… I thought the Fed’s gonna cut (bond jockeys still seem to support that message) and bad = good and so, all markets just … go UP?

Apparently Team Rate CUT (see HIMCOs latest quarterly HEREfor example) on to things — early as usual — and data been signaling this all for awhile.

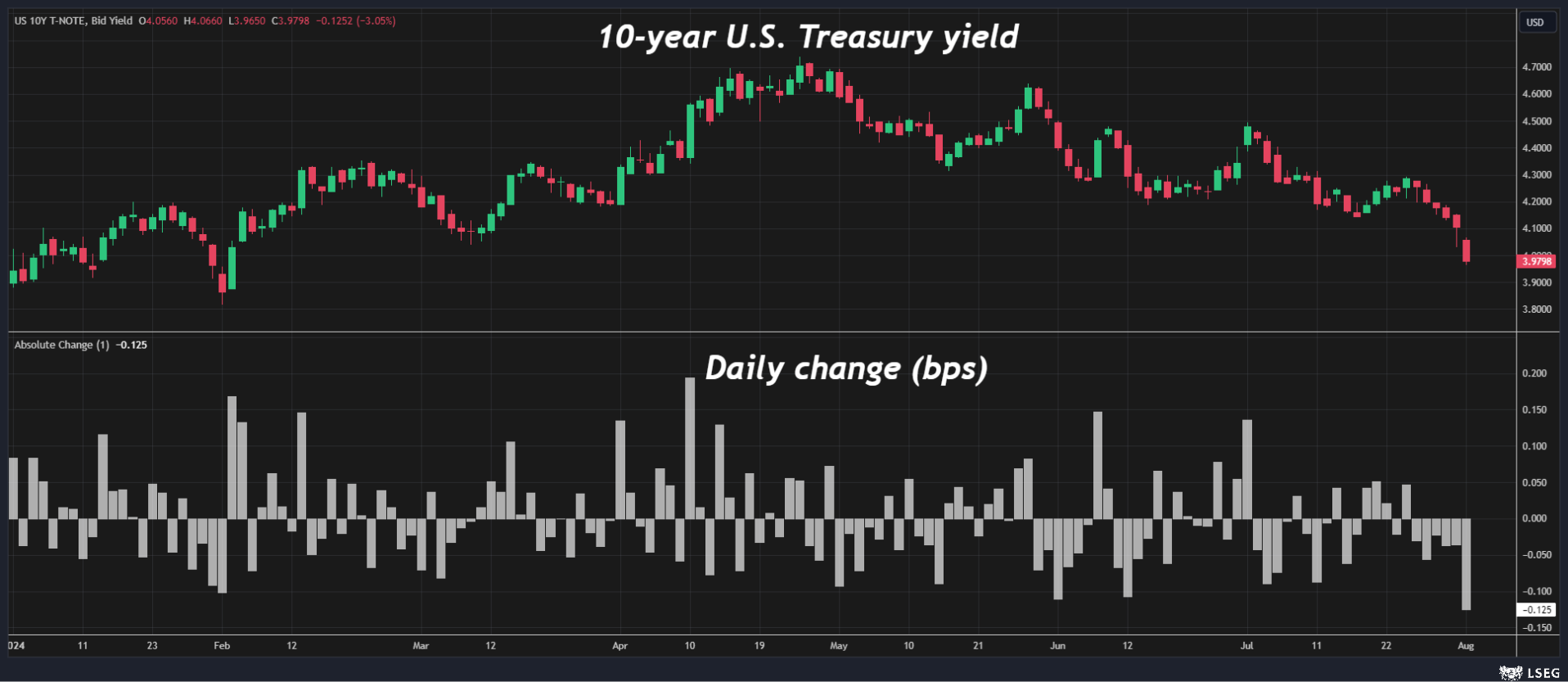

Yesterday was an interesting session and to synthesize things a bit, and as always, I was taken by the drop in 10yy (largest daily drop this year!!) noted in visual courtesy of RTRS …

… The 10-year U.S. Treasury yield tumbled 13 basis points, its biggest one-day fall this year, and is now below 4.0%. Never mind the great rotation out of Mega Tech into small caps, investors seem to be rotating out of stocks and into the safety of U.S. Treasuries…

… In as far as the totality of the picture and ahead of this mornings NFP, well …

ZH: Stocks & Bond Yields Puke Amid 'Most Volatile Earnings Season' Since GFC

… Bad (macro) news was bad news today as jobless claims surged, manufacturing surveys slumped, and construction spending tanked, sending rate-cut expectations higher...

