while WE slept: bonds are flat; over extended longs (Barclays); when get to (four)forks in the road, take them (and by THEM, DB means EXIT from short 10s)

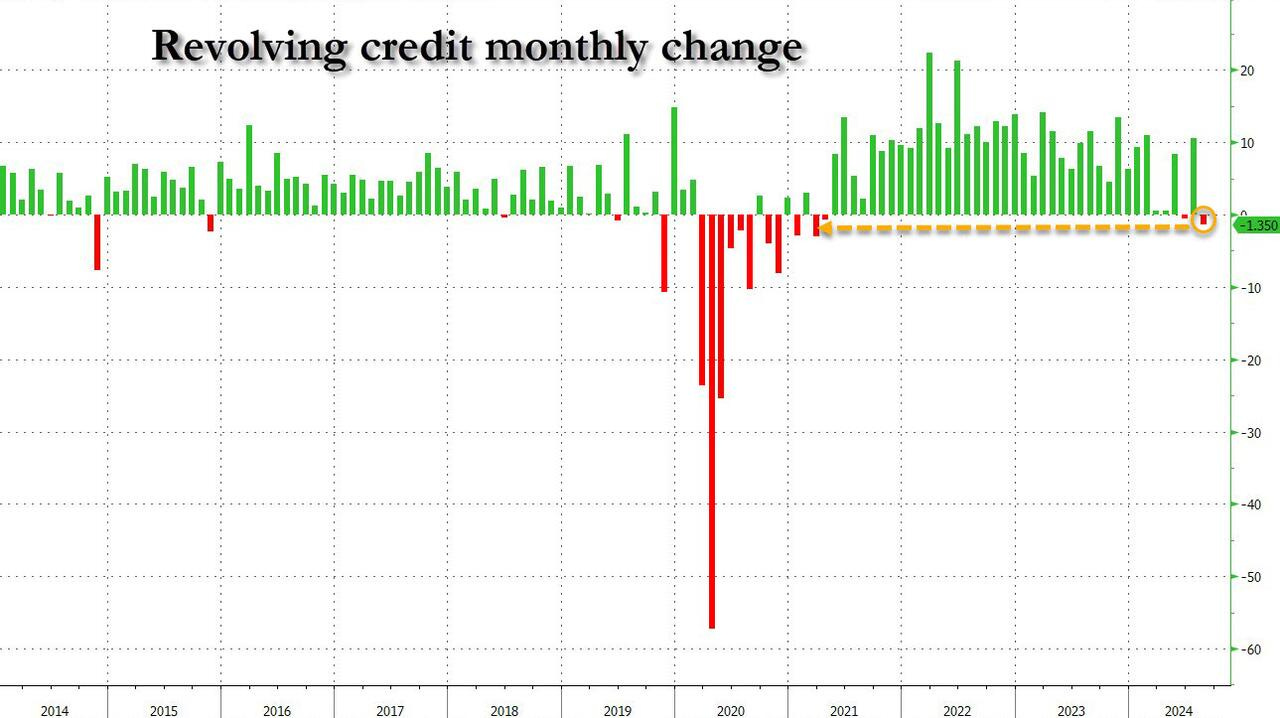

ZH: Consumers Crack: Credit Card Debt Suddenly Plunges Most Since Covid As APRs Hit Record High

… ... the punchline is that the much more consumer-outlook sensitive revolving credit reversed all of its July surge and then some, as August saw the biggest revolving credit drop since the covid crash!

… which, at days end, helped add up and resulted in following mkts wrap …

ZH: Crypto & Crude Jump; Bonds & Stocks Dump Amid Weather, War, & App Store Worries

… and little else to add here / now and so, here is a snapshot OF USTs as of 651a:

… and for some MORE of the news you might be able to use…

NEWSQUAWK: US equity futures mixed, European bourses subdued as sentiment weakens post-NDRC announcement … Bonds are flat, having initially opened with a positive bias, UK and German auctions provided no impetus … Dec'24 USTs are essentially flat, and taking a breather after four consecutive sessions of losses which were triggered by remarks from Powell guiding markets towards a 25bps rate cut and of course last Friday's hot US NFP report. The US 10 yr yield is currently around the 4% mark but down from Monday's peak at 4.03%.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ …

US elections as seen by those afar …

ABNAmro: US Elections – Spiraling debt is base case | Insights newsletter

The US debt-to-GDP ratio is on an explosive trajectory, fueled by healthcare and interest expenditures. Neither candidate has proposed policies sufficient to stabilize the ratio. With the exception of debt ceiling negotiations, the impact of large deficits will not be felt during this presidential term.

