Good morning … anyone else notice (care) where 10yy stopped going UP after the rate CUT 2d ago …

10yy DAILY: 3.77 looks to ME to be a level of interest and should be brought in for questioning …

… interesting, too, that momentum (stochastics, bottom panel) have crossed and leaned BEARISHLY and so … move higher (despite / because the news?) should maybe NOT be such a surprise??

… and so, equity markets celebrate, rate cuts (re)calibrate …

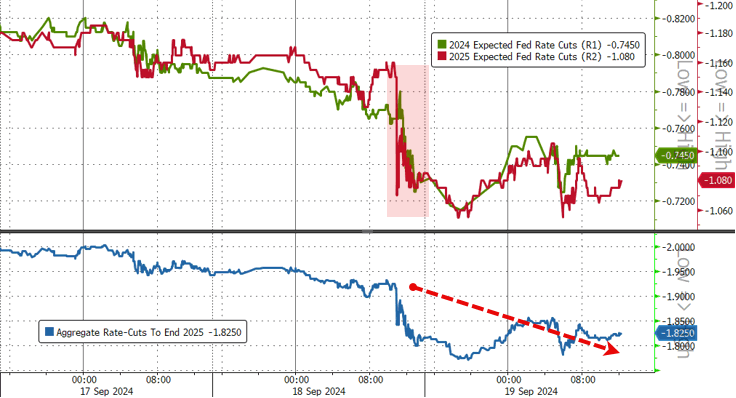

... Interestingly, rate-cut expectations to year-end 2024 (and 2025) are lower post-Fed crisis-cut. The market still expects 3 more cuts in 2024 though (and four more on top of that in 2025)

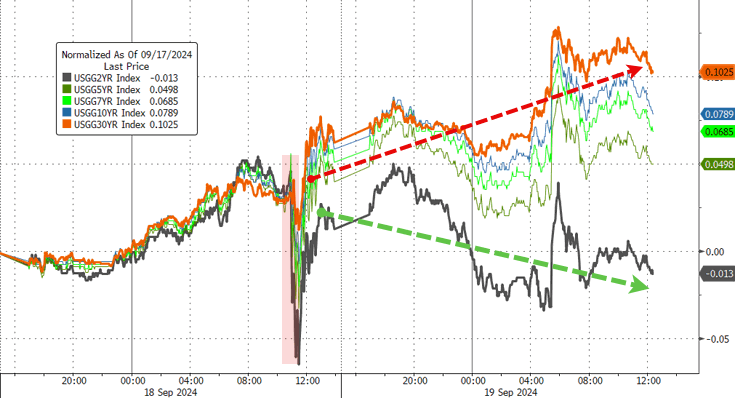

… and so, in any case, more an equity rip yer face off rally as bonds stnading idly by and yesterday (this morning) more about curvature …

… Treasury yields were mixed today with the short-end outperforming...

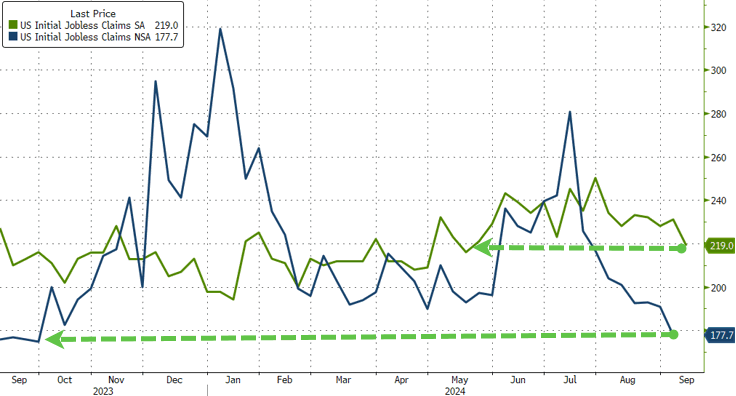

… Now this all was recap as data dust settled … some of said data SHOULD, in theory, be reviewed. EXAMPLE, yesterday’s Initial Jobless Claims — maybe don’t seem to matter BUT … they are for the ‘NFP survey week’ and so … NFP survey week SAYS …

ZH: Plunge In Jobless Claims Exposes Apolitical Fed-Cut 'Policy Error' Further

… Adjusted initial claims tumbled from 231k to 219k (lowest since May) while unadjusted claims continued to tumble to 12-month lows...

