As we kick off the beginning of the end (of Q2, H1, and fiscal year-end in Japan), I’ll skip right ahead as we’ve got lots to get through before Thursday’s NFP report — short weeks ALWAYS seem / feel long to me.

Click HERE for 30yy WEEKLY and HERE for 10yy MONTHLY (with some approximate Rosie levels etched in) and I’ll just ask …

Basking …

… lie exposed to warmth and light, typically from the sun, for relaxation and pleasure …

… are you basking, this morning?

June 30, 2025 at 12:30 AM UTC Bloomberg: Bond Traders Basking in Gains Bet Fed Will Fuel Winning Streak

…Investors who earlier this month saw a July rate cut as negligible are now pricing in nearly 1-in-5 odds for a reduction, with September seen as a lock. Even as Fed officials including Chair Jerome Powell favor waiting for clarity on the economy before easing again, traders are positioning for the possibility of earlier action should key measures such as employment weaken materially and inflation stay under control…

Rates options trades flagging the potential for lower yields and a faster pace of Fed easing have picked up markedly, while asset managers favor owning Treasuries in the five-year maturity range that would benefit from an eventual bigger Treasury rally extending into 2026…

…Disagreements among Fed officials –- who see between zero and three cuts this year and an even wider range of outcomes in 2026 — increases a chance for a policy mistake, said Jamie Patton, co-head of global rates at TCW Group. She’s favoring two- and five-year notes, which would benefit the most from a scenario where the Fed eases more than expected.

“There are over a dozen pilots sitting in the cockpit and they’re all disagreeing around the altitude of a destination airport,” Patton said. “That increases the potential for a bumpy landing if you don’t know where you’re going.”

Game ON. NFP Thursday and CPI on 7/15th to be extremely telling.

… here is a snapshot OF USTs as of 711a:

… HEREis what this shop says be behind the price action overnight…

… WHILE YOU SLEPT USTs are richer led by the belly in anticipation of month end flows, some light follow-through buying and selling in 7s-10s on profit-taking seen by the desk. Curve flows have been more active with steepening interest in 2s3s, 2s10s, and 5s30s from a number of accounts., mainly fm. That said, the curve has been able to maintain a flattening bias with 5s30s hovering around key technical resistance at ~100bps. Overall volumes are light at 60% as we approach NY, with S&P futures rising +0.4%, DAX futures -0.1%. The DXY is weaker -0.2%, while Crude is lower -0.3%, and Gold is +0.3%…

…Technically, we see a rising risk that the 4.25% resistance level in 10y yields could give way in the short-term, leaving USTs susceptible to a rally towards 4.125%, with a medium-term target of 4.00%.

… for somewhat MORE of the news you might be able to use … a few more curated links for your dining and dancing pleasure …

NEWSQUAWK US Market Open: US futures bolstered as Reconciliation Bill progresses, however July tariff deadline looms … Fixed benchmarks were contained overnight before EGBs picked up on numerous German data points … Contained overnight ahead of a busy and front-loaded week. Focus remains firmly on the trade and fiscal fronts; awaiting the reciprocal deadline and monitoring the Reconciliation Bills Senate passage respectively. While pertinent, the above developments have not changed the macro picture just yet with USTs in the green by just a handful of ticks within a narrow 111-22 to 112-00+ band, a range that is almost a repeat of Friday’s 111-22+ to 112-02 parameter …

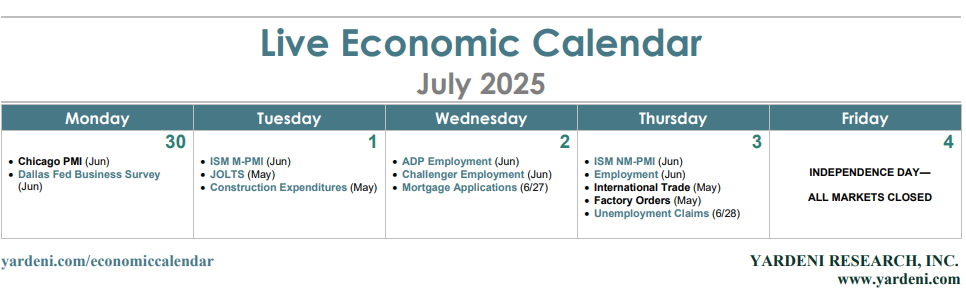

With the U.S. Independence Day holiday on Friday, the June employment report lands on Thursday. A Reuters poll shows economists expect to see a rise of 129,000, slightly below May's 139,000 increase.

