Good morning / afternoon / evening - please choose whichever one which best describes when ever it may be that YOU are stumbling across this weekends note…

First UP lets deal with a couple / few things FED related …

ZH: Bonds, Stocks, Gold Tumble After Fed's Williams Comments

… Williams — aka The Grinch of Liberty Street and perhaps reacting TO miserable Empire State Mfg data (?) — comments were then followed up with these …

Reuters Exclusive: Fed's Bostic sees two rate cuts, soft landing next year

AND we get it. JPOW & Co put more Fed PUT into the market and Williams and Bostic attempt to take some of it back.

Heads I win, tails you lose? As the day came to an end, well …

ZH: US PMIs Suggest "Weak GDP Growth" In Q4, Prices Remain "Elevated"

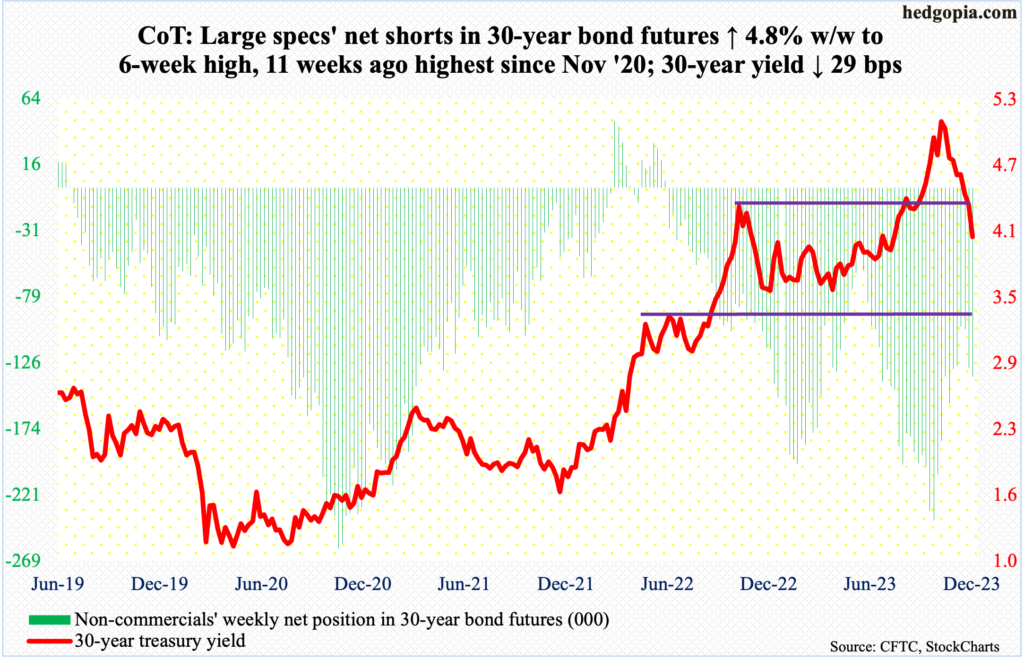

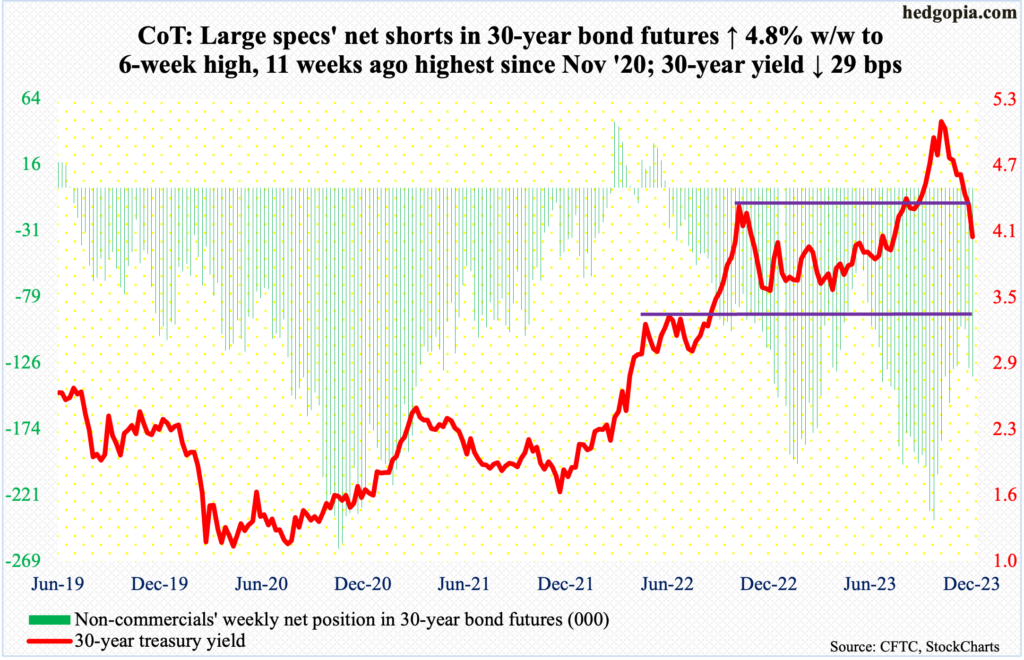

Looking at the longer - end of the curve which was fairly resilient TO Williams and Bostic — perhaps pricing in more DE / DIS-inflationary field of dreams,

Food for thought ahead of this weeks 20yr auction perhaps … thinking CONCESSION required and while there are some HOPES one gets it here as we head straight into last couple weeks of the year, characterized by lighter staffs and INCREASING vol and exaggerated MOVES which should likely be discounted / discredited a bit … well perhaps the BUY THE DIP preference inspired this past week (see updated / revised LOWER rate forecasts below) will get a chance and some of these dreams will be fulfilled.

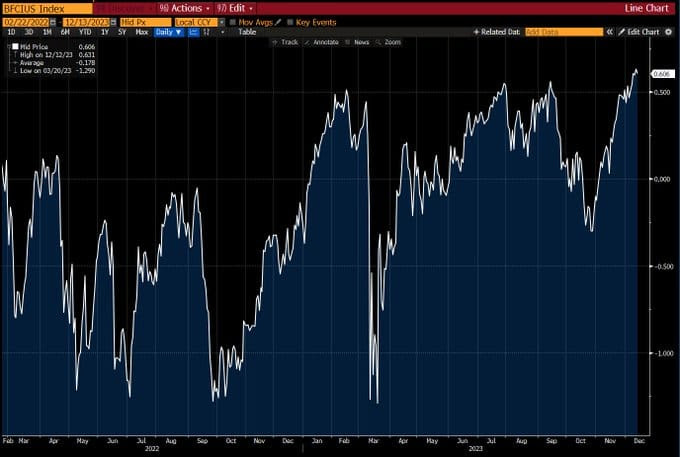

Finally and with this in mind, while there are far better explanations OF financial conditions widely available (some even on this weekends stuff below), worth noting as MacroVisor Charts of the Week does),

When looking at Bloomberg’s measure of financial conditions, it’s as if the Fed never actually tightened at all. We’re now at levels of easiness that exceed that of where we were before the tightening cycle started

Hmmm … okie dokie. Perhaps Mr. Markets doing the Feds rate CUTTING for it?

… Ok I’ll move on AND right TO the reason many / most are here … some UPDATED WEEKLY NARRATIVES … some of THE VIEWS you might be able to use where, THIS WEEKEND, I’d note a couple / few things which stood out …

