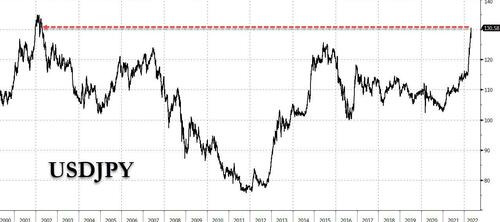

Bank of Japan unchanged last night BUT FIRMED UP its commitment to YCC by adding clarification ‘will offer to purchase 10-year JGBs at 0.25 percent every business day through fixed-rate purchase operations, unless it is highly likely that no bids will be submitted’. Meanwhile, in other news, the BoJ revises inflation up and growth down in its latest forecasts ... Results? ZeroHedge,

… HEREis what another shop says be behind the price action, you know,

WHILE YOU SLEPT Treasuries have been led modestly higher by the belly this morning ahead of what Citi expects to be a trade-induced, negative print in Q1 GDP in 90 minutes. Indeed, 'buy everything' has made a cameo with global stock markets higher too today. DXY is notably higher (+0.6%) after the BOJ defended their YCC program (see above) while front WTI futures are modestly lower (-0.45%). Asian stocks were led higher by Japan's TOPIX (+2.1%), EU and UK share markets are all in the green (SX5E +1.5%, FTSE 100 +0.9%) while ES futures are showing +1.5% here at 7am. Our overnight US rates flows saw rangebound conditions overnight- at least until ~6am NY time. During Asian hours we saw good demand for the front end from regional real$ names but that was about it. Overnight Treasury volume was only ~70% of average overall and we show in today's attachments how cash and swaps volume trends have indeed been receding this month.

… and for some MORE of the news you can use » IGMs Press Picks for today (28 April) to help weed thru the noise (some of which can be found over here at Finviz).

#got7s?

From the inbox, and ahead of GDP

WFC: Heads Up: Negative Print for Q1 GDP Growth? We are not formally changing our projection of a 0.6% annualized GDP growth rate in the rst quarter, but the risks to that estimate appear to be skewed to the downside when the BEA reports data tomorrow…

How one translate potential downside growth along with rates TECHNICALS (via 1stBOS), is completely up to you

Fixed Income Tactical Outlook … 10yr US Bond Yields are seeing a short-term correction lower, however we believe this correction will be fairly limited in nature and we look for the yield uptrend to resume shortly … 10yr US Bond Yields have corrected lower since the start of the week, however we look for the yield uptrend to resume shortly … We recently turned tactically bearish at resistance at 2.83%, with the next support seen at 3.21%, where we would turn tactically neutral. Resistance below 2.83% moves to 2.65%, below which we would also turn tactically neutral.

Will META or some other earnings SAVE the bull market in stocks OR will The Fed finish a job it seems to have set course to do,

Investing.com: Nasdaq On Track To Suffer Worst Monthly Drop Since 2008 As Powell Sparks Selloff!