… US News: When your hull gets holed by inflation BBG Imports drop at California ports as the LA-Long Beach queue of vessels waiting to unload surpasses 100 WSJ Real rates: Covid-19 fuels best-ever commercial real estate sales last year WSJ The auto loan business has become a bright spot for the banks WSJ

Treasuries are a hair lower and the curve a hair flatter this morning ahead of today's Fed and BOC events. EU/UK and US share prices are notably higher in the early hours- lending a 'risk-on' patina to the proceedings this morning. DXY is modestly higher (+0.15%) while front WTI futures are too (+0.6%). Asian stocks were mixed, EU and UK share markets are all smartly higher (SX5E +2.35%, FTSE 100 +1.75%) while ES futures are showing +1.55% here at 6:55am. Our overnight US rates flows saw a muted Asian session with some real$ buying in the long-end and fast$ selling in intermediates about the only flow of note. Indeed, I had to rub eyes over the overnight Treasury volume stats this morning (~0.30% of ave across the curve)- a low reading usually reserved for late Decembers.

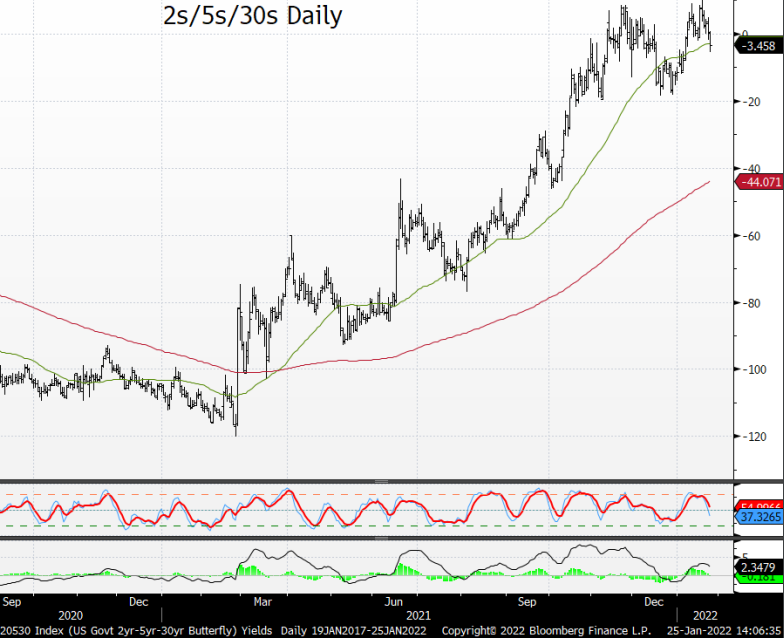

… Next up is a picture I stumbled over in Haver yesterday showing UST net issuance (gross -redemptions). It's updated through January and what stands out obviously is January's negative net issuance print- given how rare it is and before accounting for Fed purchases in this time series.

While grazing in that Haver tab I also found this next attachment showing how the WAM of outstanding marketable Treasury debt is now at the highest level (72mos) this century...

For somewhat more of the news you can use, here are IGMs Press Picks for today (26th Jan) to help weed thru the noise — most of which can be found over here at Finviz.

Treasuries were under modest pressure overnight with a relatively parallel shift higher in rates. Overnight volumes were modest with cash trading at just 37% of the 10-day moving-average. 5s were the most active issue, taking a 33% marketshare with 10s at 27%. 2s and 3s managed 22%, with each managing 11%. 7s took 13%, 20s 1%, and 30s 5%.

Today, a group of people with journalism degrees will seek to interpret the words of someone with a law degree about subjects that really only interest people with economics degrees. In other words, it is Federal Reserve decision day.

The Fed does not want to force growth below trend (growth is slowing anyway). The Fed does not want to force inflation lower (inflation will drop anyway). There is little the Fed can do to influence the price of a 2001 Honda Civic. The Fed might want to create conditions that give it political credit when inflation does slow.