Head and shoulders target reached, now what? US 10y yield reached our head and shoulders target of 4%. We see US 10y yield declining to 3.30% in 2024 and buy the dip in 1Q24 …

… Our economists have recently revised their expectations for the path of the policy rate and now expect the Fed to start cutting in June 2024 at a pace of 25bp/qtr, with a risk to an earlier start if inflation remains soft (see here). In light of that, we are adjusting our yield forecasts lower. We expect 2y yields to end 2024 at 3.8% (vs. our prior expectation of 4.2%) and 10y yields to end 2024 at 4.35% (vs. our prior expectation of 4.5%). We anticipate an earlier start to the easing cycle to have a larger effect on 2y than 10y yields and expect the yield curve to steepen…

BMOs updated year ahead (Watch the Gray Rhino, Fear the Black Swan … where again ALL cool kids forced to incorporate somewhat LOWER yields than previously — and I mean just RECENTLY — forecast)

… Team Strategy has a long-held tradition of resending the year ahead outlook during the final weeks of December in lieu of our normal weekly write-up. This year is no different with the exception of a revision based on this week's FOMC SEP and Powell's press conference. While we expect the Fed will err on the side of delaying the first cut of the cycle beyond Q1, we're now anticipating the first cut in Q2.With cuts commencing at either the May or June meeting (we're biased toward the latter), we see three 25 bp cuts at a quarterly cadence; barring a black swan event in the form of a collapse in risk assets or an external shock. The rest of our outlook remains unchanged, and we're cautiously optimistic it will survive next week... maybe…

Goldilocks: Revising G10 yield forecasts on dovish inflation focus (funny NOT funny)

… Our economists see a front-loaded rate cut schedule in the US. With a baseline featuring five cuts in 2024 and three additional 25bp cuts in 2025, we now see 2-year and 10-year USTs end 2024 at 3.7% and 4% respectively. Our projections show the trough in 10y UST yields in the middle of the year, at 3.75%, and bouncing over 2H24 on a combination of real and inflation risk premium repricing, as well as from fading downside risks to growth. Following our revisions, we now expect yield curves to steepen beyond what is priced in forwards.

