Good morning / afternoon / evening - please choose whichever one which best describes when ever it may be that YOU are stumbling across this weekends note…

I’ve been outta pocket past few days and regular pollution of this stack will likely resume Tuesday only to be once again interrupted by work related travels Thursday.

With some ‘housekeeping’ out the way AND a very weary traveler here this side, I’ll be brief and likely NOT follow the usual weekly format.

A few items from Global Wall Street which are sitting in the inbox and which I’ll HOPE to read as they would be the handful of notes / thoughts I’d like IF stranded on a desert island (OR traveling on Hwy 89N from Grand Canyon up to Salt Lake City …)

This week might start quietly but holds plenty of scope for excitement and fireworks.

The line-up of Fed, ECB, BoJ and potentially Chinese announcements raises the possibility of a repeat of the bullish price action seen in Q4 2022.

But there are notable differences to the situation three quarters ago: the Fed will be careful in its messaging; higher yields in Japan could feed into other markets; and USD positioning is currently short.

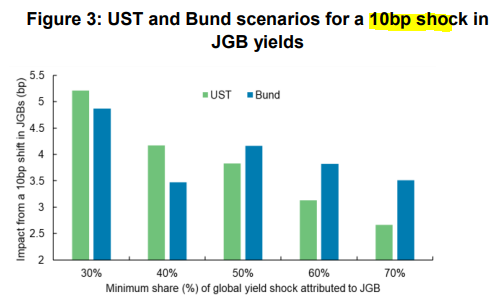

… Higher yields in Japan could feed through to other markets. Our analysis finds that a 10bp shift in the 10y JGB yield could translate into a 4-5bp shift in 10y UST and Bund yields (Fig. 3). Such a move is probably more likely in the current setting: US yields have fallen post the June CPI release, and Bund valuations are quite rich, especially after the move following the UK CPI. We are thus also short the Bund going into the BoJ meeting (EUR rates: Tactical short into next week’s risk events, dated 19 July, and BoJ YCC: July meeting a risk event for EGBs and USTs, dated 21 July).

In what world is 10bps a ‘shock’?

Moving on to this NEXT easy like Sunday morning read,

Markets have been stronger than we expected. Some of this story is straightforward, some is not, and strength has come against an unusual backdrop: across asset classes, the capital structure increasingly looks 'upside down'.

Our investment strategy has been based on the assumption that strong DM growth was set to slow sharply as post-Covid stimulus waned and policy tightened at the fastest pace in 40 years. That was the message from both a variety of our leading indicators, as well as our strategy and economic forecasts. Sharp slowing, from an elevated base, has often rewarded defensive positioning, a pattern we thought would unfold again. Valuations did not appear cheap enough to offset the pressure of this slowdown.

But our assumption about which cyclical regime to position for has been wrong. Growth has remained solid, with the US on track for a ~2% growth rate in 1H following this week’s retail sales estimate and US economic surprises coming in at the strongest pace since late 2020. Twenty years from now, an analyst may look back at 1H23 and find it quite obvious: economic data were good, and surprisingly so. Stocks, especially more cyclical ones, outperformed bonds.

Yet below this ‘straightforward’ story is another that is genuinely remarkable. While growth has held up, forward estimates for both global equities (MSCI ACWI) and US equities (S&P 500) haven’t risen all year. The entirety of the global and US equity rallies has been about higher valuations, and to an unusual degree. Over the last 25 years, only twice have we seen more year-to-date multiple expansion – in 2009 and 2020. Both of those years saw deep recessions met by enormous easing, supporting the case that valuations should expand ahead of an (eventual) longer-run rebound. That does not describe 2023.

Only two other years had similar year-to-date multiple expansion – 1998 and 2019. 2019 also saw global equities rally despite a shrinking Fed balance sheet and falling global EPS. Yet core inflation was ~2% in 2019 (and 1998), a level we don’t expect until the end of next year. Coincidentally, both 1998 and 2019 saw markets trade poorly in August-September, and multiple Fed rate cuts in the back half of the year…

You may come TO the shop for the comic strips but you’ll STAY for the Hornbach & Co notes,

MS: Financial Conditions vs. Inflation | Global Macro Strategist

What matters more to central banks? Financial conditions or inflation? Markets increasingly price the idea that easier financial conditions offset moderating inflation in central bank reaction functions. We still suggest buying bonds on growing risks of less inflation than central banks project.

… United States Rates market led astray by growth and labor data? Yields rose mildly this week on stronger data for jobless claims. There are multiple issues with the dynamic where yields have risen based on recent growth and labor data: (1) healthy labor market flows do not mean a "tight" labor market, and therefore does not mean higher inflation, and (2) the jobless claims data itself isn't reliable and may be overstating the strength of the labor market (see Making 'False' Claims?).