Evidence of the impact on the economy from Trump's tariffs and their potentially inflationary effect, along with the mass layoffs among government employees and the likelihood of big cuts to a raft of welfare benefits is starting to materialise in other data points.

So far, the monthly non-farm payrolls report has not been one of them. May's number marked the fifth upside surprise in the past 12 months, and the ninth reading below the 200,000 mark over the past year. Layoffs are historically low, but hiring is not exactly booming.

The most recent weekly jobless claims numbers showed the number of Americans filing new applications for jobless benefits fell, but work opportunities are becoming scarce as businesses are reluctant to hire while things such as import tariffs are in flux.

Finviz (for everything else I might have overlooked …)

Moving from some of the news to some of THE VIEWS you might be able to use… here’s some of what Global Wall St is sayin’ …

As always, there’s different ways to view data and here’s latest example of this from across the pond, in review of Chinese data …

The recovering new export orders and shipping data suggest exports could remain resilient in June. The rebound in construction PMI indicates improved infrastructure investment. But we see more signs of deterioration in the labour market, and no signs of improvement in industrial profits.

… The US tax bill should be finalised this week although at the moment it needs to pass the Senate today (or possibly tomorrow), after a drama filled weekend of horse trading, and then back to the House for final approval. The President wants it done by Friday's holiday. At that point attention will swiftly focus to the July 9th deadline extension for reciprocal tariffs. Indeed you'll probably get headlines build up this week and the risk to the market is that with the S&P 500 hitting a new record high at the end of last week, with Treasury yields more becalmed, and with a new tax cutting bill, it's possible that the Trump Administration feels emboldened to be aggressive again. On Friday the US announced that they were stopping trade talks with Canada in retaliation for their digital service taxes and that new tariffs would be launched within a week. However, overnight Canada has dropped this tax to enable talks to restart. This is perhaps a warning shot for the world. So before next Wednesday a lot of water will flow under the global trade bridge…

…For payrolls, DB expects the headline number (+100k forecast vs. +139k previously) to be slightly below the consensus of +113k, with a similar story for private payrolls (DB +100k, consensus +110k, vs. +140k previously). This would also be below the three-month average of 135k and 133k, respectively. Their rationale is based on 1) initial jobless claims being up 8.8% during the June survey week relative to May; and 2) their observation of a recent pattern of subdued summer payroll gains. They also expect the unemployment rate to edge up a tenth to 4.3% but with the risks skewed to it staying unchanged.

Although 100k on payrolls seems low, our economists think the breakeven rate which keeps the unemployment rate steady, is around 100k at the moment and could even be as low as 50k given the Trump Administrations' migration policies. If correct we could have a situation where low payroll growth still tightens the labour market. See US Economic Perspectives: Potential paths for breakeven employment for more on this…

Here are a few words from a domestic shop on rates, tariffs, stocks and reason for economic forecasting (to figure out why they are wrong)…

June 30, 2025 MS: The Tariff Singularity | Global Macro Strategist

Tariffs, with related US government revenue annualizing over 1% of US GDP, rarely represent a zero-sum game, even ignoring deadweight loss. Investors hand-wring about who bears more of the cost – the producer or the consumer – but miss the bigger picture that keeps us bullish USTs and bearish USD.

Key takeaways

If tariffs are taxes, consider this: so far in June, on an annualized basis, US importers paid the equivalent of 65% of corporate income taxes paid in 2024.

Framing tariffs in relation to after-tax profits in 1Q25, US import tariffs in June, annualized, represented 15% of non-financial corporate profits after tax.

1Q25 profit margins would have fallen to 11.7% from 13.8%, well below the 15-year moving average of 12.2%, if corporations absorbed all tariff expenses.

