Good morning … OK so maybe I am ‘overselling’ the idea of a SPIKE in EZ CPI but still, NOT what you — as the ECB — wanna see as yer tasked with lowering rates given de / dis inflation and so to clarify …

FT: Eurozone inflation edges up to 2.6% in July Latest figure comes amid expectations that region’s central bank will cut interest rates at its next policy vote

…. The figure is higher than the 2.5 per cent increase in the year to June. Economists polled by Reuters had anticipated price pressures to remain flat at 2.5 per cent…

… meanwhile, the BOJ HIKES overnight in a widely anticipated move. One which seems to have NOT rocked markets with HIKE OR with its plans to REDUCE bond purchases …

Nikkei Asia: BOJ raises interest rate to 0.25% in aggressive move

… The bank also announced a plan to taper its purchases of Japanese government bonds (JGBs). Monthly purchases will be reduced to 3 trillion yen by the first quarter of 2026 compared with the current pace of 6 trillion yen.

To make the tapering process as predictable as possible, the BOJ said purchase amounts will be reduced by about 400 billion yen every quarter…

… an eventFUL month-end upon us with BoJ in rear-view mirror and the Fed dead ahead.

While I’d like to think something funDUHmental was at work yesterday, i’m reminded that …

… Geopolitical tensions were responsible for 10-year yields drifting as low as 4.128% on Tuesday – breaching the 4.142% resistance level and marking the lowest for benchmark rates since March 12th. Treasuries started the session on strong footing, although the bid was challenged by the stronger headline figures for JOLTS Job Openings and Consumer Confidence. While the bid eventually reemerged before the headlines related to Israel targeting Hezbollah in a strike on Beirut, it was unquestionably the safe-haven flows that broke the yield range in 10s. The 2-year sector rallied as well and with the front-end reaching 4.344%, the 2s/10s curve resumed its steepening – albeit well within the orbit of -20 bp. The market is approaching Wednesday’s marquee events with a bond bullish tone that will be tested by an uneventful refunding statement and an on-hold Fed decision…

… which then leads TO this mornings h’line

AP: Hamas leader Ismail Haniyeh is killed in Iran by an alleged Israeli strike, threatening escalation

… And so, in addition TO techAmentals offered HERE yest and along with all the geopolitical concerns of this moment seemingly TRUMPING any / everything more funmy humble view of LONG bonds …

30yy: triangulating, becoming overBOUGHT, at / near / THRU resistance

prolly should be lookin’ at MONTHLY chart but for now, DAILY yields becoming but are not YET overBOUGHT and depending on how thick a line and how you draw it, well, yields triangulating …

… and from a friend specifically relating TO index extensions (via BBG, I believe)

UST Aggregate Index: +0.05y Duration extension for USTs, just below its past three July prints averaging +0.08y and its 12 month average +0.08y.

… make as much / little of that buying need as it may be, as you’d like but first, a look back at the day which just was …