… Exhibit 23 and Exhibit 24 show that 10y yields have continued to follow the (mostly upside) growth surprises trajectory while getting disconnected from the (downside) surprises in inflation. We think this is the wrong framework for the rates market because if the market wants to track the Fed path, it should focus more on inflation over growth – not only because inflation is directly the Fed's mandate (unlike GDP growth), but also because recent Fed comments around monetary policy have been singularly focused on inflation outcomes, rather than growth or labor markets (see quotes in grey box further below).

Rates markets should follow cooling inflation instead of strong growth: Growth and inflation surprises have become unusually disconnected in the last 2 months – and rates markets have followed growth over inflation. Instead, rates markets should focus on inflation over growth – not only because inflation is directly the Fed's mandate (unlike GDP growth), but also because recent Fed comments around monetary policy have been singularly focused on inflation outcomes. We stay long duration vs. long 5y notes (targeting 3.50%), as well as FFV3H4 flatteners.

FOMC preview: Is the real fed funds path too high?: Mary Daly's recent comment about taking fed funds rate toward neutral as inflation moves towards 2% is notable because it signals that the real fed funds rate could stay stable to lower. Yet, we see markets pricing higher real rates into next year – an outcome even more hawkish than the one realized under Paul Volcker in the 1980s when inflation was cooling. We think the July FOMC meeting could provide clarity on this dynamic, while likely pointing towards "July and done" in line with our economists.

Treasury August Refunding Preview: Given increases in near-term deficit estimates and expectation for T-bill share of outstanding debt to rise above TBAC’s recommended 15-20% range, our base case is for Treasury to increase coupon auction sizes across tenors, with smaller increases in 7y and 20y tenors. Risks are then skewed toward further coupon increases at November refunding and beyond.

All together there’s a desire to stay LONG (5s) and in (FFV3H4) flatteners …

NEXT up are some thoughts from THE proverbial best in (rates strategy) show, and with that in mind, a few snippets as to what they are thinking and WHY they constantly win Institutional Investors popularity contest

… Our constructive bias on duration remains intact and the ability to avoid is 4-handle in the week just passed is some solace or, at least, consolation …

… It’s Fed week and the end of July will bring a 25 bp hike from the FOMC and the commencement of more entrenched summer trading conditions as August gets underway and out of office replies replace any significant conviction in the Treasury market. The size of the tightening move is no longer up for debate with no SEP on offer, Powell’s press conference will serve to set the tone coming out of the meeting and, in more practical terms, determine the trajectory of the rates market over the course of the summer. Following CPI, we were of the mind that the Chair would strike a more measured tone rather than risk sounding unduly hawkish given the progress made bringing inflation lower. However, the combination of retail sales and jobless claims, along with the fact financial conditions have continued to ease, will give Powell the cover needed to leave future hikes firmly on the table – if only to keep policy easing priced out over the course of 2023 …

… All else equal, the event risk posed by the Fed would suggest softer front-end Treasury auctions, however it is worth mentioning the last three times 2s were auctioned during Fed week (7/25/22, 1/24/2022, 7/26/2021), the auction stopped through. Zooming out and discussing 2s, 5s, and 7s as a whole in the primary market; over the last two months, June’s 5s were the only offering that tailed of the six events. While headline results at coupon auctions have been mixed so far in July, bidding statistics have been generally strong, and as such, we’ll look for solid dip-buying interest with current valuations presenting what could be the highest yielding 2-year auction since 2006, with 5s and 7s also within striking distance of the cycle highs. Thursday’s historic takedown of 10-year TIPS at an auction that stopped through nearly 6 bp with a 98.5% non-dealer allocation was certainly an encouraging indication of strong demand for Treasuries at this point in the cycle …

They go on to detail having gotten OUT of 2s10s steepener and noted,

… Aside from the technicals, we’re also of the mind that outright 2-year yields have rallied a bit too far if the Fed is going to be successful in its endeavors to keep rates on hold into 2024. While we maintain the -108 bp level is an attractive zone to add core steepener positions in 2s/10s, that is predicated on the idea that 2s in outright terms would be far closer to 5% than 4.75%.

In this vein, we'll enter a tactical short in the 2-year sector with momentum crossing in favor of a larger selloff and support sparse until 5% given the relatively thin volume profile between current levels and a handle change. We'll set our target at 4.95% with a stop at 4.75% in keeping with the tactical driver of the trade, and will look to exit either once that level is reached, or in the wake of the FOMC …

As always, a great place to BEGIN and offer another POSSIBLE take or way to phrase the question (earlier on last week as I stopped monitoring the inbox)

… The technical picture on 2’s and the techamentals from above, provide an increasingly convincing backdrop that 2yr yields have peaked. If that view is correct, then July may very well be the final rate hike in this cycle.