Equity markets have been resilient since bottoming in April, and the rally has been more fundamentally-driven than many appreciate. While there could be some consolidation during 3Q, we remain bullish on a 6-12 month horizon as EPS tailwinds expand, and the market has line of sight to Fed cuts.

Rate of Change Is Improving on (1) Earnings Revisions…

…(2) Market Expectations of Fed Policy…As noted last week, the equity market isn’t going to wait for the obvious signal in terms of a more dovish shift in monetary policy from the Fed—i.e., stocks will get in front of it. Our economists see the Fed cutting 7 times next year, a dynamic that’s likely to be a 2H25 tailwind for back-end rates and valuation. In fact, there are already early signs the equity market is starting to price this now. Our work shows equity performance is strong during Fed cutting cycles even if this tailwind starts to get discounted ahead of time. Recent survey and micro data points suggest employment may be more of a risk than inflation. To the extent this brings forward expectations for cuts, it's likely constructive for stocks assuming we don't see an accelerative rise in the unemployment rate/multiple negative payroll numbers in a row (not our economists' baseline).

…And (3) Other Policy/Geopolitical Dynamics…

… The growth deceleration to start the year also did not elicit any response from the Fed, which further weighed on stocks into the April capitulation (Exhibit 1).

…the equity market is likely to price a more dovish reaction function from the Fed as we head into the second half of this year, and this transition has likely begun over the past couple of weeks. In fact, the Bloomberg Fed Sentiment Natural Language Processing Model is also indicating that the Fed and its various members have already started to hint at a less hawkish tone. As noted, this is just another reason why equity markets have remained so strong.

A good friend of mine likes to say that the main reason that he forecasts is to find out why he was wrong. Our view of a meaningful deceleration in the US and the global economy from tariffs and other policies has yet to play out. We find ourselves waiting. So, while we wait, we take stock of the questions that clients are throwing our way…

…One could pose a similar question for the US. For an administration that bills itself as pro-growth, imposing tariffs and restricting immigration will lead to a slowdown and higher inflation. But the question we get from clients is whether tariffs really matter all that much. After all, in the last US CPI print, there was only a little evidence of the effect. A key point we have been making about tariffs since before the US election is that tariffs take about three months before they show through to inflation. With tariffs trickling in in February and March and then stepping up notably in April, it is simply premature, in our view, to expect inflation to have picked up meaningfully yet. We do expect the next two prints, however, to show the upward trend in prices.

Rather than simply waiting for our prints to come, we have also tried to pressure test our view. The Purchasing Managers' Index (PMI) output prices seems to have decent historical correlation with core inflation, and anecdotal evidence, such announcements of price changes automakers, the timing of inventory depletion, and reports from some retailers give us some comfort and confidence. The timing matters a lot, though, and is unfortunately highly uncertain. We do not think the Fed cuts rates this year, while the market has priced in a cut in September. For us to be right, the higher inflation has to show meaningfully before that meeting.

With a series of tariff deadlines approaching, this note reviews historical experiences of trade negotiations to help set expectations and identify what we will be focusing on in the outcomes. We also consider how the negotiations affect the transmission of tariffs to economic data.

Key takeaways

Trade negotiations usually span years not months, which suggests any near-term outcomes would likely take the shape of framework agreements or narrow deals.

The recent UK and 2018/19 China experience suggests July (and August) may be milestones in a longer negotiation journey.

The interaction of country (reciprocal) versus sector (Section 232) tariffs remain an open question; we see the July deadlines as informing how they interact.

The timing of tariff impact on the economy will be affected by the actual application of tariffs as well as the negotiated outcomes.

Over the past few days, Canada and the US stopped talking about trade, and started talking about trade again. Unusually, this was not a unilateral retreat by the US—Canada surrendered its digital services tax. Markets, quite rightly, are ignoring all of this. US President Trump cut taxes on US consumers of UK cars—from today the tax goes to 10%.