… While the official unemployment rate dipped modestly from three-year highs, jobless claims have crashed to near record lows.

Does that really look like an economy that needs a 50bps rate-cut?

As one market veteran pointed out to us this morning, "either The Fed is a bunch of idiots, or this data is total bullshit." Fact of the matter is, Powell even admitted - after bringing up the massive revision to the payrolls data - that it is more likely the latter (bullshit data) than the former (idiots); though we suspect it's a bit of both (blending with some political pressure).

… AND who cares. We get what we get and we don’t get upset. Moving on TO the day ahead and some time for a weekend thought or two before Sunday NFL ticket and for now … here is a snapshot OF USTs as of 656a:

… and for some MORE of the news you might be able to use…

NEWSQUAWK: JPY hit and fixed bid after Ueda, XAU at highs; Fed speak due … Bonds are slightly bid, taking impetus from the BoJ announcement; Gilts initially underperformed vs peers after hotter-than-expected UK Retail Sales … USTs are slightly firmer with specifics light thus far for the US but with action coming from the BoJ; while the decision itself was largely uneventful the presser saw a particularly dovish Ueda. Thus far, USTs have probed but failed to breach 115-00 or, by extension, test yesterday’s 115-02+ top. Fed's Bowman (who dissented at the most recent meeting) is set speak about her decision later.

