Good morning. After yesterdays coyote UGLY 10y auction (biggest tail in years post CPI), we’ll get another chance for redemption and measure of ‘demand’ with this afternoons long bond auction…

Whether or not the likes of Lacy Hunt / HIMCO are going to be in buying remains to be seen.

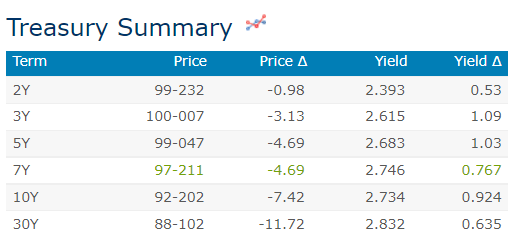

Meanwhile, here is a snapshot of UST rates, prices and moves as of 715a…

… And HEREis what other shops saying behind the overnight price action …

WHILE YOU SLEPT USTs are mixed and steeper, outperforming UK Gilts (10y +4.5bps) after a higher 1.1% MoM (0.7% exp) March UK CPI, while future volumes have tailed off after a 'better-bid' was found in Tokyo overnight. There was a 4.2k FV buyer at 4am, which helped USTs off the lows (2s5s10s -1bp). Risk-assets are divergent, SHCOMP -0.8% and NKY +1.9% overnight on a USDJPY move >126, while DAX futures are -0.7% and SPX is showing +0.4% here at 6:45am. 2s10s remains biased steeper in early action (+2.5bps) after yesterday's continued TU block buys (falling OI consistent with short-covering). The DXY is marginally higher, still above the 100-figure, while Oil (+1.3%) is recouping the 100-handle as well.

… and for some MORE of the news you can use, head TO Harkster.com … Knowledge without the noise (and if its ALL the noise and links you like, Finviz).

From the Global Wall Street inbox department, first a few (more)charts from 1stBOS weekly MACRO thematics

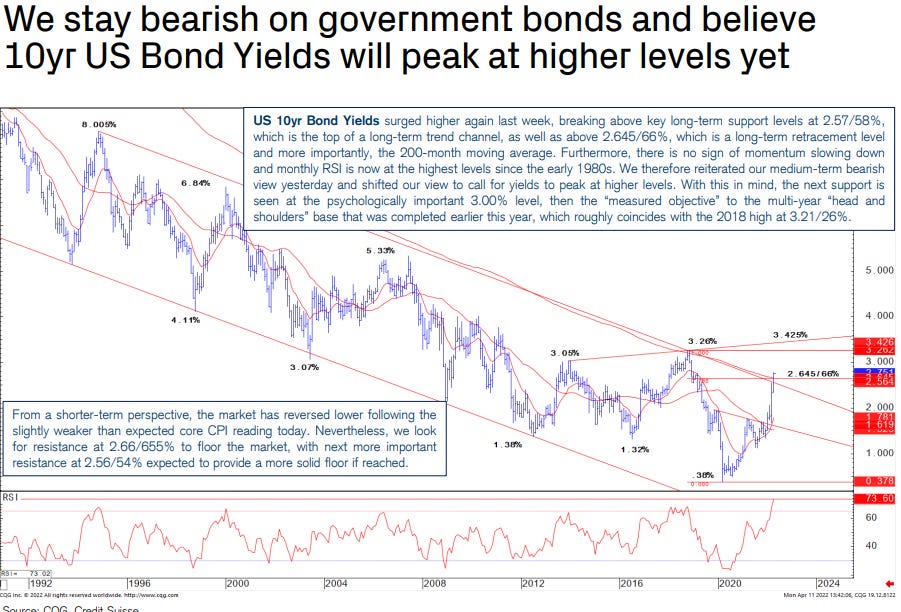

* Although we have seen a short-term pullback in global rates markets today following the slight miss in core CPI, the 10yr US Bond Yield maintains last week’s breakout above secular support levels including the top of it’s multi-year trend channel and more importantly above the 200-month moving average. We therefore maintain our core bearish view on government bonds and expect higher yields to remain a key cross-asset driver, particularly for a higher USDJPY, but also the outperformance of defensive equity market sectors and markets, as we saw in 2018 when the Fed was previously tightening policy.

* 10yr US Bond Yields saw a near-term pullback today but with no signs of momentum exhaustion and with a major breakout in place, we stay medium-term bearish, with the next major supports at 3.00% and eventually 3.21/26%.

* 10yr US Real Yields are also pausing from just ahead of our prior core objective and key support at -.04%, however we now look for an eventual move beyond here, with the next major support at .245/25%. If US Breakevens top out, the risk is for a move beyond .245/25% in Real Yields.