The US Senate is trying to pass a budget. Markets expect this will keep the US fiscal position on an unsustainable path (ideas of deficit reduction generally rest on some very heroic assumptions about economic growth and tax revenue). As US debt levels grow, it is worth remembering that private sector wealth is at a record high. The US government may, in time, seek to mobilize that wealth to finance the growing deficit…

Economic Comment: July 9 is fast approaching On July 9 substantial additional tariffs could snap into place after having been postponed on April 9. On Thursday, White House press secretary Karoline Leavitt was asked about the July 9 deadline."Perhaps it could be extended but that's a decision for the president," she said. Despite a significant juncture for economic policy approaching in the next two weeks, information on what happens appears to us to be elusive. Reports note some negotiations are ongoing, rasing hopes of trade deals, which could be a reason to postpone some tariffs further but perhaps not others. President Trump said on June 11 that he would set new tariffs unilaterally. What those would be is unclear, and that seemed to be what happened on April 2. There also seems to be a lot of optimism considering two options for what might be on the table for July 9 are keeping existing high tariffs or adding some that are higher…

The Week Ahead: June employment report likely suggests slowing Released on Thursday due to the Friday holiday, we expect to see a step down in the pace of nonfarm payroll employment gains in June to 100K, and an increase in the unemployment rate to 4.3%, as incoming indicators suggest hiring has cooled over the last several weeks. We walk through the risks starting on page 22. On Tuesday, Chair Powell joins other central bank chiefs on a panel, in a week somewhat light on Fed speak. We expect the ISM manufacturing composite edged up but remained below 50 in June. Although we don't forecast the month-to-month volatility in the JOLTS, we expect the general direction of travel for openings is lower. Lightweight vehicle sales will offer the first hard data of the month on consumer spending…

… finally, from Dr. Bond Vigilante, a few thoughts on the big / holiday-shortened economic week ahead …

Jun 29, 2025 Yardeni: ECONOMIC WEEK AHEAD: June 30-July 4

It may be July 4th week in the US, but we don't expect many fireworks on the economic data front. Of course, surprises could come from events in the Middle East, as Israel, Iran, and the Trump administration figure out whether the ceasefire will hold or missiles will start flying again. Surprises could also come from Trump's trade negotiations. A bunch of deals are expected in coming days.

On Capitol Hill, the Senate today passed a revised version of President Donald Trump's 940-page Big, Beautiful Bill, getting it closer to Trump's July 4 deadline. The question now is whether the House will embrace Senate alterations to the original House version of the legislation.

The markets will also pay close attention to a speech (Mon) by Federal Reserve Chair Jerome Powell. Speaking in Sintra, Portugal, Powell may drop a hint or two about whether last week's mixed data on trade, housing, and consumption might have altered his view that rate cuts aren't under serious consideration at Fed headquarters.

Fireworks or not, here's a brief look at this week's economic data highlights:

(1) Employment report. The release with the greatest chance of influencing the Fed's wait-and-see approach is the June jobs report (Thu). We're expecting hiring activity to remain reasonably brisk now that the fog of war is lifting in the Middle East and in US trade relationships. The jobless rate might tick up to 4.3% or even 4.4% given the modest upturn in initial unemployment claims (chart). We expect that a solid gain of 125,000-150,000 in payrolls should allay recession fears.

(2) Unemployment claims. We expect initial claims for unemployment insurance (Thu) to confirm that layoffs still remain low as reported by Challenger (Wed) (chart). Continuing claims may suggest the duration of unemployment is increasing for some. Yet overall, we look for fresh confirmation that industries from healthcare to leisure and hospitality are benefiting from the Baby Boomers’ splurging on restaurants, cruises, and other entertainment.

