Good morning / afternoon / evening (please choose whichever one which best describes when ever it may be that YOU are stumbling across this weekends note…

First a quick look back in the rear-view mirror...as the day/week/month and quarter comes TO a close AND the wait for HIMCOs latest quarterly begins …

ZH: Fed's Favorite Inflation Signal Remains 'Stuck' As Wage-Growth Re-Accelerates In May

… Even more focused, is the Fed's view on Services inflation ex-Shelter, and the PCE-equivalent shows that is very much stuck at high levels...

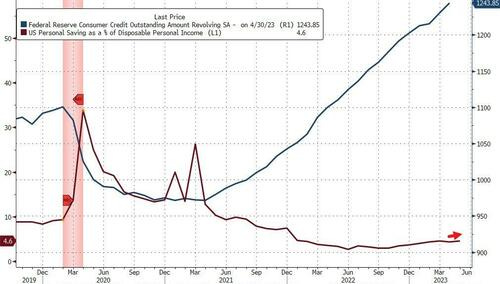

… Putting all that together, we see that the savings rate increased to 4.6% from 4.3%...

Source: Bloomberg

Is the consumer starting to pull back? Stalling spending combined with sticky core PCE - smells like teen-stagflation to us

OR perhaps you prefer it SPUN a bit differently,

CalculatedRisk: PCE Measure of Shelter Finally Slowing YoY

And hey, that isn’t ALL which could be seen ‘finally slowing’,

ZH: UMich Inflation Expectations Crash In June; Democrats Lead Sentiment Rebound

BMOentered longer-term and FUNduhMENTAL 2s10s steepener BNPs Sunday TEA notes ‘upside risks to US yields REMAINS relevant’ JPMs HALFTIME report — legendary annotated visual of stocks AND bonds

MSon BOND MKT SEASONALITY, “… FOUR REASONS WHY LONGS COULD WORK FROM MID-JULY”

And so with THESE NARRATIVES in mind, I’ll move from a few of the best in the business, TO a couple / few things from the intertubes for your dining and dancing pleasure …

… If we look at real GDP data, we can break the report into three buckets: Cyclical GDP, Real Final Sales, and Non-Cyclical GDP.

Cyclical GDP is the sum of residential fixed investment, durable goods consumption, and business equipment investment. Noncyclical GDP is the difference between Real Final Sales and Cyclical GDP.

The Cyclical Economy has been in contraction for four consecutive quarters, which is uncommon outside recessionary or pre-recessionary periods.

Non-Cyclical GDP is accelerating, but that is not abnormal in early recessionary periods, like 2008.

What’s important is the sequence or order. All downturns will start with the red line, Cyclical GDP, and then move to the blue line, Real Final Sales, and lastly, the black line, Non-Cyclical GDP…

Not a bad place to begin as the shot clock starts and we await latest from HIMCO.

As we wait for that AND we consider the performance of H1 as it may / may not relate TO risks which need to be taken in H2,

In fact, the S&P 500 was up 15.9% during the first half of 2023.

So how does this first half compare?

To answer that question, today’s chart presents the best first halves for the S&P 500 since 1950 (blue columns).

Conclusion…

This is the tenth best first half for the S&P 500 since 1950.

It is worth noting that a majority of first halves illustrated on today’s chart were followed by second halves (gray columns) that were somewhat less robust.

And moving along TO some thoughts on the front end,

Invesco Insights: What to keep in mind about high short-term rates

Key takeaways

Inverted yield curve

Investors are getting better yields from short-term bonds than from longer-term bonds.

Reinvestment risk

Attractive short-term yields come with the risk of having to reinvest at a lower rate later.

Reallocation option

Beginning to move money from T-bills to corporate bonds can minimize this risk.

… Yield on short-term bills are expected to be lower

With short-term rates the highest in decades, it’s tempting to keep a large allocation to cash equivalents like T-bills. However, that introduces reinvestment risk —the probability of not being able to reinvest this money at the same rate. In our opinion, the best way to minimize this risk is to begin to move from T-bills into more traditional bonds such as corporates. For instance, since 2008, the monthly return on corporates bonds has outperformed T-bills by 425 basis points on average (see chart below).4 Investors, of course, won’t be able to time the market perfectly when doing this. But it will, at least, minimize the risk of having to invest in 3-month T-bills at a lower rate when the yield curve returns to normal and short-term rates are lower than long-term rates.

Corporate bonds have outperformed short-term bills

Corporate BONDS > TBILLS … because, you know, they are apples to apples? Since on this topic, a JUNE update of distress from the FRBNY

Corporate bond market functioning remained close to historical norms over the month of June, with the end-of-month market-level CMDI around its historical median

Market functioning in both the high-yield and investment-grade sectors remained roughly flat over the course of the month.

