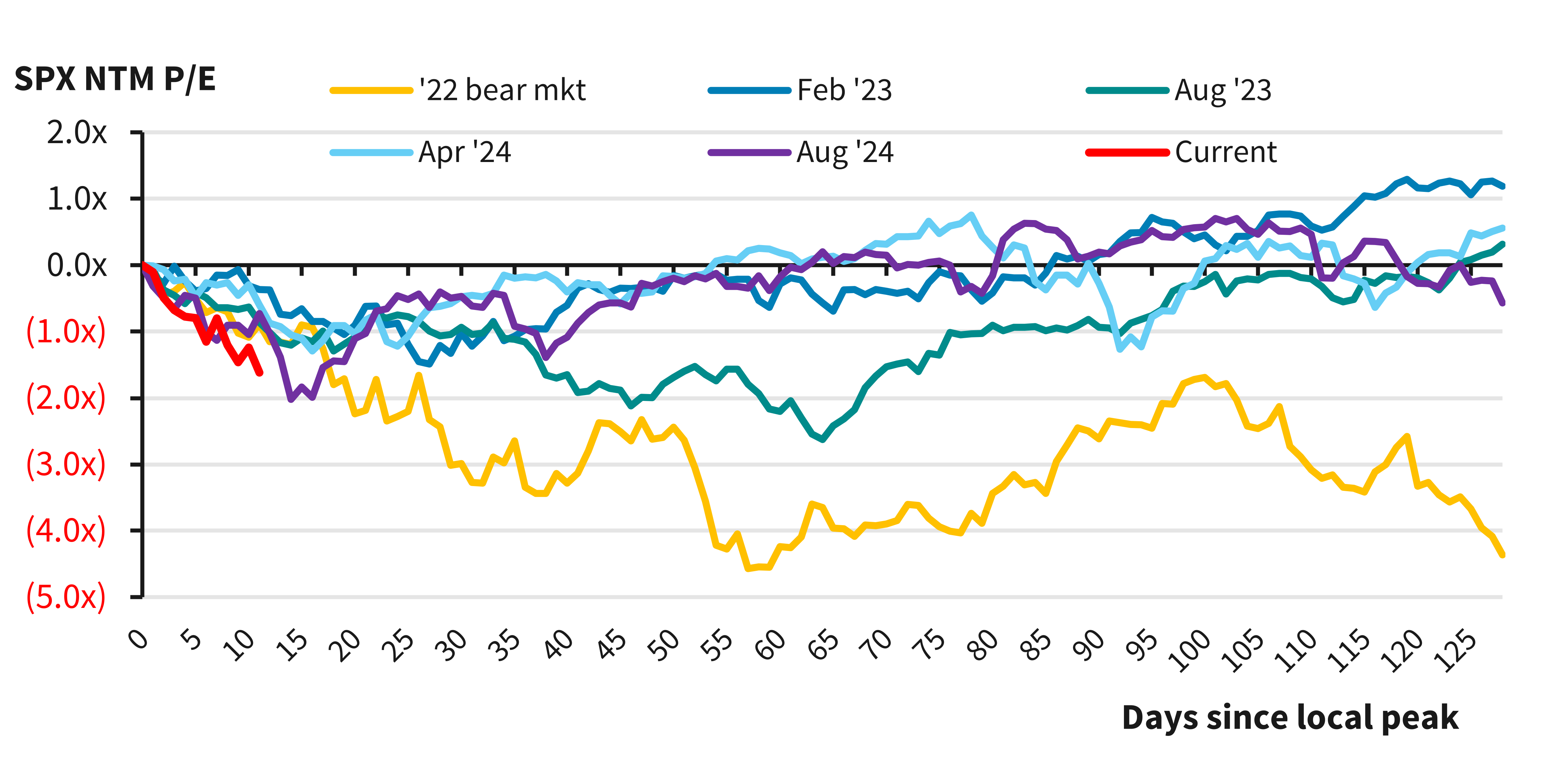

De-rating has been fast and furious vs. comparable selloffs of the last 3 years; positioning was not overly extended, pointing to fundamental repricing over technical unwind. Exuberance getting washed out; absent a "Trump put," could get worse before it gets better.