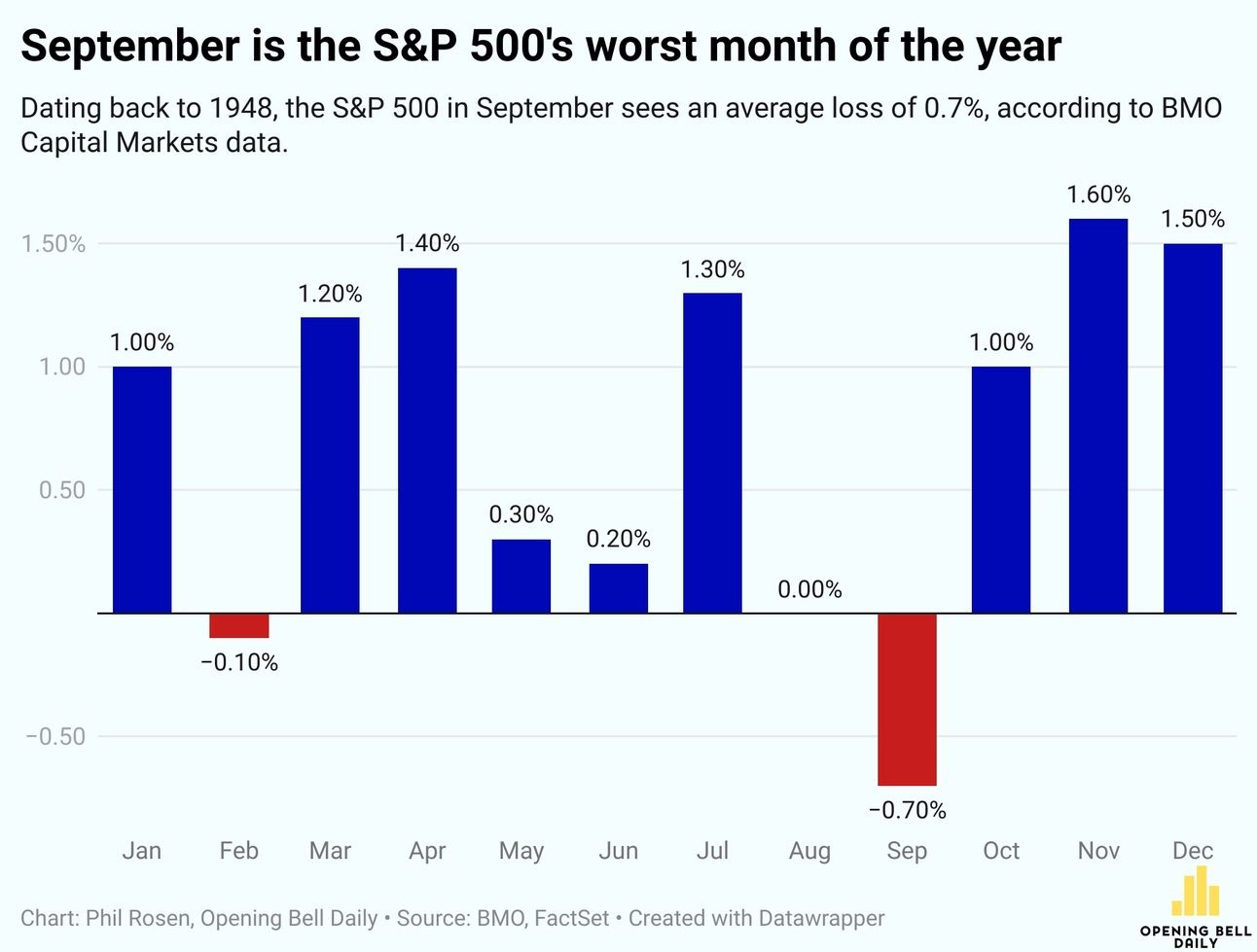

Opening Bell Daily: September, September. Stocks are on track for a rare achievement. Investors can thank the Fed. The 50-basis-point rate cut has juiced markets toward their first winning September in years.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ …

BARCAP U.S. Equity Strategy: Food for Thought: Value vs. Growth, Post-Rate Cut

In past non-recessionary rate cutting cycles, median Value returns surpassed those of Growth immediately after the "first" rate cut (t+1m to t+3m), but inconsistently. Past t+3m, Growth outperformance takes over and with more consistency, i.e. there could be more Growth upside ahead if we are on track for a soft landing.

… post IJC …

BMO: Jobless Claims Drop to 219k during NFP Survey Week

…On net, it was a round of data that offered reassurance that the US economy remains on stable footing for the time being.

