… HEREis what another shop says be behind the price action overnight…

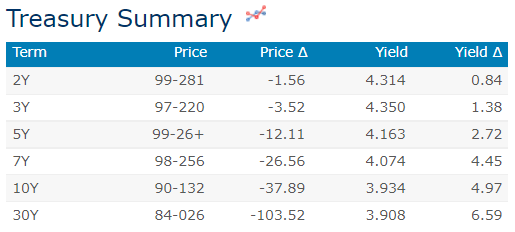

… WHILE YOU SLEPT Treasuries are mostly lower with the curve pivoting steeper off a little-changed 2-year yield after heavy sell-offs in the UK and German long-ends yesterday (see links above). DXY is UNCHD while front WTI futures are lower (-2.3%). Asian stocks were mostly lower (NKY -2.6%, Taiwan's TAIEX -4.35% and Korea's KOSDAQ -4.15%), EU and Uk share markets are all in the red while ES futures are showing -0.6% here at 7:10am. Our overnight US rates flows saw better selling during Asian hours (fast$ and real$) with a series of FV and TY blocks accelerating the move. We also saw better paying in swaps during a largely one-way (selling) session. During London's AM hours our flow flipped to buying (mostly front-end), following modest rebounds in the UK and German markets. Overnight Treasury volume was ~140% of average all across the curve.

… This monthly chart of Treasury 10yrs shows the 2009 and 2010 peaks in 10's near 4%, which is why we've expected the 4.00% level to act as a solid support for 10's- being the first-revisit to those twice-rejected yield highs since then. Do note in the lower panel that long-term momentum still guides bearishly even though momentum levels remain in deeply 'oversold' territory. It's perhaps no surprise then that some asset mangers are beginning to warm-up to bonds for the first time in years: FT

… and for some MORE of the news you can use » IGMs Press Picks for today (11 Oct) to help weed thru the noise (some of which can be found over here at Finviz).

STILL waiting for Dr. Lacy Hunt’s latest quarterly and while we wait, a few other items inboxed which may be somewhat funTERtaining

Goldilocks: More Progress, More Risks The September jobs report was firm, with a 263k increase in nonfarm payrolls and a drop in the unemployment rate to 3.5%. But overall, the recent labor market news supports our forecast of gradual adjustment. Job growth has continued to decelerate across the key indicators, i.e. the payroll survey, the revamped ADP private jobs measure, and both the headline and payroll-adjusted household survey (the latter two calculated as 6-month averages to smooth out the much greater month-to-month noise). The drop in the unemployment rate merely reversed the surprising increase in August. And the wage news has improved a bit, not only because of the slowdown in average hourly earnings growth to 0.3% in the last two months but also because of the decline in the monthly employer-side wage surveys; the Q3 employment cost index released on October 28 should provide more clarity.

MSs latest from Andrew Sheets asking and attempting to answer,

Should You FX Hedge Your Assets? We examine how FX-hedging assets can boost risk/reward for USD-based investors through the cycle, and what this means for asset allocation. We revisit our FX-hedged yield analysis and think current opportunities lie in Japanese equities and EM equities for a USD-based investor.

To hedge or not to hedge? History says if you're a USD-based investor, 'hedge' for (most) assets: Hedging non-USD assets has produced superior returns. USD-based investors interested in through-the-cycle performance often benefit from hedging currency, due to higher returns, lower vols and better Sharpes. Because the advantages of hedging are driven mostly by vol reduction rather than 'carry', this is an 'all weather' theme. Fixed income benefits more than equities from FX hedging.

Foreign assets FX hedged can serve as portfolio diversifiers for USD-based investors: Historically, the optimal portfolio for a USD-based investor on an unhedged basis is dominated by USD assets. But since hedged foreign assets can lead to lower/negative correlations, lowering portfolio volatility, they help to push the efficient frontier upwards and outwards.

Revisiting FX-hedged yields: For a USD-based investor, Japan equities now offer the highest FX-hedged carry of 7.7% within DM, while vol-adjusted carry for EM equities is higher versus history across the board. For an EUR- or JPY-based investor, FX-hedged USD-denominated assets no longer look attractive compared to local assets, reversing the trend of the last few years.

Longer term, shifts in relative attractiveness of FX-hedged assets should benefit EUR: While stagflationary concerns in Europe keep us bearish on EUR in the near term, the longer-term EUR-positive element of ECB normalisation and higher local yields should not be ignored going into 2023. The unusually large gap between local yields and comparable FX-hedged yields abroad is likely to turn increasingly EUR-positive.