How does the current de-rating stack up against recent risk-off episodes? Assuming 2/19/25 was the local peak for SPX, we compared current multiple compression against peak-to-trough declines of at least 5% since the 2022 bear market, finding that the current P/E washout is the fastest and most severe of the last 3 years. This is notable in that positioning was not overly extended this time, whereas prior (near-)corrections were preceded by record SPX futures positioning among LOs, extended systematic equity longs and downside asymmetry in CTA flows (see our Aug '23, Apr '24 and Jul '24 positioning analyses). We think this frames the current pullback as less of a technical unwind and more of a fundamental reassessment of the growth outlook amid an increase in economic and policy ...

The current selloff has been the most aggressive de-rating seen over the last 3 years

… France on ECB …

BNP ECB: Especially uncertain times, especially vague guidance

KEY MESSAGES

The ECB took a step closer to the end of its easing cycle by delivering another 25bp cut in March and signalling that policy was becoming “meaningfully less restrictive”. But it also suggested it had not yet reached its destination.

President Lagarde left April wide open as the Governing Council tries to assess developments in geopolitics and domestic fiscal spending as well as incoming data. We see an April cut as marginally more likely than not and leave our terminal rate forecast at 2%.

However, given our view that higher defence and infrastructure spending will materially boost GDP and price pressures in the medium term, we see a strong case for the ECB to begin raising interest rates later in 2026, as the effects start to materialise.

The watchword from the March ECB press conference was ‘uncertainty’. According to President Lagarde, the ECB is facing ‘huge’ uncertainty at many levels, from energy prices to tariffs and trade war to ‘massive’ fiscal easing with spending on defence and infrastructure. This lack of visibility on the path ahead for growth and inflation challenges policymakers, making it even more difficult to project forward the path of monetary policy.

It is entirely appropriate that the ECB is retaining policy optionality. President Lagarde said the ECB will be more data dependent than ever. But there was a sense from Lagarde that the bar to a pause in April is lower than we thought and that the 'direction of travel' was no longer clear. The analogy to have in mind is the ECB “tiptoeing in a dark room”.

We continue to think a rate cut in April is more likely than not. This is based on the assumption of a growth shock from US tariffs in early April. Despite the downgrade to the staff GDP projections, no US tariffs on Europe have been incorporated yet, meaning more downgrades are to be expected. It would require a benign tariffs announcement in April to pause the easing cycle, in our view.

However, our baseline terminal rate forecast of 1.50% by end-2025 could be challenged. We had talked about a landing zone for terminal rates in 2025 of 1.00-1.75%. Even with the tariff shock outstanding, given the scale of what is now coming in terms of fiscal easing, the risks are shifting and there is now arguably more upside risk than downside risk around the 1.50% call in 2025. With simplifying assumptions on fiscal policy, in this note we roughly calculate that the policy rate in 2027 could be c.50bp higher than assumed in the baseline (2.75% vs. 2.25%). The timing and coordination of the defence and infrastructure spending will be key and we will reconsider our ECB call as Europe’s fiscal plans become clearer.

… Same shop with an interesting chart and question on all our minds …

… Trade wars have been around for some time, but global trade has not yet really declined and has been stable near 45% of world GDP since the GFC. Far from stopping China’s export juggernaut, China’s trade surplus has tripled from USD350bn in 2018 when trade wars began to nearly USD1tn. The real legacy of the 2018-19 trade war was the rise of connector economy trade. Bilateral US tariffs on China led to a re-routing of Chinese goods through economies like Mexico and others, still ending up in the US. Many countries saw an increase in trade as they facilitated the movement of goods between China and the US. Supply chains lengthened and global trade did not fundamentally change or fall.

