Treasuries were little under modest pressure overnight with the flattening momentum still evident. 5s/30s dipped to 54.6 bp as 30s returned to 2.06% despite tomorrow’s long bond auction. Overnight volumes were above the norm with cash trading at 119% of the 10-day moving-average. 5s were the most active issue, taking a 32% marketshare with 10s a close second at 31%. 2s and 3s combined to take 23% at 11% and 12%, respectively. 7s managed 8%, 20s 1%, and 30s 5%. We’ve seen buying in 3s, 5s, and 20s.

And for somewhat MORE, from the orignators OF the catch phrase,

WHILE YOU SLEPT

Treasuries are modestly lower and the curve flatter this morning as the December CPI print is awaited. DXY is little changed while front WTI futures have extended their gains (+0.8%). Asian stocks were smartly higher (Hang Seng China Enterprises index up nearly 3%), EU and UK share markets are mixed/higher while ES futures are little changed here at 7am. Our overnight US rates flows saw a tight range overnight with Asian real$ buying seen in intermediates alongside hedger-related selling in the long-end. The Fed will buy back ~$1.8bn in 22.5y-30y USTs this morning. Overnight Treasury volume was ~70% of average all across the curve- including in 10yrs which are up for a reopening this afternoon.

SO volumes were either ABOVE (10d)MA or a fraction OF (some other day)MA. Whatever you want to believe, go right ahead. It looks to ME (as per visual above) there’s not much to see here BEFORE CPI.

The White House braces for a 'brutal' inflation report Axios

That in mind, CPI and PPI in CHINA declined overnight. We’ve got THAT going for us — here’s Goldilocks’ bottom line,

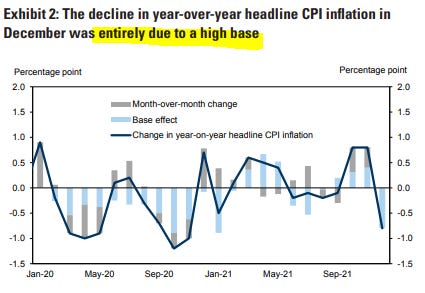

China's CPI inflation fell to +1.5% yoy in December (vs. +2.3% yoy in November), primarily due to a high base of food prices and a sequential decrease of fuel costs. PPI inflation fell to +10.3% yoy in December, lower than market expectation, from +12.9% yoy in November, primarily on a sequential decrease of prices in upstream sectors. We expect CPI inflation to stay moderate and PPI inflation to decline further in the near term.

… China’s headline CPI fell to +1.5% yoy in December from +2.3% yoy in November, primarily due to a high base as shown in Exhibit 2. In month-on-month terms, headline CPI fell to -0.1% (seasonally adjusted annualized rate) in December (vs. +4.9% mom s.a. ann in November).

From BBG setting the table for day ahead

Treasuries Steady, Front-End Lags Ahead of CPI, 10-Year Auction

Treasuries are marginally cheaper across the curve, while front-end underperforms ahead of December CPI release at 8:30am ET. Stocks advance with miners, oil & gas sectors outperforming over European session. Session highlight also includes 10-year note auction, a $36b reopening.

Treasury 2-year yields higher by 1.8bp vs. Tuesday close while rest of the curve is less than 1bp cheaper on the day; 10-year yields around 1.74% with both bunds and gilts outperforming by over 2bp in the sector

S&P futures higher by 0.15% while Estoxx50 advances 0.5% in early Europe session

December CPI figures may show inflation climbing to 7.0%, a result which could see front- end fully price in a March rate hike (currently priced at 85%)

U.S. auctions resume with $36b 10-year reopening at 1pm, followed by $22b 30-year reopening Thursday

WI 10-year at around 1.745%, above auction stops since January 2020 and ~23bp cheaper than December stop-out which tailed 0.4bp

IG dollar issuance slate includes five deals; borrowers priced $15.2b Tuesday, paying an average 9bp in concessions

Three-month dollar Libor -0.60bp at 0.23843%

U.S. economic data slate includes December CPI (8:30am) and monthly budget statement (2pm)

Fed speakers include Kashkari at 1pm; Fed releases Beige book at 2pm

AND From BBGs Macro Squawk team approx 615a,

Risk Assets Rally as Market Awaits Inflation Print

European equities climb back toward opening highs after a choppy first hour of cash trading. Euro Stoxx 50 adds 0.7%, FTSE 100 outperforms at the margin. Miners, oil & gas and tech are the strongest performing sectors. S&P futures hold in the green, Nasdaq futures recover toward Asia’s best levels ahead of today’s inflation print. Fixed income is mixed: bunds and gilts drift higher, 10y point outperforming. Bund futures regain 170. Cash USTs bear flatten, cheapening roughly 2bps across the short end. Peripheral spreads tighten slightly. In FX, Bloomberg Dollar spot pops back up to flat on the session. Commodity currencies outperform but trade off best levels with G-10 FX generally trading narrow ranges. Crude futures fade a modest push higher. WTI stalls after a test of $82, Brent trades near $84. Spot gold drifts slightly lower near $1,817/oz. Base metals are in the green with LME nickel up 4%. KEY HEADLINES:

Villeroy: ECB to do what’s necessary to get inflation around 2%

Germany tells banks to build EU22bn in capital buffers

Spain plans minimum wage increases for 2022, 2023: Expansion

EU warns on frequent boosters; China stops flights: Virus Update

China December CPI 1.5% vs 1.7% est, PPI 10.3% vs 11.3% est

China’s Dec. new loans 1.13T yuan vs 1.25T yuan est.

The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($647,200 or less) increased to 3.52% from 3.33% for loans with a 20% down payment.

That is the highest rate since March 2020. It was 64 basis points lower the same week one year ago.

Mortgage applications to purchase a home rose 2% last week compared with the previous week.

Mortgage rates have moved to their highest level in more than a year, and that may have potential homebuyers nervous that their affordability window is closing faster than expected. Home prices are still gaining, and winter is historically the slowest season for the housing market, but mortgage demand from buyers moved higher…

Nothing without consequence … As far as some other news you can use, HERE are IGMs Press Picks from earlier today which was the first place I saw this, from the FT,

Surging real yields blow hole in ‘everything rally’ (FT) Rise in expected bond returns after accounting for inflation poses ‘test for risk assets’ … “Realyields tell you the true level of funding costs, without hiding behind inflation, so we’re going to learn a lot about the genuine health of corporate balance sheets”

Thats it for now. Not sure when next update will be (yesterday there were quite a few) so for now, good luck out there and don’t forget to get those bids in for 10s early and often…Back to the day job…