Good morning. These morning updates are clearly more for me in an effort to stay connected and, by default, more rear-view mirror looking, than not. That said, along with what happened while we slept AND a few links thru to what the BRAINard said and how SHE defined ‘rapid’ at least as far as the markets are concerned, just a few other items thinking beyond today/this week and perhaps even this year.

First, ALL markets are steel reelin’ and dealin’ with BRAINard comments yesterday

RTRS: Fed's balance sheet runoff will be rapid, Brainard says

… Against that backdrop, I will turn to policy. It is of paramount importance to get inflation down. Accordingly, the Committee will continue tightening monetary policy methodically through a series of interest rate increases and by starting to reduce the balance sheet at a RAPID pace as soon as our May meeting…

stocks down. Bonds down (in price) and the rest, as they say, is history still being written.

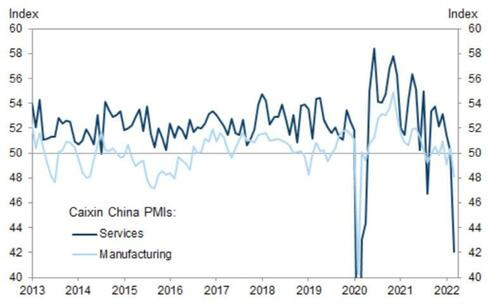

In other news overnight, somewhat related to ‘global’ macro,

China Services PMI Crashes In March As COVID Crisis Worsens -ZH

Said another way, by a large German bank (not on PMI, mind you),

DB Research have released a significant World Outlook document yesterday (link here), in which we’ve updated our views on the global economy and financial markets given developments since the start of the year. In terms of the key takeaways, we’ve downgraded our growth forecasts, with an out-of-consensus view that a US recession is now the base case by the end of next year, since higher inflation will require a more aggressive tightening in monetary policy from central banks, and we now see the Fed moving much faster, with 50bp hikes at the next 3 meetings, and a terminal rate of 3.6% by mid-2023. The outlook has been further dampened by Russia’s invasion of Ukraine, which has pushed up energy prices and led to further disruption for key commodity markets and supply chains.

With the outlook moving in a more stagflationary direction, we expect growth to slow materially in the second half of 2023, tipping the US into recession by the end of that year. Indeed historically, there’s been just 2 occasions over the last 70 years when the Fed has raised rates by 300bps and left inflation on a downward trajectory without causing a recession. And as we’ve written many times in the EMR, the recent inversion of the 2s10s curve has on average preceded the start of a recession by around 18 months (see more in our recent chartbook here). Over in the Euro Area, we’re also forecasting a more aggressive tightening cycle, with the ECB raising rates by 250bps between this September and December 2023. But unlike in the US, we think Euro Area growth will be modestly above zero in the winter of 2023-24. Along with the updated call for US recession, Jim’s also expecting credit spreads to widen out by the end of next year. See the full credit update from him here.

Here is a snapshot of UST rates, prices and moves as of 718a

… And HEREis what another shop says be behind the price action, you know,

WHILE YOU SLEPT Treasuries have extended losses and the curve has rebounded further after yesterday's triumvirate of hawkish Fed speakers (Brainard, George and Daly) have rates on edge ahead of this afternoon's Minutes and promised QT framework reveal. DXY is little changed (+0.07%) while front WTI futures are higher (+1.7%). Asian stocks were lower except in China where they were UNCHD, EU and UK share markets are all in the red (SX5E -1.8%, SX7E -2.9%) and ES futures are showing -0.7% here at 7am. Our overnight US rates flows saw a drift higher in rates during Asian hours with net better real$ buying (10's) seen on our desk- contrary to the price action. During London's AM hours the desk reported relatively balanced flows despite the price action. Asian 2-way flow in the long-end was a feature while some accounts dipped toes into off-the-runs- particularly in the TU and US deliverables sectors. Overnight Treasury volume was solid again at ~160% of average with 30's (231%) and 10's (202%) seeing the highest relative average turnover overnight.

… US News: Treasury Secretary Yellen will appear before a House committee today and will warn of 'enormous economic repercussions' from Ukraine invasion NYT Add declining immigration to problems weighing on the labor market WSJ The US, UK and Australia join to co-develop hypersonic missiles WSJ NY votes to reform bail reform amid rising violent crime WSJ

… Our first attachment shows Bieber's RPM time series for daily futures block trades by DV01. If you squint you can see that yesterday's block flow was the highest in years in DV01 terms... Higher than even during the earliest days of the pandemic rates meltdown two years ago.

… JGB 40yrs closed last night (+6.3bp) up against its 2017 and 2018 high prints- still trying to finally fill a gap created in early 2016 after the BOJ's adoption of QQE and NIRP early that year.

… and for some MORE of the news you can use » IGMs Press Picks for today (6 April) to help weed thru the noise (some of which can be found over here at Finviz).

This will all fit together in the fullness of time (Lacy Hunt’s quarterly should drop any day) but as far as the hear and now and in the Mike Wilson / MS camp, this short comment from BBG on increased equity VOL (and picture) as it relates TO what the Fed heads said just yesterday

… Federal Reserve Governor Lael Brainard sent a $9 trillion bowling ball hurtling through financial market skittles Tuesday, in comments which should really shake investors out of any lingering sense of complacency. She said the Fed would start reducing its bond holdings as soon as next month ``at a rapid pace.'' Alongside over-aggressive rate hikes, a faster-than-expected rundown of the Fed’s giant balance sheet is a second policy move with the potential to destabilize global markets. Not only does it mean a key buyer of Treasuries has disappeared but shrinking bond holdings pulls liquidity from the financial system which can result in higher borrowing costs and spikes in volatility across asset classes. Deutsche Bank estimated its impact through 2023 could be the equivalent of four rate hikes -- that's on top of the near 10 already priced in to markets to next February. When the Fed last reduced its balance sheet back in 2017 and 2018, the rolloff helped fuel a disruptive surge in repo rates, a keystone of short-term funding markets and preceded a sharp selloff in global stocks. A build up in the Fed's balance sheet has been a huge driver of gains in global risk assets in recent years. It stands to reason that a reduction is likely to have the opposite effect.

Prefer a visual of the S&P? BBGs got that (and a few words,

Federal Reserve Governor Lael Brainard’s call for a reduction in the central bank’s balance sheet had a much stronger impact on equities than recent calls for aggressive rate hikes. A look back at the course of share prices and quantitative easing makes it pretty clear why investors are so concerned. Correlation doesn’t necessarily mean causation, but it would seem imprudent to simply set aside the way stocks ballooned over the past decade along with balance sheets, and also how they dropped when global central bank assets declined meaningfully.

At the very least there are reasons to expect such a response. Central bank purchases are supposed to push extra money into the financial system, which would tend to drive up asset prices as the demand represented by all that extra cash chases a less elastic supply of stocks, bonds and other securities. There’s also the fact that QE is designed to repress yields, so an end to that repression would tend to undercut stock valuations. And P/E ratios are still above pre-pandemic record highs.

#GotBONDS ? They are TEETERING, you know. Perhaps setting up the next great DIPortunity …

While I continue to believe that US leads (that saying — as goes America, so goes the world) but this ‘toon from Investing.com does make one pause (again) to consider,

And what, then of all those (of us) depending upon their factories and the importing / exporting of in/de/dis-inflation, etc…clearly I need another gallon of coffee and so … that is all for now. Off to the day job…