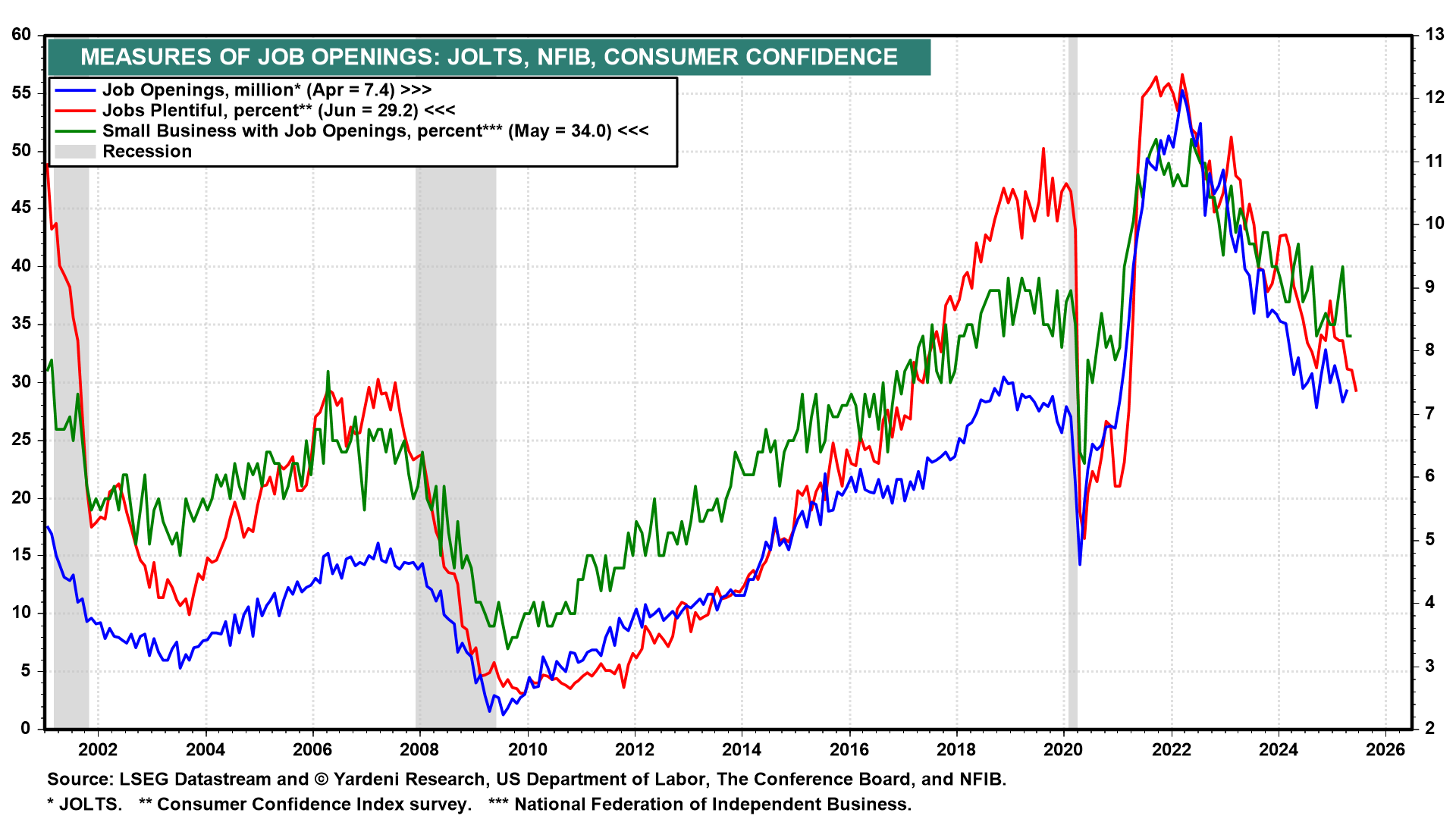

(3) JOLTS. The May Job Openings and Labor Turnover Survey (Tue) takes on greater importance as economists search for signs that the labor market is cracking. The healthy April reading surprised many, as the available jobs component increased by 191,000 from the previous month. We see little evidence to suggest that May’s reading won’t likewise point to solid employment conditions (chart).

(4) Regional Fed surveys. The hard data/soft data disconnect continues to confound many. Given the strength of the former and tentativeness of the latter, regional Fed series could offer useful signals. May's Chicago Business Barometer (Mon), which is a regional purchasing managers' index, saw its 18th consecutive month of contraction (chart). The Dallas Fed's May business survey (Mon) also showed the trade war taking its toll. Going forward, both gauges bear watching for signs of stabilization after Trump delayed his "reciprocal tariffs" on April 9.

… And from the Global Wall Street inbox TO the intertubes, a few curated links …

Aren’t we all …

June 30, 2025 Apollo: Fed Worried About Stagflation

When FOMC members produce their forecasts ahead of Fed meetings, they are also asked how they view the risks to inflation and unemployment.

