What is to follow is NOT, repeat NOT that ‘4D chess’ type analysis that Global Wall seems to be leaning. Of only in catch phrase form … I’ll lead with Quick Look at 10s and frankly, I’m underwhelmed. Don’t get me wrong, happy to see bonds still NOT DEAD yet but I’d have thought drop in yields coulda woulda been more substantial…

Back TO 10s when last I left BEFORE the fit hit the shan, watchin’ 4.00% …

10s DAILY (1y): still watchin’ 4.00% and askin questions …

… with momentum extremely overBOUGHT, one question I might be inclined to ask is IF it’s different this time? another question might be are stocks going to lose their influence? …

Just a couple questions of many MORE on my mind having been outta pocket past couple / few days …

Quick detour … how was NFP? All weather, I’m told, yes? Nevermind. I’ll quit while I’m behind. NOTE: “Adult Swim!” signs hanging everywhere as you enter the market place … here is a snapshot OF USTs as of 705a:

… for somewhat MORE of the news you might be able to use … a few more curated links for your dining and dancing pleasure …

NEWSQUAWKUS Market Open: Bonds bid, DXY firmer and Equities deep in the red after Commerce Secretary Lutnick said there is no postponing tariffs … USTs are firmer, at best have been above the 114-00 handle to a 114-10 peak, a high that printed just after the re-opening of trade when the selling in Asia was at its most pronounced and saw the Nikkei 225 hit circuit breakers. The main development this morning came from China, with reports via Bloomberg sources that they are considering frontloading stimulus. An update which prompted a bit of a pullback from highs for fixed, though only modest at the time. Thereafter, as the risk tone came off worst levels, USTs pulled back to a 113-12+ low. Though, still firmer on the session with the 10yr yield still just below 4%; Friday’s base was 3.86%.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s some of what Global Wall St is sayin’ … A quick recap without ANY commentary and in alphabetical order (time / date stamped to best of my abilities) … here’s what desks will be talkin’ ‘bout …

4 April 2025 Barclays: US Outlook and FOMC Update: Lower growth, higher inflation to follow 'Liberation Day'

Following the Liberation Day tariff announcements, we lowered our GDP growth and raised our inflation projections for 2025. We now flesh out our forecast through end-2026. The higher inflation projection leads us to remove a policy rate cut in 2026. We now expect two 25bp cuts in 2025 and 2026.

…As a brief summary of our recent trading activity:

Booked profits on part of our short position in 10-year breakevens (entered March 31st at 240 bp) at our initial target of 230 bp on Thursday, April 3rd. On Friday, we booked profits on the remaining portion of the clip at 225 bp.

Booked profits on part of our core-steepener position in 2s/10s (entered February 5th at 23.3 bp) at our initial target of 38.0 bp on Friday, April 4th. We're now targeting a retest of the early-January peak of 42.9 bp.

Stopped out for a loss on our short position in July 2025 Federal Funds Futures FFN5 (entered March 14th at 95.925) on Thursday, April 3rd at 95.950.

Stopped out for a loss on our short position in January 2026 Federal Funds Futures FFF6 (entered March 31st at 96.485) on Thursday, April 3rd at 96.560.

This week, we'll look to enter a 2s/10s flattener position in the wake of the 10- and 30-year auctions…

Misguided investor beliefs: Investors held on to hopes for less aggressive actions from the Trump administration, leading to an overweight in risk assets and an underestimation of recession probabilities.

Market correction and de-risking: The realization of recession risks led to a significant sell-off of risky assets.

Recession playbook: Historical analysis suggests that in the context of recessions, the current sell-off has been rapid, but further downside is possible.

Base case in a rising recession: another 10% correction for spot with volatility remaining bid.

Defensives >> Cyclicals: Defensive sectors and indices such as SMI, UKX or Food & Staples, Utilities, and Healthcare should outperform, while cyclical ones like DAX, CAC or Autos, Banks and Industrials likely underperform during recession fears.

European banks in recessions: SX7E has potential to extend further if market conditions worsen, led by earnings volatility and outflows.

We expect the tariffs announced on Liberation Day to be a stagflationary shock for the US economy. We think the Fed remains on hold for now, more concerned about the risk of inflation than it has so far let on.