… an inflation outlook and a few words on the bounce back …

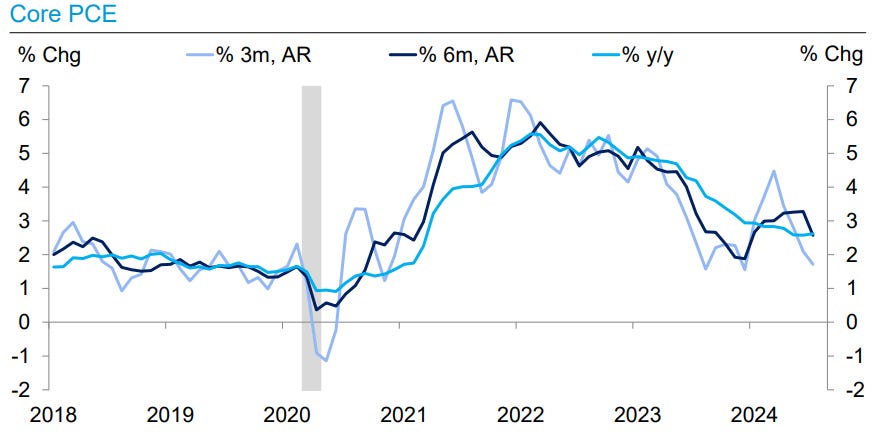

DB: US Inflation Outlook: Inflation downgraded in the dual mandate

…Core PCE seems to be returning to target after a bumpy first quarter

…High inflation risks receding for professional forecasters

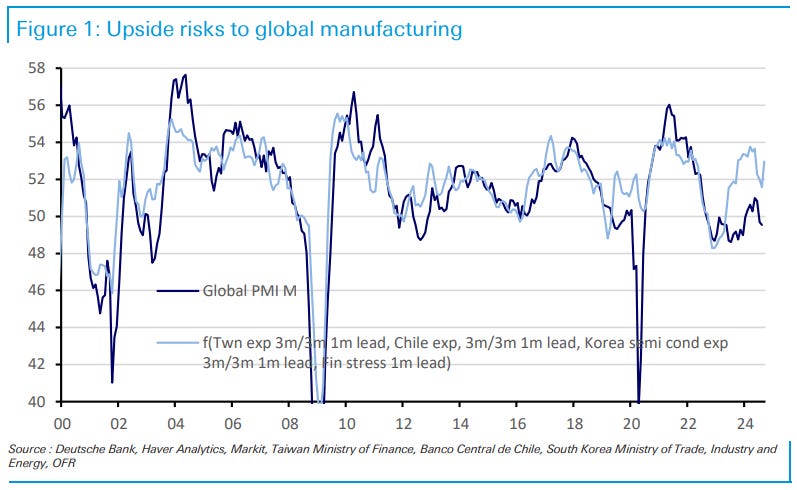

Leading indicators suggest some upside to global manufacturing after a soft patch that lasted a few months. The potential turnaround in global manufacturing reinforces the signal sent by the Fed and ECB bank lending surveys which are both consistent with growth at or above potential. From a pricing perspective, the terminal rate currently priced is below plausible estimates of neutral (3.25-3.50%), while the term premium remains low. Finally, some positioning indicators suggest potential vulnerabilities to long UST positions. Taken together, the macro environment, current pricing and positioning support a mildly bearish duration view in the US.

… here’s a few words on WHY rate cut = bad (for bonds) …

… The answer lies in a third, more debatable, aspect of policy confirmed by the Fed yesterday, which in my view is also very bearish for bonds: the Fed’s estimate of the “neutral” policy rate—that will neither stimulate nor deflate the real economy—seems far too low. Yesterday’s SEP showed a median of 2.9% for this “longer run” level of Fed Funds. However, the estimates of different Federal Open Market Committee members ranged from 2.4% to 3.8% on this issue. In my view, the high end of this range is likely to be proved right. The Fed’s neutral rate estimate of 2.9% effectively assumes that the historically unprecedented low interest rates of the post-2008 crisis period were not a temporary aberration, but a permanent “new normal” that will again become the equilibrium state of the world economy in the years and decades ahead. This seems unlikely, considering that the deleveraging that followed the GFC is over, that US companies and households now have historically strong balance sheets and, most importantly, that long-term changes in the capital intensiveness of industry, in geopolitics, in fiscal policy and in demographics are all moving the global economy away from excess savings and secular stagnation towards higher investment and lower savings.

Another way of seeing the same anomaly is to consider the real neutral rate after subtracting expected inflation. The Fed’s assumption of a 2.9% neutral rate becomes a real rate of 0.9% if we subtract 2% PCE inflation. But as argued above, 2% is now a floor for inflation, not an average, and CPI, not PCE, is the inflation benchmark used for key economic decision-making, for example in cost-of-living adjustments for Social Security payments, and wage contracts and in inflation-linked bond payments. If we, therefore, subtract the average 2.9% rate of CPI inflation posited above from the Fed’s 2.9% median estimate we get a real neutral rate of zero. This turns out to be much lower than the real neutral rate assumed by the Fed in the decade between 2008 and 2018, which varied between 0.5% and 4% in real terms after allowing for the 40bp difference between CPI and PCE inflation.

Putting together these three observations, which have now been confirmed by the Fed’s actions as well as its words, adds up to a clearly bearish outlook for US bonds. My longstanding view since the 2022 energy shock has been that the US 10-year treasury yield will trade in a range of 3.5% to 5.5%. When yields approach the bottom of this range the risks are strongly skewed in the bearish direction. Falling short-term interest rates, far from helping bonds, could coincide with rising bond yields as the yield curve disinverts and then steepens. This now seems the likely prospect for the weeks and months ahead.

… Here in this next note, once again I detect more than just a note of saracasm from Paul Donovan … almost a note of true disdain for our system in its beauty (as well as its faults) … not sure WHAT it is but some of the times, I’m just NOT a fan …

US politics keeps resurrecting ideas from the 1970s—most recently questioning central bank independence. Some economists argue that Federal Reserve Chair Powell is the worst central bank head since Fed Chair Burns (who served US President Nixon). Burns was independent in theory, but not in practice. Former US President Trump suggested this week’s rate cut was political in nature, and that the Fed should be more under his control. US President Biden defended Fed independence yesterday.

Politically, voters are unexcited about central bank independence (many US voters do not know what the Fed does or who Powell is—at times economists would regard such ignorance as bliss). Economically, independent central banks were the main reason inflation was tamed after the 1970s. Markets appear not to be taking threats to Fed independence seriously—if they did, the implications could be significant.

