Good morning / afternoon / evening (please choose which ever one which best describes when ever you are stumbling across this shorter than short note) …

Before traders on the east coast hit the ground running Friday on into week and month’s end, BBG John Authers’,

When banks have a problem, we all have a problem. That was a central learning from the implosion of 2008, and last month’s sharp market reversals in the wake of the failures of several sizeable regional banks showed that it held good. Expectations for the Federal Reserve turned on a dime. For a succession of weekends, survivors of 2008 suffered flashbacks as they awaited news of the latest institution in trouble, be it Silicon Valley Bank, Signature Bank or Credit Suisse Group AG.

Another such week lies ahead. Confidence in First Republic Bank appears to be shot. Somehow soon, it will be put out of its misery, whether through a sale or some kind of formal government closure. The banking problem remains unfixed. And yet, this coming weekend is inspiring relatively little tension. Why not? Let’s count the ways…

… The possibility of a repetition of 1929 or 2008 indeed looks slim, and the stakes for First Republic are not as high as they were in many of the tense meetings in the fall of 15 years ago. But the possibility that the difficulties for the banks continue to put a lead weight on the economy is very real. With rates and the yield curve where they are at present, there’s a real chance of a serious economic slowdown. And that in turn is why so many are prepared to bet that the Fed won’t keep rates where they are for much longer, and that encourages them to keep paying for stocks.

FRC bids anyone? JPM, PNC? US Bank? Perhaps the only folks NOT asked to bid are you and I?

BMO outta 10yy longs at tgt and getting in to 5s30s steepener DB connects dots from BEIGE book thru to SLOOS NWM updated fed call TO 25bps hike (?) SocGEN - NOT SO FAST … “…data dependence implies greater vigilance and more volatility in global rates. BUCKLE UP!”

AND more… A few other items from the intertubes which may be of interest into a crucial week ahead with FOMC and NFP … First up on Treasury market POSITIONS,

HEDGOPIA NOTES … again … still … the largest net SHORT 10y since 2018?

POSITIONS — shortest since September of 2018 — or shortest EVER (depending on how you economically workbench the data) will remain an important factor when attempting to ‘analyze’ price action…

Stagflation or Simply Sticky Inflation? While the bond market’s rebound this year shows increasing confidence a global wave of rate hikes will tame inflation, nagging concerns remain.

The world’s biggest money managers are becoming more deeply divided over whether cost pressures will fade away. Allianz Global Investors reckons central banks will win the inflation battle; BlackRock Inc. is among those skeptical of rate-cut bets. Former Treasury Secretary Lawrence Summers weighed in, saying a “meaningful” economic downturn is probably needed to tame inflation.

In another sign of sub-surface cracks in the bond market, hedge funds set the biggest short on record against benchmark 10-year futures. Funds also extended overall bearish bets for a fifth-straight week. That stance contrasts with Wall Street veteran Bob Michele, who anticipates a flattening of the yield curve to 3% for securities maturing in two through 30 years.

The Federal Reserve is still expected to raise its benchmark rate by a quarter-point next week, while the European Central Bank is talking about another half-point increase — and then maybe some more. Goldman Sachs sees the Bank of England also hiking rates, to keep it close to the Fed.

The conundrum this poses for investors got sharper when the latest first-quarter GDP update showed the US in the “worst of both worlds.” Growth slowed to a 1.1% annualized pace while inflation accelerated. Traders promptly boosted bets on stickier inflation.

The big fear is a bout of stagflation could be on the way. In response, some funds, including Australian pension managers, are turning to commodities for protection…

POSITIONS can help predict flows.