Meanwhile, back at the ranch, global CBs continue to distance themselves from the FOMC …

ZH: Bank of England Cuts Rate to 5.0% In "Finely Balanced" 5-4 Vote, Offers No Signals On Next Moves

… which was then chased down by a nice (?) IJC and Mfg data, at least as far as the FOMC and Team Rate CUT are concerned …

ZH: Initial Jobless Claims Surge To 12-Month Highs ZH: "Near Stalling Of Production" - US Manufacturing Surveys Collapsed In July

… in other words, BAD is the new GOOD and so USTs with a ‘3 handle’ are the new ‘4 handle’ of yester(day/week/month and H1, 2024) …

10yy MONTHLY …

… momentum leaning towards but not yet extremely overBOUGHT as it drops below 4.00% — important psychologically but otherwise, not much signficance …

… I’ll likely have something more to say over weekend after NFP and the pricing mechanism — UST market — makes some decisions. For now and ahead of this mornings NFP …

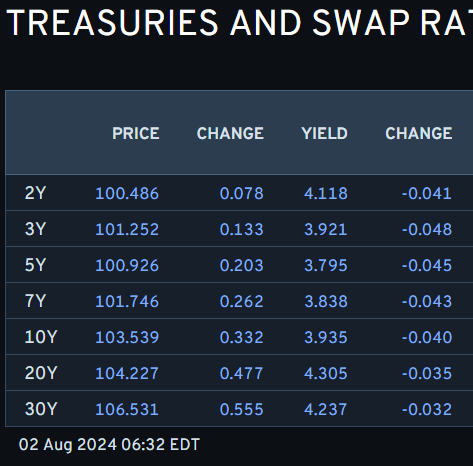

NEWSQUAWK: US Market Open: ISM-sparked pressure added to by significant INTC pressure, NFP ahead … Fixed benchmarks continue to rise with yields pressured across the curve into Payrolls and the first post-FOMC Fed speak … USTs as high as 113-00, extending on Thursday’s 112-26 peak with yields pressured across the curve with 3s through 10s now all sub-4.00% and the 2yr as low as 4.10%.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ and how they are celebrating HIGHER IJC (and so, bad > worse = GOOD at least as far as Team Rate CUTS goes…)

BARCAP: Initial claims likely overstated by seasonal factors

Initial jobless claims increased last week, driven in part by outsized gains in Michigan and Massachusetts. Last week's reading of 249k was 14k above where the index stood in the prior week. NSA data continue to return towards historical trends, indicating residual seasonality distortions in the SA data.

BARCAP: ISM manufacturing: Softer print exaggerates downside risks

The ISM manufacturing composite dropped 1.7pts in July, to 46.8, near the lower end of the soft readings seen since late 2022. The employment component was especially weak, falling to levels last seen in summer 2020. However, we continue to caution that the ISM has been misleadingly soft for some time now.

BARCAP: June construction spending continues slide amid broad-based weakness

Construction spending fell 0.3% m/m in June, driven by broad-based declines across private and public spending. Today's data come alongside a sharp revision to April spending, up to 1.3% m/m from 0.3% m/m prior, and a downward revision to May spending.

At its August meeting, the MPC cut Bank Rate by 25bp, with a 5-4 vote, but kept a cautious tone on the path of policy hereafter. We continue to expect the next 25bp cut to come in November, with further cuts taking Bank Rate to 3.75% by August next year. We also expect £100bn of QT to be announced in September.

BARCAP U.S. Equity Strategy: Food for Thought: When Bad News is Just Bad News

SPX reaction to the July ISM manufacturing composite was the worst since April 2018, and rarely seen over the last decade. This was in spite of a number of potential upside catalysts heading into Thursday. Barclays economists warn against reading too much into the print; still, macro jitters are on the rise in equities.