US and EU rates markets should continue the momentum toward more recession pricing. We suggest long 10y USTs and 1y CPI swaps and add 2s10s ESTR steepeners. We extend our targets on long EURUSD and EURTHB.

Oil prices face a double whammy of rising growth concerns and increased OPEC+ supply.

04 Apr 2025 BNP US rates: Trade updates after Liberation Day

KEY MESSAGES With the significant market moves after Liberation Day, we make modest changes to our suggested trades.

Replace long 5y breakevens with 1y CPI swaps: We continue to think inflation risks are still tilted to the upside, but instead of 5y TIPS breakevens, we express that trade in the front-end – by being long 1y CPI swaps. Target: 400bp. Stop: 300bp.

Switch 10y TIPS to 10y nominals: We have maintained duration longs via long 10y TIPS since the inauguration and suggest moving to 10y nominals as risk-off conditions get extreme. We continue to think duration trades are easier than curve trades. Target: 3.70%. Stop: 4.15%.

We close our SOFR/FF short and take profits with markets already pricing the possibility of a Treasury market liquidity event and an earlier debt ceiling resolution.

Finally, we add a 6m1y payer ladder – as a cheap way to play for some degree of mean reversion in Fed pricing. Buy 6m1y A/A+25/A+50 (1x-1x-1) payer ladder. Entry: 2bp. Target: 25bp. Stop: -6bp.

…Fig. 1: In the past 50 years, a two-day SPX sell-off >10% has only happened in Covid 2020; GFC 2008; and Black Monday 1987

04 Apr 2025 BNP: US: The hardest part of playing chicken is knowing when to flinch

KEY MESSAGES

Fed Chair Powell’s remarks suggested a wait-and-see approach where the FOMC’s next move could be a rate cut, a hike or a continued and prolonged hold, depending on how trade policy unfolds and how it impacts hard economic data.

We see trade policy as a high-stakes negotiation game and believe the Trump administration is more sensitive to tightening financial conditions than it lets on.

Payroll growth at 228k in March suggests strong momentum but is ultimately a backward-looking measurement.

Technical indicators suggests that the sell-off in US equities (S&P 500 and Nasdaq Composite) could continue in the near term, with strong supports only likely at their respective 200w MAs. That said, however, we warn that weekly slow stochastics for both is now in deeply oversold territory. We have only been this deeply oversold on four other occasions in the past decade. Each time, however, we have seen a significant bounce (>10%) for both SPX and CCMP.

10y UST scenarios with US tariffs In our pre-election forecast update, we noted our baseline rates outlook was predicated on a resilient labor market, sticky inflation, and the Fed remaining on hold this year. However, we emphasized that policy uncertainty – especially with respect to trade and fiscal – would be key to the rates outlook going forward…

… The key question now for our outlook is whether higher projected tariff revenues will be used to justify a larger fiscal package via bigger tax cuts and/or smaller spending cuts. Notwithstanding Secretary Bessent’s continued focus on spending reductions, we do see this as a possible strategy by the White House, noting that this administration has been consistent on its messaging of delivering a growth boost. Maximalist tariffs could be an on-ramp for Congressional leaders to agree to a budget deal with large static revenue assumptions based on tariffs that don’t ultimately materialize. Given the significant uncertainties and our expectation for more clarity on the fiscal front in the coming weeks, for now we consider the implications of two alternative scenarios for US rates (summarized in the table below)…