Nothing to see here, I suppose. Might as well consider CORP BONDS risk essentially the very same as TBILLS then … ?

Lets just take a moment, though, and consider what IF — Dudley was right and 10yy were to move TO 4.5% … would there be any impact on corporates (or households) who rely on financing? Mortgage rates have so far, NOT impacted economy as one might have expected … YET.

Former New York Fed president and current Bloomberg Opinion columnist Bill Dudley made waves on Thursday with a big call: ten-year Treasury yields might be heading to 4.5%.

The entire column is well worth reading, but for newsletter purposes, here’s the meat of Dudley’s argument:

Suppose the Fed’s short-term interest-rate target, adjusted for inflation, averages about 1% over the next decade. Inflation averages 2.5%, and the bond risk premium is one percentage point. In sum, this suggests a 10-year Treasury note yield of 4.5%. And that’s a conservative estimate: Given historical neutral short-term rates, the recent persistence of inflation and the troubling US fiscal trajectory, all three elements could easily go higher.

For context, 10-year Treasury yields haven’t seen 4.5% since 2007. They’re currently hovering near 3.83%, well below this cycle’s high of 4.33% reached in October.

Dudley’s call stands outside the Wall Street consensus, with many money managers making the case that now is the time to start extending duration. Firmly on the other side of the the trade is Morgan Stanley’s Matthew Hornbach, who wrote in mid-June that he expects 10-year yields to end 2023 at 3.5% — a full percentage point below Dudley’s call.

As fate would have it, Hornbach joined Bloomberg Television hours after Dudley’s column published and walked through his forecast. It centers on the argument that federal fiscal support — once a wrench in the Fed’s inflation fight — will pullback this year, turning into a tailwind for the central bank’s campaign to stamp out price pressures.

“We do think inflation will decelerate more meaningfully than the Fed is expecting,” Hornbach, Morgan Stanley’s global head of macro strategy, said on Bloomberg Television.