With US tariffs now rising to levels not seen in the post-WWII era, the first-order impact is that global trade could begin to decline by more than anything we have seen since the 1930s. The second-order impact is that if the US – and West more broadly – becomes less willing to import Chinese goods, these goods will need to be absorbed elsewhere …

Stocks are RICH. Here are 4 reasons why …

First Trust: Four Valuation Models Flash Caution for the S&P 500 Index

With the market volatile, we thought it would be a good time to take a look at alternative valuation models. Every major valuation metric of the S&P 500 Index is flashing warning signs. In this week’s “Three on Thursday,” we look at three key different valuation models, each offering a unique perspective on just how stretched equity prices may be. As a bonus, we’ve included our own in-house model and what it shows. Explore the four charts below for a clearer picture of where valuations stand for the S&P 500 Index…

The Fed Model, popularized during Alan Greenspan’s tenure as Federal Reserve Chair, compares the difference between the S&P 500 Index’s earnings yield (inverse of the P/E ratio, so E/P) and the 10-year U.S. Treasury yield to gauge stock market valuation. The higher the earnings yield on stocks versus the yield on bonds, the stronger the case that future returns on stocks will exceed the yield on bonds. This week’s selloff has pushed it back out of negative territory, but the metric still sits close to levels not seen since the Dot Com bubble…

… Bunds. James BUNDS …

ING: Rates Spark: The 3%+ area targetted for the 10yr Bund

The ECB has cut by 25bp, and Europe is awash with the narrative of fiscal expansion leaving less room (or need) for monetary stimulus. US non-farm payrolls next. It's typically influential, but this time the market will look through a firm number, or, regard a weak number as validating current levels. So not expecting much impact. Still, got to be watched …

… Our CPI forecasts translate into a February core PCE inflation reading of 0.24% m/m (2.7% y/y), about 4bp slower than January's pace. The expected easing in m/m core PCE largely reflects our core CPI forecasts. The CPI and PPI data (due March 13) should help refine our forecast.

… same shop on ECB …

ING: ECB cuts rates but the door to further cuts is closing quickly

After today's 25bp rate cut, we expect the ECB to pause at the next meeting and to cut only one more time before the summer

… same shop with a look at the new / reiteration of the ARMS race …

Europe is known to move little in good times and fast in times of crises. This week, European fiscal spending seems to be making a return as recent proposals from the European Commission and Germany suggest that a large fiscal push to boost defence and infrastructure spending is on its way. Markets have reacted strongly; here, we take a look at what it all means

… a global MACRO commentary summarizing yesterday in a sentence or two …

ECB cuts rates by 25bp; US tariffs on USMCA goods delayed; upside surprise in Swedish inflation; choppy UST and USD price action amid macro developments; Japan's largest union seeks notable wage hike; US implied equity volatility continues to rise; DXY at 104.22 (-0.1%); US 10y at 4.278% (-0.0bp)

… same shop with a CPI precap of its very own …

MS: US Inflation Monitor: CPI Preview: Stepping down

We expect core CPI at 0.32% m/m in February (3.2% y/y), stepping down from January but still elevated. We expect a milder push from wildfires and residual seasonality this time. Both core goods and services decelerate. We see headline at 0.32% m/m, 2.9% y/y, NSA Index: 319.323.

… with CPI in mind, taking a step back and looking more holistically at the USofA and for the week ahead …

We take on board greater-than-expected intensity in trade policies and revise growth lower in 2025 and 2026. We now see higher inflation in 2025 with a more pronounced and sooner reacceleration in goods prices. The mix of firm inflation and low unemployment could put the Fed in a bind.

Key takeaways

Our real growth forecast comes down to 1.5% and 1.2% (from 1.9% and 1.3%)

We now see headline PCE inflation of 2.5% y/y and core PCE of 2.7% by December, up two-tenths.

We still expect disinflation until April/May and a 25bp cut in June, followed by a pause as inflation reaccelerates.

