while WE slept: Bonds bid following JPOW; Trump trade (bull / bear steepener?); "The earlier reactions point to a potential increase of ~15bp in 10y UST…" -DB; "Why wait?" -GS

JPOW has spoken and the bond market continues to listen … Here’s a look at 7yy (for no apparent reason other than I offer a more comprehensive and techAmental look at 2s, 5s, 10s and 30s below!)

7yy: oversold momentum can be worked off by a trade HIGHER in yields OR more simply, time at a price … it would seem to me that the way things ‘feel’ out there right now is that time at a price is more / most likely …

… perhaps ReSale TALES will have something to say but …

… Would ALSO seem to me that JPOW taking center stage at the moment and is more powerful than Trump trades of bigger deficits and BEAR steepener (some going as far as saying Trump trade = 10yy approx 15bp HIGHER next few days) and so, on JPOW yesterday

Fed Watch Advisors Notes: Powell repeated no signals would be given today. That would normally be a boring message. But Powell did 'signal' by saying that the last three CPI reports “do add” to his confidence. The market did not wait and priced the probability of a rate cut in September over 100% (Figure 1). The Fed Index—the AI-driven filter of Fed news—jumped on Powell’s headlines perceived as “dovish”. The market has now fully priced a Fed providing forward guidance at the July meeting…

Figure 1: The Fed Index and Probability of a September Cut (%)

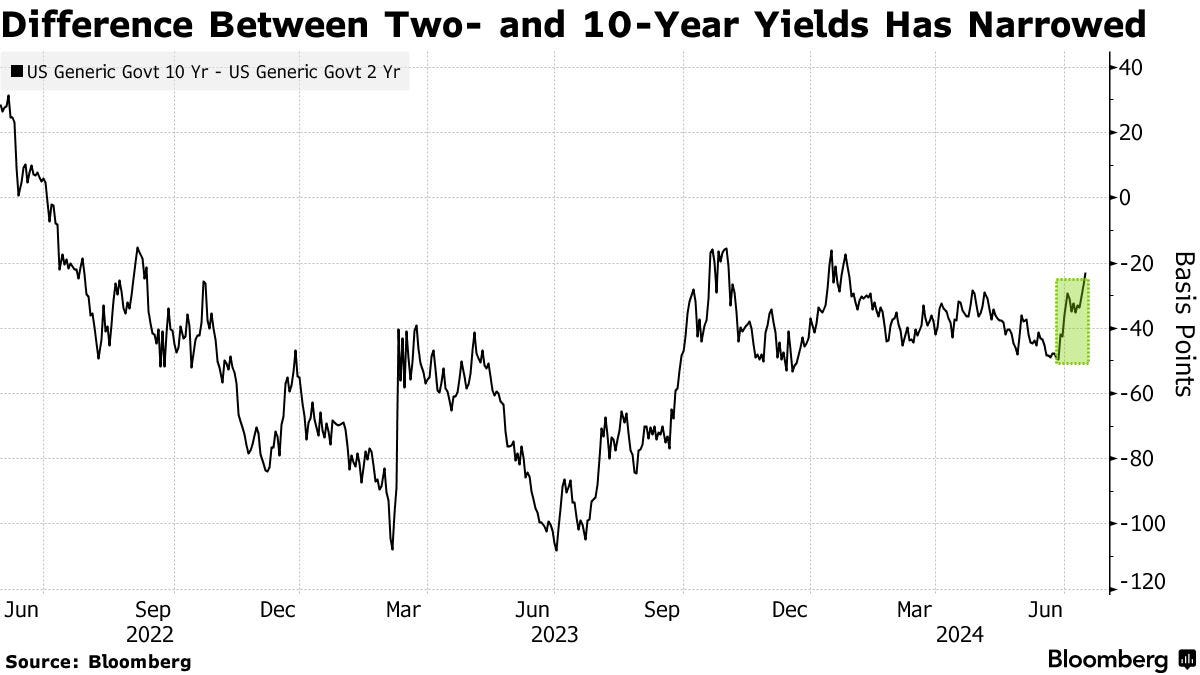

… Many focus on the steepening of the yield curve and the odds of former President Trump winning the election (Figure 2). Bond markets are pricing the possibility that a Trump presidency widens the deficit, and the Treasury may have to fund the massive budget hole by selling longer-maturity bonds. That drives up 10Y yields while the stock market rallies in anticipation of corporate tax cuts and deregulation, aka "the Trump trade."

