Good morning / afternoon / evening - please choose whichever one which best describes when ever it may be that YOU are stumbling across this weekends note…

Not sure best way to begin SO I’ll address the elephant in the room — JPOW at JHOLE first — with some clickable links for your review … Generally speaking, as I would interpret it … he’s said absolutely NOTHING we shouldn’t already know and shared absolutely NOTHING new …

CalculatedRISK: Fed Chair Powell: Inflation: Progress and the Path Ahead ING: Powell signals Fed to tread carefully, but that rates will stay high Wells Fargo: Powell at Jackson Hole: Fed Committed to 2% Inflation but Agility Required

… We believe there is a high bar for the FOMC to raise rates at its September 20 meeting. We forecast the Committee will remain on hold at subsequent meetings, but we acknowledge the risk of further tightening if economic growth does not slow to a below-trend rate and/or inflation remains unacceptably high.

WolfSt: Powell Smacks Down Calls to Raise 2% Inflation Target: “2% Is and Will Remain our Inflation Target” WSJ: Powell Says Fed Will ‘Proceed Carefully’ on Any Further Rate Rises ZH: "A Long Way To Go" - Fed Chair Powell Delivers Hawkish J-Hole Speech

Okie dokie … Ok I’ll move on AND right TO the reason many / most are here … some UPDATED weekly NARRATIVES where I’d note a couple / few things which stood out to ME this weekend …

BMO- Powell: 2% will Remain Inflation Target, r* Difficult to Measure Goldilocks- Powell Revives Plan to “Proceed Carefully” in Jackson Hole Speech Goldilocks WEEKLY (on who’s buyin’ bonds)

… Diminishing foreign support for USTs. Although foreign purchases have been a source of support for USTs over the past two years, much of this buying has come from the non-official sector (Exhibit 2). Foreign official sector holdings have been stable since the first half of the last decade, with periodic buying largely offsetting sales from prior years…

September is a bad month for rates and gold, good for the USD against the JPY and EUR, as well as BRL and TRY. It’s also a good month for most credit markets.

AND more. MUCH, much more…all told, you’ll find it’s one small part JHOLE review, another small part NFP precap and victory lap and a large part, ‘outta office, enjoying the Hamptons Hedge, will return sometime AFTER Labor Day’ … (in other words, there’s really not MUCH there, THEREthis weekend…)

Moving along and away FROM highly sought after and often paywalled and Global Wall Street narratives TO a few other things widely available and maybe as useful from the WWW