Cuts resume in March 2026 once the unemployment rate starts increasing. Our terminal rate remains at 2.625%

… Revisions to our outlook still leave the Fed in a difficult spot. If we are right that increased tariff intensity causes inflation to firm later this year and immigration controls limit labor force growth and keep the unemployment rate low, then the Fed may find it difficult to ease. Even if we are wrong on tariffs firming inflation and, instead, inflation moves sideways, then further Fed cuts this year still have a high bar. In sum, we think investors have unrealistic expectations about the ability of the Fed to deliver the rate cuts markets have priced in (about 75bp of rate cuts in 2025 at the time of our writing). We think markets will ultimately get these cuts, but much later than they expect…

The ECB cut rates to 2.5% at the March meeting, and described rates as becoming meaningfully less restrictive. GDP projections were revised down, with risks tilted to the downside.

… perhaps too little too late here but an NFP precap moments before data prints …

At the beginning of this week, we saw no reason to expect a major shift in the tone of the employment data this month. That’s still our base case, but some of the peripheral labor market indicators that have come out this week tilted the odds toward a slightly softer bias. For instance, the latest report from the NFIB small business survey in February showed the hiring intentions component down three points to 15% in February—raising the possibility that our 120,000 private sector job forecast (consensus 146,000) may be too optimistic (see chart below). While the NFIB's pre-COVID track record is far from perfect, the series has done a decent job at signaling the monthly directional change in payrolls since the pandemic, and the February reading looks consistent with less than 100,000 payrolls (see chart below).Overall, we still project an increase of 150,000 in total nonfarm payrolls in February (consensus 160,000). A realization of our estimate would put the three-month average gain at 200,000 (versus 237,000 as of January). We also expect the unemployment rate held steady at 4.0% (consensus 4.0%) and hourly earnings increased 0.2%m/m/4.1%y/y (consensus 0.3%/4.1%). Also on Friday, Fed Chair Powell will speak on the “Economic Outlook” just four hours after the release of the employment report (and ahead of the blackout period that starts Friday night at midnight) at a policy forum in NY; the chair is scheduled to release prepared remarks and take questions from the audience.

… our neighbors to the north have some words …

RBC: DOGE cuts could push up the U.S. unemployment rate

We have been thinking about how the DOGE layoff announcements may impact the upcoming labor market data. While the headlines have been frequent, we still see a wide range of estimates in terms of the overall impact on the economy. In total, we estimate the potential range of job losses from 100,000 in a low-layoff scenario to 550,000 in a high-layoff scenario. Below, we provide our estimates for the DOGE cuts and how those could show up in the data releases in the coming months with respect to payrolls, the unemployment rate, and jobless claims.

… covered wagons on the horizon … so too is the CPI …

Wells Fargo: February CPI Preview: The Tariff Winds Start to Blow

Summary Consumer price inflation came out of the gate strong in 2025, but price growth looks to have cooled somewhat in February. We estimate headline CPI rose 0.25% and the core index advanced 0.27%. The moderation in the core index is likely to reflect some giveback in a handful of categories that soared in January (e.g., prescription drugs, used cars, motor vehicle insurance and recreation services) and lead to softer monthly prints for both core goods and services. However, we believe growing concerns over tariffs are already affecting pricing decisions and will help to keep the pace of consumer price inflation firm overall…

… same shop with ‘a few more simulations’…

Wells Fargo: Tariffs Driving You Crazy? A Few More Simulations to Ease Your Mind

Summary U.S. tariff policy is rapidly changing. And in an attempt to proactively assess the economic impact of tariffs, we modeled and ran two new simulations based on different tariff assumptions. The first scenario is similar to the assumptions currently underlying our global economic outlook, albeit with minor tweaks. The second scenario represents a more contentious tariff posture from the United States as well as full retaliation from major U.S. trading partners. In short, the more aggressive the tariff policy becomes the closer the global economy—and U.S. economy—get to recession, and the further central banks are from reaching their respective inflation targets. For now, this exercise is purely indicative, and we will formally adjust our tariff assumptions and forecasts in our monthly update next week.

The ECB cut interest rates by 25bps at its March meeting, taking the deposit rate to 2.5%, in line with our and market expectations.

