weekly observations (5/29th); DEAL (or no deal?) so issuance may be coming; "Markets will struggle as 500bn of liquidity is removed to rebuild the Treasury cash buffer"; "Deflation Tsunami"

Good morning / afternoon / evening (please choose whichever one which best describes when ever is is you are stumbling across this weekends note…

I’ll LEAD with the obvious,

Reuters: Biden, McCarthy reach tentative US debt ceiling deal

“TENTATIVE” … ok then

Reuters: Investors react to tentative US debt ceiling deal

REACT - they say the pen is mightier than the sword but I’d say investor ‘reaction’ pales in comparison TO market expressions … lets see when markets open up AND how all TENTATIVE deal snakes its way thru the swamp …

I’ll follow the above LEAD with THIS LINK thru to a PDF chock full of sellside narratives of Global Wall Street and detail somewhat more just below but for now…understand MOST of what is noted and written was BEFORE the deal reached ‘in principle’ last night.

I also understand many / most don’t really need or care about my ranting and so if THISis what you are here for, no need to waste MORE of your time than I have already …

In as far as a deal reached IN PRINCIPLE, well, I take that to mean it all sounds good and NOW each of the negotiators has to go sell it to their respective factions in HOPES it will pass and be signed before the X-DATE (which many — including Goldilocks— now suggest is June 5th).

Before I dive a little deeper (not ever TOO deep, really), the bond market has been speaking VOLUMES the past couple weeks. What I’ve heard,

PIVOT — ie RATE CUTS — and March’s ‘bank run’ (aka F2Q)BID to bonds, well

… That saw the market very hawkishly reprice the entire short-term rate curve with 100% odds of another hike by July and pricing in rates being only 25bps lower by Jan 2024 (from 125bps lower right after the FOMC)...

… Treasury yields were dumped all week, but today saw some buying come back into the long-end, leaving the short-end (2Y) up 30bps on the week while 30Y yields were up only 3bps...

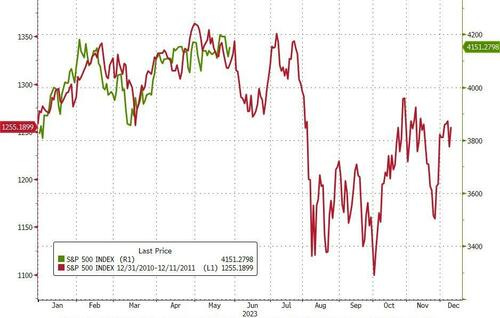

…Finally, as optimism builds of a debt-ceiling deal, remember, remember, the summer of 2011...

THAT was then, how this deal and following issuance impacts markets and liquidity is the WHAT NEXT and so … That said, I have gathered a few links / excerpts from Global Wall Street’s inbox and this weekend I’d highlight many ARE discussing the avalanche of ISSUANCE once a deal is achieved and voted. THIS DEAL will have consequences for issuance and so, LIQUIDITY in the markets. Treasury issues securities and hopefully willing buyers show up (as they appeared to do in the week just past) and so, dollars leave the system. This is a design feature not a flaw. MATH.

BMOs weekly, “Summer Plans?” — best in biz a buyer of (10yy) DIP BNP on LIQUIDITY, “…Once there is a deal, the Treasury will have runway to rebuild the TGA via a surge in T-bill supply with QT running in the background. This implies a potentially record pace of dollars leaving the system, with the combined effect of a higher TGA and QT worth about USD800bn in liquidity draining by September, in our view…There are ways that cash can be drawn out of RRP and back into reserves if needed, but they are generally costly and not without frictions” BREANsecon weekly section noting, “Recession Signal from Profits Building CSFBsmea culpa — called end of hike cycle too soon and so, JUNE HIKE it is… SocGEN, “…With yields at the high end of the recent ranges we remain neutral on rates. We look to leg into longs if the 10yT yield rises further toward 4%.” TDs ‘Doubling Down on Long 5y Treasuries’

AND MORE … Moving along, a quick recap AS far as what happened Friday, well in all the noise, there was a few things to note,

First, hard to start anywhere other than ‘flation data

ZH: Fed's Favorite Inflation Indicator Re-Accelerated In April

AND check out visual of A and PRO cyclical ‘flation … NO BUENO …

ZH: Core US Durable Goods Orders See Annual Decline; Investment Proxy Soared

ADORABLE indeed

ZH: UMich Inflation Expectations Remain At 12 Year Highs

… However, 5-10Y inflation expectations remain at their highs of the last 12 years...

