Good morning / afternoon / evening (please choose whichever one which best describes when ever it may be that YOU are stumbling across this weekends note…

It may very well be one of the shorter notes on record as I wish NOT to interrupt any / all fathers day celebrations that should be occurring.

Yours as well as mine … Jumping in,

You’ll find plenty more useful visuals out there but both daily and weekly appear to be well within RANGES and at / near supports with momentum almost a push. Perhaps weekly momentum will become oversold and a BUY over the next few weeks - time will tell - but in the meanwhile, lets get on with it …

BMO— forced outta tactical steepeners and sets forward entry dip BUY (10s) GS, “Markets appear considerably more optimistic than we are about the pace of inflation normalization” MSadds FFVSH4 flatteners — bullish leaning trade w/protection against hikes

From a few of the best in the business TO a couple / few things from the intertubes for your dining and dancing pleasure …

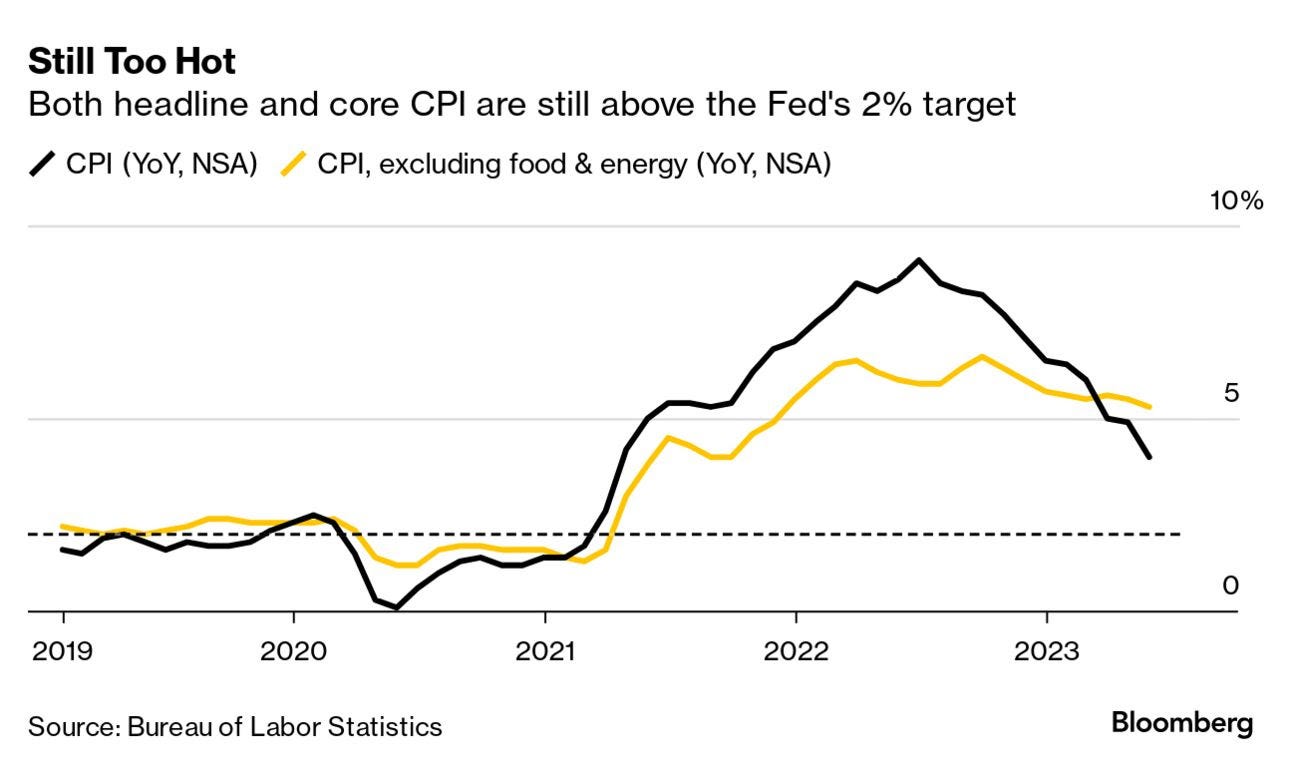

… “It’s probably a little easier to make the argument that it’s starting to look like a wage-price spiral. In ‘21, that certainly wasn’t the case. ‘21 into ‘22, supply chains for sure, maybe some profit margins were widening and you hadn’t yet seen the wage inflation that we’re seeing now,” Michael Feroli said on Bloomberg Television. “There’s kind of been a handoff from that earlier ‘21 into ‘22 into the current phase we’re seeing, which looks a little more like a traditional wage-price spiral.”