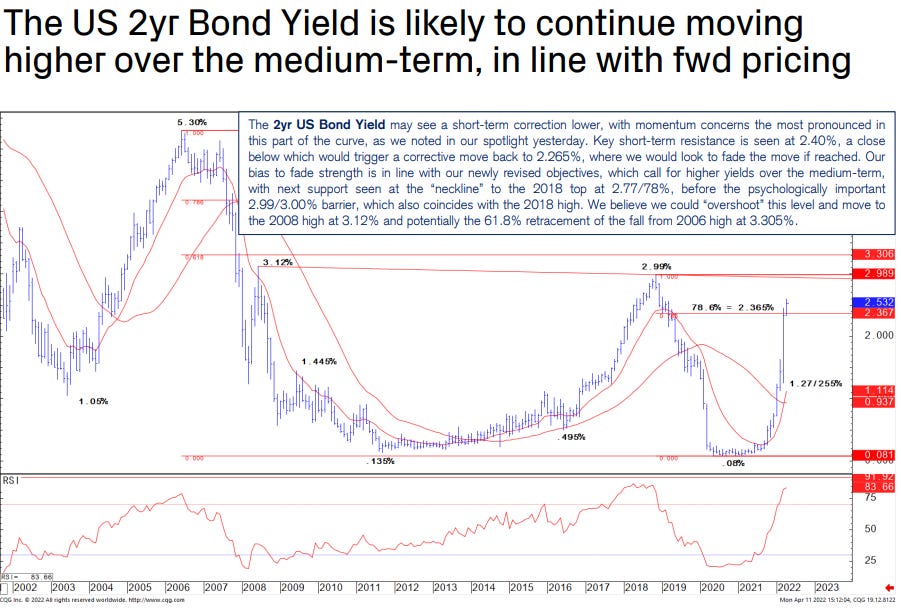

* The 2yr US Bond Yield is the main part of the US curve where we have seen a clear loss of momentum, however we look again to fade rallies and believe the market will eventually break above it’s 2018 high. Resultantly, we also look to fade further steepening in the 2s10s Bond Curve…

As Global Wall Street awaits latest thoughts from Lacy Hunt / Hoisington to drop (ok, maybe its just ME and a couple other bond folks) AND as far as THE Big $hort goes, the very latest from Zoltan Pozsar just may tide you over

The rise of Bretton Woods III – the new monetary world order that we’ve been busy imagining since the outbreak of the war – and the corresponding rise of (1) the renminbi, (2) commodities, and (3) monetary gold as reserve assets to upend the dominance of the U.S. dollar and the “exorbitant privilege” mean a relative decline of the ancienrégimemonétaire and its instrument: the Eurodollar.

Not a demise of the Eurodollar. A relative decline of it…

…which should naturally give rise to a set of “big shorts”.

The big shorts will include the U.S. price level (shorting inflation expectations), shorting policy rates, shorting the curve inversion (the yield curve has gone mad), and shorting some U.S. dollar FX pegs and the U.S. dollar versus the renminbi…

Perhaps a bit TOO much there, there to digest before your 2nd gallon of coffee and quite possibly could have used something a bit, well, lighter. The latest from Scott Minerd and GUGGENHEIM, then, offers,

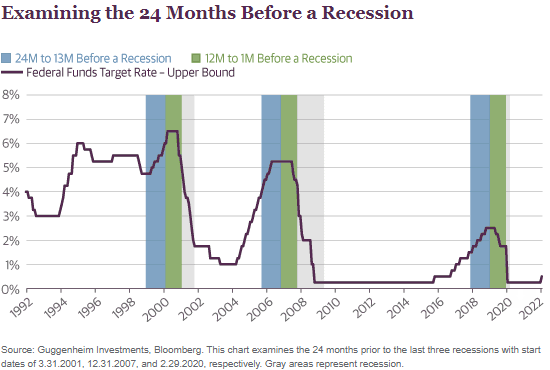

As the Federal Reserve (Fed) ratchets up its hawkishness—both in Fedspeak and in the latest minutes—the resulting market volatility and bouts of yield curve inversion show investors are discounting tighter and tighter financial conditions. The Fed has only just begun a hiking cycle and is contemplating shrinking its balance sheet as soon as May. The Fed’s policy, in its simplest formulation, is designed to slow down the economy, even to the point of recession, to try to tame inflation. The economy is still growing vigorously and the execution of Fed policy has yet to fully unfold, so fears of an imminent recession are overblown. But it is not too early to think about how different asset classes and market sectors perform in the period leading up to a recession.

… The conclusion is quite straightforward: Riskier assets have tended to perform well when the expansion is still in its penultimate year because this period, which historically overlaps a Fed hiking cycle, takes place when growth is strong. Strong growth means healthy corporate earnings, a stable labor market, low corporate defaults and bankruptcies, all of which support the performance of equities and high yield credit. However, by the final 12 months before a recession, rate hikes have tightened financial conditions and slowed economic growth. This environment tends to see lower-risk, longer-duration assets outperform riskier sectors. It is at this point, just a year out from recession, that investors should look to become more defensive. Because as Sir John Templeton famously said, the four most costly words in investing are “This time is different.