Treasuries volatility is becoming a sorer and sorer point as the Federal Reserve’s most-aggressive tightening campaign in at least a generation roils the world’s deepest bond market. With the Fed running down its balance sheet as fast as it dares, other traditional buyers are also fleeing.

US commercial banks are absent partly because the US central bank is draining reserves out of the financial system. Foreign central banks are running down reserves (much of them held as Treasuries) to lessen the impact of Fed policy on their currencies. Then there’s Japan’s deep-pocketed pensions and life insurers who’ve traditionally favored the US as a safe and stable source of long-dated yield. The divergence between the ultra-easy Bank of Japan’s settings and the uber-hawkish Fed means they face deeply negative yields on a hedged basis. The upshot is that the only buyers left are far more price sensitive than those that are leaving, so that helps exacerbate patches of illiquidity and some of the bursts higher in yields.

USTs may not look attractive for those overseas BUT they are looking like a relative GOOD alternative (sorry, TINA) to, well, a lot of other yields out there.

WHY on earth would ANYONE wanna buy a US Treasury, putting the FIXED in fixed income? Rex Nutting of MarketWatch,

… If the Fed still wants a soft landing, it needs to heed these indicators. Unfortunately, the Fed, by looking into the rearview mirror, is not paying attention to the road ahead.

For instance, growth in the money supply has long been seen as a source of inflationary pressures. Larry Summers, Jason Furman and others who correctly predicted the 2021-22 inflationary cycle saw that large increases in stimulus (in the form of direct payments to households financed by the Fed’s quantitative easing) would lead to strong effective demand in an environment of restricted supply—a recipe for high inflation…

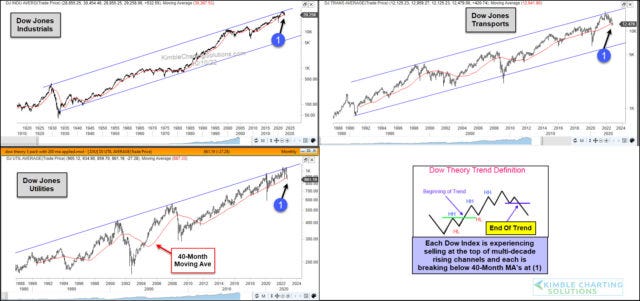

Hmm … ok then. Back TO markets, the forward looking pricing / discounting of cash flows mechanism … here’s one for the chartologists out there … Kimble,

… That’s right, it could get worse. Today’s chart 3-pack highlights 3 Dow indices that are decisively bearish… andattempting to trigger a Dow Theory sell signal.

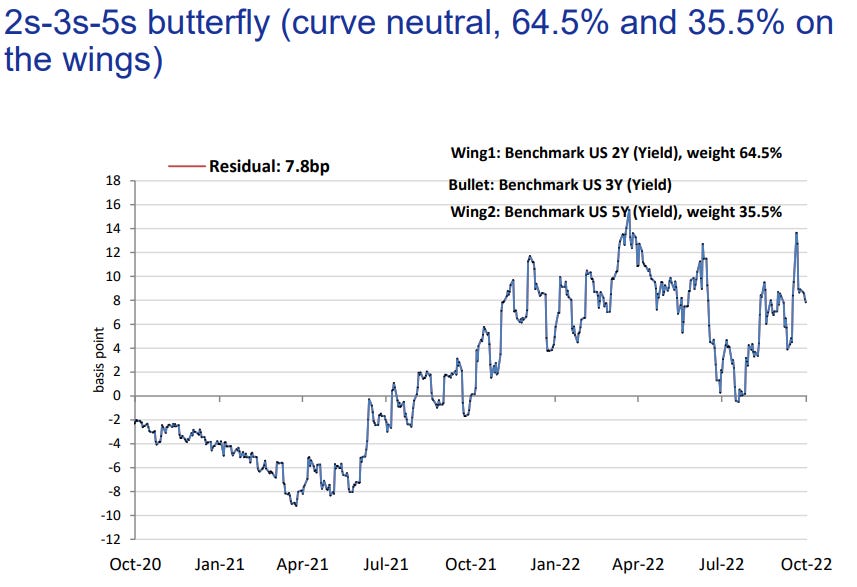

With all this in mind, gotta ask if you’ve got 3s? Auction later on this afternoon … here’s a couple visuals of them on the curve (via DB) to consider,