Good morning / afternoon / evening - please choose whichever one which best describes when ever it may be that YOU are stumbling across this weekends note…

Which, frankly, I did not spend too much time on (as noted yest) and so I’ll be real quick here tonight.

First, a visual …

We’re bumping up against October CHEAPS and momentum remains overSOLD (no signs of a rolling over, actually getting MORE oversold) and yet there’s a comfort with a soft landing narrative. There seems to be a very dismissive attitude towards the FED and this as the dots plot set to thicken — expecting another hike this year AND fewer CUTS next — combine for a very sanguine view ‘out there’ and I guess I must be missing something. It’s not as if prices of gas at the pumps have shown ANY signs of ease and the worlds all of a sudden, a much safer place…

NEXT UP lets deal with a couple / few things from yesterday…

ZH: US Manufacturing Production Lower YoY For 6th Straight Month, As Automaker Output Plunges ZH: UMich Inflation Expectations Plunged In Early September Survey (perfect … further confusing matters and markets…)

With CPI and PPI both printing hotter than expected, import and exports prices rising more than expected, and the market's implied inflation expectation also soaring, this morning's much-watched UMich inflation expectations index should be a little moot.

Nevertheless, the survey respondents from the UMich survey saw inflation expectations plunging both short- and medium-term...

… Survey Director Joanne Hsu notes that "so far, few consumers mentioned the potential federal government shutdown, but if the shutdown comes to bear, consumer views on the economy will likely slide, as was the case just a few months ago when the debt ceiling neared a breach."

… This all culminated with this

ZH: Crude Pumped To 10-Mth High As Stagflation-Scares Slam Stocks & Bonds

… Ok I’ll move on AND right TO the reason many / most are here … some UPDATED WEEKLY NARRATIVES where I’d note a couple / few things which stood out to ME this weekend …

… We added to our long 10s position in the selloff to 4.32%, and remain comfortable with a longer term bias to see rates move lower from current levels…

BloombergBNP - Where to see auto strike impact in data and Fed policy

The United Auto Workers (UAW) strike will likely ripple through jobless claims, production statistics, and ultimately payroll growth, assuming a deal is not reached soon. We think Fed officials will look through these effects, which would reverse over time. Events could nevertheless reinforce a wait-and-see approach at the Fed’s rate decision on 1 November…

DB - Individual demand for 2yr Treasuries is back (think NONCOMPS) JEFF - FOMC Preview: No Rate Change Expected... Potential Dot Headache MS - remain LONG 5s, 30y TIPS and … (if I said this you’d laugh …)

…This Time IS Different for Real Yields …

SocGen FI Weekly, “On hold” (another revision worth note…)

… 10yT yield to end the year at 3.75% We revised our Treasury forecasts and now expect only a modest decline to 3.75% by year-end. Yields should continue to decline in 2024, as we anticipate a recession by mid-year (see GEO for details). With a later recession (than what we had previously anticipated, i.e. early 2024) and ‘high-for-longer’ policy rates, we now expect the 10yT yield to bottom at 3.25% by mid-2024 but start to rise again in 2H of next year when the economy starts to recover after a mild recession.

… Moving along and away FROM highly sought after (?)and often paywalled Global Wall Street narratives TO a few other things widely available and maybe as useful from the WWW

The 10 largest companies in the S&P500 make up 34% of the index, and these 10 mega-cap companies have an average P/E ratio of 50, see chart below.

ZH: "Getting Cold Feet": Rising Home Contract Cancellations Hits 10-Month High As Affordability Crisis Worsens (this one here strikes me as important as the world continues to wait for concrete signals RATES MATTER and that nothing happens without consequence — allowing for or validating rate CUTS (?) — largely given data holding up … perhaps sources of data we’re currently analyzing needs to shape shift a bit? thankfully ZH has link thru to report for further investigation … )

A new Redfin report Friday revealed the latest rumblings of a worsening housing affordability crisis. It showed the number of residential real estate deals that fell through in August surged to the highest level in a year. This is due to a combination of a 30-year fixed mortgage rate above 7% and rising home prices that has caused a 'homebuyer stickier shock.'

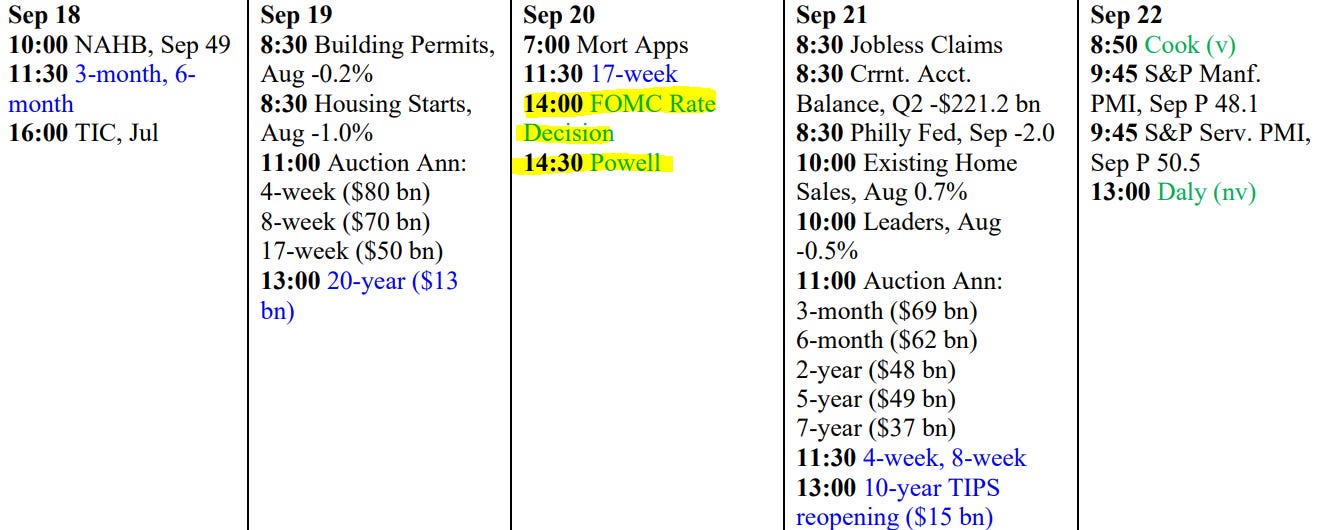

… AND for any / all (still)interested in trying to plan your trades and trade your plans in / around FUNduhMENTALs, here are a couple economic calendars and LINKS I used when I was closer to and IN ‘the game’.

First, this from the best in the strategy biz is a LINKthru TO this calendar,

Good work !!!

The Dot Plot appears to be the most significant piece of information that

will come from this FED meeting......

The Supply of Treasuries keeping coming on STRONG....just add them up on your Calendar.

Hard to see the 10 year Bond Rate going below 4%, any time soon. IMO