The Fed wants to stabilize the economy and inflation when the extraordinary demand shock of the post-pandemic world reverts to normality. There is a big difference between the policy path and the economic/market outcome of a “Volcker shock” squeezing inflation out of the economy, versus a stabilization at normal.

The EU and the US are close to coordinating Russian sanctions. The Italians are still trying to elect a president. British politics are still a mix of the “Great British Bakeoff” and “Dirty Dancing”. Facebook’s Libra (or Diem) is reportedly selling assets—presumably marking the end of whatever that was. It is a timely reminder that technological complexity is not always economically useful.

For somewhat MORE on decision day and with somewhat more context in / around CLEANER POSITIONS ahead of the Fed, Bloomberg,

Bond bears have been lightening up on their Treasuries shorts ahead of today's Federal Reserve meeting. Whether spooked by the risk-off shift in stock markets or just profit taking after the recent surge in yields, the move suggests a degree of caution that hawkish expectations may have gone a step too far. A gauge of short Treasuries positions by JPMorgan clients has retreated while net speculative bearish bets on five-year futures -- particularly sensitive to Fed policy -- have been reduced, according to the latest data from the Commodity Futures Trading Commission. Swaps traders too have cooled their hawkish ardor a tad. They are still pricing in just under a 27 basis point move in March -- so slightly more than one hike -- but it was 28 basis points last week. Any comments from officials that suggests a faster-than-expected balance sheet reduction would open up the possibility of a less aggressive series of rate hikes.

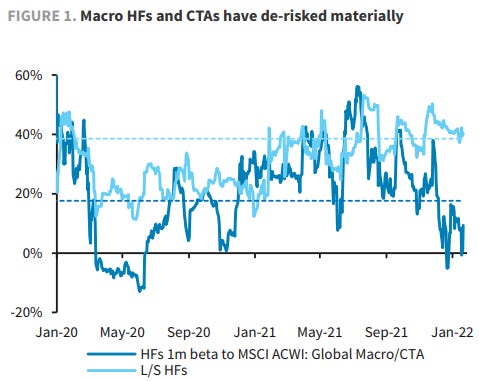

Speaking of CLEANER POSITIONS, even stock jockeys are gettin’ into the game. Barclays on STOCKS,

Positioning is cleaner post HF/CTA selling. MFs and Retail remain very overweight equities, though, so more de-risking is possible if growth/earnings fundamentals worsen, and more pain may be needed before Fed put kicks in. Investors should act with care, but be opportunistic. We find it premature to position for recession.

For MORE ahead of the Fed, and back TO BONDS, this from The Terminal via ZH,

This month’s bond rout is overdone. Wednesday’s Federal Reserve meeting may offer more carrots than sticks for debt investors.

… Keep in mind that the Fed’s plan to rapidly shrink its balance sheet should help deliver a steeper yield curve, in contrast to the flattening implied by commentators including JPMorgan Chase & Co.’s Jamie Dimon, who see the risk of more than four rate hikes this year.

Dimon has been wrong-footed on rates before -- including a 2018 warning that 10-year Treasury yields would hit 5% -- yet traders are falling over each other to catch the bandwagon. It’s easy to momentum-chase rate shorts, and profitable for a time, whereas betting on balance-sheet reductions is a tougher game.

Also keep in mind that forecasts and the bond market itself show that inflation should cool, either because the impact of supply shocks fade as the coronavirus shifts from pandemic to endemic, or the first one or two hikes from the Fed’s zero bound hit the real world harder than traders envisage.

On top of this, there’s the dynamic whereby the more aggressive the market gets with pricing in steep hikes, the less aggressive the Fed needs to be to get financial conditions back to normal.

So even if the broad outlook for bonds remains bearish for the next few quarters, many traders could find themselves unhappily ahead of the Fed this week.