The good news is that the Fed is much better equipped to deal with wage-driven inflation than it is to combat supply-driven shocks or soaring energy prices, Feroli said. The bad news is that persistent rising pay means that it could be a slow descent from 4% inflation back to the central bank’s 2% target, according to Bank of America Corp.’s Ethan Harris….

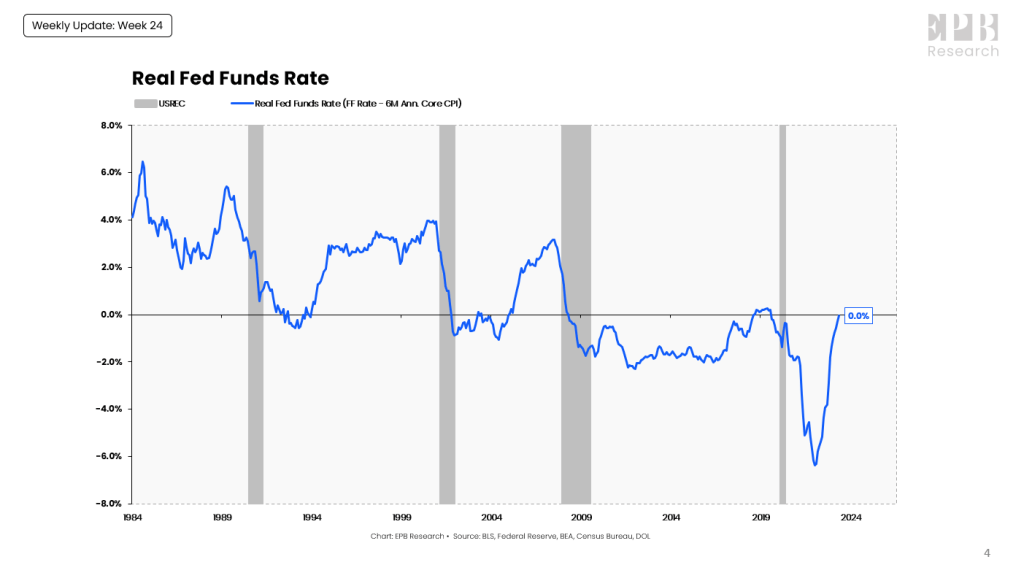

The Real Fed Funds Rate, measured by the Fed Funds Rate less 6-month Core CPI, is roughly 0%, rising from -6% in early 2022.

The downward trend in the real Fed Funds rate is due to the secular forces of lower population growth and higher debt levels.

…The economy was only able to withstand a real interest rate of 0.2% in 2018 before the Fed had to start cutting interest rates.

Today, the Real Fed Funds Rate is back to the same level but will continue to increase from here even if the Fed doesn’t raise rates anymore due to the decline in Core CPI from the lagged shelter data.

The economy is unlikely to withstand a higher level of real interest rates compared to five years ago when the debt and demographic profile, both domestically and globally, are materially worse.

Nevertheless, the Real Rate will rise and increase pressure on the economy at a time when recessionary conditions are proliferating through a wider basket of data…

Knowledge Leaders: FedGPT? AI Sentiment Analysis Shows Powell Is Still Quite Hawkish

… Nevertheless, the Fed’s DOT Plot Projection, released with the policy decision at 2pm Eastern, caused US equity markets to instantly dive, but then recover when Powell walked back the impression that two hikes were imminent, only to decline once more before a later afternoon rally as comment sentiment seemed to deteriorate later in the press conference.

Sentiment hit a press conference low according to SpeakAI’s analysis, when Powell addressed the deleterious effects of inflation on society. Powell’s transcribed comments around this included:

“So we’re still talking about, I mean, what is as strong a labor market as we’ve seen in, you know, a half century here in the United States. So overall, unemployment of 3.7 percent is three-tenths higher than it was measured to be at the last-a month ago, but still it’s extraordinarily low. And so it’s a very, very tight labor market.” –Powell

“People on a fixed income are hurt the worst and the fastest by high inflation.” –Powell

Is the Fed suddenly more hawkish than expected?

