Good morning … a couple / few things to kill time and fill space between now and this afternoons FOMC meeting, updated DOTS <GO> and press conference.

First, it has been detailed how today’s the first time since June of 2020 that BOTH CPI and the FOMC meeting were on the same day (AT MWellerFX HERE with a look at how the VIX pegged at ~13 … just ‘ahead of the fireworks’) and it is with that in mind, a look at 2yy on heels of an absolutely stellar 10yr auction (more just below) yest …

2yy DAILY: bearish momentum flattening out, SUPPORT up near 4.60% …

… and as the price history / context sinks in, I am reminded earlier this morning that on the last FOMC days the 2yr has rallied making this afternoons event risk even MORE funTERtaining, giving recency bias …

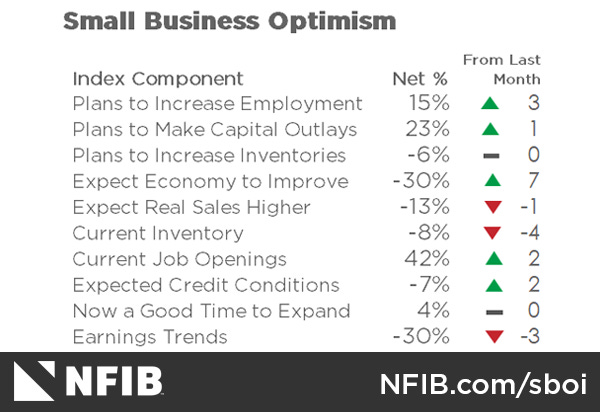

NEXTUP a quick look BACK as the day began with (and I missed) latest from Dunkelberg & Co’s NFIB …

NFIBs May 2024 Report: Small Business Uncertainty Index Reaches Highest Level Since 2020 (image below… inflation FIRST — trend is yer friend — while UNCERTAINTY, well, not so much)

… The small business sector is responsible for the production of over 40% of GDP and employment, a crucial portion of the economy,” said NFIB Chief Economist Bill Dunkelberg. “But for 29 consecutive months, small business owners have expressed historically low optimism and their views about future business conditions are at the worst levels seen in 50 years. Small business owners need relief as inflation has not eased much on Main Street.

… INFLATION The net percent of owners raising average selling prices was unchanged from April at a net 25 percent seasonally adjusted. Twentytwo percent of owners reported that inflation was their single most important problem in operating their business, unchanged from April. Unadjusted, 12 percent (down 1 point) reported lower average selling prices and 40 percent (down 1 point) reported higher average prices. Price hikes were most frequent in the retail (55 percent higher, 6 percent lower), finance (50 percent higher, 3 percent lower), construction (42 percent higher, 9 percent lower), manufacturing (42 percent higher, 12 percent lower), and services (37 percent higher, 6 percent lower) sectors. Seasonally adjusted, a net 28 percent plan price hikes in May (up 2 points).

… It is said that small business powers this country forward and at moment, we’re talking about high degree of uncertainty BUT at the same time, inflation as a concern is, at least, moderating … perhaps one will influence the other (and in a good way)…It’s not special to suggest only the passing of some more time will be needed for that to be the case … AND in the meanwhile AND as far as 10yr auction came and went …

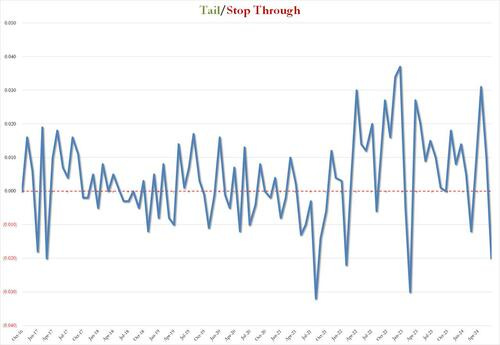

ZH: Stellar 10Y Auction Sees Surge In Foreign Demand, Near Record Stop Through

… The high yield stopped at 4.438%, down 5bps from last month's 4.4830%, and stopped through the When Issued by 2.0bps, which not only followed three consecutive tails, but was the biggest stop through since February 2023.

There's more: the bid to cover shot up to 2.67 from 2.486, the highest since Feb 2022, and was well above the six-auction average of 2.50.

