Good morning … Happy BoE Day! Watch what they said not what they did as yet another member of the global central banking committee proves YOU know more than they do with regards TO your personal situation and the (grim)realities of the ‘flation.

BoE Hikes 25bps to 1% in 6-3 Split Vote, WARNS OF UK RECESSION Later This Year -ZH

THAT was fun. While it is being called a DOVISH (for stocks) hike, I’d suggest just the opposite. I’m thinking if it as more of a BEARISH, not bullish (stocks and BONDS) hike. Here’s why,

… should the Federal Reserve cease in their efforts to calm inflation before it has been fully restrained, bond investors should be wary.

HIMCOs Q1 missive HERE IF, somehow, you missed it. IF this is the beginning of the Fed letting down their guard then those invested/trading the longer end of the curve should become increasingly uncomfortable. Unless, of course, one views enough being priced and ultimately, a harder landing for stocks just ahead, THEN, there’s every reason to think rates will once again become safe haven it once was. More on THAT in a moment.

As history is still being written and not yet knowable, we’ll just have to sit by and wait / watch to see how they do BEFORE we rush to judgement.

Whether or NOT 75bps hike is/was appropriate and coming, well, was source of debate (mostly on Nomura desk which then leaked into market psyche — last weeks decline?) and it was put to bed swiftly …

Meanwhile, for a more topical run down of what it was that happened,

“Highly Attentive” Fed Unleashes Biggest Rate-Hike Since Bursting The Dot-Com Bubble -ZH

ADP was weak(est since COVID -ZH), trade deficit EXPLODES (ZH) and UST CUTS auction sizes (MORE than expected -ZH)

By days end, a DOVISH / BULLISH (STOCKS) hike is how the record books will have seen this one and John Authers morning note (Powell Won’t Welcome Being Seen as Dovish) shows,

… the stock market had its best day in two years, with the S&P 500 gaining almost 3%, virtually all of it coming after the news from the Fed:

ZH offered somewhat DIFFERENT angle of the same concept noting,

… this was the greatest upside-day for the S&P 500 on a Fed Rate-Hike day since Nov 1978!!

Do NOT read what happened next. Authers continues attempting to put / keep moves and TRENDS in context.

… Meanwhile, one of the most important facts of post-GFC life appears to be over. For decades before the crisis, it was taken as axiomatic that bonds should yield more than stocks to compensate investors for the lack of opportunities for capital growth. In late 2008, to much horror, the dividend yield on the S&P 500 at last overtook the 10-year Treasury yield. Put differently, this meant that stocks looked to be a spectacularly good value compared to bonds. With 10-year yields and stock dividend yields remaining close throughout the last decade, there has continued to be great support for equity valuations. That’s no longer the case:

It’s always possible that an accident somewhere in the financial system will send investors rushing back into bonds again, as has happened on the other times when the downward trend was threatened. It’s also possible that money will flow into bonds now that they actually seem to be decent value for the first time in a decade…

… Just a few things to consider on this ‘moving day’ between ADP and NFP …

Said another way,

… here is a snapshot OF USTs as of 725a:

… HEREis what another shop says be behind the price action, you know,

… Overnight Flows Treasuries were modestly weaker in the front end of the curve while retaining the bulk of yesterday’s bid in the long end. There was a muted responses to the disappointing German orders data as investors awaited the Bank of England’s rate decision. Japan’s market closed for Children’s Day… -BMOs morning outlook, “Stabilizing, not Stable”

… and for some MORE of the news you can use » IGMs Press Picks for today (5May) to help weed thru the noise (some of which can be found over here at Finviz).

Here are a few MORE things to consider ahead of tomorrows NFP.

First up from the trends and charts department, 1stBOS techs ahead of the FOMC included some MONTHLY charts of 5s, 10s and 30s — bearish across the board. These words and this visual stood out

… 2yr & 5yr US Bond Yields are both critically placed around the “necklines” to their 2018 tops at 2.785% and 3.01/05% respectively. However, we stay biased towards a break above these levels and a deeper move higher, with the next supports at 2.945% and 3.09% respectively…

30yr US Bond Yields have broken to new highs after rebounding from their 13-day exponential moving average.

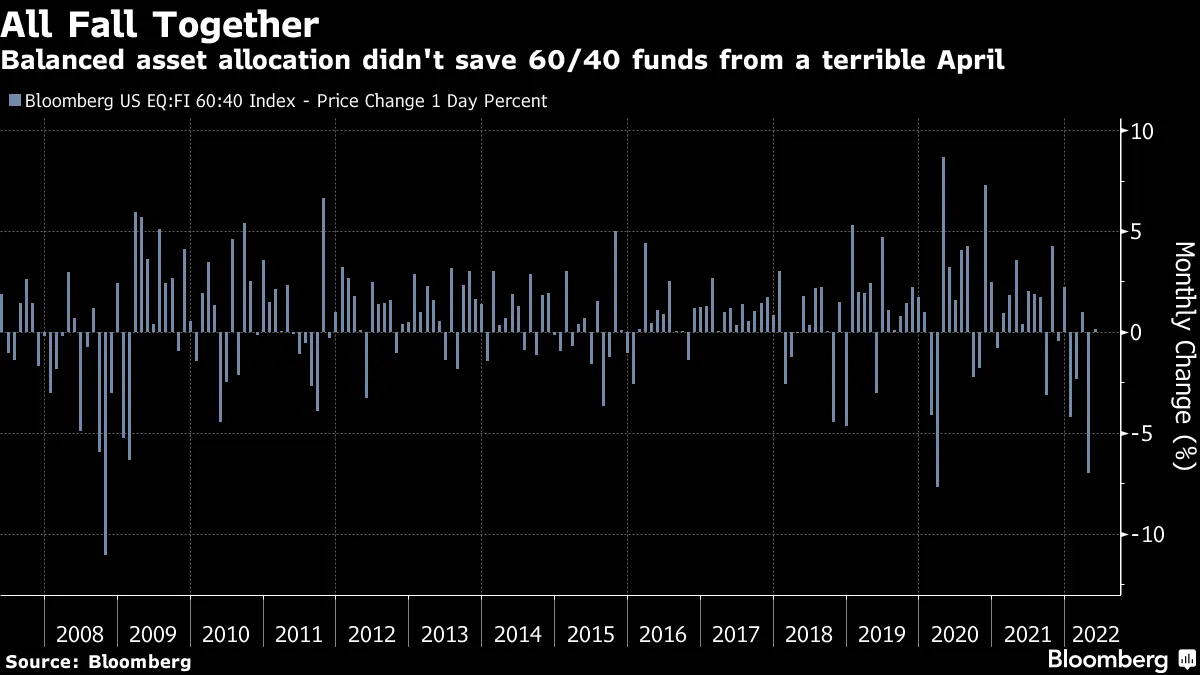

…Finally, not sure how I missed this one (well, yes I am) but yesterday I highlighted John Authers' note / VISUALof how the party at Club 60-40 is OVER and this largely a reflection of the fact / visual noted by DBs Jim Reid — US10yrs have had worst start to year since … wait for it … drumroll please,

… Talking of Treasuries, today's CoTD shows that 2022 so far has seen the worst total return start for the 10yr Treasury since 1788, just before George Washington's presidency. A remarkable statistic which shows how much the market has been blindsided by inflation…

Mean reversion. Think DOGS OF THE DOW idea. That which underperformed — to a HISTORIC amount — might JUST be ready to OUTperform?

That in mind, I’d like to wish one and all a very Happy

Sorry. Not sorry … THAT is all for now. Off to the day job…

{kind=link}