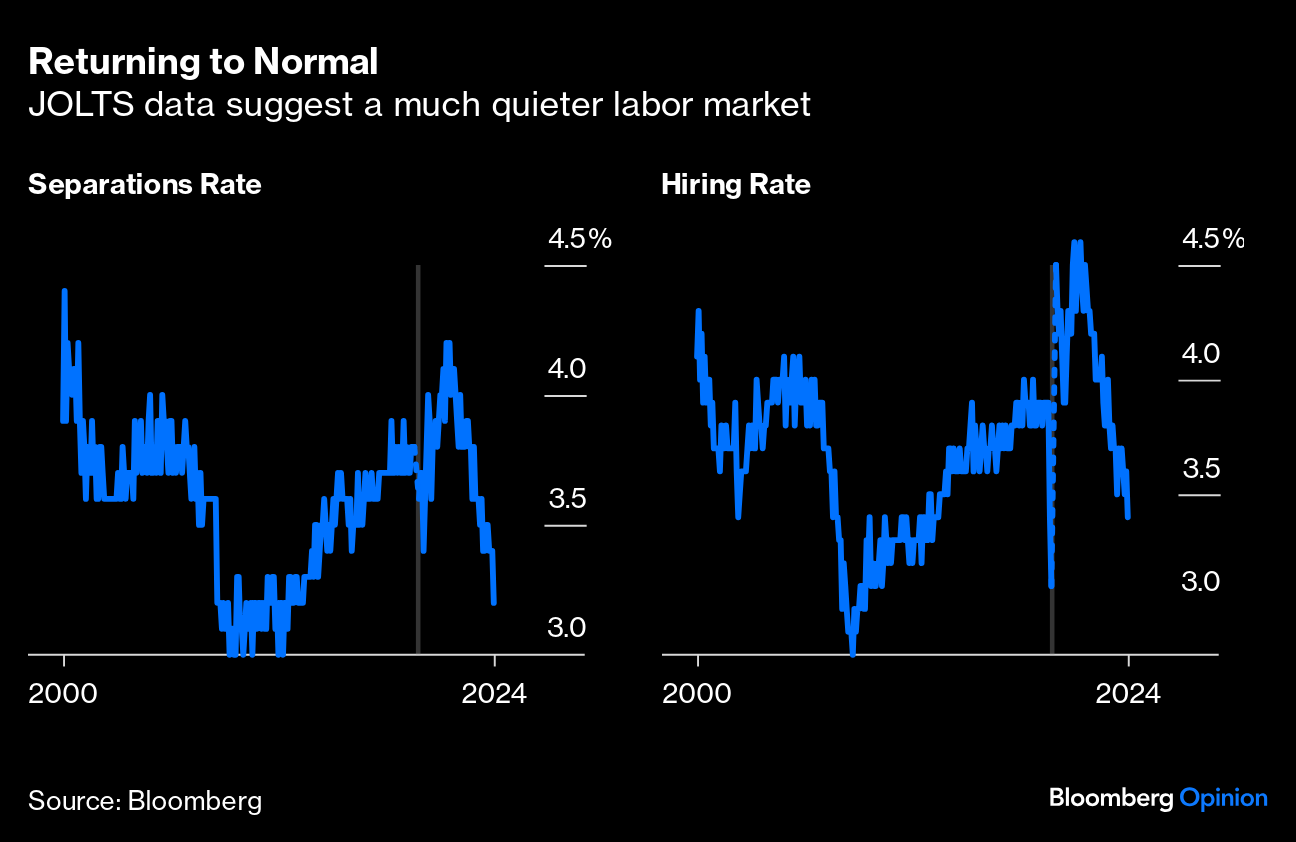

ZH: Catastrophic JOLTS: Private Sector Job Openings Plunge To 6 Year Low As Both Hiring And Quits Crater

… Putting it all together, while private sector job openings plunged to a level seen back in late 2018, government job openings are just shy of a record high!

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s SOME of what Global Wall St is sayin’ …

BARCAP: June JOLTS: Openings in line with FOMC's 'sweet spot'

The latest readings show that job openings have stabilized after reaching prepandemic levels relative to unemployment, in line with the controlled labor market cooling in the Fed's baseline. Hiring and separation rates point to less dynamism, suggesting that rebalancing has hit a lull following a post-pandemic burst.

Since our original publication in April, small business sentiment has remained downbeat, continuing to exhibit a stark divide between attitudes and overall business conditions in the small business sector and the overall economy.

In our prior report, we had used a novel methodology to show that this pessimism was justified by hard data that we can infer from other economic aggregates, which suggest that the nonfinancial noncorporate business (NFNCB) sector has been in a deep slump from Q1 2022 through Q3 2024. Given that this had coexisted with robust overall growth, we had little reason to believe this would undermine the expansion.

According to newly available data through Q1 2024, the NFNCB sector, this deep slump has been sustained, consistent with the evolution of small business sentiment indicators from the NFIB. As before, much of this weakness reflects the squeeze from wage cost pressures and diminishing productivity, with smaller businesses lacking the power to pass on higher unit labor costs to customers.

The struggles of this sector remain in sharp contrast with the much larger corporate sector, where hard data suggest that activity has continued to grow at a robust clip. Although wage pressures for corporate businesses have been just as acute as for small businesses, gains in productivity and market power have helped the former to sustain strong profitability.

As before, we have little cause to believe that the poor conditions in the small- and medium-sized business sector will undermine the overall expansion, which we expect to remain resilient in the coming quarters despite the elevated Fed funds rate.

In April, we had highlighted the deep slump in the small- and medium-sized business sector from Q1 2022 through Q3 2023, even amid a resilient, consumer-driven expansion. We update our estimates using newly published data through Q1 2024, showing that this remains the case.

DB: How do yields change around FOMC meetings? (you ask, they answer … cuz, you know, it IS II voting time … )

Ahead of tomorrow’s FOMC release and press conference, today’s COTD examines how yields have evolved around past Fed meetings since the 2022 hiking cycle. We find that SEP meetings see larger average movements in yields than non-SEP meetings. The chart groups market reactions into two events: the statement release (along with the SEP for quarter-end months) and the press conference. We measure changes in 10y yields between 1:55pm and 2:05pm for the statement and between 2:25pm and 4pm for the press conference.

…Another interesting finding is that over the course of this cycle, 10y yields tend to decline around Chair Powell’s press conferences. In contrast, yield changes around statement and SEP releases are more mixed. Since 2022, 15 out of the 19 FOMC meetings saw decreased yields in the window around press conferences. One potential explanation for this is that messaging from Chair Powell at these meetings has been more dovish compared to market expectations. However, since the market is already priced for multiple Fed cuts over the remainder of this year, which indicates dovish expectations heading into tomorrow’s meeting, the bar may be high for yields to repeat their pattern, while there are risks for higher yields if the tone of tomorrow’s meeting is more hawkish than expected.