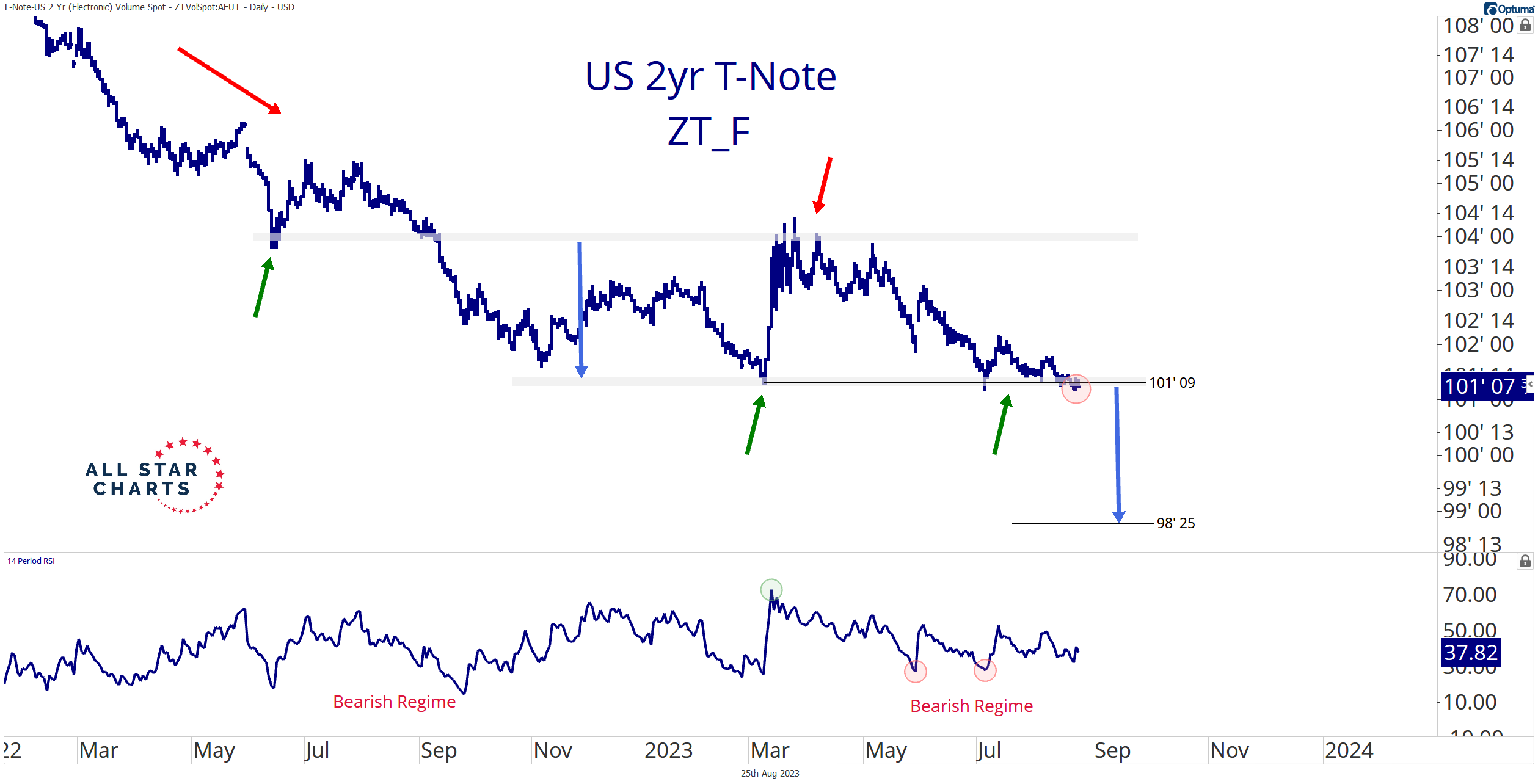

AllStarCHARTS- 2-year T-Note Flashes “Sell” (if at first, second or third, you don’t succeed, well, nevermind…? it’s precisely this kinda thinking that is REQUIRED before Mr. Market can / will reverse course … once weaker hands are rinsed OUT and precisely when NOBODY in their right minds would touch bonds … AND when Fed takes a somewhat LESS HAWKISH stance … the front end can / will stabilise but for now, … )

I thought it was time to bring these beaten-down assets back into the fold as

US treasuries printed fresh 6-month highs.

But I was wrong.

Fast forward to today, and the downtrend for bonds remains intact. And those false breakouts last spring have led to fresh breakdowns as we head into the fall.

The 10- and 30-year futures are flashing sell signals as they undercut their respective March pivot lows.

Now, the shorter end of the curve is doing the same.

Here’s the 2-year T-note completing a bearish continuation pattern:

The momentum profile alone reveals sellers control this market with two oversold readings since May. I imagine we’ll witness a third on a valid breakdown below 101’09.

That’s my level – the March pivot low.

The 2-year T-note is a short on a decisive close below the former low with a measured target at approximately 98’25.

You certainly don’t have to take this trade.

If shorting bonds fails to jibe with your mindset, just don’t take the trade.

But I don’t understand the urge to buy treasuries down here.

Whether we’re looking at the 30-, 10-, 5-, or 2-year bond, I can’t find a single chart I want to buy.

Plus, I’ve tried. Twice!

It didn’t work.

I’m sure buying bonds will eventually make sense.

But not yet…

Crescat Cap - VIOLENT REPRICING (interesting visual of bonds and NAZ for future reference and a reminder that tech stocks have, in past, been a VERY LONG DURATION instrument)

…Tech Stocks vs. 10-year Treasuries 10-year Treasury prices just broke down below the levels that triggered the bank runs earlier this year. Maintaining high earnings multiples for financial assets requires a low discount rate which is also known as the “cost of capital”. For stocks, there are three components to estimating this rate for purposes of a discounted cash flow valuation model. The risk-free rate, which is often assumed to be the 10-year Treasury yield, is just one of the building blocks. But Treasury yields alone are not the discount rate for risky assets. A risk premium to Treasuries needs to be applied. There are risk premiums for general equity market risk and for stock-specific risk. The recent increase in the risk-free rate alone should be driving valuations for popular tech stocks lower, as it did in 2022. This relationship can be seen in the chart below, but there has been a major speculative divergence in 2023, one that is destined to be reconciled in our view, potentially very soon.

HedgOPIAon POSITIONS (specs remain largely short 10s and bonds)

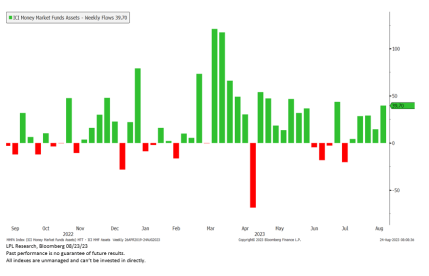

LPL - Cash Piling Up on the Sidelines (choosing to do nothing, sit in cash NOW it turns out becoming more popular … not only to do but to write about)

Key Takeaways:

Cash in money market funds continues to climb in record-high territory.

Rising interest rates supported by the Federal Reserve’s (Fed) higher-for-longer monetary policy and turmoil in the regional banking space earlier this year have underpinned steady inflows into the space.

While a Fed rate cut could create some headwinds for money market fund flows, don’t hold your breath for an immediate trend change.