Uncertainty about the outlook remains high. Thus, the ECB is sticking to it's meeting-by-meeting approach to setting policy. We still expect cuts in April and June, taking the deposit rate to 2%.

Monetary easing, fiscal policy, and a potential ceasefire in Ukraine remain supportive for Eurozone equity and bond markets. In equities, this favors a selective approach and continue to recommend gaining exposure to the DAX through structured strategies or via our “Six Ways to Invest in Europe” theme. In fixed income, we favor medium-tenor quality corporate bonds.

Having imposed aggressive taxes on US consumers at the start of the week, US President Trump partially retreated from taxing Mexican and Canadian imports yesterday (assuming goods are compliant with the revised NAFTA). The taxes are delayed until 2 April, but markets will likely price in more retreats.

Some Mexican and Canadian imports are still taxed (including some cars, now experiencing their fourth tax regime this week). There US consumers will need to find 27.5% of the price to pay to the US government. This week’s tax and retreat has incurred an economic cost. Uncertainty has risen for companies and financial markets, with some questioning whether the US government has a coherent policy.

Today’s US employment report will not really reflect government job losses, because the government is not a significant employer and because timing will push the losses into later months. The main future employment hit is likely to be from private sector businesses that depend (directly or indirectly) on government employment.

China’s import and export data for February were both weaker than expected. The import numbers do not suggest a strong domestic consumer at the moment. German January factory orders data is also due.

… Dr Bond Vigilante weighing in on Challenger, Gray and Christmas …

Yardeni: Layoffs Rising According To Challenger Report. Is That Alarming?

We raised the odds of a recession on March 4 from 20% to 35%. Today's Challenger Report showed an alarming jump in February's announced job layoffs to 172,017, the highest since July 2020 (chart). On the other hand, initial unemployment claims remained low through the February 28 week. So we aren't raising our odds of a recession again, for now.

A third of February's layoffs were announced by the government sector. That's not surprising given the activities of the DOGE Boys (chart). Announced layoffs in the private sector totaled 109,777 with retailing accounting for 35% of those layoffs.

Stock prices sold off again today on the layoffs news. We are still expecting a solid February employment report tomorrow reflecting a rebound in payrolls and in the average workweek following the coldest January since 1988 and the severe fires in Los Angeles during that month…

…(5) Will the price of a barrel of Brent crude oil hold support around $69? It might given recent stimulus measures in China and Germany. Lower oil prices should stimulate more global economic growth and oil demand. Then again, oil supplies are plentiful.

…(10) How many more 25bps fed funds rate cuts are likely over the next 12 months? The fed funds rate futures market shows three more. We remain in the none-and-done camp.

… And from the Global Wall Street inbox TO the intertubes, a few curated links …

Uncertainty … leading to downside protection interest … BIGLY …

Investors are getting very worried about the downside risks to their portfolios. VIX call volume buying is near record-high levels, and S&P 500 put volume buying is near record-high levels, see charts below.

Bloomberg: Tariff anxiety and the dilemma of forecasting Investors want clarity. Will the Trump administration stand up to the market?

