while we slept -- 5yy --most interesting chart; 'moment of truth, or denial?'; glass half empty; stocks vs bonds, worst H1 on record ... CONFIRMED (can we move on, now?)

CNBC: Treasury yields fall as recession fears continue to dampen risk sentiment CNBC: Stock futures slip after another losing week on Wall Street

… here is a snapshot OF USTs as of 735a:

… HEREis what another shop says be behind the price action, you know,

WHILE YOU SLEPT Treasuries are lower and the 2s5s curve is flatter- Tsys perhaps playing catch-up to sell-offs in Bunds and Gilts yesterday (both those markets rallying back and outperforming USTs today). DXY is sharply higher (+1%) while front WTI futures are modestly lower (-0.5%). Asian stocks were mixed, EU and UK share markets are all in the red (SX5E -0.75%) while ES futures are showing -0.5% here at 7:25am. Our overnight US rates flows saw Asian real$ selling in intermediates after Friday's sharp rally. During London hours, Asian losses were retraced with real$ names buying intermediates and 10's outright. Flows in the under-performing front end have been 2-way with banks selling 1.5-2y paper while asset managers bought the dip via off the runs.

… UST 5yrs, monthly: This is the most interesting chart. Monthly momentum consistently guided bearishly from the start of 2021 (breakout above 0.50% range highs then) until last month's peak near 3.62%. Now two things are happening: 1) Long term momentum is rolling bullishly (a clear sign that buyers are asserting more control over the sellers) and 2) last month's rejection of levels above the 2018 cycle high traced out a giant Shooting Star- a classically-formed bear exhaustion signal. We will almost certainly need a daily close <2.71% to signal sustainability for these new signals. Watch for that and remember it's a resistance until it's not...

… and for some MORE of the news you can use » IGMs Press Picks for today (5 July) to help weed thru the noise (some of which can be found over here at Finviz).

Here are those ‘few things’ promised. To begin, we must know what happened yesterday — 4th July — when global bond markets were open for biz. DBs Jim Reid

… We’ll start with markets in Europe since they were open yesterday. The biggest story there was a sizeable selloff among sovereign bonds as they gave up some of their gains over the last couple of weeks. Yields on 10yr bunds were up +10.1bps, but they were one of the better performers given the risk-off tone and yields on 10yr OATs (+12.7bps) and BTPs (+15.8bps) saw even larger rises, which followed comments from Bundesbank president Nagel who said that it was “virtually impossible to establish for sure whether or not a widened spread is fundamentally justified”. Nevertheless, Nagel did not entirely rule out an anti-fragmentation instrument but said that this “can be justified only in exceptional circumstances and under narrowly-defined conditions.” …

US markets SEEM calm but they were anything but. Moving along, Barclays weekly view fresh off a very bad terrible no good H1, Q2:

Half empty Fears of recession are increasing, after the worst first half for stocks and bonds in decades

This is all then CONFIRMED as per originator of these longer-term visuals of returns.

Okie dokie — spoken like a true BOND shop? Moving along TO stonks and everyone’s favorite equity bear — Mike Wilson / MS:

The Moment of Truth, or Denial? With interest rates and equity risk premiums starting to reflect the growth slowdown more accurately, the direction of stocks from here should be mostly about earnings. 2Q results should shed some light on the outcome. Today, we look at where the risk is most/least significant.

Rates and ERP starting to reflect growth slowdown...

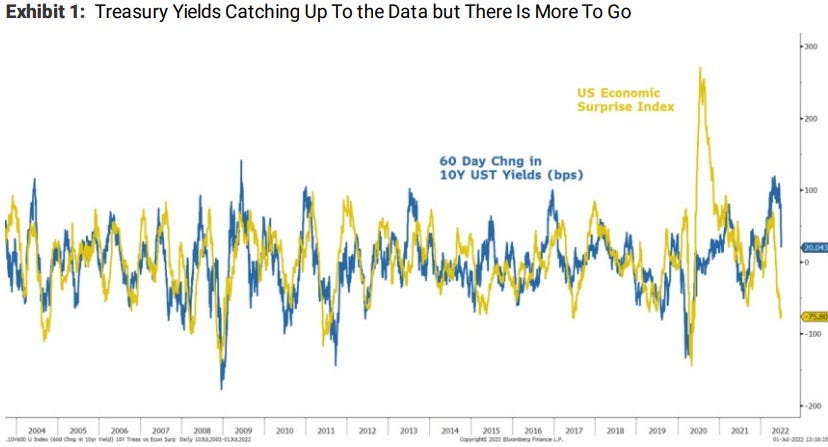

…Fast forward one week, and it looks like the answer is somewhere in between…meaning the equity market may not yet be sure what to make of the fall in rates. First, rates fell another 20 bps last week after having falling 40bps the prior 2 weeks, leaving 10-year US Treasury yields down 60 bps from their recent high in Mid June. However, as noted last week, yields are still lagging the recent negative data surprises which continued to come in worse than expected last week. In other words, the risk of growth slowing more than expected has only increased.

S&P 500 and Nasdaq 100 forward earnings estimates are both 20%+ above the post-GFC trend... On that score, we developed an industry level earnings risk heat map to assess risk across a number of relevant measures... Given the increasing risk to growth, the market is rewarding earnings stability...

From the CHARTS department — where, you know, everyone likes updated TOLD YA SO (?)

We laid it out 2 weeks ago in our June mid-month conference call.

It was time to buy bonds.

And I think this simple chart really helps illustrate why.

We're looking at the 10yr Breakevens peaking months ago, along with our Equally-weighted Commodities Index also peaking around the same time.

All of this while Rates made one more new high:

I HATE I TOLD YA SO … I prefer the pragmatic approach of the likes you’ll find the other day (HERE) where shorts were NEUTRALISED and levels remain the focus.

Then there’s THIS from the charts department — stocks v bonds (via John Authers latest)

… The ebb and flow of belief in a recession shows up clearly in the relative performance of stocks and bonds this year (proxied, as I usually do, by the SPY and TLT exchange-traded funds that track the S&P 500 and Bloomberg’s index of long-dated Treasuries). This has been a historically awful year for bonds; yet on July 1, as Wall Street prepared for Independence Day, bonds at one point had outperformed stocks for the year:

The chart attests to the volatility of sentiment over inflation, and over the likely effect on the economy. After the invasion of Ukraine, stocks dipped badly relative to bonds as a recession seemed more likely. Stocks then enjoyed strong outperformance as the inflation figures worsened; and now, with worrying numbers on growth, stocks have fallen back again. Inflation fears are receding, but only because of confidence that the economic slowdown will be so drastic that it will extinguish pricing pressure…

All told, looks like H2 set to be more of the same … visually, via Investing.com

… THAT is all for now, as money managers are just now tending to results of Q2, H1 preparing reports to present … And as the countdown TO the next quarterly missive by Lacy Hunt has begun.

For somewhat MORE — Factory Orders today, FOMC mins tomorrow and NFP Friday but again, for now, I’m off to the day job…

Loved the insight !