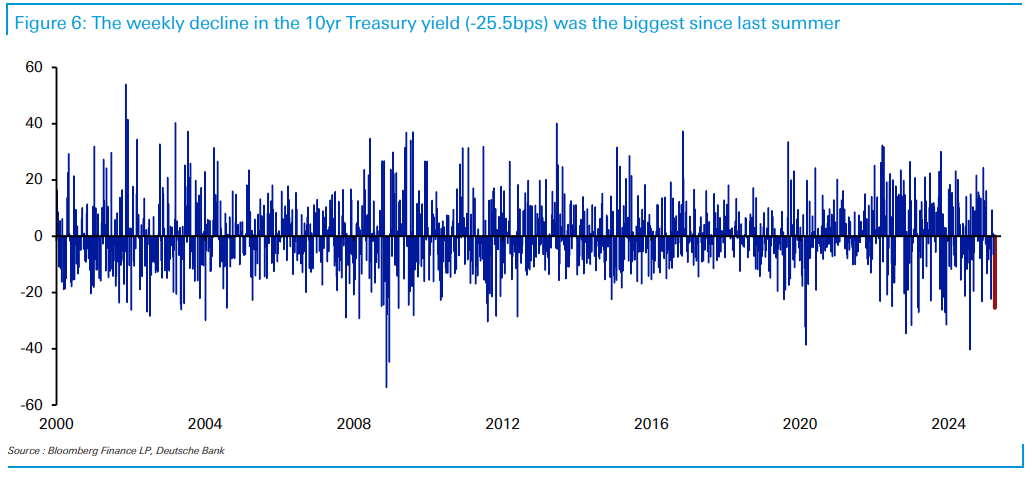

7 April 2025 DB Mapping Markets: 10 charts on how last week's moves compare with history

…1. The two-day change in the S&P 500 on Thursday and Friday (-10.5%) was the 5th worst since WWII.

…5. US HY spreads widened by +93bps in two days on Thursday and Friday. The only time we've seen bigger moves are the post-9/11 market reopening, the height of the GFC, the S&P US credit rating downgrade after the debt ceiling crisis in 2011, and Covid-19.

6. For the US 10yr Treasury, the moves weren't so dramatic, and the -25.5bps decline last week was "only" the biggest since last summer's turmoil.

1. Near-term negotiations 2. Fiscal policy announcements 3. Political signs of non-alignment in the Trump administration and Republican Party 4. Hedge fund margin calls 5. This week’s US inflation report (Thursday) and consumer sentiment figures (Friday) 6. Other hot money flows 7. Credit spreads v absolute level of bond yields 8. IPO suspensions

7 April 2025 DB: Our new gold forecast: 3,350 this year

What's going on with inflation breakevens? Tariffs are supposed to push up prices, but breakevens have fallen. Not great as it points to macro malaise. Equities down too points to lower earnings. Lower bond yields gel with that, and we likely get more. But as we likely hit 4% inflation again in the months ahead, longer rates will be pressured back up again

April 4, 2025 MS: Stay Long Duration, Add Curve Steepeners | US Rates Strategy

After significant intermediate sector outperformance, we suggest investors restructure portfolios to position for a significantly steeper Treasury yield curve ahead. We suggest investors enter 3s30s Treasury curve steepeners overlaid with an outright long in 7y Treasuries.

Key takeaways

Further escalation in the trade conflict would send yields lower, but we don't think investors should stay long duration only to hedge further escalation.

Without an accommodating Fed, we expect continued downgrading of growth expectations by investors as the prospect for long-lasting tariffs sinks in.

If investor growth expectations fall further, so too should the prices of riskier asset classes — raising risks for downside surprises in economic growth data.

Continue to favor long duration around the 7y key rate, but exit long 5s on 2s5s30s. Enter UST 3s30s steepeners and SOFR 1y1y vs. 5y5y steepeners.

We think March US CPI presents asymmetric risks for Treasury yields. A higher print means more risk off and lower yields. A lower print means lower yields.

Last Friday showed some signs of capitulation as the Nasdaq reached bear market territory and safety stocks and gold sold off. With recession risks rising and no sign of a Fed or Trump put, investors are left to figure out when to step in. Today, we offer our thoughts.

Key Takeaways

Many stocks have traded poorly all year even if the major indices held up until mid February. In most cases, the weakness was directly related to negative earnings revisions breadth, which had little to do with tariffs. Now, tariffs are weighing mightily on sentiment and confidence, and will likely lead to more negative earnings revisions during 1Q reporting season while increasing the odds of a recession. The question is how much of this has been priced and which sectors/stocks look attractive or vulnerable. Today we consider index level risks and sector risks should a recession arrive or markets decide to trade one.

Cyclicals have underperformed defensives by more than 40% over the past year with almost half of that happening between April and September of last year. This suggests growth has been a concern for awhile and in line with our core views that much of the private economy has been struggling for years, why large cap quality has dominated performance and why we have been so consistently recommending those factors since 2021 with the exception of last fall when the Fed started cutting rates. With the dramatic outperformance of defensives YTD, Friday's sell off in these names suggests forced selling/liquidation and signs of exhaustion in the correction.