Why is that?

The chart below overlays the FED Funds Rate and 2yr Yields.

In May 2000, 2yr Yields peaked and so did FFR. The FED held peak rates for 7 months.

In June 2006, 2yr Yields peaked and so did FFR. The FED held peak rates for 14 months.

In November 2018, 2yr Yields peaked and FFR peaked the following month. The FED held peak rates for 6 months.

Each time 2s peaked, the FFR peaked soon after.

However, one thing to note is that shortly after 2yr yields peaked we saw yields fall in a dramatic fashion. I don’t believe that will be the case this time. The FED has a dual mandate - to achieve maximum employment and price stability. In the past 30+ years, the FED has truly only had to focus on the former task given that inflation really was not a worry. That is not the current scenario …

Have yields peaked and IS this time different? Rather than offer a view, I’ll insert a large bank in the USofAs review OF RangeZilla

… Technicals: US yield ranges reviewed ahead of the Fed We review our base case year ahead view of 1H23 yields topping and then potentially dropping in 2H23. Can see keeping bullish UST bias with 2Y < 5.1%, 5Y < 4.5% and 10Y & 30Y < 4.10%.

Ranges hold. 2Y double top? 5y triple top? Or wave 4 range before higher?

Yields have a tendency to retest the prior highs once, if not twice, as part of a formal technical topping process which is often disguised as a range. This is what we're seeing so far in the charts of 2Y and 5Y yield. The potential for a "double top" in the 2Y yield and "triple top" in the 5Y yield remain provided 2Y is below 5.1% and 5Y below 4.5%.

TRIPLE TOPs are things I thought were only spoken of but rarely things that proved useful … perhaps this time WILL be different?

building on these concepts I would pause a moment and offer a large German bank take on SEASONALITY in a note,

Our seasonality analysis suggests that the second half of July is positive for duration and credit spreads. Both USTs and Bunds demonstrate rally signals, SPGB/Bund also historically tightens in this period, and 5y5y HICP seasonally rallies. It is worth noting the second half of July is actually the strongest signal for duration in the entire calendar year.

… Bid-ask spreads and order book depth for Treasuries are at similar levels compared to June, with elevated book depth for 10yr notes. Treasury price errors to fitted curve decreased, highlighting a recovery in liquidity conditions. (TIPS market is an exception, with spline errors spiking to the highest level since the peak of the pandemic).

Our valuation models suggest that 10yr US breakeven inflation is trading 29.6bps richer than fair value, while 10yr Treasuries continue to trade close to fair value, with the residual staying within one standard deviation. For cross-market valuation, hedged treasury yield spreads against DBRs improved over the past month, while hedged yield spreads against JGBs has continued to deteriorate, with both still favoring domestic bonds over hedged Treasuries. In our term premium estimates, US and Germany TP remains inverted, with the UK having the steepest TP slope …

From SEASONALS right TO the macro economic backdrop FROM the gentleman in charge of all things economic research related, asking

DB (Hooper): Recession or soft landing: Is disinflation different this time?

… In brief, we see the line between mild recession and soft landing as increasingly fine and view the probabilities of the latter outcome undeniably on the rise. If the coming months, indeed weeks, provide further evidence of soft landing dynamics – resilient growth and labor market data met with softening wage and price inflation as the economy comes into better balance – this could tip the scales to the view that this time is different enough to warrant a soft landing.

Taking this into consideration AND trying to formulate some thoughts into / through this coming weeks FOMC meeting — hawkish HIKE anyone?

For a somewhat more esoteric take on next weeks FOMC meeting, a few words / thoughts from former Bear economist, John Ryding

… If the Fed wants to begin cutting rates while inflation is still above 2% but declining (as it should to reduce the risk of undershooting the inflation target), Chair Powell, Governor Chris Waller, and others could argue that cutting rates by less than inflation is declining is actually a passive tightening in policy.

Thus, we have the concept of passive tightening and easing. The latter concept is increasingly applying to the Bank of Japan, which meets a week from today…

Interesting. For a more basic takeaway — the HAWKISH HIKE,

With resilient activity and labor market data, we are all but certain that the FOMC will proceed with a 25bp hike at its July meeting, in line with its communication and the June Summary of Economic Projections. We expect the FOMC and Chair Powell to signal a tightening bias for future meetings.

Finally, before a couple economic calendars, a few items from the intertubes of interest

Bond investors are certain that central bank interest-rate increases are drawing to a close, fueling a strong bias to buy any dips.