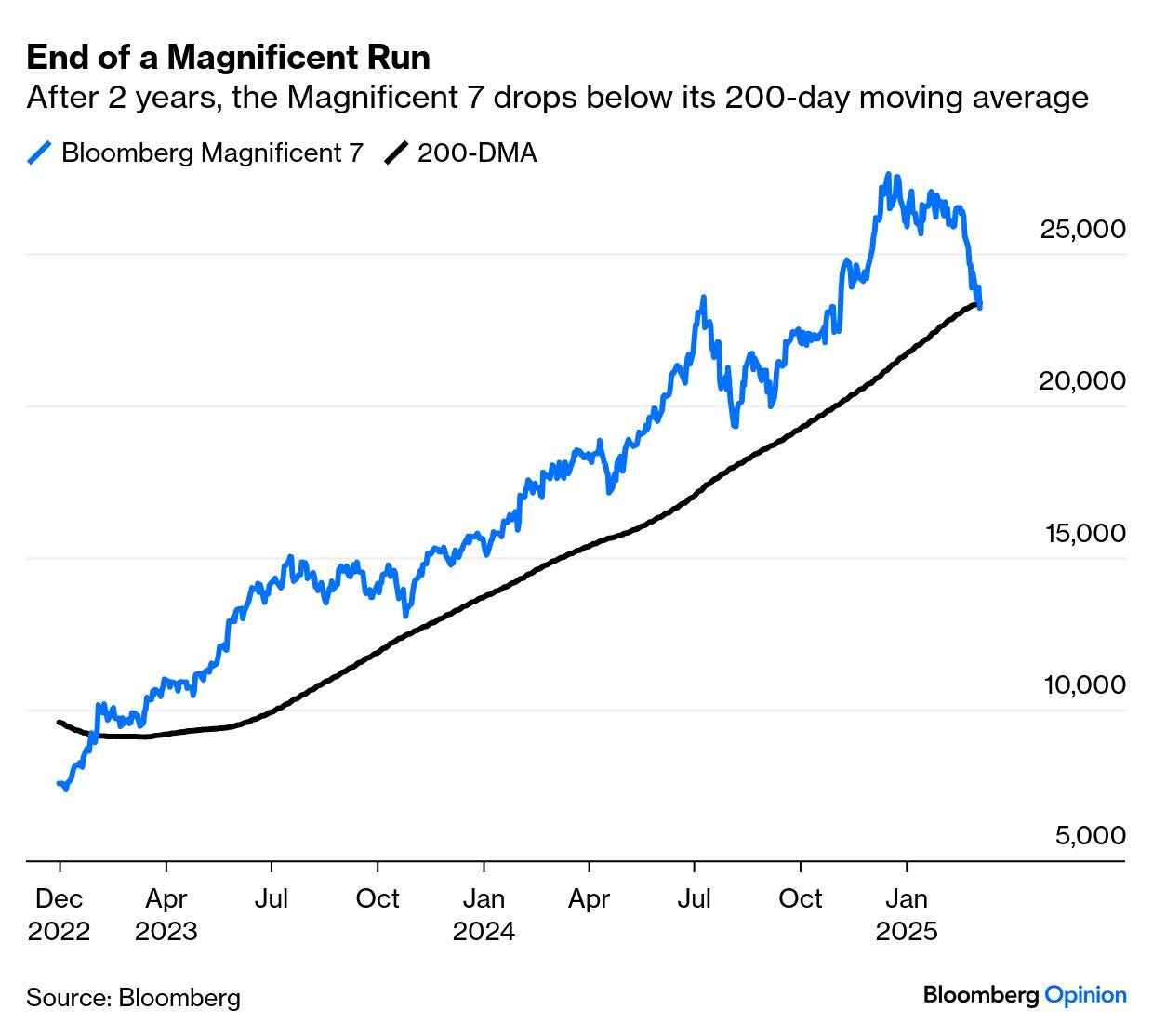

… The cost of tariff uncertainty is growing very visible, most clearly in a continuing sell-off for US stocks, which has now left the Nasdaq Composite down more than 10% from its recent peak (the popular definition of a “correction”). The Bloomberg Magnificent 7 index, including the dominant tech groups, is down 16%, and has just dropped below its 200-day moving average for the first time in more than two years:

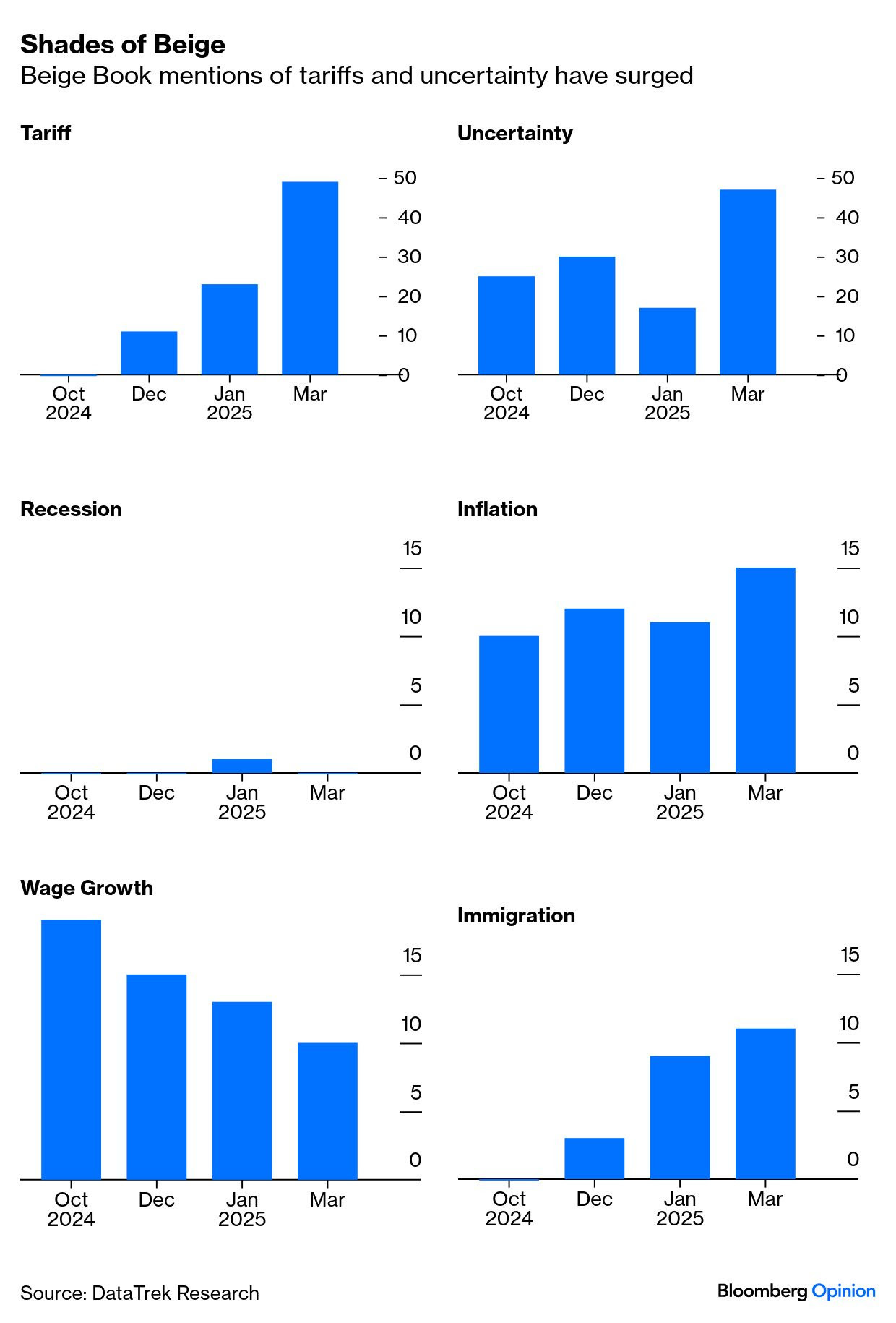

The latest edition of the Federal Reserve’s Beige Book, its qualitative collection of anecdotes garnered by regional branches, was published this week and showed that the central banks’ contacts were talking about tariffs far more than they had in December (when the election result was known). Virtually nobody is talking about recession. The data in this chart counts the number of mentions for each word, compiled by DataTrek Research:

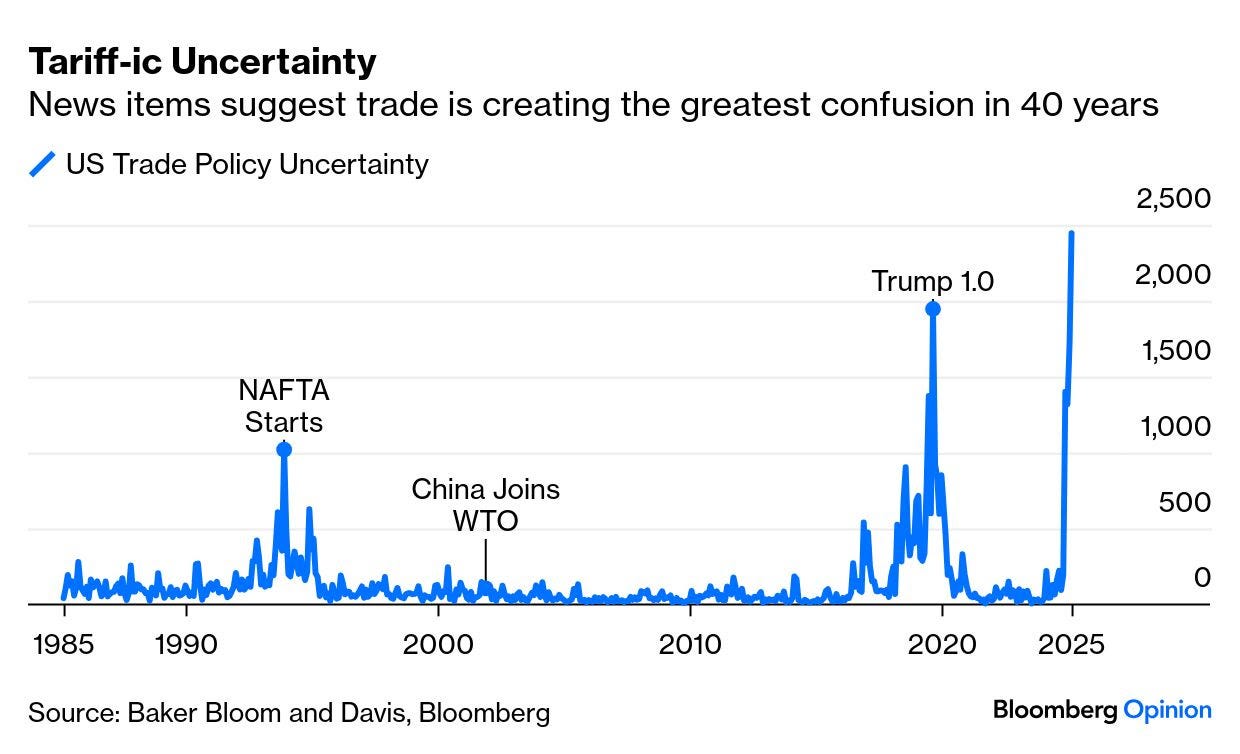

That’s strong prima facie evidence that tariffs are causing worry, and may already be changing executives’ behavior. Moreover, the Baker Bloom and Davis index of trade policy uncertainty, derived from analysis of media mentions, has just spiked to the highest in the 40 years since its inception. Current anxiety dwarfs the concerns that people had as the original Nafta treaty was coming into effect, or during the first Trump administration. China’s entry to the World Trade Organization, with hindsight by far the most significant trade change in this era, didn’t register:

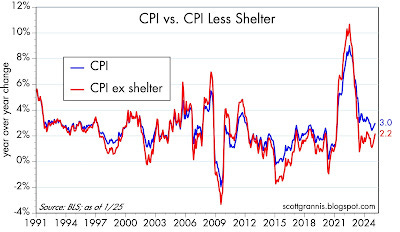

…Chart #9 compares the year over year change in the CPI to the CPI ex-shelter costs. If one agrees that shelter costs as per the government's calculation are overstated, then the CPI has been at or below the Fed's target of 2% since mid-2023.

Chart #9

From the twitter … a reiteration of the ZH chart above …

at JesseCohenInv

This chart is fascinating.

It shows the S&P 500 2018-19 during the first Trump Trade War in green vs. S&P 500 2025 during Trump Trade War 2.0 in red.