BMO: Jobless Claims Highest Since August 2023 at 249k -- 10s reach 4.014%

… While there wasn't anything within this morning's data that should directly influence the market's expectations for tomorrow's NFP print, when combined with ADP and the Fed's renewed emphasis on its dual mandate, there is unquestionably a growing sense of apprehension on the employment front…

BMO: ISM Manf. Disappoints -- Triggering 3-handle 10s

… In the wake of the releases, 10-year yields broke below 4.0% to trade at 3.976%. While the sustainability of sub-4.0% 10-year yields will ultimately come down to Friday's employment report, for the time being, we are unwilling to fade the price action currently underway …

BNP: Bank of England: A first cut. No commitment on a second.

KEY MESSAGES

Thursday’s decision to cut Bank Rate by 25bp to 5.0% was followed by a relatively hawkish Bank of England press conference. This suggests to us that the MPC members for whom the decision was a close call may prefer a relatively gradual pace of monetary policy easing from here.

We are a little more optimistic than the BoE on services inflation over the coming months, and so we continue to hold our view that it will cut again in September. However, we see risks skewed towards a delay until November.

The BoE did not explicitly push back on market pricing, however, a medium-term inflation forecast that undershoots the 2.0% inflation target is to us an implicit sign that the BoE may see the neutral rate as a little lower than markets think.

FX: With event-risk behind us we take profit on our short GBPAUD trade idea. However, in the near term we see more risks of further weakness in the GBP given a dovish BoE, bullish GBP positioning and potentially looser fiscal policy than previously expected.

While techs on US equities are bearish, we think that moves lower could be limited in the short term. We see support levels nearby, and the short lived break below 55w MA in April gives us more reason to be cautious. We keep a close watch on weekly closes, given the event risks ahead, to evaluate further.

Watch support at:

ES1: 5334-5368 (May and April highs), followed by 5206 (May 31 low)

NQ1: 18709 (March highs), followed by 18241 (May 31 low)

For the past year and a half, leading indicators were consistent with a pick up in global manufacturing. Over the past couple of months, these leading indicators have turned suggesting that the momentum in global manufacturing is fading.

This is helpful in setting the global macro environment as potential distortions to the US data are endlessly debated (eg. is the rise in jobless claims impacted by one off events?). This global backdrop argues in favour of taking more seriously the weakness in some of the US data.

… The risk-off mood saw 10yr Treasury yields fall beneath 4% yesterday, while 2yr yields have traded as low as 4.11% overnight, their lowest since May 2023 before settling back to nearly unchanged in Asia at 4.14%. This comes as investors price more and more rate cuts for the year ahead. Futures are now pricing in over 175bps of Fed rate cuts over the next 12 months, which is the sort of pace that we’ve only seen in a recession in recent cycles. In addition, there was even mounting speculation the Fed would kick off the easing cycle with a larger 50bp move in September, with futures pricing in 33bps of cuts at that meeting, up +3.3bps from the previous day…

… In terms of the data responsible for the equity falls and big bond rally, there were two main culprits. The first were the weekly initial jobless claims, which rose to their highest in nearly a year, coming in at 249k over the week ending July 27 (vs. 236k expected). And on top of that, the continuing claims for the previous week came in at their highest level since November 2021, at 1.877m (vs. 1.855m expected). Now admittedly, some of that increase in continuing claims was because of Texas, which was recently impacted by a hurricane, so the underlying trend may not be as bad as that looks. But even so, it added to the trend of deteriorating labour market data, which has led to growing concerns that the Fed’s restrictive policy is starting to create more negative outcomes.

That narrative then got a further boost from the ISM manufacturing, which fell to 46.8 in July (vs. 48.8 expected). That’s the lowest it’s been since November last year, and the details in the subcomponents weren’t particularly good either. For instance, the employment print fell to just 43.3, which is the lowest since June 2020 when the economy was still suffering from the impact of the Covid-19 pandemic. So there was little respite for those seeking a more bullish narrative on economic performance. However to put things into some perspective, yesterday did see the Atlanta Fed’s GDPNow estimate for Q3 fall but from an annualized rate of 2.8% to a still decent 2.5%.