… POSITIONS matter …

BARCAP: Long & Short of It September on the Sidelines

Long-only equity exposure still low and hedge funds no longer dip buyers ahead of macro catalysts; systematic funds are slowly re-accumulating equities; options suggest wait-and-see heading into US elections; retail preferred cash, credit & EM equities; Big Tech a smaller overweight but still preferred over other sectors.

… Global macro and multi-strategy hedge funds take a breather after acting as dip buyers in August risk-off …

… Long positioning in bonds by asset managers remains over-extended …

… mispricings and speculators close to a tipping point? some say maybe so …

BNP: Quant trades of the week: An ‘Expansion’ regime with risks: Long USD, long equity

… Rates sell-off pushes CTAs closer to tipping point CTAs closer to tipping point: Last week’s ISM and employment data continued to showed resilient activity in the US, above our expectations. MarFA™ Macro valuation residuals continued to grow with rising activity strength and positive data surprises. US 5y and 10y now look 18bp (2.8 z-scores) and 13bp (2.2 z-scores) cheap.

Last week we highlighted how from the perspective of CTAs, market asymmetry is biased to receive rates and that in an “unchanged” spot scenario (over 21 days) we would expect to see a continued increase in long positions. We also highlight that a sell-off of around 27bp would result in almost a full unwind of their long positioning.

Following a near-20bp sell-off, our CTA tracker now shows a significant reduction of current “long” trend signal strength. This weakening of the trend signal means that in an “unchanged” spot scenario over the next 21 days, CTAs should be reducing their long position (not building). However, if we get another 20-30bp sell-off from current levels, CTAs would likely turn net short.

At this point, we do not add any short/payer positions, but we do close our long Switzerland 10y position for a small profit.

… and just when you thought it was safe to read and click ‘round, another late to the party note on NFP …

The shock of Friday's payrolls will reverberate around markets for some time. In today's CoTD we show 2 charts that highlight how unusual such a number is in the month that the Fed starts easing.

The first chart shows the path of payrolls in each Fed easing cycle since 1957. Month zero equals the first ease in the cycle and then we show the median path 12 months before and after. As can be seen, the month of the first cut normally sees a big slowdown in payrolls. But in 2024 we've seen the exact opposite.

The second chart shows what payrolls was in the month of that first ease in the cycle. The only higher numbers outside of last month was in the October 1987 cycle which was only because of the stock market crash, and then in 1984 when rates were cut from highly restrictive territory mid-cycle as we retreated from very high Volcker-inspired real rates. Interestingly, the next highest was in September 1998 after the Russian/LTCM crisis.

So both charts show how unusual it is to get such a bumper payroll report as the Fed starts easing rates.It feels to me that either the data is a big outlier (payrolls are very volatile and prone to revisions) or the Fed won't cut as much as the market still expects.

Four fork roads lie ahead for bond markets: (1) US election outcome, (2) European policy response, (3) China stimulus effectiveness, and (4) oil price outlook.

Given the wide range of plausible outcomes and current market pricing, we are reducing risk in our macro portfolio.

We are exiting the short UST10y and the cross-market short Dec-26 Sofr vs. Euribor, which are both currently trading close to our indicative targets.

For now, we are maintaining the EUR2s30s steepener and the short JGBs (2028 maturity), which remain attractive from a valuation perspective and have (presumably) a lower beta to the four key uncertainties outlined above.

US market rates have a strut about them. And why not. Jobs galore is seems (latest payrolls report). We'd called for a backup in rates. What's next? We're at near completion of the first leg of our post-rate-hike process. That builds room for a reversion back down. But don't get too carried away, as even at current levels, the 10yr rate is low vs equilibrium

… and finally, something we can agree upon … facts are that Williams IS an economist and so, his FRBNY views are ones we should note …

New York Federal Reserve President Williams—a genuine economist, who should thus be listened to —signaled that the Fed is happy with the state of the US economy and that two 25bp rate cuts this year would be appropriate. This clearer guidance for the future is a big improvement on Fed Chair Powell’s inept dependence on dodgy data.