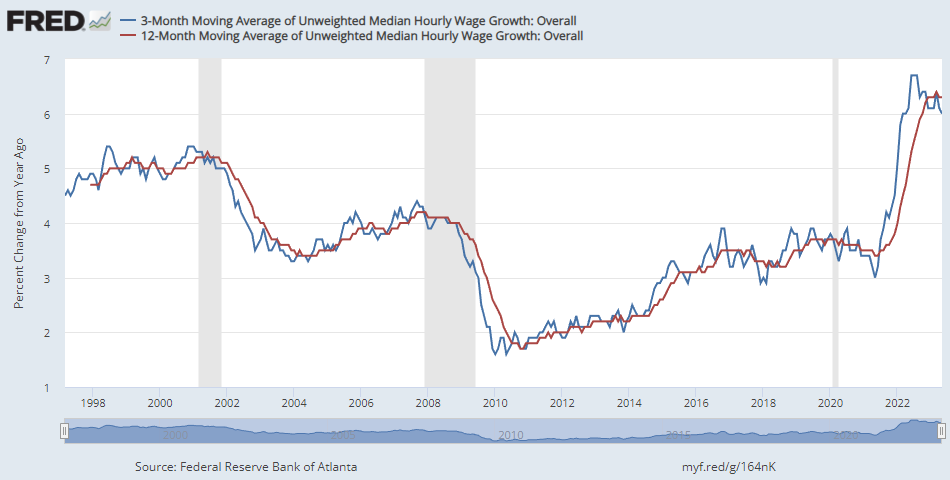

St. Louis FRED: Tracking wage growth : A measure of labor earnings growth from the Atlanta Fed

… Now, what do the data show? First, the tracked wage growth rates have not been smaller than zero between 1997 and the time of this writing. Perhaps this isn’t surprising because the CPS reports non-inflation-adjusted, or nominal, earnings. Second, the downward trend in tracked wage growth recorded between 1997 and 2011 reversed after that later date. Last and most startling, the slowdown in tracked wage growth that followed the 2001 and the 2007-2009 recessions (the shaded areas in the FRED graph) did not materialize after the 2020 recession. Instead, tracked wage growth has accelerated noticeably since 2021 and only recently seems to have plateaued. That reflects the currently resilient conditions of the overall labor market and the upward pressure on nominal wages resulting from the recent bout of above-average inflation.

McClellan: Revisiting Baltic Dry Index’s Message - Chart In Focus

Back in March 2023, I wrote a Chart In Focus article about how the movements of the Baltic Dry Index (BDI) tend to show up again just over a month later as similar movements in the SP500. Given the message from this model right now, it seems like an appropriate time to revisit this topic.

… The BDI peaked on May 10, 2023, which was 25 trading days ago. That should mean that a top is due for the stock market right about now…

I hope these few links serve as a starting point of ALL the wonderful information out there readily available for your consumption as you prep your P&Ls for the week ahead.

These in combination with Global Wall Street inbox and link-A-palooza — notes and views and NARRATIVES — will hopefully support your Father’s Day napping and celebrations over the next couple / few holiday long weekend days just ahead …

Before hitting send, and finally ahead of a couple calendars just below, you’ll note Monetary Policy reporting TO congress and so, THE ACTUAL REPORT released Friday,

… Financial conditions. Financial conditions have tightened further since January. The FOMC has raised the target range for the federal funds rate a further 75 basis points since January, and the market-implied expected path of the federal funds rate over the next year shifted up. Though yields on longer-term nominal Treasury securities were little changed, on net, over this period, the relatively high level of interest rates has weighed on financing activity. Business loans at banks grew since the start of 2023, but the pace of growth continued to slow as banks tightened standards and average borrowing costs rose. Investmentgrade corporate bond issuance rebounded to a brisk pace in May, following a slowdown in March and April. Speculative-grade issuance rebounded as well but was still subdued by historical standards. While business credit quality remains strong, some indicators of future business defaults are somewhat elevated. For households, mortgage originations remained weak, although consumer loans (such as auto loans and credit cards) grew further. After having risen last year, delinquency rates leveled off in the first quarter for auto loans and continued to increase for credit card loans…

AND for any / all (still)interested in trying to plan your trades and trade your plans in / around FUNduhMENTALs, here are a couple economic calendars and LINKS I used when I was closer to and IN ‘the game’.

First, this from the best in the strategy biz is a LINKthru TO this calendar,

I hope you get better than another shitty necktie for the collection! Happy Father's Day, or in my case I'm Happy I'm not the Father Day....but I'm a really happy uncle!

I hope you get better than another shitty necktie for the collection! Happy Father's Day, or in my case I'm Happy I'm not the Father Day....but I'm a really happy uncle!