High watermarks in money market assets have historically not been reached until the Fed significantly cuts interest rates. Of course, these periods also overlapped near the last three major bottoms in the S&P 500.

… Cash has consistently flowed into money market funds this year. As of August 16, money market funds have captured inflows during 24 of the last 33 weeks (year to date), including a current five-week inflow streak.

Follow the Money Attractive yields north of 5% have enticed investors to move cash from lower-yielding bank accounts to money market funds. Fund flows out of the banking space were further exacerbated by the turmoil in regional banks this spring—including the shuttering of three major regional banks. The chart below compares total money market assets to total deposit liabilities among commercial banks in the U.S.

Will Mortgage Rates hit 8%? Powell signals "Higher for Longer"

… Meanwhile, the cost of renting a standard apartment in America is $1,859/month. Indicating that it is 50% more expensive to buy a house, a financial reality that is going to keep many first-time homebuyers on the sidelines.

There are only two ways this can go: 1) Home Prices Down or 2) Inflation Up…

The risk reward on bonds is insane here if we make a double bottom here in $TLT. Not a trend fighter myself, but it looks tempting.

Finally, as summer is winding down and we’re all focused on seeing whatever it is we want to see from JPOWs JHOLE speech, another ‘official’ document worth a look …

FRBSF Working Paper: Passive Quantitative Easing: Bond Supply Effects through a Halt to Debt Issuance

Abstract This article presents empirical evidence of a supply-induced transmission channel to longterm interest rates caused by a halt to government debt issuance. This is conceptually equivalent to a central bank-operated asset purchase program, commonly known as quantitative easing (QE). However, as it involves neither asset purchases nor associated creation of central bank reserves, we refer to it as passive QE. For evidence, we analyze the response of Danish government bond risk premia to a temporary halt in government debt issuance announced by the Danish National Bank. The data suggest that declines in longterm yields during its enforcement reflected both reduced term premia, consistent with supply-induced portfolio balance effects, and increased safety premia, consistent with safe assets scarcity effects.

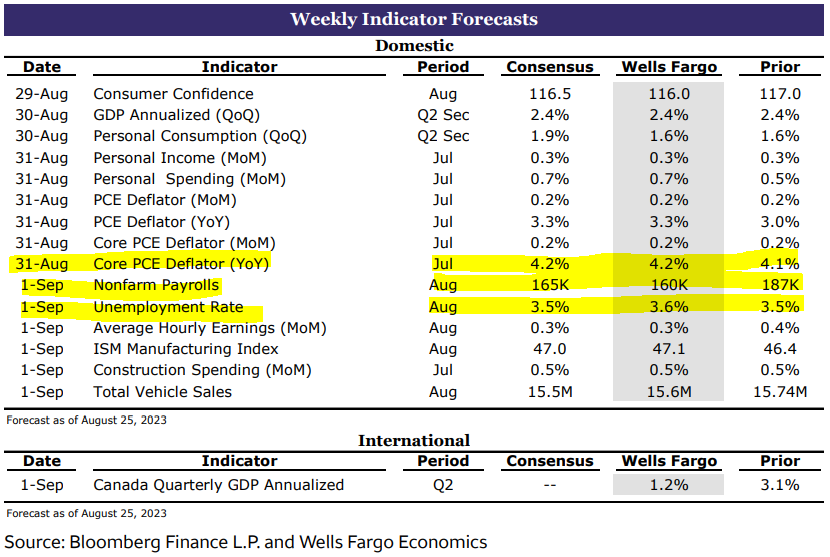

AND for any / all (still)interested in trying to plan your trades and trade your plans in / around FUNduhMENTALs, here are a couple economic calendars and LINKS I used when I was closer to and IN ‘the game’.

First, this from the best in the strategy biz is a LINKthru TO this calendar,

All in all, a good week here as Thing 3 freshman football team went TO Wall, NJ and emerged victorious followed by a DUB last with our local edition OF Friday Night Lights … Lots of football, food, fun and HOPEFULLY decent weather just ahead. GIANTS v jets later on today here hopefully as much / MORE good stuff for you all.

THAT is all for now. Enjoy whatever is left of YOUR weekend …

Raising little footballers nice! I'd be more excited about the upcoming season, but I'm a confused Raiders/Patriots fan nough' said....

The used car market's on fire out in Sacramento, lots of purchases Friday. Even dealers tell me it's CRAZY. I wonders if some are in a hurry to buy something before Student Loans payments restart, and/or DDB's favorite topic-the Covid employee retainer benefits go away. All-Star charts rock thanks!

Raising little footballers nice! I'd be more excited about the upcoming season, but I'm a confused Raiders/Patriots fan nough' said....

The used car market's on fire out in Sacramento, lots of purchases Friday. Even dealers tell me it's CRAZY. I wonders if some are in a hurry to buy something before Student Loans payments restart, and/or DDB's favorite topic-the Covid employee retainer benefits go away. All-Star charts rock thanks!

Great Summary !!!