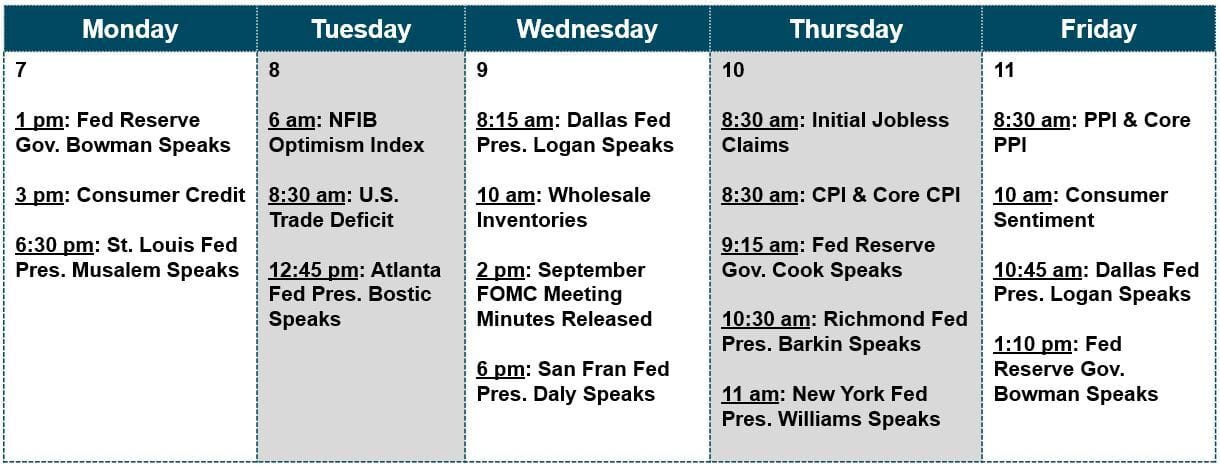

The US NFIB small business sentiment poll is due. This survey has been optimistic during Republican administrations and pessimistic during Democrat administrations, and the correlation is more likely political than economic. Vice-President Harris’s consistent modest lead in polls suggests an obstacle to optimism in today’s data. August trade data is due—of some relevance with talk of trade taxes flying around everywhere…

Good morning. US equity futures are trading a bit lower this morning as Treasury yields continue to tick higher following last Friday's stronger-than-expected jobs report.