AND … now for a quick spin ‘round the intertubes and of all the noise, something which stood out to me was this one by RealInvestmentAdvice via ZH

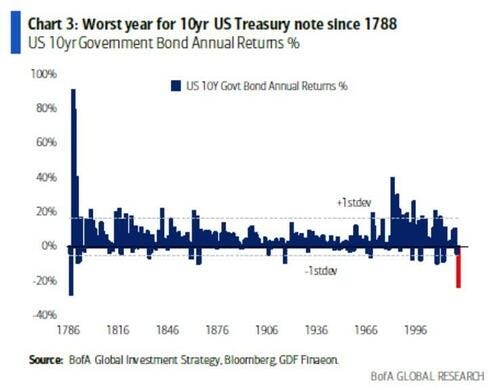

I received many emails and questions on “why” we are adding the U.S. Treasury bond to our portfolios. The question is understandable, given its dire performance in 2022, where bonds had the biggest drawdown since 1786.

However, there is, as they say, “more to the story than meets the eye.”

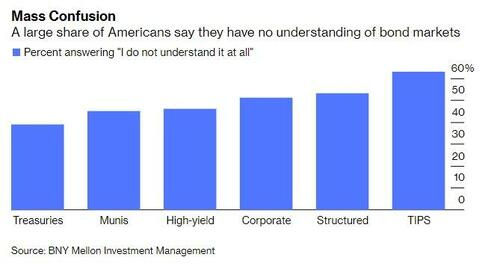

A previous survey from BNY Mellon shows that very few people understand the bond market and how it works.

“A BNY Mellon Investment Management national survey on fixed-income investing was stunning: A measly 8% of Americans were able to accurately define fixed-income investments.“

Both longer-term Treasury yields and short-term Treasury yields tend to decline during recessions, but the effect is larger and more consistent with short-term Treasuries.

Over the last eight recessions, the median maximum yield decline for the 3-month Treasury was 2.82% and 1.14% for the 10-year Treasury.

With an attractive yield compared to recent history and prospects of price appreciation if there were a recession, intermediate maturity Treasuries have a reasonable outlook on top of their potential diversification benefits if we were to see a downturn.

The prospect of a decline in yields makes shorter maturity Treasuries less attractive, as investors may need to reinvest at much lower rates when bonds mature.

… INVESTMENT TAKEAWAYS

When yields were very low, the bar for stocks beating bonds was low as well. Higher bond yields raise the bar. We continue to favor stocks over bonds because of factors that might limit the market impact of a potential recession discussed above, but we also believe that fixed income’s defensive attributes have strengthened with elevated recession risk ahead.

10-year yields don’t always meaningfully decline during recessions and are generally most vulnerable to increasing when there’s a threat of rising inflation. The inflation trend continues to be toward inflation moving gradually toward the Fed’s 2% target, but there is some risk of inflation being stickier than expected.

We no longer fear rate sensitivity (duration) and in fact have been neutral relative to our benchmark since October 2022.

At the same time, we are somewhat more concerned about shorter-maturity bonds due to reinvestment risk. Memories of bond losses in 2022 might be keeping some investors from looking at intermediate-maturity bonds at a time when they are actually attractive.

THIS one caught my eyes, too as it appeared earlier in the week from Knowledge Leaders Capital (Gavekal?)

… Hence, it is that distinct feeling that we’ve been here before that has investors mostly concluding that the federal government will agree to raise the debt limit to avoid default on its debt, but that the issues for investors won’t end there. Indeed, House Speaker Kevin McCarthy said this afternoon, “we can get a deal tonight, we can get a deal tomorrow.” While it might take a bit longer, investors may be asking: what comes next?

In 2011, the agreed-upon budget cuts led equity investors to question how government spending reductions might affect certain companies, and growth in general. This probably explains the record net speculator short interest in the e-mini S&P 500 and the 2-year, 5-year and 10-year combined option and future contracts. Investors are short both stocks and government bonds to a record extent.

Investors seem to only have eyes for cash.