“Higher prices bring out buyers - Lower prices bring out sellers - Size opens eyes… When they’re yelling you should be selling, crying you should be buying.” -Larry McCarthy

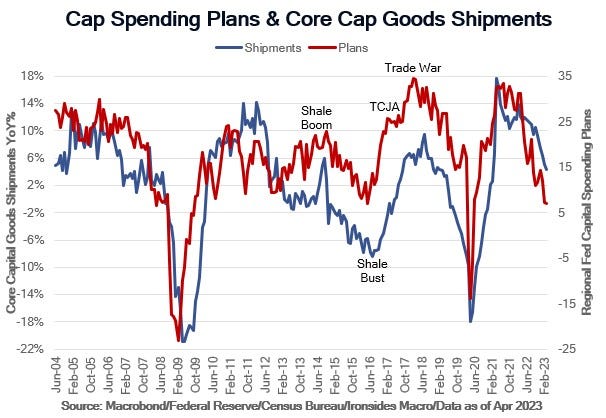

Economically speaking, Barry Knapp of Ironsides MAC, a snippet / VISUAL,

… Incoming data this week was mixed and probably left the Fed on track for another misguided rate hike. GDP was weaker than expected, however the miss was primarily attributable to a sharp drop in inventory investment to the long-term trendline. While core domestic demand was robust, consumption was boosted by an increase in auto supply. There was ample evidence from earnings reports that consumption is slowing. Weak equipment and software capital investment dampened the outlook and highlights our view that overly restrictive monetary policy is impairing supply. The effect of policy on supply was evident in strong new home sales, weak pending home sales of existing homes and a surprising increase in the Case Shiller 20-City Composite House Price Index. The March personal consumption deflator report was favorable, our calculation of core services less rent of shelter was 2.9%, softer than February’s 3.1% reading. The employment cost index was hotter than expected for the quarter, but on an annualized basis it eased marginally and private sector wage growth of 5.07% is right on top of the nonsupervisory average hourly earnings series, thereby making the quarterly increase in the Atlanta Fed Wage Tracker an outlier.

Figure 1: Capital spending plans are as low as they were following the shale oil bust when energy was 36% of S&P 500 capex.

Simmering in the background of the earnings and macro data barrage was First Republic Bank’s Q1 earnings report that made it clear their assets and liabilities are upside down, underscoring that the risk of a nonlinear tightening of credit is far from mitigated. The FOMC appears determined to increase the policy rate another 25 basis points. New-Keynesian demand models attempting to quantify the impact of tighter credit are dependent on unstable relationships. Forecasts of the impact of reduced credit on residential investment, labor income, consumption and prices, based on a couple of post-war credit contractions, are highly uncertain. On the other hand, we know with certainty that the $1.75 trillion of banking system USTs and $900 billion of mortgage-backed securities purchases in ‘20 and ‘21, financed at a 4.75-5% policy rate, is unsustainable for all but the Fed. In other words, the equilibrium policy rate for the household and nonfinancial corporate sectors are unknowable, but for the banking system the current policy rate is overly restrictive. While 25bp might not seem like much to the FRB/US model, a 5% policy for longer will accelerate the bank deposit beta, leading to increasing unstable and expensive liabilities, forcing more banks to shrink their assets…

Rest is behind a paywall and so, food for thought…

… While the Federal Open Market Committee (FOMC) is still expected to implement a 25 basis point (0.25%) hike at next week’s May meeting, the situation shown in the chart below, where the fed funds rate is above both headline and core PCE, adds credence to the view that May’s likely hike could be the final flourish at the end of the Fed’s current rate hiking cycle. The widening of the difference between the fed funds rate and inflation will be a key topic for the remainder of 2023 as we access the potential for, and timing of, rate cuts.

Summary Today’s PCE data is largely what was expected, and the while inflation trend grinds on, we believe we will see a continued cooling throughout 2023 with inflation likely to be under 4% by the end of the year. There is still uncertainty out there however, and the U.S. economy is likely at an inflection point with consumer spending softening in recent months, as consumers have become more pessimistic about the future. The latest consumer confidence report corroborates that thesis. This weakening consumer data, combined with what we now know about PCE, puts the Fed in a position to potentially suspend the current rate hiking cycle after one more rate hike next week. The improved inflation dynamics, a slowdown in business activity and signs of a softer job market will likely force the Fed to consider ending its current rate hiking campaign later this year.

Dunno. Compelling or not? YOU decide…back TO banking for a moment,

AND for any / all (still)interested in trying to plan your trades and trade your plans in / around FUNduhMENTALs, here are a couple economic calendars and LINKS I used when I was closer to and IN ‘the game’.

First, this from the best in the strategy biz is a LINKthru TO this calendar,