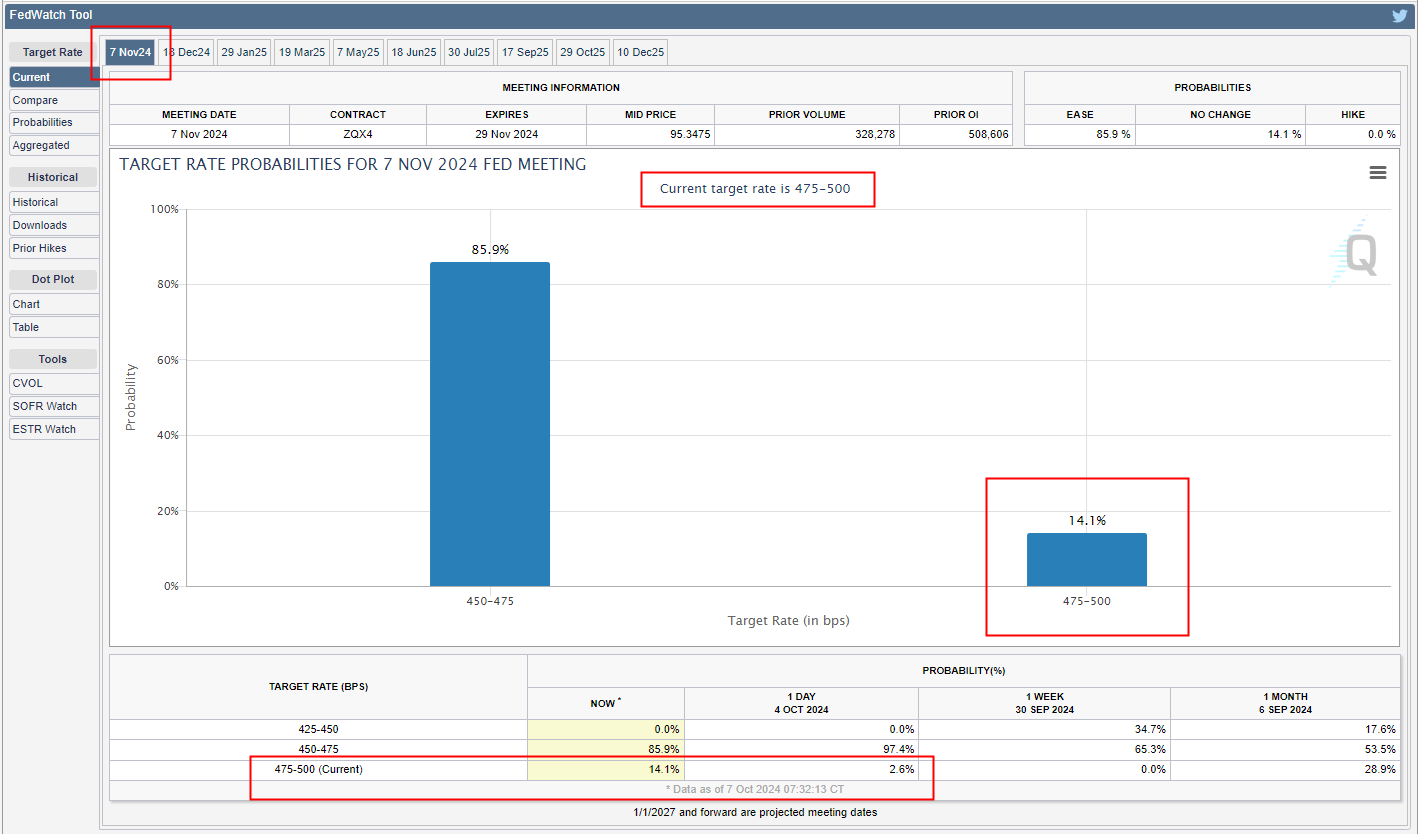

A couple of weeks ago after the Fed cut rates by 50 basis points at its September meeting, market odds were roughly 50/50 that they would cut by another 50 basis points at the November FOMC meeting on November 7th (two days after the election).

Fast forward to this morning, and market odds that the Fed cuts by another 50 bps are effectively zero, while the odds that the Fed doesn't cut at all are suddenly ticking higher. As shown below, Fed Funds Futures pricing highlighted by the CME's FedWatch tool show a 14.1% chance of NO CUT at the November Fed meeting.

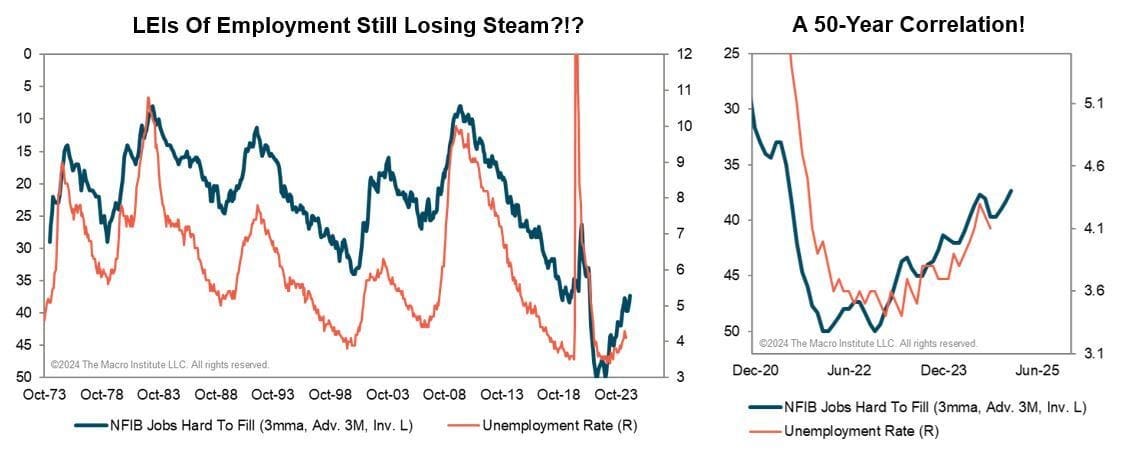

The September payrolls report provided much needed relief to investors increasingly concerned about labor markets. The numbers certainly looked good on the surface. That said, large revisions recently leave some doubt as to whether the numbers will hold up as the BLS continues its revision process. More importantly, perhaps, is that the employment picture looked weaker in survey data from the ISM and the NFIB. The chart here shows the "Jobs Hard To Fill" series from the NFIB, which hit its weakest level in years in September. This one is also a great leading indicator of wage/core inflation and argues that the downward trend in both series continues for the foreseeable future.

I'm among many who can't believe those Jets fired Salah. Too bad Roger's buddy Hackett isn't the intern coach 🤣🤣🤣