AND … as debt ceiling resolves and the issuance of TBILLS machine kicks back into overdrive,

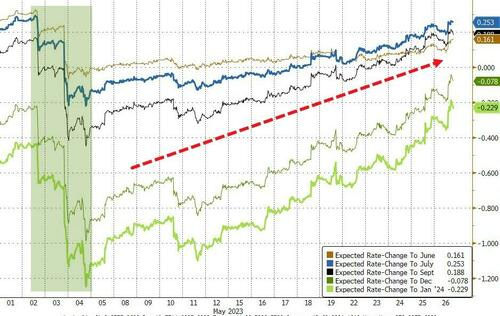

… Raising the debt ceiling also come with challenges for markets. As the Treasury will issue more bonds and bills to rebuild their cash buffer, there will be less money on bank reserves available to fund trades in other markets. Historically there has been a strong link between moves in bank reserves and markets. The 500bn reduction pencilled in until september does not bode well.

Chart 5: Markets will struggle as 500bn of liquidity is removed to rebuild the Treasury cash buffer

Inflation is one of the great economic debates and often leaves big economic thinkers at loggerheads. I am not a financial titan, but looking at the world from 100,000 feet, the conditions are in place for the world to see inflation heading meaningfully lower.

For years, inflation has been too low for comfort for the world’s major central banks. Inflation remained elusive despite ultra-accommodative policy through negative interest rates and an eye-watering amount of quantitative easing (QE). It wasn’t until a pandemic that shuttered economies and ground supply chains to a halt, a war that raised geopolitical tensions and damaged global food and energy security, and a further increase in money supply in response ,that inflation moved meaningfully higher. The question is, is it here to stay?

Inflation is the measurement of the price change for goods and services. As prices start to find a level and stop increasing, the year on year (YoY) change will eventually trend to zero. We will begin seeing these ‘base effects’ drop out, and inflation will start behaving…