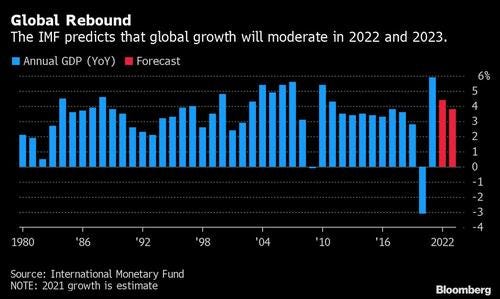

… Finally — least important for last — the IMFs LATEST World Economic Outlook, Rising Caseloads, A Disrupted Recover, and Higher Inflation can best be viewed/summarized by ZeroHedge

IMF Slashes Global GDP Growth To 4.4% In 2022, Warns On Aggressive Fed Tightening

… The U.S. saw its forecast cut on the imploding outlook for President Joe Biden’s spending agenda and China, the second-biggest, on challenges in real estate. Some more details:

The fund slashed its forecast for growth in the U.S. by 1.2 percentage points to 4%. The revision reflects removal of assumptions for a positive impact from Biden’s Build Back Better social-spending plan, which died in Congress; earlier withdrawal of Federal Reserve support; and continued supply-chain bottlenecks

The IMF trimmed China’s growth forecast by 0.8 point to 4.8%, citing disruptions caused by the pandemic, the nation’s zero-tolerance policy for Covid-19 and disruption in the housing sector.

The IMF cut its growth forecasts for Brazil and Mexico by 1.2 percentage points to 0.3% and 2.8%, respectively, with the fight against inflation already prompting tighter monetary policy that will weigh on domestic demand

India will see the fastest growth among major economies at 9% from 8.5%, due to credit-growth improvements

Looking even forward, which is a silly exercise as nobody can anticipate what happens between now and year-end 2023, IMF sees more slowdown, with global growth dropping to 3.8%, which however was a 0.2% increase from its previous forecast, but the cumulative expansion for the two years will still be 0.3% less than previously forecast.

According to the IMF, the world economy expanded 5.9% last year the most in four decades of detailed data. That followed a 3.1% contraction in 2020 that was the worst peacetime decline in broader figures since the Great Depression.

“The last two years reaffirm that this crisis and the ongoing recovery is like no other,” Gita Gopinath, who became the fund’s No. 2 official this month after three years as its chief economist, wrote in a blog accompanying the report.

“Policy makers must vigilantly monitor a broad swath of incoming economic data, prepare for contingencies, and be ready to communicate and execute policy changes at short notice,” Gopinath said. “In parallel, bold, and effective international cooperation should ensure that this is the year the world escapes the grip of the pandemic.”

… Perhaps the most interesting comment came from Gopinath who said that any miscommunication fof the Fed policy changes may provoke flight to safety and trigger capital outflow from Emerging Markets.

How will less accommodative monetary policy in the United States affect global financial conditions? With inflation on the rise and still large pent-up demand in the system in part due to the pandemic recovery program, US monetary policy will have to tighten. But how far and fast is not yet clear. The WEO forecast is conditioned on an end to asset purchases in March 2022 and three rate increases in both 2022 and 2023—consistent with what will be needed to bring inflation back down to the 2 percent medium-term goal. But there are upside risks. Inflation could turn out higher than expected (if, for instance, supply disruptions persist and wage pressures feed into inflation). A different policy stance will be required if circumstances change. Communicating such changes will be a delicate task and risks prompting strong market reactions that could, in turn, result in tighter financial market conditions. Markets’ reactions to (actual or perceived) changes in Federal Reserve policies will govern how less-accommodative policy in the United States spills over to other countries, particularly emerging markets and frontier economies. Any miscommunication or misunderstanding of such changes may provoke a flight to safety, raising spreads for riskier borrowers. This may put undue pressure on emerging market currencies, firms, and fiscal positions

Is Jamie Dimon still sticking with "six or seven" rate hikes?

Only time will tell. Anyways, that’s all for now. Off to the day job…