The US employment report for July is due. Like Orwellian newspeak, this can often mean the reverse of what it says it means. The household and establishment surveys portray contrasting pictures of employment (and both have shocking response rates). Immigration, self-employment, automation, and switching to higher quality jobs all play a role in messing with the data.

The broad picture is of a cooling US labor market, without any reason for fear of unemployment to increase. Hiring seems to be slowing but firing is not a widespread concern. A neutral labor market merits rate cuts—because rate cuts are not an economic stimulus if they are primarily matching the decline in inflation (and keeping real interest rates neutral). This is one reason the Federal Reserve is now late in lowering rates…

Wells Fargo: ISM's Grim Message: Diminished Activity Without Lower Prices

Summary It has been gloomy for two years in the manufacturing sector, but today's ISM report shows that various measures of activity have sunk to levels not seen since the initial arrival of the pandemic. Most troubling is that this suffering comes without the merit of lower prices.

Wells Fargo: Firm Productivity Gains Helping the Inflation Fight

Nonfarm labor productivity increased at a stronger-than-expected 2.3% annualized rate in Q2, bringing the year-ago change to 2.7%. The pickup helped tamp down growth in unit labor costs. Unit labor costs are now growing less than 2% on trend and provide further evidence that inflation pressures from the labor market are easing.

Wells Fargo: Bank of England Joins Central Bank Rate Cut Club

Today was a good day for the diehard hard-landers and the "stag-disinflationists." They're probably high fiving each other. We are in neither camp–we expect a continuation of “immaculate disinflation,” i.e., a growing economy with subdued inflation. We're high fiving over today’s productivity and labor costs report.

In any event, bond investors are certainly enjoying themselves; the 10-year yield fell 12 basis points to 3.98% and is now down more than 60bps in the past 3 months. The 10-year TIPS yield slid below 1.8% to its lowest since February (chart).

Are we on the verge of a recession, or in one now? We don't think so–especially as the Fed is preparing to cut interest rates to stymie one anyway. But stock investors might be reconsidering whether the odds of a recession are increasing. Let's review some of the data that jolted markets today:

(1) Unemployment claims. Initial claims increased by 14,000 to 249,000 (sa) in the week ended July 27 while continuing claims rose by 33,000 to 1.88 million in the week ended July 20 (chart)….

… And from Global Wall Street inbox TO the WWW,

AAA: Gas Prices Tumble as a Storm Looms, and AAA Adds EV Charging Data

WASHINGTON, D.C. (August 1, 2024)—The national average for a gallon of gas dipped four cents since last week to $3.48. The drop comes as a tropical wave with storm-forming potential is slowly approaching the Caribbean Sea. Should it enter the Gulf of Mexico, expect oil prices to move higher.

Bloomberg: 5 Things You Need to Know to Start Your Day: Asia

… The mood in US stocks has rapidly soured after Thursday’s weak American economic data. Curiously, bad news is becoming bad news for equities as fears of a central bank policy mistake rise.

It’s too early to tell if a bigger change of regime is afoot in the stock market, but the most recent session marked a departure from the “bad news is good news” framework in which equities have traded for much of this year. Stocks have typically rallied as a widely watched index of economic surprises fell, presumably because it increased the odds of the Federal Reserve cutting interest rates. But with the Fed so far standing pat in the face of deteriorating data, there’s growing concern in some quarters that that it’s falling behind the curve and any rate cut may arrive too late to contain the economic, and profit, damage.

The swoon in small caps is telling in that regard. Shares of smaller firms are more sensitive to economic activity weakening so they bore the brunt of the selloff Thursday. The Russell 2000 fell more than 3%, its second-worst drop this year.

In the S&P 500, defensive sectors such as real estate, utilities and consumer staples held up in the green despite the broader index’s drop. This also suggests that growth fears are starting to emerge.