Last Thursday, we offered 5100-5200 as the next area of technical support for the S&P 500. With the market quickly trading there on Friday and overnight futures down another 3-5% so far, our thoughts turn to the next area of support, which lies closer to the 200-week moving average, or 4700. Valuations also offer better support at that price so investors should be prepared for another 7-8% potential downside from Friday's close if there is no line of sight to a less severe trade environment and the Fed remains firmly on hold.

Recent developments and price action further emphasize our preference on high quality/large cap/more defensive equities and indices. We offer screens in today's note for names that fit the bill. We are also adding American Tower (AMT) to our Fresh Money Buy List to replace our removal of ETN last week. This is a defensive name with offensive properties that can offer a good balance in this kind of environment, especially as rates come down in line with our rates team's forecast.

We see small cap underperformance relative to large caps continuing given their (1) higher exposure to macro uncertainty, (2) decelerating EPS estimates, and (3) tendency to underperform in a late cycle environment. That said, small cap opportunities are rich under the surface. We offer key screens for stock selection.

… The inconsistency here is that bond yields remain quite elevated if a recession is coming ( Exhibit 2 ). Our rates team believe this is due to the fact that bond traders have become jaded in recent years to lingering recession fears. We think it could also be due to the very real risk of record supply hitting while foreign buyers have decided to rotate out of US assets due to the tariffs and other policy announcements which have weighed on the US Dollar.

… Current market pricing for the Fed is a little more than 4 cuts this year so if our economists forecasts prove to be right--i.e. 1-1.5% growth and no Fed cuts the rest of the year, it's going to be a slog for equity markets with continued underperformance of low quality cyclicals. It's conceivable the Fed could continue to lag market pricing like they did last fall ( Exhibit 5 and Exhibit 6 ). In that case, the equity market may decide to press the Fed and price a recession for fear of no Trump put or Fed put is available. That is exactly the risk equity markets were contemplating on Friday, in our view.

April 7, 2025 MS: The Weekly Worldview: A Recipe for Recession?

We take stock of the factors that could increase recession risks in the US…

… So, are we on the cusp of a recession? Maybe. Forecasting is hard, as the saying goes, especially about the future. Our base case is that the US economy slows notably but avoids prolonged contraction. A “global recession” is hard to define, but the possibility of 3% growth in China, no growth in Europe, slowing across EM Asia, with the US contracting … that outcome needs serious thought.

With some major markets entering bear markets or correction territory, we track performance to date of global equities compared to large sell-offs through history. While markets like gold are behaving differently from prior cycles, the rally in bonds suggests 'old' diversifiers work once again.

… Strategy implications – these are the diversifiers you're looking for: The decline in 10Y UST yields has been steeper than in the median bear market at this point in a sell-off, laying to rest the concern over the past few years that a bond-equity strategy is dead. The 'classic' stock-bond correlations prevail, and bonds should continue being a good portfolio diversifier.

… And from the Global Wall Street inbox TO the intertubes, a few curated links …

April 6, 2025 Apollo: A Careful Look at the Incoming Hard Data

Our daily and weekly indicators for the US economy are available here, and the conclusion is that the hard data is still doing okay, but there are signs of weakness emerging.

Specifically:

– Las Vegas visitor volumes and total room nights occupied have started to decline, see the first two charts.

– Weekly bankruptcy filings are moving higher, see the third chart.

– Weekly data for movie theatre visits is weak, see the fourth chart.

– Daily data for job postings has been weaker in recent weeks, see the fifth chart.

– Daily TSA travel data is slightly weaker than at this time last year, see the sixth chart.

– Continuing claims are moving higher, see the seventh chart…

April 7, 2025 at 10:30 AM UTC | Bill Dudley Bloomberg: Stagflation Is Now America’s Best-Case Scenario Trump’s tariffs risk a brutal combination of recession and inflation.

… For bonds, the main issue will be the trajectory of short-term interest rates. Currently, markets are pricing in more than 100 basis points of easing this year. I think that’s likely (and justified) only in the event of an actual economic downturn. This isn’t 2019, when below-target inflation allowed the Fed to cut rates as “insurance” against recession. Nowadays, the world’s most powerful central bank has a lot less room for maneuver…