Figure 2: Curve steepening and the odds of the election (%)

… AND so, here is a snapshot OF USTs as of 648a:

… and for some MORE of the news you might be able to use…

NEWSQUAWK: US Market Open: RTY continues to outperform, DXY flat & Crude at lows ahead of US Retail Sales … Bonds are higher following Fed Chair Powell's comments and with yields unwinding some of their Trump-induced steepening … USTs are firmer and holding near highs of 111-10+, as Powell's inflation language serves to weigh on short-term yields, alongside an ongoing pullback in crude; action which is also being seen at the long end of the curve which is currently underperforming and the curve as a whole is flattening.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ …

CitiFX: US yields: Close to a break (levels to watch and the ‘what next’)

US yields are testing important short term support levels. A break would open up significant moves lower in yields: ~28bps for 2y yields, ~18bps for 10y yields. We also highlight short term support and resistance levels to watch

US 2y yields Yields are testing support at 4.40% (March 2024 low), after breaking below the 4.55% support (March 27 low). IF we break below this level on a weekly basis, we will open up a 28bps move lower towards 4.12% (2024 low). On the flip side, resistance will first be seen at 4.55% (March 27 high).

Keep a close eye on any cross higher from 'oversold' territory in the weekly slow stochastics. This was indicative of a reversal earlier in the year.

…US 30y yields Yields are still hovering around the 55w MA (4.43%), having failed to close decisively lower on a weekly basis in recent weeks. IF we see a decisive close below 4.33% (March 28 low) on a weekly basis, it would open a move towards 4.19% (March 2024 low)

Weekly slow stochastics continues to tick lower, and is close to touching 'oversold' territory.

DB: Fixed Income Blog - A quick revisit of the Trump trade (10s UP 15bps…)

The attempted assassination of former President Trump is another in a string of developments over the past month that have shaken up the election picture. Here we offer some perspective on how US rates may respond over the coming days based on the reaction to earlier significant moves in prediction market probabilities.

Based on implied probabilities from PredictIt, Trump’s probability of winning the election has moved up by around 6ppt since Friday, from 60% to 66%. This increase is similar to the shifts in probabilities following the debate several weeks ago and following Trump’s strong showing in the Iowa caucus in January; both led to an increase of ~6ppt in Trump’s probability, as shown in Figure 1.

Figure 2 shows the rates market reaction to these earlier comparable shifts in probability and gives a benchmark for what we might see over the coming days (though other contemporaneous developments have influenced these earlier moves; e.g.,the PCE inflation data and French election in late June). The starkest move has been a bear-steepening in the curve and rise in term premia. Additionally, the breakeven curve has shifted up and flattened, and swap spreads have narrowed though only very slightly (speculation around a slowing in QT in January and valuation considerations in late June may have muted those moves).

The earlier reactions point to a potential increase of ~15bp in 10y UST yield in coming days…

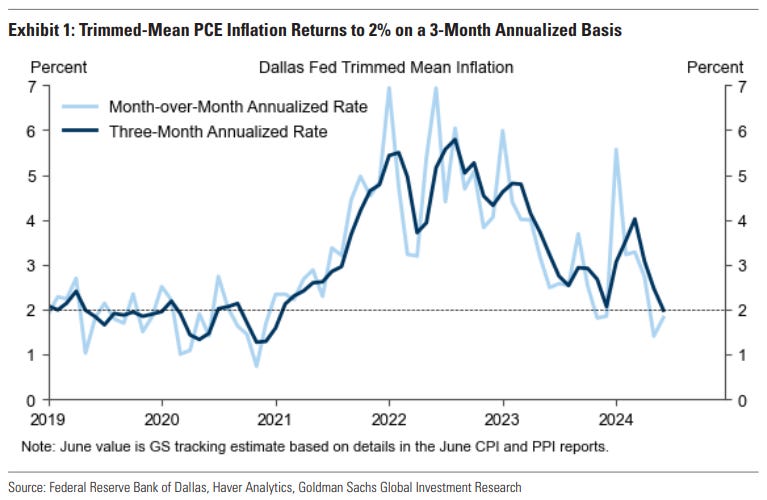

1. The US core CPI increase of just 0.06% in June confirms that the Q1 pickup was an outlier, in part because of residual seasonality. Based on CPI and PPI but pending import prices, we estimate monthly inflation rates of 0.19% for core PCE and 0.15% for core market-based PCE. The Dallas Fed trimmed-mean PCE probably also rose 0.15% on the month and has now returned to the lows of late last year on a 3-month annualized basis. We expect further benign prints in July and August, partly because of weakness in the relatively persistent shelter components (which is likely to be particularly pronounced in the July report because shelter inflation is calculated as a 6-month average growth rate and January was an outlier to the high side).

JPM US FI Weekly (f’cast REVISION … again written prior TO past weekend turn of events but still … )

…Governments We revise our interest rate forecast lower, as we now see the first ease in September. While the proximity to the first ease supports lower yields, we stay neutral duration given the dovish Fed path currently priced and the punitive carry of holdings longs. Hold 5s/30s steepeners as pre-easing cyclicals support a continuation of this move, but the curve appears steep locally relative to the level of front-end yields, and we recommend adding a beta-weighted 2-year short to hedge this risk. We discuss RV opportunities, 20-year valuations, and June STRIPS data. Stay neutral on inflation after taking profits on 1Yx1Y inflation swap longs earlier this week. Use further cheapening to reinitiate bullish exposure.