It's a Wonderful Life for Bulls, where the bells have rung on Constitution Ave and the doves have gained their wings. The FOMC in the December Summary of Economic Projections (SEP) projected a median policy rate at 4.625%, below most expectations into the meeting, including ours. This decidedly bullish outcome sparked a bull steepening rally that may continue to squeeze into year-end, and validates our core 2024 Year Ahead views of duration longs and front-end driven steepeners, as well as our expectations of a Fed easing cycle starting in Q2.

UBS: We would not suggest fading the rally, but it is hard to pile on (amen)

Moving along and away FROM highly sought after and often paywalled and Global Wall Street narratives TO a few other things widely available and maybe as useful from the WWW

AllStarCharts: Bonds Sweeten a Potential Santa Claus Rally

The Bond market is turning the page.

Our long US treasury trades are finally working. And investors are reaching for high-yield debt.

On the surface, it’s a positive shift for the hardest-hit markets in 2022.

But it also sends a clear message to stock market investors…

Buy!

Credit spreads are contracting as the iShares High Yield Corporate Bond ETF $HYG trades at fresh 52-week highs relative to the iShares 3-7yr Treasury Bond ETF $IEI.

That’s what’s been on the menu since October. Whether it becomes a staple in the coming months will dictate the direction of the broader equity markets (lower MOVE Index equals higher stock prices, and vice versa.)

Credit spreads are tightening. High-yield bonds are attracting investors. And bond market volatility is shrinking.

Calling a Truce I’ve never attended, but I imagine that one of the first things they teach you in Wall Street School is “don’t fight the Federal Reserve.” Usually, it’s pretty good advice: the central bank has a habit of doing what it says it’s planning.

That was a touchstone for equity and bond bears alike over the past few weeks as traders priced in increasingly dramatic rate cuts in 2024 despite consistent pushback from Fed officials.

That made it all the more surprising when at Wednesday’s press conference following the third straight on-hold decision, chair Jerome Powell said officials discussed the timing of rate cuts. Quarterly projections showed Fed officials expect to lower rates by 75 basis points next year. And notably, Powell didn’t take the opportunity to push back against the major easing in financial conditions seen in recent weeks, as many predicted he might.

That performance paved the way for the biggest post-Fed rally in almost 15 years. Stocks, bonds and commodities all surged in harmony, building upon a trend that began in November as economic data increasingly suggested that the central bank has managed to do what was once thought of as near-impossible: cool decades-high inflation with minimal economic damage.

Bloomberg: Wall Street's risks as rates descend the Matterhorn (Authers' OpED)

…Melt-Up? If there’s a risk, it’s that the Fed has repeated the crucial error of 1998, when the meltdown of the Long-Term Capital Management hedge fund and the freezing of capital markets in its wake prompted rate cuts at a time when the economy seemed to need hikes. The result was the biggest melt-up of the stock market in history.

There are significant differences between the post-pandemic world and the much greater optimism of the late 1990s, but there are some crucial similarities. If we take a brutally simple version of equity valuation focused entirely on cold, hard cash, we can compare the yield on three month T-bills (cash) to the dividend yield on the S&P 500. The more the return on cash exceeds that on stocks, the harder it will be for stock gains to be sustained. That ratio is now its highest since the dot-com bubble. As of the middle of 1998, it was exactly where it is now, and began to dip; then came the LTCM bailout and the melt-up that followed:

My thanks to Absolute Strategy Research’s Ian Harnett for suggesting the chart. And if the notion of a melt-up seems implausible, let me offer this extraordinary factoid from the brilliant statisticians at Bespoke Investment Group:

The small-cap Russell 2,000 made a new 52-week high today after hitting a 52-week low just 48 days ago. That's the shortest turnaround time in the index's history to go from 52-week low to 52-week high dating back to the 1970s!

To me at least, that sounds uncomfortably like the lunacy we witnessed in 1999. If there’s a downside to the Fed’s pivot, it’s the risk of a melt-up.

Tearing Up Forecasts The biggest problem could be confusion. It’s dangerous to scramble perceptions as much as they have been this week. The Fed’s change has been so sudden and so stark that many investors must literally tear up their forecasts and start again.

