Good morning / afternoon / evening - please choose whichever one which best describes when ever it may be that YOU are stumbling across this weekends note…

First UP, some good news courtesy of AT xieyebloomberg

Bloomberg: Bond Market Gets Lifeline as $25 Trillion Gauge Erases 2023 Loss

Benchmark index now shows gain for 2023 after rally this week

Softening job market, inflation boost bets on Fed rate cuts

By Ye Xie November 17, 2023 at 7:50 PM UTC

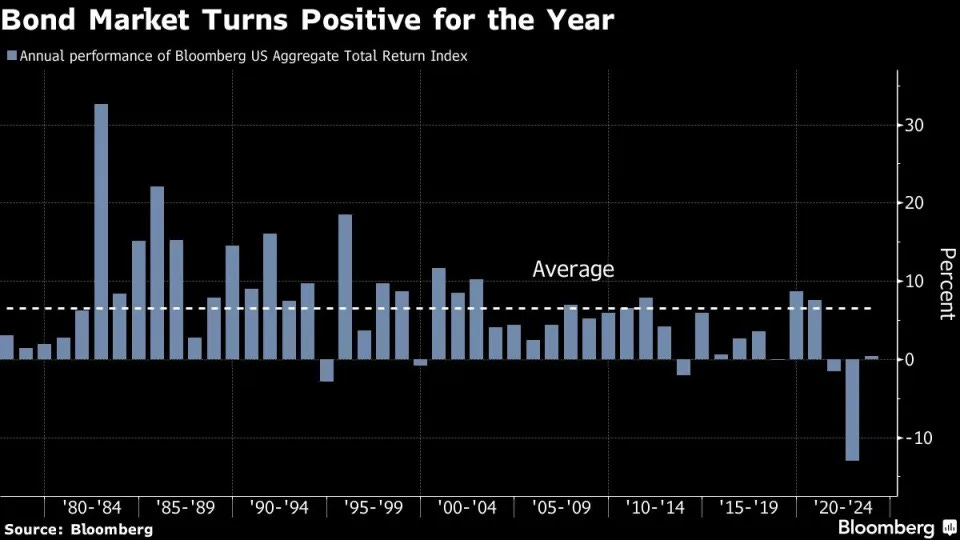

At least for now, the US bond market is on track to avoid the not-so-glorious milestone of a third consecutive year of losses, which by some accounts would have been the worst performance since the 18th century.

Following a softer-than-expected inflation report, the Bloomberg US Aggregate index has gained 1.2% this week through Thursday and is up 0.4% for the year. The benchmark, which tracks $25 trillion of investment-grade government and corporate debt, posted a record loss of 13% in 2022 and declined 1.5% the previous year. The index has never slid three straight years.

Of course, the meager gain means it won’t take much for the market to end the year with a loss. Until a month ago, such a fate seemed inevitable, with 10-year yields briefly hitting 5% for the first time in more than a decade. Four weeks ago, the bond market was nursing a 2023 loss of about 3%…

Given the small margin of victory lets not all be spiking the football too soon … In fact for further context, see JPM note referenced below …

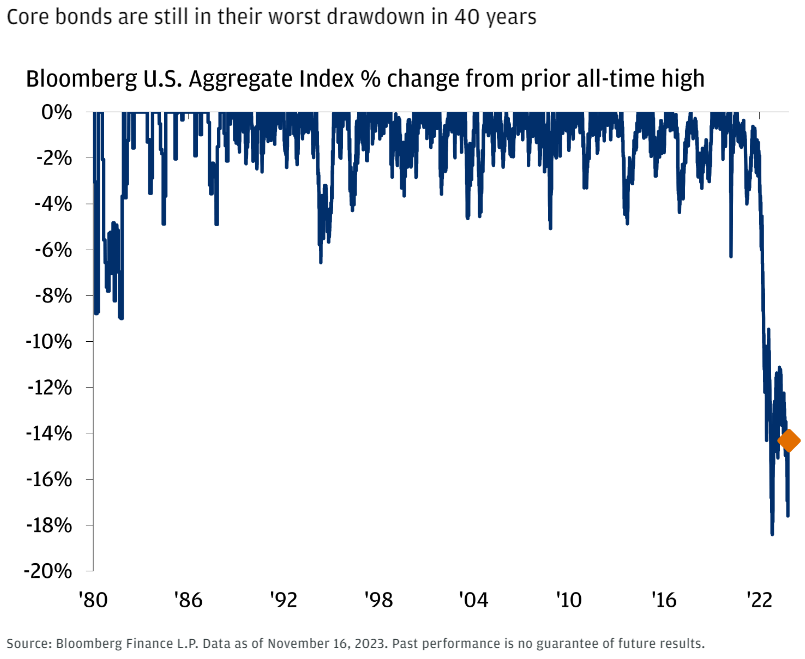

… Bonds are still at a historically attractive entry point. With the big decline in yields over the last few weeks, we mentioned that U.S. core bonds have now erased all of their 2023 losses. But, yields are still hovering around their most elevated levels in the last decade, and even with the latest rally, the Bloomberg U.S. Aggregate Bond Index is still down about 15% from its all-time highs. In other words, this is still the biggest dip in core bonds that investors have had the opportunity to buy over the last 40+ years.

But while we believe bonds stand to offer better potential for income and diversification this cycle than the last one (which was defined by an era of ultra-low rates), yields may not stay as high as they are today forever. We know from the past that when the Fed finishes hiking, rates tend to fall pretty quickly. The last few weeks is case in point.