… Today’s CoTD updates their analysis and shows the difference between the Real Clear Politics betting probabilities of a Trump victory in November, and a combined Biden/Harris equivalent which takes care of the likely handing over of the Democratic Party nomination.

Obviously correlation doesn’t equal causality but there is some evidence that history could be repeating itself with positive polling momentum from Harris eroding the peak probability of a Trump victory and making the contest look closer than it did two weeks ago…

UBS: Is Fed policy error nearly over? (assumption here is that … because nothing has ‘broken’ yet, hiking rates was / remains a MISTAKE? just jealous cuz they — UK — pay orders of magnitude MORE for a gallon LITRE of gas PETROL??)

The Federal Reserve is not expected to end its policy error today, but hopefully a rate cut will be signaled for September. Monetary policy has progressively tightened since the start of last year. For savers, slowing price inflation has increased real interest rates. For borrowers, slowing household income growth has increased real interest rates. The pressure of real policy has become ever more onerous as the economy has slowed.

Markets are still lack a medium-term policy framework. “Data dependency” sounds a sensible strategy, but in the midst of economic structural upheaval short-term data flow is unreliable. A broader examination of the role of policy in structural change would be useful, but is unlikely to be forthcoming…

On net, the JOLTS data point to a labor market that has normalized, but which does not look to have turned the corner into outright weakness. Job openings declined in June to 8.18 million from an upwardly revised 8.23 million in May. The layoff and discharge rate ticked down to 0.9% in a sign that demand for existing workers continues to hold up despite demand for new workers fading.

… And from Global Wall Street inbox TO the WWW,

Bloomberg: Trump crypto plan could end Bitcoin's anarchic vision (on JOLTS and specifically the LACK OF ‘response rate’ and yet, we all put increasing amt of weight on the report?)

… Another problem goes beyond exaggeration — people simply don’t reply at all. These are some of the key numbers from the latest JOLTS (Job Openings and Labor Turnover Survey) produced by the Bureau of Labor Statistics. The rate at which people are leaving jobs is falling, as is the rate at which they’re being hired. That suggests a labor market steadily returning to normal after Covid-19:

That’s believable, but it’s not clear that we can put much faith in it because response rates, already declining before the pandemic, have collapsed since. For the JOLTS, response rates are barely above 30%, and numbers answering inflation and employment surveys have also dropped severely:

The BLS explains what’s going wrong in a lengthy research report. Again, the forced move away from the tried-and-tested method of talking to people on their landline is an issue. As we brace for more key economic survey data, and decisions by data-dependent central banks, bear in mind that if garbage goes in, garbage will come out. To help, you could provide some truthful answers to the latest MLIV Pulse survey on what the effects of an easing cycle could be.

ING: Disappointing eurozone inflation makes September rate cut a close call

Preliminary figures for both headline and core inflation came in slightly higher than expected in the eurozone. While we believe that the downtrend remains intact, today's figures make a September rate cut from the ECB a very close call

at JamieSaettele

TLT coiled heading into FOMC and NFP. Coiled markets lead to breakouts and trends.

Euro-area inflation surprised positively and rose one notch to 2.6% in July. Uncertainty around the future trends is substantial and the ECB is likely to continue in a mode of no precommitments, but we still find another rate cut in September likely.

Here are four reasons inflation-related reasons for the Fed to be confident enough to begin cutting rates now:

The lower-than-expected inflation data since the June meeting returned to disinflation and confirmed that some of the inflation early in the year was likely due to calendar effects and one-off increases, not an underlying re-acceleration.

The monthly pace of rent of shelter inflation (tenant and owners’ equivalent) moved down to its pre-pandemic pace, which should be an important source of further disinflation in the outlook in the second half.

Wage growth—while still above the pre-pandemic pace—has moderated. A better balance between the supply of and demand for workers reduces cost pressures, reducing an upside riskto inflation.

Industry reports and the Fed’s Beige Book suggest that consumers are becoming more price-sensitive again, which limits businesses’ ability to raise prices.

at Todd_Sohn

You may be aware that the 1-year anniversary of the Fed Pause just occurred, but we find it notable that the conclusion of July marks 4-years since the Bloomberg Bond Agg Index last posted a new all-time high. It’s by far the longest streak since index inception (January 1976).

Barchart: Claudia Sahm, the creator of the Sahm Rule used to identify recessions in real-time, says the Fed's decision not to cut interest rates today doesn't make sense....

I guess Friday's NFP....should be Inline or Ok ???

Jeffrey Gundlach: Fed Day

https://youtu.be/IJY2et3gimQ?si=GdlbxG10CsXTsRqv

Barchart: Claudia Sahm, the creator of the Sahm Rule used to identify recessions in real-time, says the Fed's decision not to cut interest rates today doesn't make sense....

I guess Friday's NFP....should be Inline or Ok ???

Today's ADP...on the weak side...

I might tend to agree with Miss Sahm....