…Treasuries Is this it?

We now forecast the first Fed ease in September (vs. November previously) with a quarterly pace of cuts thereafter. We lower our YE24 2- and 10-year forecasts to 4.30% and 4.15% to reflect an earlier onset to easing

With the first ease in view, this has typically supported a further decline in Treasury yields. However, the market is pricing in a more aggressive pace of cuts than we have forecast, and a more decisive slowing in payroll growth is needed to justify this pricing: remain neutral on duration

Pre-easing cyclicals also favor further long-end steepening, and the carry profile is better than outright longs: maintain 5s/30s steepeners. However, the curve locally appears too steep after controlling for front-end yield levels and may turn more rangebound in the coming weeks: we recommend adding beta-weighted shorts in 2-year Treasuries…

… The 20-year sector has cheapened on the fly over the last 6- weeks and now appears slightly cheap. Risks appear well balanced given valuations are only slightly cheap and implied volatility is likely to stay stable in the months ahead …

… Turning back to the Fed, given that we have brought forward our first expected ease to September, and now expect 2 cuts this year, we make forecast adjustments to reflect this new reality (Figure 16We lowruintes rafoctel anrioset Fdaing). Notably, we lowered our YE24 and 2Q25 10-year forecast from 4.40% and 4.0%, respectively to 4.15% and 3.90%, respectively. We also lowered our YE24 2-year forecast from 4.60% to 4.30% to reflect this earlier first cut. Overall, as discussed above, we think Treasury yields will remain more rangebound over the near term, as it will take more decisive labor market weakening to justify more than 50bp of easing over 2H24 …

… At the end of May, we cautioned the 20-year sector had benefitted from a carry-seeking environment, and that further outperformance was unlikely, absent a further step-down in implied volatility (see Treasuries, U.S. Fixed Income Markets Weekly, 5/31/24). Accordingly, amid the unwind of carry trades over the last month, it’s not surprising the 20-year sector has cheapened along the curve: as Figure 20The 20-yarsecto hasepnd 5bothepar Tsuyflince ourlast pdehnof May. shows, the 10s/20s/30s par butterfly is currently in the 45th percentile of its 3-year range, versus the 6th percentile on May 31…

UBS: Does the vice president matter? (more importantly, does ReSale TALES?)

Former US President Trump’s selection of Senator Vance as his running mate is not immediately market moving but it is market relevant. In a television interview, Vance identified China as the US’s greatest threat. Markets have been inclined to think that Trump would not really tax US consumers who buy goods partially made overseas as aggressively as they threaten—but the rhetoric suggests tariff threats may be serious.

June US retail sales data are released. Price changes matter, as this is a value measure (durable goods are in the most aggressively deflationary episode in over two decades). Disinflation, deflation, a cyber-attack on auto dealers, strains for lower-income households, and the shift to spending on services suggest a lower number. US consumers’ relentless hedonism suggests something not too low.

… And from Global Wall Street inbox TO the WWW,

Bloomberg: Trump Trade Jumpstarts Bond Bet That Needs Fed for Next Boost

Rising deficits and Trump tax cuts weigh on long-end yields

… “The Fed moving rates lower is a big catalyst for the curve to steepen,” said John Madziyire, senior portfolio manager at Vanguard. “On the political side, any chance of a sweep in November means fiscal deficits come front and center.”

…Speaking Monday, Fed Chair Jerome Powell noted progress on inflation while declining to spell out the central bank’s future policy shifts, and reiterated that an “unexpected” weakening in the labor market would trigger rate cuts.

… The private sector as a whole is in much better share than it has been over the last 20 years on average but the public sector is in far worse share with an increasing share of that debt burden, which up to 90%, has shifted specifically to the federal government.

Within the private sector, there are some pockets of increased debt burden. The corporate and noncorporate sector have a high level of multi-family apartment mortgage debt. There was huge overbuilding in multi-family apartments over the last 10-15 years and it’s clear that some of this multi-family mortgage debt is bad debt that will cause losses. There is always bad debt when leverage increases rapidly.

The household sector has a lower debt burden compared to the last 20 years but it’s all from a reduction in mortgage debt. Consumer debt burdens remain just as high as ever in the last 20 years, with student loans and auto loans being the biggest culprits.

Higher government debt, will continue to reduce the standard of living for the average American and within the private sector, we should be most focused on the buildup of debt within the multi-family sector, mostly owned by regional banks and private equity funds.

The Babylon Bee:

Secret Service Vows To Find Out What Went Wrong At The Trump Rally As Soon As They Figure Out Who Left Cocaine In The White House

The Left Wing.........your friends ?????

https://youtu.be/eMp3xxg5Zrg?si=SLDmIH72upxp7A-_