There’s still plenty of confusion though about what maximum levels rates will reach, how rapidly policy makers will pivot to cuts and just how harsh the expected economic slowdowns are going to be.

The consensus is extremely strong that another rate hike is coming for most majors, starting with the Federal Reserve next week. After that, things become murkier as economies remain resilient even while inflation readings start to soften.

Former Fed head Ben Bernanke said the US central bank’s next hike may be its last, a stance Deutsche Bank also has plenty of time for. Investors though are unsure, especially after the latest labor-market data came in surprisingly strong.

European Central Bank officials pushed back against expectations it will hike in both July and September. Even avowed hawks such as Dutch central bank head Klaas Knot and Bundesbank president Joachim Nagel stressed that the latter meeting will depend on what the data show.

Core inflation for the region surged to keep investors nervous. The UK went the other way, with a sudden slowdown in inflation spurring economists to say the risks are receding that the Bank of England takes its cash rate to 7%.

The key investor reactions were to buy bonds and sell the US dollar. Recent rallies for Treasuries showed signs that hedge funds dumping bets against bonds were helping to fuel gains. One set of trades that seems to be losing favor is betting on the direction of the yield curve, with the US economy’s palpable health casting doubts on its worth as a recession indicator. Jan Hatzius, Goldman Sachs Group Inc.’s chief economist, added his voice to those doubting the curve this week as he lowered his odds for a recession.

Even in ultra-dovish Japan bond markets are facing turmoil, though there it centers on whether the central bank will finally start to join the global tightening cycle.

A year ago, the U.S. was in the midst of a “vibe-cession.” Even though businesses were hiring and debt defaults were low, the economy wasn’t good, or even fine.

Inflation was surging. Gasoline prices were high. The housing market was at a standstill. The stock market was down and crypto prices had collapsed. Consumer sentiment (as measured by the University of Michigan) hit its worst levels on record. That means that, last summer, U.S. consumers felt worse about the economy than they did during the COVID lockdowns, the Global Financial Crisis, the Tech bubble-bust, or the Volker recession.

This summer, we are seeing a big positive vibe shift. So why is everyone feeling better all of a sudden?

… Markets, as they tend to do, didn’t wait for the vibe shift to adjust. Throughout the year, equity markets have been rallying because the outlook was improving. After a nearly 20% gain so far this year for global equities, we aren’t surprised that many people feel like they have “missed it.”

But instead of asking “how long can the good times last,” we think investors should instead consider that for the U.S. economy and markets, “the good times” are much more common than the bad.

Reventure on HOUSING: Why the US Housing Market hasn't Crashed yet (repeat of 2008?)

AND for any / all (still)interested in trying to plan your trades and trade your plans in / around FUNduhMENTALs, here are a couple economic calendars and LINKS I used when I was closer to and IN ‘the game’.

First, this from the best in the strategy biz is a LINKthru TO this calendar,

Before I hit SEND, saving the (next to) best for last … The latest quarterly review is OUT and you likely have seen or caught wind of it before here and now BUT in the case you missed (like me), HERE is a link to p1,

Other major considerations indicate that the U.S. economy is far weaker than recognized. Productivity, or output per hour in the nonfarm sector, declined by a record pace over the past ten quarters. Neither a rising standard of living nor increasing corporate profitability are achievable over time without higher productivity. For the eleven quarters since the pandemic/recession ended, real average hourly earnings (which cover 119 million full time wage and salaried workers) fell at a 2.9% annual rate. This is the largest decline registered in any economic expansion of comparable length since the earnings series originated. While firms continued to add employees, the rate of increase in wages have lagged inflation. Moreover, while establishments have continued to add employees, they have simultaneously reduced the number of hours that their staff are working. Since January, non-farm payrolls have increased by 1.2 million, but the average workweek has dropped from 34.6 hours to 34.4 hours, leaving aggregate hours worked virtually unchanged. To restore productivity, firms will need to rationalize their workforce, which will simultaneously reduce labor costs, inflation and household purchasing power.

The continued tightening of financial cycle conditions with lower inflation and poor economic performance will mean that long dated U.S. Treasury yields will continue to trend lower.

Shocking, I know … NOT nearly as shocking, though, for a Northeasterner’s first visit TO THE Canyon and Utah. Some of the views from past couple days on the road …

THE Canyon

“Snoopy Mountain” (Sedona),

AND THE very best for last (IMO), Thing 1s new back yard view with golf course (bottom left, base of the hill),

… THAT is all for now. Enjoy whatever is left of YOUR weekend …

Welcome to Arizona....

Hope the FED is listening to YOU !!!