Bloomberg: Markets now fear the Fed's waiting game is too long (Authers’ OpED)

What a difference a day makes. After rising on expectations of a September rate cut, stocks sell off after a slew of data points to recession…

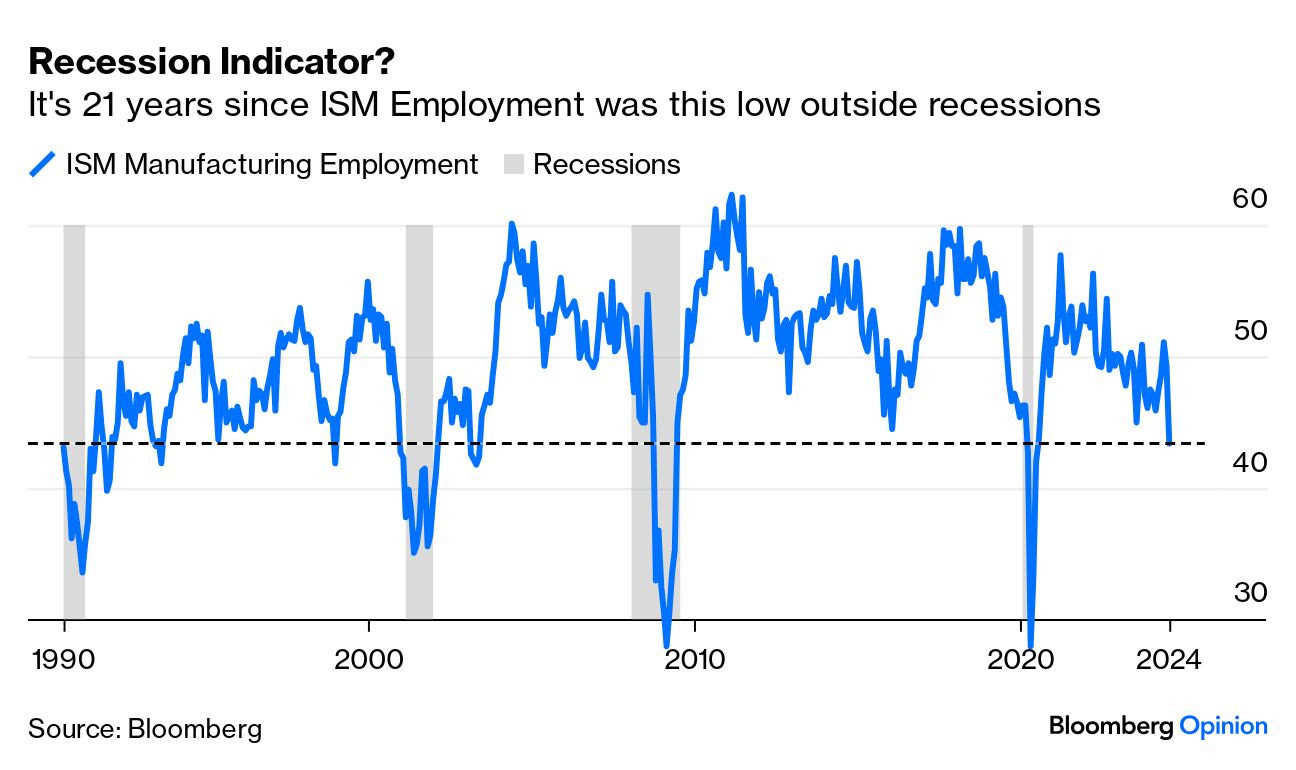

… Meanwhile, the monthly ISM survey of supply managers in the manufacturing sector was horrible. Notably, the diffusion index on manufacturers’ plans for employments is its lowest since the beginning of the pandemic. It’s 21 years since it last dropped to such a level outside of a recession (although there were a few more incidents during the 1990s):