At the end of last month, Points of Return featured a roundup of the Wall Street forecasts for the end-of-2024 level of the S&P 500. The chart we ran barely two weeks ago appears below, with a new annotation showing where the S&P 500 has closed. US stocks are already where all but the most bullish strategists expected them to be 12 months from now. Either they now go back to the drawing board and publish new forecasts, or live with the fact that they are bearishly predicting a decline next year:

Yes, this does rather expose the folly of publishing predictions for the next year when there’s still more than a month of the current one to run, a point we made at the time. But the exercise has a serious side. Strategists and asset allocators build their assumptions steadily and don’t expect to have to change them suddenly. They’re going to have to do that now.

And note that it’s not just the stock market that has already galloped through everything that was expected for 2024. Bond market predictions are all over the place, and strategists were already publishing new forecasts on Thursday. The Fed’s pivot was that big a deal. I found the note from Barclays, formally changing their position to expect earlier rate cuts, to be particularly telling:

Our economists have recently revised their expectations for the path of the policy rate and now expect the Fed to start cutting in June 2024 at a pace of 25bp/qtr, with a risk to an earlier start if inflation remains soft. In light of that, we are adjusting our yield forecasts lower. We expect 2yr yields to end 2024 at 3.8% (vs. our prior expectation of 4.2%) and 10yr yields to end 2024 at 4.35% (vs. our prior expectation of 4.5%).

This means that they expect an uninverted yield curve next year, which would make sense. But it also means that Barclays, even on revised assumptions, predicts that the 10-year yield will be higher in 12 months’ time than its current 3.95%. Even though they’re updating forecasters to account for a newly dovish Fed, they still think the bond rally is “excessive” and has gone too far.

It’s always dangerous to fight the Fed, so you can expect plenty of investors to chase this rally. But confusion on this scale presents dangers. Rather like a storm or a shower of snow on the descent of the Matterhorn, if your visibility is low and you're not sure where you are, the risk of accidents grows much greater.

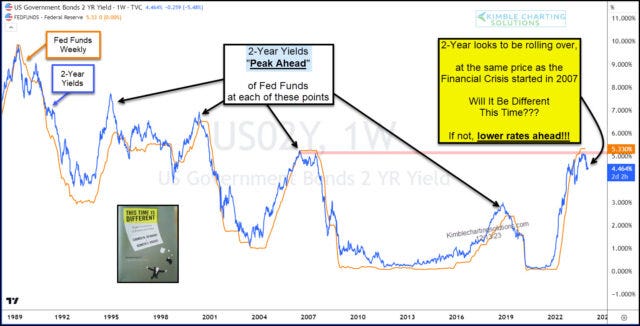

As you can see, at critical turning points, the 2-year yield turned down ahead of Fed Funds. That appears to be happening again now. And right at prior highs (resistance).

… AND for any / all (still)interested in trying to plan your trades and trade your plans in / around FUNduhMENTALs, here are a couple economic calendars and LINKS I used when I was closer to and IN ‘the game’.

First, this from the best in the strategy biz is a LINKthru TO this calendar,

THAT is all for now. Enjoy whatever is left of YOUR weekend AND year.

** PROGRAMMING NOTE ** » this is likely to be THE LAST WEEKLY compilation of the year as I’m going to be travelling along with the herd (ALL of the ‘things’) and wishing YOU and yours a Merry Xmas and happy holiday of whatever your choosing and all the very best in to the new year!

A quick historical word on Inflation (from "What an Old Coin Collection tells us about Money from the past"-Mises):

A Ben Franklin 90% silver half dollar, then worth 50 cents, has a melt value of $9.50 today (CPLie number is $5.06). In 1962, "one of the last yrs of sound money", loaf of bread was 21 cents, gas was 27 cents, and eggs were 32 cents a dozen. I wasn't born till 71, but I remember the 25 cent candy bar. They're over $2 now. We may not be Weimar (YET), but that's some MASSIVE currency devaluation in my lifetime. That's my TRUEFLATION (no diss to DDB!).

{kind=link}

Politics triumphs over Economics???

https://www.zerohedge.com/markets/now-it-all-makes-sense

A quick historical word on Inflation (from "What an Old Coin Collection tells us about Money from the past"-Mises):

A Ben Franklin 90% silver half dollar, then worth 50 cents, has a melt value of $9.50 today (CPLie number is $5.06). In 1962, "one of the last yrs of sound money", loaf of bread was 21 cents, gas was 27 cents, and eggs were 32 cents a dozen. I wasn't born till 71, but I remember the 25 cent candy bar. They're over $2 now. We may not be Weimar (YET), but that's some MASSIVE currency devaluation in my lifetime. That's my TRUEFLATION (no diss to DDB!).