Currently, there are no FOMC members who foresee downside risks to the unemployment rate or inflation, see charts below.

In other words, the Fed continues to forecast stagflation and is concerned that we may experience rising inflation and rising unemployment at the same time.

These worries are likely driven by higher oil prices, tariffs, and immigration restrictions, all of which are putting upward pressure on inflation and unemployment simultaneously.

A view (on stocks vs bonds)from The Terminal …

June 30, 2025 at 4:00 AM UTC Bloomberg: With a Weakening Dollar, It’s America Second The new S&P 500 record doesn’t look like one in any other major currency. By John Authers

… It’s also more or less impossible to say that stocks are decent value compared to bonds. This rally, combined with sticky Treasury yields as the Federal Reserve resists cutting rates, has brought the earnings yield on the S&P (the inverse of the price/earnings multiple) below the 10-year Treasury yield. Buy now and you are receiving no compensation for the extra risk of stocks compared to bonds:

This points to another key explanation for the rally: The belief that rates and longer-term yields will soon fall. That’s in part because of the increasing pressure on the Fed, and the likelihood that it will soon be under the charge of someone more dovish. Any signal that the Fed’s independence is in question would do further damage to the dollar, but that would not be a problem for domestic investors in US equities.

There’s also a prevalent belief that the Fed should cut rates. That would follow from a belief that tariffs’ impact on inflation is exaggerated (which we’ll return to, and will be tested by the forthcoming employment data) and also from concern over the housing market, which is showing serious signs of cracking (see below).

There are always upside risks with the stock market to go with the downside, and there are plenty of them (as Jonathan Levin points out). This all-time high still looks premature.

A(nother)mid-year outlook (and a few slides from THE DECK which caught my eye) …

June 27, 2025 NewEdge: Mid-Year Outlook: The Summer of Mudd

Economic Data Has Been Surprisingly Bad in Q2

…Inflation Was in the “Last Mile” Down to Target as of May

…Inflation Concerns Are Keeping the Fed on the Sideline Despite Weaker Growth

…Bond Yields Have Not Been As Responsive to Weak Data

…60/40 Portfolio Performing Well Despite April Stock Market Correction

Finally, from ZH, a BAML note …

Saturday, Jun 28, 2025 - 10:40 PM ZH: Hartnett: These Are The Best Trades For The Second Half Of 2025

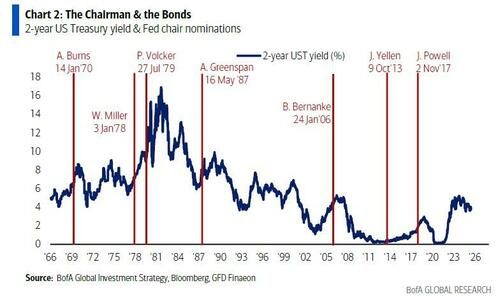

… Central banks slashing rates is just one reason for the meltup, the other one is that Trump is now widely expected to nominate the new (shadow) Fed Chairman early fall (with the guarantee that many more rate cuts are coming), but as Hartnett notes, bonds always test the new Chair, and in the first 3 months following the 7 Fed nominations since 1970 (Burns, Miller, Volcker, Greenspan, Bernanke, Yellen, Powell) yields are up every time (2-year +65bps, 10-year yields +49bps), the US dollar is down 2%, and the S&P 500 is mixed.

… Moving on to Hartnett's weekly comments on markets, we start with Price & Positioning, where the BofA strategist points out that while contrarian trades worked in H1, and no guarantee they work in H2 (especially as - US dollar and gold aside - there are no big positioning extremes in Jun), but for what it’s worth the contrarian trades for H2 based on H1 performance, sentiment, flows are…

Long US dollar,

Long oil, short gold,

Long US consumer discretionary, short EU banks

Long airlines, short defense,

Long Mag7, short China tech,

Long REITs/homebuilders, short infrastructure,

Long small cap value, short momentum.

… finally, proud to announce all that hard work finally paid off with heat really setting in AND summer-time getting into full swing here …