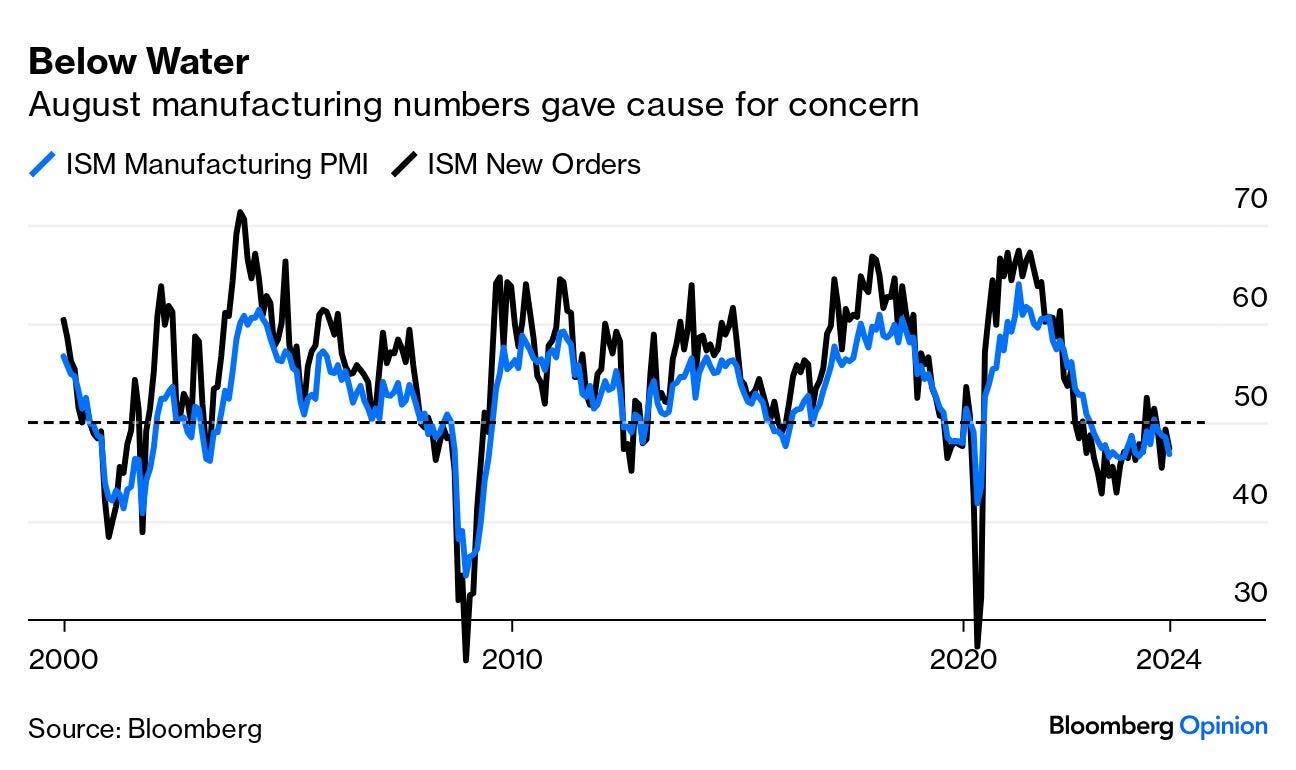

The headline manufacturing PMI, and the new orders reading that is taken as a good leading indicator, both slipped ominously into negative territory. (In theory, any number below 50 means recession rather than contraction):

ING: US slowdown fears heighten the odds of Fed rate cuts

Buisness surveys are not looking good. Today's manufacturing ISM looks particularly soft with the employment metrics looking especially poor. The Fed signalled the potential for a September rate cut, but today's data has given the market even greater faith the Fed will loosen monetary policy with the pricing now in excess of 75bp of cuts this year

Paulsen Perspectives: Bond Yields Feeling that Gravitational Pull How low could the 10-year Bond Yield decline if the Federal Reserve finally removes a unique and artificial yield barrier?

… Charts 1 and 2 demonstrate that bond yields were tied closely to price pressures as inflation accelerated between mid-2020 to mid-2022. But since inflation peaked, bond yields have ignored moderating inflation and continued climbing. Why have bond yields risen as the annual CPI inflation rate has declined from 9.1% to 3% and while U.S. commodity prices have collapsed by over 30% from their high two years ago? And how much longer can inflation keep heading south while bond yields stubbornly stay elevated?