Japan’s consumer price inflation data was unexciting, rising very slightly as markets expected. German producer price inflation was a little stronger, with rising consumer goods prices contributing…

… really don’t care whether or not he’s a fan of Trump. Didn’t ask and frankly, should NOT be able to tell … NOT what I’m looking for at O’Dark Thirty from an economic write up … oh well.

Wells Fargo: August LEI: Light at the End of Tunnel?

Summary For now, the best that can be said about the Leading Economic Index is that the declines are getting smaller, but positive developments with interest rates point to some potential relief from rate-sensitive parts of the economy that have been weighing on this barometer.

…There is light ahead in the tunnel. The interest rate spread component of the LEI has been a consistently negative contributor to the index for the past 21 months, subtracting an average of 0.13 percentage points in each. However, the component, which is calculated as the spread between the 10-year Treasury yield and the federal funds rate, has the potential to be a positive contributor in the not so distant future. With the Federal Reserve lowering the federal funds target range by 50 bps yesterday and the yield curve starting to disinvert, the spread between the 10-year yield and the federal funds rate has narrowed thus far in September.

Now that monetary policy easing has begun, the LEI should get some breathing room. In addition to a brighter outlook for the interest rate spread, lower rates should provide some relief for the manufacturing sector, which is an area that has weighed heavily on the LEI through the ISM new orders index, new orders of core capital goods and the average weekly hours worked by factory workers. The interest rate sensitive sector has stagnated in recent years, but it should be one area of the economy that will benefit as rates decline. Even as the outlook for the LEI improves, the index has not provided an accurate signal of the strength of the business cycle and has overstated weakness in the economy for two and a half years …

… AND …

Yardeni: Powell & Co. Slams The Pedal To The Metal

Wow, the Fed lowered the federal funds rate (FFR) by 50bps yesterday and the economy is already responding. Jobless claims fell and two regional business surveys strengthened in September, while the Coincident Economic Index rose to a new record high, though in August!

We are kidding, of course. But perhaps the economy didn't need to be stimulated so much. It appears Fed officials got their soft landing but feel a need to act fast to avert a hard landing. The most immediate impact of the Fed's easing move was to send stock prices soaring today to new record highs in a way that is reminiscent of the late 1990s meltup. Consider the following:

… (4) Bond yield. The 10-year Treasury yield is up 13 bps from its Tuesday closing level to 3.75% today (chart). While TIPS yields are edging higher, nominal Treasury yields are climbing even more, suggesting that the bond market is less convinced that inflation will be lower in the future now that the Fed is slamming the pedal to the metal.

(5) Yield curve. The US Treasury yield curve spread between the 10- and 2-year bonds steepened further into positive territory, rising to 0.13 percentage points early today (chart). The current move confirms that the bond market doesn't think the economy needed yesterday's 50bps jolt.

… And from Global Wall Street inbox TO the WWW,

Here’s some GOOD news. Gas prices are falling …

AAA: Gas Price Decline Slows, But Likely Won’t Stop

…According to new data from the Energy Information Administration (EIA), gas demand increased slightly last week from 8.47 million b/d to 8.77. Meanwhile, total domestic gasoline stocks remained flat at 221.6 million barrels, while gasoline production increased last week, averaging 9.7 million barrels per day. Lackluster gasoline demand and low oil costs will likely keep pump prices sliding.

Today’s national average for a gallon of gas is $3.22, 19 cents less than a month ago and 66 cents less than a year ago.

… got this going for us … but then maybe that ‘narrative’ — good is good and bad is bad is all wrong?