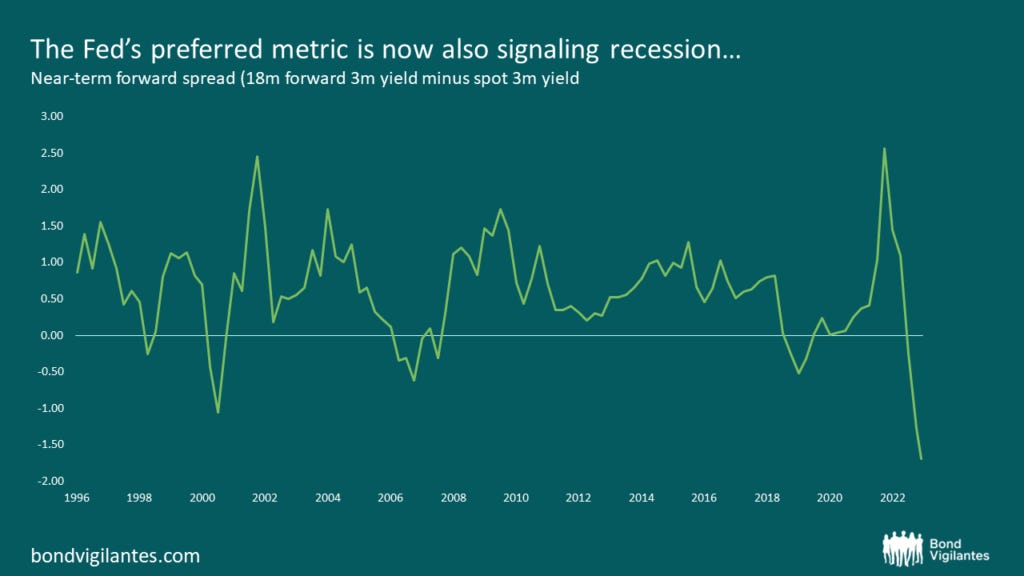

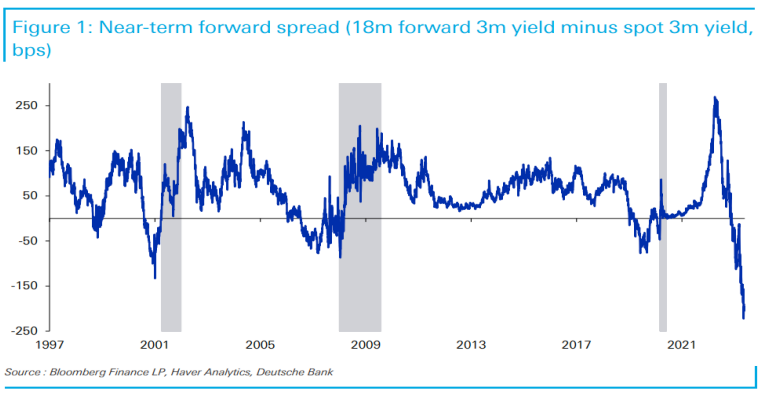

… On the other hand, the Fed needs to engender confidence; they have said that the spread between 18m forward 3m and spot 3m yield is a better indicator and inferred that recession was less likely. I’m not here to say which measure is better, but… the Fed’s measure has rolled over in spectacular fashion and now suggests the same. That was quick.

Perhaps the biggest threat to inflation is artificial intelligence (AI)…

Speaking of a DEFLATION TSUNAMI, well, no not really BUT

The latest data suggests a possible recession in late 2022 or early 2023, with weakening indicators in real personal income, industrial production, and retail sales.

… In addition to the six monthly coincident indicators, when dating recessionary periods, the NBER looks at one quarterly series. That quarterly series is actually not real GDP but rather the average of Real GDP and Real GDI, gross domestic income.

Because the income side of the economy is much weaker than previously thought, contrary to the strong wage narrative, real GDI has started to contract, and the average of real GDP and real GDI has been negative in four of the last five quarters.

So the NBER looks at seven key coincident variables, six monthly and one quarterly. Four of the seven critical variables are either flat or down relative to September 2022, which builds a reasonable case for a recession beginning late in 2022 or at the start of 2023, pending a continued deterioration in labor market data.

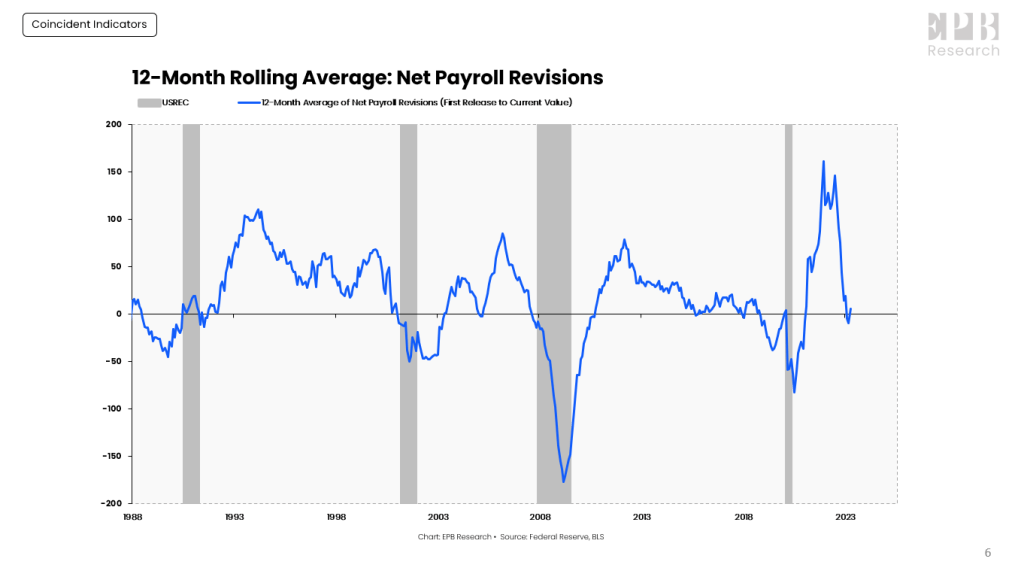

In real-time, the monthly BLS jobs report will offer, at best, a fictitious reading on the current state of labor market gains. This chart shows the 12-month rolling payroll revisions, which clearly demonstrates that the BLS data does not work in real-time as the revisions are completely cyclical.

Moving forward, this data suggest that downward revisions to BLS payroll data will be the rule, not the exception, as is the case in all pre-recessionary periods of the past.