RBA: Building Blocks of Fixed Income: A Macro Framework

… The bulk of fixed income returns can be explained through two macro drivers: credit exposure and interest rates exposure. For each of these return drivers, investors must make critical decisions around allocation (how much exposure) and selection (how you get those exposures), depending on the macro backdrop…

… Today’s fixed income investors are faced with two dilemmas:

Because corporate profit growth has been so strong, fixed rate corporate bond spreads are historically tight, which creates little opportunity from an overweight allocation. (Chart 1)

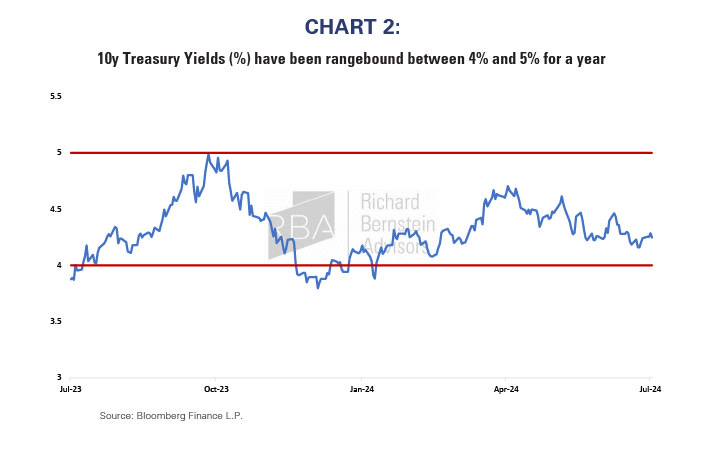

Interest rates may be rangebound due to (1) unclear economic growth, (2) a potential Fed cutting cycle and (3) structurally sticky inflation. (Chart 2)

Until this dynamic changes, traditional allocation opportunities within fixed income appear somewhat limited. So, what is an investor to do? This is where selection comes into play. Through the optimization of interest rate and credit risk, as well as by leveraging investments outside the conventional Bloomberg Aggregate Index, we have identified three attractive ways to take advantage of credit and duration selection opportunities:

Gain exposure to healthy corporate profit growth and higher yields through BBB CLOs. BBB CLOs have default risk of single-A corporates but are relatively cheap and deliver the potential for both income and price appreciation.

Get interest rate exposure where income is highest. By owning the long end and the short end (the two highest yielding parts of the treasury curve) simultaneously, we can maximize yield without taking too much or too little duration.

Position for further curve steepening. We believe yield curve normalization over time will generate alpha – either as the Fed cuts interest rates, sending the curve steeper – or as inflation accelerates, sending the curve steeper. By owning steepeners through Exchange Traded Funds (“ETFs”) that utilize options, we can also capture an increase in volatility.

Today is a time where emphasizing selection within fixed income is necessary to capture alpha. Eventually, when spreads widen and economic growth begins to break one way or the other, we anticipate that our return will increasingly stem from sector allocation decisions. Until that time, however, fixed income portfolios need to be nimble and creative to weather what could be a tricky second half of 2024.

at sstrazza

I have no idea what to make of today's price action... but, I do know that this is how bad things begin...

Credit spreads making a big move today. Biggest daily spike since January. Hitting highest level since February.

* $IEI$HYG is a crude measure for credit spreads *

… I’ll HOPE to have more over weekend including a bit more of a look at some yields / levels (daily / weekly / monthly) especially as the WEEKLY price data may / may not inform a view and shape shift the narrative AFTER the mornings JOBS data.

And on THAT note, how I think Team Rate CUT is expecting jobs report to look …

I'm back!!! I move for 3 days and WTF gold's closing in on $2,500, Q is in Correction, and yields are tumbling! I've had a few strange but confirmed intuitions this wk, I can't view the 'screens' for 3 days and everything goes Apesh!t! Don't unsub me if I miss a few more posts next wk I'm far beyond Living in a Suitcase currently but it's All Good! Long story :)

{kind=link}

{kind=link}

I'm back!!! I move for 3 days and WTF gold's closing in on $2,500, Q is in Correction, and yields are tumbling! I've had a few strange but confirmed intuitions this wk, I can't view the 'screens' for 3 days and everything goes Apesh!t! Don't unsub me if I miss a few more posts next wk I'm far beyond Living in a Suitcase currently but it's All Good! Long story :)

If I could get a copy of the “BARCAP: US Equity strategy” that would be greatly appreciated! If not I understand as well