The internals were also stellar, with Indirects taking down 74.5%, the most since February 2024 when foreigners took down 79.5%. And with Directs awarded 13.8%, down from 18.7% in May and the lowest since August 2021, Dealers ended up holding 11.6%, the lowest since August 2023…

… how’s THAT for somewhat more CERTAINTY — buying 10s ahead of CPI!!

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT Treasuries are modestly richer led by the belly on 110% volumes. Activity in Asia was generally muted, the desk seeing light real$ buying in long-end (and small FV block buyer). Treasuries pushed higher into the London open led by bunds, with OATs still underperforming (while Italy outperforms bunds by ~2.5bps in 10y). Position-squaring flows were evident with a block flattener going through in TU-UXY (~630k/01), which appeared to be an unwind. Some systematic selling in 10s was noted, while 10s30s sits a tad steeper with 30y supply tomorrow. Crude Oil continues to trade well (+1.3%) on API reporting some inventory slippage overnight, while Copper and Gold are flat. Mixed APAC equity performance was seen (NKY -0.7%, KOSPI +0.8%, SHCOMP +0.3%), and Eurostoxx futures are moderately higher (VG +0.4%, SX7E +1%). S&P futures are showing +7pts here at 7am.

… and for some MORE of the news you might be able to use…

NEWSQUAWK: US Market Open: Price action tentative ahead of today's key US CPI & FOMC announcement … USTs are flat and at highs, Bunds/Gilts both move higher with the latter also factoring in the in-line GDP metrics, with focus on the soft Construction figures … USTs are flat ahead of US CPI for one final read into the FOMC meeting where market pricing currently has a 99% chance of an unchanged rate. Currently holding near a fresh WTD high at 109-20, sparked by Tuesday's strong US auction.

Despite the government-led increase in utility costs and train fares, China’s CPI inflation remained subdued, coming in at 0.3% y/y in May, a touch below market expectations. On a m/m basis, headline CPI, core CPI and services CPI all fell into deflation. We lower our 2025 full-year CPI inflation forecast to 1.2%.

•May: 0.3% y/y for CPI, and -1.4% y/y for PPI •Bloomberg consensus forecast (Barclays): 0.4% (0.3%) y/y for CPI, and -1.5% (-1.5%) y/yfor PPI •April: 0.3% y/y for CPI, and -2.5% y/y for PPI

Economists are overstimulated by the US today. We have the excitement of US consumer price inflation. We have the excitement of a Federal Reserve policy decision. Fed Chair Powell’s press conference can be relied upon to dampen economists’ passions. The Fed is unlikely to change policy. The fabled dot plots of policy projections will add confusion (a black mark on a chart gives no sense of confidence or risk)…

…China’s price data is far less relevant to the global economy, and is mainly a domestic concern. Core non-food consumer goods prices remained weak, hinting at weak domestic demand. Producer prices are still in deflation….

Wells Fargo: Small Business Optimism Up Slightly in May Economic Uncertainty and Persistent Inflation Continue to Weigh on Outlooks

Summary Uncertainty Abounds Uncertainty surrounding expectations for economic growth and interest rates appears to be weighing on small businesses. The NFIB Small Business Optimism Index posted another modest gain in May; yet at 90.5, the index remains far below its 50-year average of 98. The primary stand out was a jump in the uncertainty index to its highest point since November 2020. As markets bet on when the Fed will ultimately cut rates, high financing costs are steadily chipping away at business sentiment. Sales, earnings and capital outlays also remained muted. Inflation is still the top challenge facing small businesses as the last mile back to 2% proves to be more difficult than previously anticipated. That said, compensation pressures do not appear to be a significant threat to reigniting inflation at the moment.

Wells Fargo: Do We Have Potential?: An Analysis of U.S. Potential Economic Growth

Summary An economy's long-run sustainable rate of economic growth—the rate at which it can grow over a long period of time at a constant inflation rate—is determined by underlying supply factors, specifically by its labor force growth rate and its underlying rate of labor productivity growth. Unlike actual GDP growth, an economy's potential growth rate is unobservable and must be estimated. While the concept of potential economic growth may appear to be largely an academic exercise to some readers, there are important real world consequences associated with potential economic growth. An economy that can grow at a robust rate for a sustained period will be better able to project economic and geopolitical power. Additionally, strong potential economic growth allows real economic growth to grow at a stronger rate without leading to higher inflation. In a five-part series of reports, which we collate in this compendium, we analyze the outlook for potential economic growth in the United States.