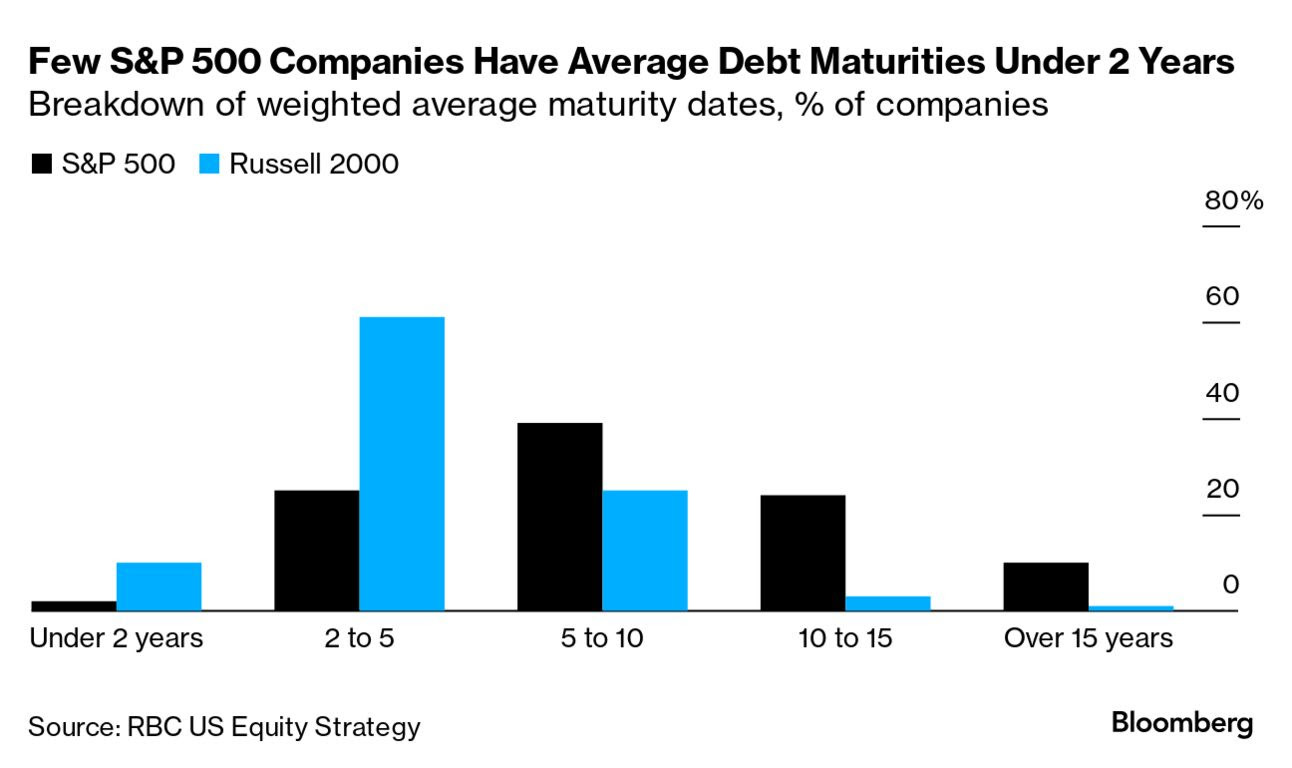

Stocks Can Scale The Maturity Wall

In the same way that the debt ceiling spooks the Treasury market every couple of years, a looming maturity wall surfaces in bear cases for the corporate credit market. Here’s the bogeyman this time around: about $88 billion of junk bonds are maturing through the end of next year, and overall, the high-yield market has the shortest average time to maturity on record.

But how big of a threat are those upcoming maturities and rising debt service costs to the stock market? Lori Calvasina of RBC Capital Markets had some soothing statistics in a note this week: very few companies in the S&P 500 and the Russell 2000 have weighted average maturities in the 2-year-or-sooner timeframe. Specifically, that comes to just 2% of firms in the S&P 500, and 10% among small-cap companies, according to RBC.

“Overall, we continue to see balance sheets as manageable,” wrote Calvasina, the firm’s head of US equity strategy. “Higher interest rates are clearly a headwind, but from a public company balance sheet perspective this issue appears to be one that companies have some time to deal with, particularly if the Fed starts cutting in 2024.”

According to RBC, the weighted average maturity in the small cap index is roughly 4.6 years, versus 8.5 years for the big benchmark, leaving the larger companies better equipped to navigate through any upcoming maturity hurdles. Not to mention, the S&P 500’s weighted average interest expense as a percent of sales has dropped to about 2%, comfortably below the gauge’s long-term average just below 3%.

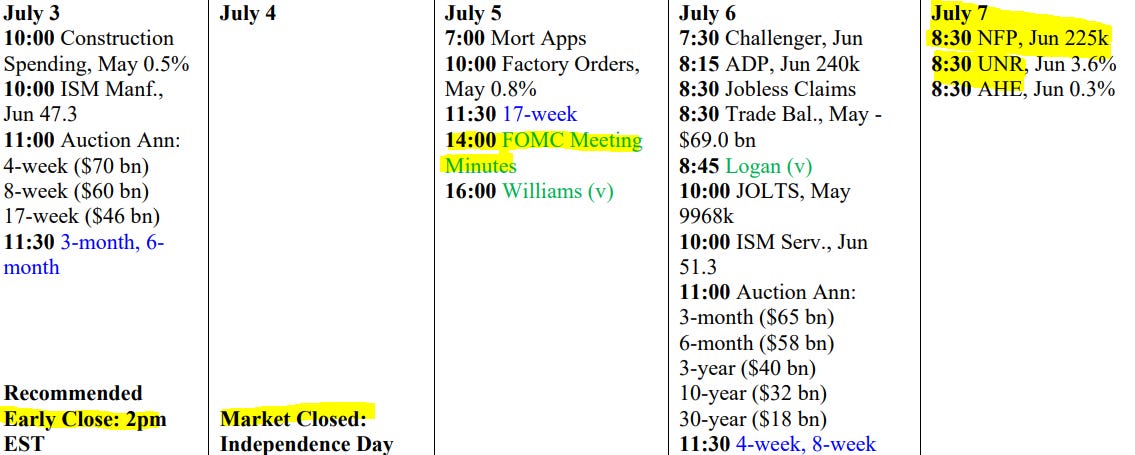

AND for any / all (still)interested in trying to plan your trades and trade your plans in / around FUNduhMENTALs, here are a couple economic calendars and LINKS I used when I was closer to and IN ‘the game’.

First, this from the best in the strategy biz is a LINKthru TO this calendar,

Off to enjoy whatever is left OF the weekend ahead … but first, in the BETTER THAN MOST ANY ALTERNATIVES category, EARTH from a real estate perspective

OR, if you prefer a live look in at how AI is developing as it may relate TO this weeks JOBS report,

AND … THAT is all for now. Enjoy whatever is left of YOUR weekend …

")

Dudley's 4.5% call seems Logical....

I have a HARD TIME seeing Federal Gov't Spending decreasing, any time soon.

Wage Growth may moderate, but very slowly

Inflation Y/E 2023.....4%

Inflation Y/E 2024.....3.3%

Inflation Y/E 2025.....2.5%