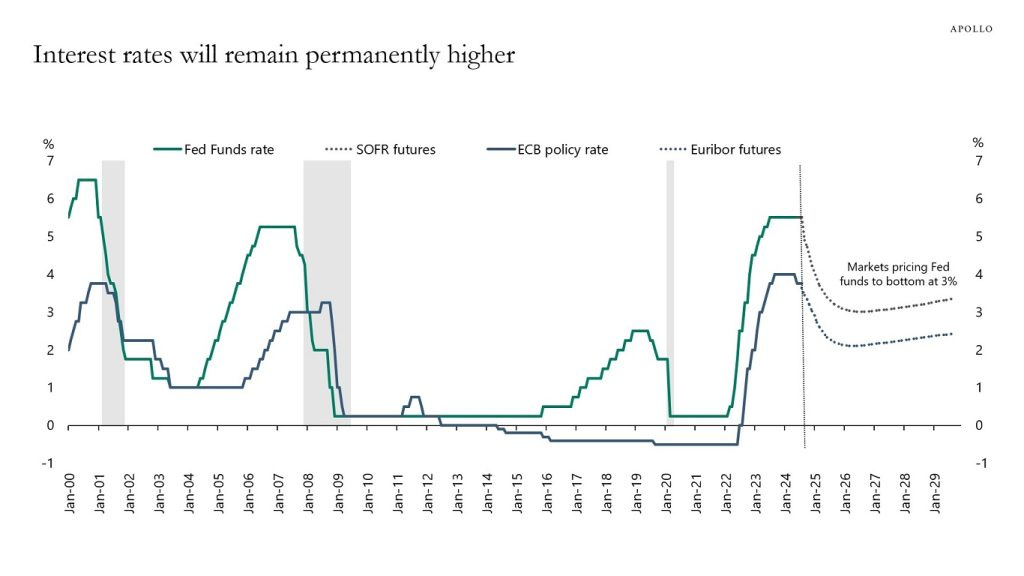

Apollo: The Market Narrative Is Almost Always Wrong

Since the Fed started raising rates, the terminal rate has fluctuated between 2% and 4.5%, see chart below.

That’s a pretty wide range of outcomes.

The bottom line is that the market narrative at any point in time is almost always wrong.

Source: CME, Haver Analytics, Apollo Chief Economist

…A soft landing remains our base case, driving our broadly constructive view on direct lending. Our expectation remains that it will take longer for inflation to come down to the central bank’s 2% target range, and as a result the curve will continue to steepen, meaning long rates are going to decline less than short rates. The combination of a strong economic backdrop along with elevated yields further out the curve is favorable for high-quality private credit. With private credit spreads of 5%-6% and Original Issue Discounts of 2% factored in, investors should still be able to command solid returns over the coming years. We continue to believe that the opportunity set to lend to bigger businesses on a first lien, senior secured basis at elevated yields remains attractive.

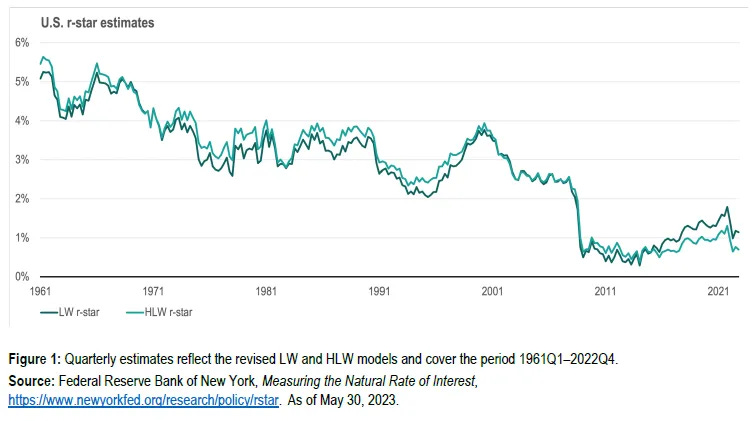

… AND From John Authers / BBG, more on the un prove’able R* so in theory EVERYONE is accurate as this is simply a concept for those up in the ivory tower (and those who wanna be right up there next to ‘em) …

Bloomberg: With more cuts coming, it's time to get R*

The neutral real rate of interest is back in focus as the shocks from the pandemic and 2008 are finally being worked out of the financial system.

… Demographics on their own have ensured a decline in R*, as has disappointing productivity growth. The Global Financial Crisis administered a massive further blow downward. A number of estimates are out there. Vanguard Group’s chief economist Joe Davis shows how two models from the New York Fed have measured the neutral rate going back to 1960:

There’s room for argument over whether rates should have stayed as low as they did for so long after the GFC, but the basic point that the crisis pushed down the neutral rate is hard to contest…

"The 2% inflation target isn't an average it's now the floor" (of inflation target). Haunting Words :(