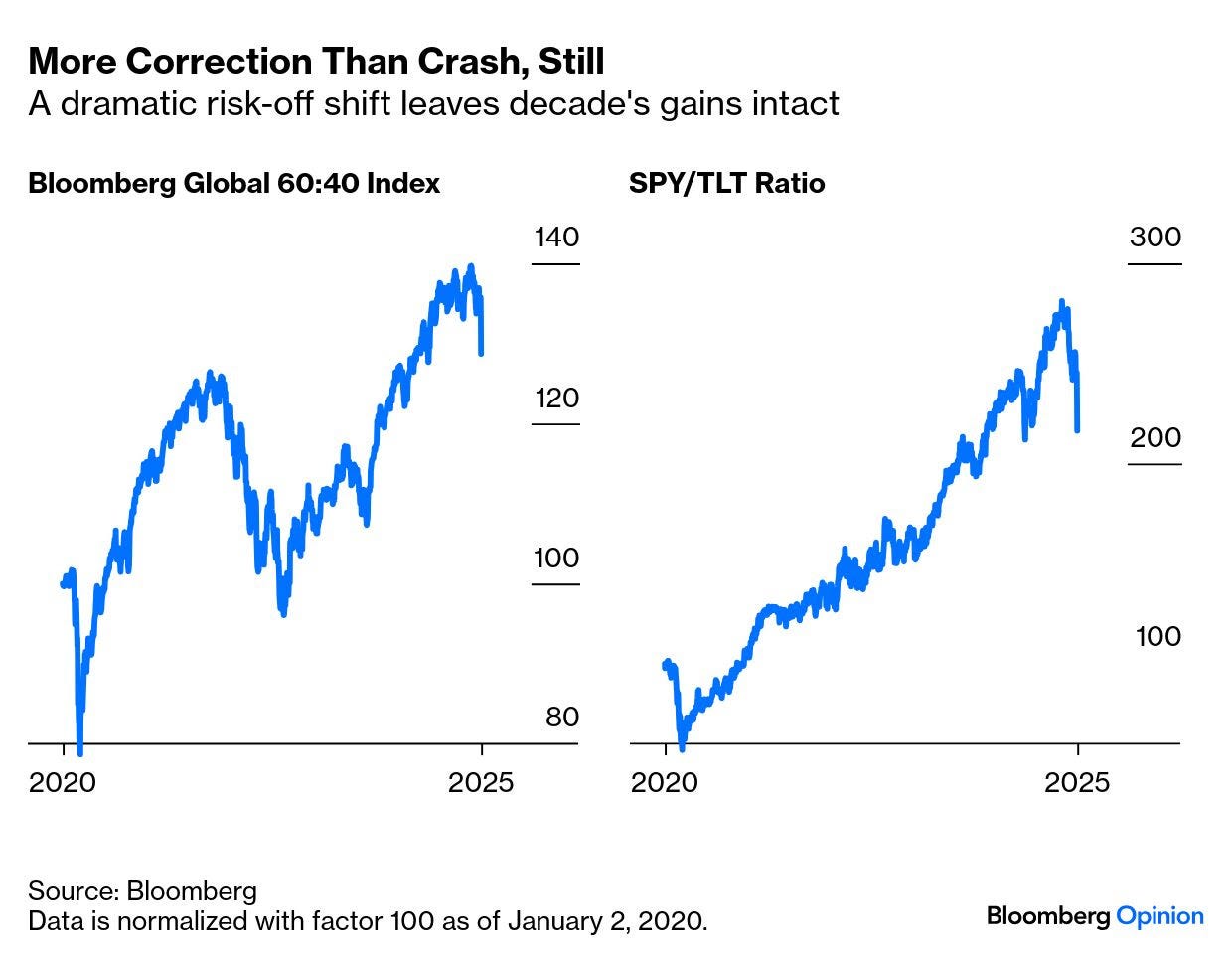

April 7, 2025 at 5:00 AM UTC Bloomberg: There's no sign that markets have had enough yet How bad was the Trump tariff quake? Let’s chart the ways.