The potential growth rate in the U.S. economy has trended lower in recent decades as growth in labor productivity and growth in the labor force have both slowed. During the last decade, the labor force has decelerated due in part to slower population growth. Labor productivity—which is determined by growth in the capital stock, changes in labor "composition" and changes in total factor productivity (TFP)— has also softened. Though capital accumulation accelerated during the past decade, weak TFP growth significantly downshifted labor productivity growth. As a result, the Congressional Budget Office (CBO) estimates that the potential growth rate of the U.S. economy is only 2.2% per annum presently.

Though potential growth has been lackluster during the last decade, we look for it to grow more strongly in the next few years. Labor force growth has strengthened considerably in the past two years, due primarily to robust immigration flows and a post-pandemic rebound in the labor force participation rate (LFPR). We expect immigration to further boost the LFPR, alongside other factors such as the flexibility of remote work. The net capital stock has also exhibited positive growth recently, due in part to a surge in the construction of manufacturing facilities. We expect stronger growth in the net capital stock in the near future, especially due to spending on hardware and software that will be required to more fully develop automation and artificial intelligence (AI) capabilities in the business sector. TFP growth has remained lackluster in the wake of the global financial crisis, but there are some reasons for optimism. We anticipate remote work and AI will have the potential to lift TFP growth, which will ultimately strengthen labor productivity growth by the end of the decade, alongside the boost from capital stock growth.

Ultimately, we suspect the economy's potential growth rate will be stronger than what it averaged over the past expansion (~1.8%). Potential growth rates are challenging to estimate, but we feel reasonably confident that the potential growth rate of the U.S. economy could ramp up to 2.5 percent per annum by the end of the decade. A potential growth rate as high as 3% could be within reach if labor force growth does not sink back to rates of the past decade and AI adoption speedily diffuses throughout the economy.

… And from Global Wall Street inbox TO the WWW,

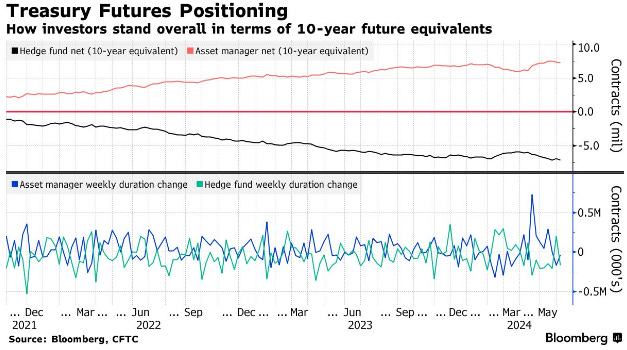

Bloomberg: Bond Traders Quick to Abandon Long Wagers Before Fed Meeting, CPI Data

Position exodus seen in 10-year futures since jobs report

Investors’ net-long position dropped to lowest in two months

… Asset Manager Duration Longs Unwound For the second week in a row, asset managers pared bullish Treasury futures wagers after CFTC data in the week up to June 4 showed an equivalent duration unwind of roughly 40,000 10-year note futures equivalents. Prior to this, asset managers had been extending long positions over several consecutive weeks from April 16 through to May 21. On the flip side, hedge funds extended their net duration shorts by roughly 168,000 10-year note futures equivalents, pushing overall net duration shorts through 7 million contracts.

Bloomberg: Pimco Warns of More Regional Bank Failures on Property Pain

Banks selling quality assets first to avoid big losses: Murray

Pimco has been amassing property portfolios for 18 months

Political uncertainty continues to drive Eurozone bond spreads, including a more noticeable nudge wider in Bund asset swap spreads. The key to overall rates direction stil lies in US data and what the Fed makes of it. A US CPI at consensus today, together with a potentially hawkish Fed, would support a bearish bias

… UST 10y yields have been sensitive to CPI releases this year

Yahoo: It could be time to start buying the dip on Treasury yields

Paul Ciana shares his technical outlook on Treasury yields.

ZH: Global Food Prices Rise For Third Straight Month, Fueling Instability Risks In Developing World

More of the As The Narrative Turns show AFTER today’s CPI and FOMC drama but for now

Dippin' Dot Mania Day !