AND for somewhat more esoteric view of the economic situation,

Kimble: Doc Copper Break Of Support Suggest Softer Economy, Says Joe Friday

Finally, for those who’s eyeballs have NOT yet rolled back into their heads and completely passed out, if you somehow missed this past week’s installment of Harley Mr. MOVE Bassman, HE presents to you …

…Moral Hazard is defined as a situation in which one person makes the decision about how much risk to take while someone else bears the cost if things go badly. But I prefer a more general definition - a lack of incentives to guard against risk. Thus, I urge the FED to seriously consider the risks of Moral Hazard…

… Not to say “I told you so”, but much of my “Open Letter to the FED” – July 26, 2021 has been prescient.

Here I suggested: 1) Reduce MBS and TIPs purchases; 2) Steepen the Yield Curve; 3) Shorten “Forward Guidance” to reduce Moral Hazard.

The most pressing need now is to steepen the Yield Curve, which means we need longer-term rates to be higher than shorter-term rates…

… The FED’s too specific “forward guidance” via the Dots offered investors unsupported confidence in the economic future. As such, too many investors and financial managers exhibited classic Moral Hazard by taking on imprudent levels of risk..

Finally, the big “surprise” will be sourced from the battle between the -blar line Yield Curve and the Stock market; I promise an ugly denouement for one.

Remember: For most investments, sizing is more important than entry level….

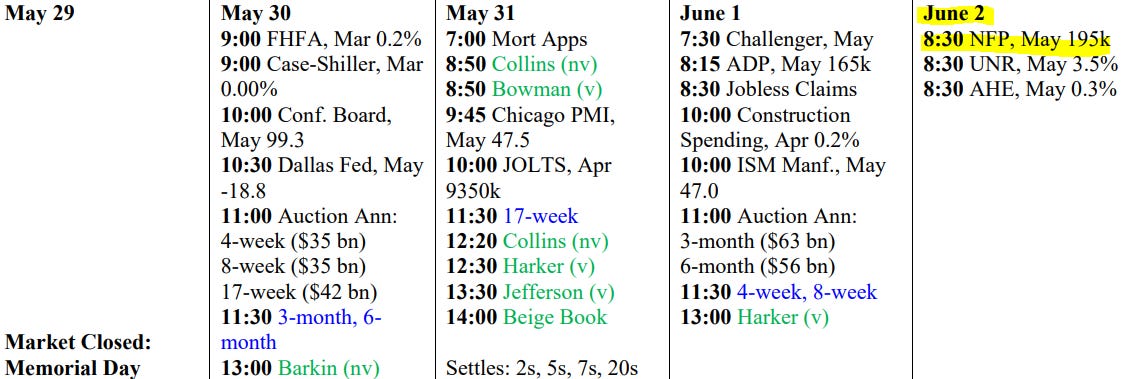

AND for any / all (still)interested in trying to plan your trades and trade your plans in / around FUNduhMENTALs, here are a couple economic calendars and LINKS I used when I was closer to and IN ‘the game’.

First, this from the best in the strategy biz is a LINKthru TO this calendar,

AND we’ve reached the point of this weekends hit where I’d like to pause and offer my sincere gratitude (and condolences) to any / all who has managed to make it this far. Said another way,

OR Straight from the ‘horses mouth’ and best in bonds/tech/macro strategy, BMOs Macro Horizon’s latest pod,

…and as the tornado of headlines from Washington DC continues to drive the macro narrative, the expression NOT IN KANSAS ANYMORE, becomes particularly apropos, as does the notion of the road to seeking opportunities is paved with positive carry …

Let us HOPE something goes from TENTATIVE and in principle TO DONE in DC as something’s got to give and help poor old Uncle Sam,

… THAT is all for now. Enjoy whatever is left of YOUR weekend … and thanks to all those who have served AND their families for their sacrifice as ALL gave some and some gave, all … remember,

All the whiles of the so-called NoFlation era, er, um, ASSET BUBBLES...., oh never mind! After your light hearted note that sobering final picture's a real Gut Punch; a Great Holiday Weekend to yourself and to all!

Great Letter !!!!

We'll see if finally the NFP, comes in low, but I wouldn't bet on it.........

All the whiles of the so-called NoFlation era, er, um, ASSET BUBBLES...., oh never mind! After your light hearted note that sobering final picture's a real Gut Punch; a Great Holiday Weekend to yourself and to all!