… The market has swung away from a position that looked extreme. A 60/40 index (the classic 60% equities 40% bonds allocation) is the lowest in six months, but no worse than that. Similarly, stocks relative to bonds, as proxied by the popular SPY and TLT exchange-traded funds, have lost a lot of ground, but have held on to most of their post-pandemic gains. Retirement funds haven’t been wiped out. Keep this in proportion; while remembering that there’s also plenty of room below for this to go much further:

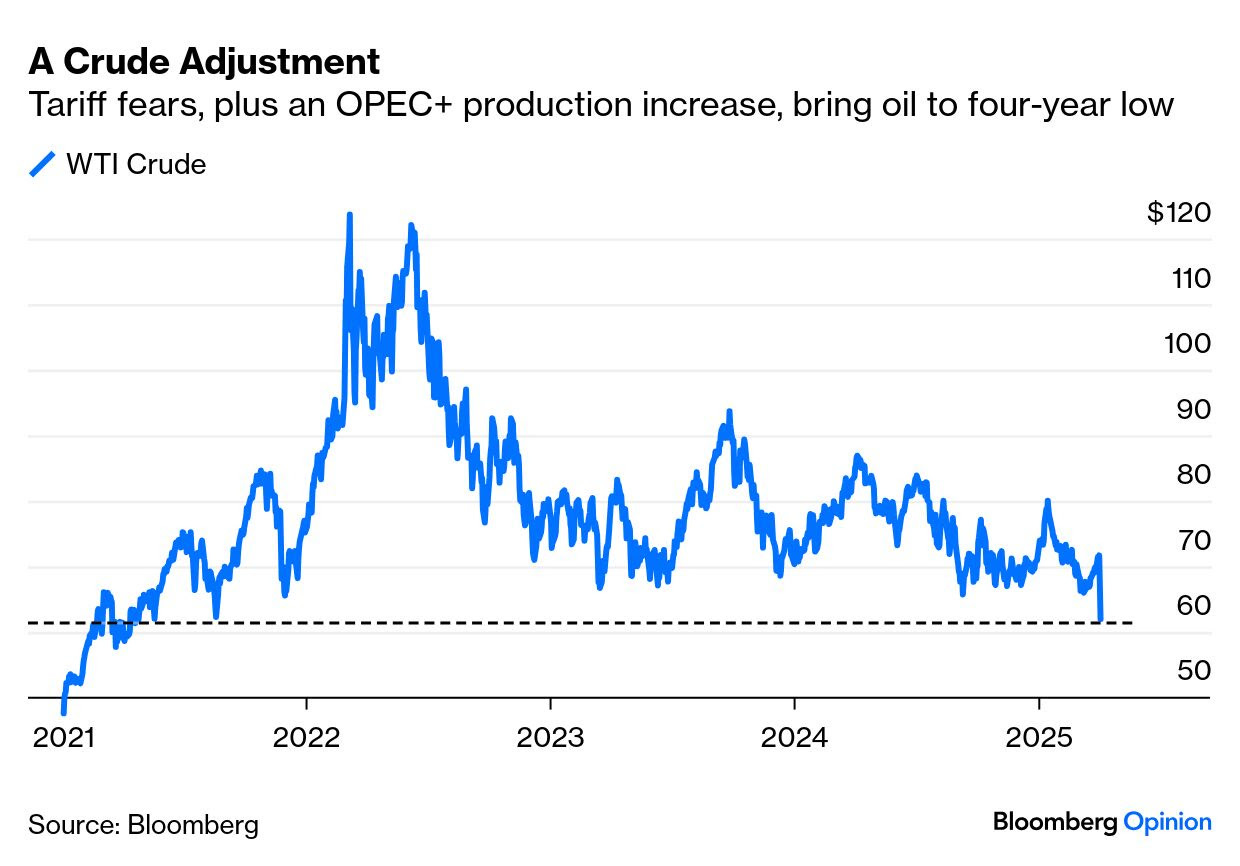

… Another critical development came in the oil market, fueled by a combination of growing recession fears and the decision by the OPEC+ cartel to increase supply. In early Asian trading, West Texas Intermediate crude dropped below $60 per barrel for the first time in four years. This is good news for an administration trying to show that it can contain inflation:

Sun, Apr 6, 4:47 PM BESPOKE: Two-Day Drops of 10%+

The S&P 500 ended last week down 10%+ in the two days following President Trump's "Liberation Day" tariff directives. There have only been three other periods since 1952 when the current five-day trading week began that we've had two-day drops of 10%+:

October 1987 November 2008 March 2020

We'll see where futures trade tonight and early tomorrow morning,

Apr 06, 2025 TKer by Sam Ro: If you know where things are heading, then you probably don't know what you're talking about

… THAT is all for now. Off to the day job…More of a view and some commentary on other views later but first …

Searching for a Bottom: "are we there yet, Dad ??"