SO … worst in 40yrs BUT getting less bad? just needing some more ready and willing to buy dips…clearly over the past several weeks some have been enticed off the sidelines to do just that, for whatever their motivation may be (speculative bets / short covering, official purchases, banks, pension funds…)

Lots of work to do and known UNKNOWNS and in the week ahead, we’re likely to see plenty of soul searching and possibly even some INCREASED vol (that possible?) as some look towards desks staffed with the ‘B team’ where a quick buck may be had and so, bonuses earned.

Otherwise known as amateur hour.

If you’ve not YET made your returns and generated your alpha with 6wks left in the year, NOW is likely NOT the time to bet the ranch BUT … we’ve seen just that before and we’ll likely see it again in the future … and to they, them, and those out there trying I only say … good luck!

Ok I’ll move on AND right TO the reason many / most are here …some UPDATED WEEKLY NARRATIVES … some of THE VIEWS you might be able to use …

THIS WEEKEND I’d note a couple / few things which stood out to ME this weekend …

Apollo: Stocks Are Stories, Bonds and Credit Are Contracts

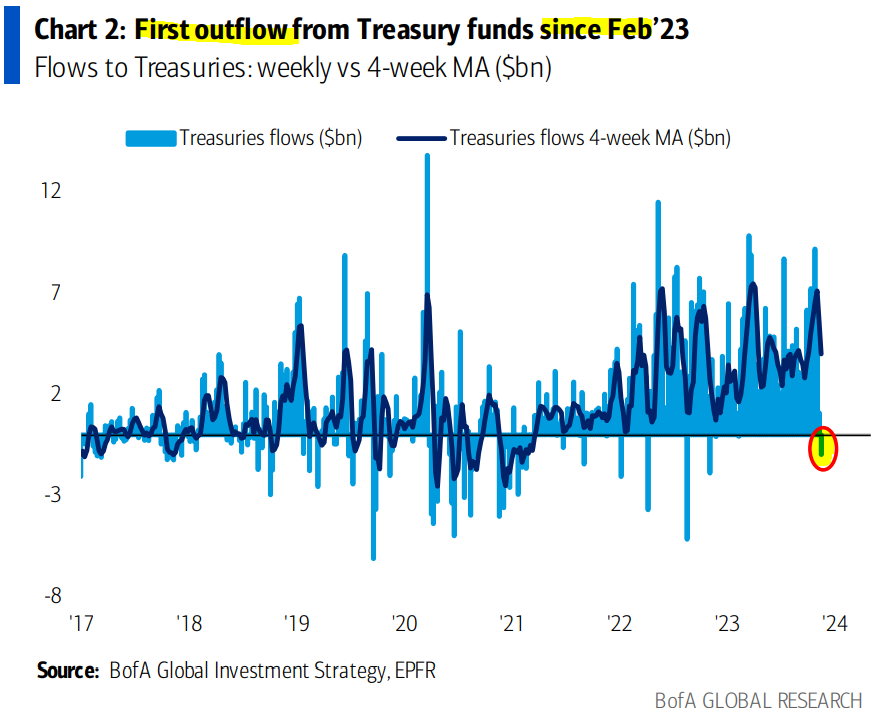

BAMLs Flow Show: Twelve Angry Trades (one caught my eye as it relates TO rates going down 3 outta past 4 weeks)

Flows To Know: Treasuries: 1st outflow since Feb’23 ($1.0bn – Chart 2)

BMO rates weekly: Concession, Not Contrition (faderate CUTS and stay in flattener)

… look to fade the Q1 2024 cuts that have made their way into valuations by steepening the Dec23/Apr 24 fed funds futures curve …

Brean WEEKLY (asking and attempting to answer question)

…Where Do Ten-Year Treasury Yields Belong … Assuming no rate cuts, the model would predict about a 5% 10-year yield for fiscal 2025. We would discount this projection somewhat given its implications for real yields and since we expect rate cuts beginning next year (unless the decline in inflation stalls out) but what is clear is that a return to the low-rate environment that prevailed before the pandemic looks fairly unlikely …

DB: FCIs belie Q1 cuts (consistent message with BMO and some others …)

… Too much easing priced in 2024, but not yet enough asymmetry for outright short

JEFF weekly: Understanding Just How Rare Soft Landings Are

JPM: Top market Takeaways: Is the coast clear? Investing amid the rally

…Bonds are still at a historically attractive entry point.

MS: 2024 Global Macro Strategy Outlook: Land of Confusion …

In the US, we expect Treasury yields to move lower over the forecast horizon, with 10-year Treasury yields trading around 4.20% by 1H24 and 3.95% by the end of 2024.We see 2-year yields end 1H24 at 4.40% and hit 3.70% by the end of 2024. We suggest long 30-year Treasuries as a medium-term trade for 1H24…

NatWEST 2024: Navigating inflation, policy, and politics in a more divergent world (rate CUTS coming Q2 2024 with end 2024 band of 3-3.25% and 2024 SHOULD be first positive year for US rates in 3 tough ones and BELLY should lead … 5s should end 2024 at 3.40%)

UBS rates weekly: US: Still long-term bullish but case for near-term holding pattern

… While we are positive in the longer term, we think we may be in a holding pattern before 10s break substantially below 4.50% on weaker data and a smooth auction cycle. This should draw investors to carry and roll trades, like being long 20s, which should benefit from expectations that the US Treasury will be far more gentle in raising 20yr auctions than in raising 10s and 30s

… Moving along and away FROM highly sought after and often paywalled and Global Wall Street narratives TO a couple / few other things widely available and maybe as useful from the WWW

Bloomberg: Wall Street Traders Are Placing All-or-Nothing Bets on a Soft Landing

… After three straight months of outflows, junk-bond exchange-traded funds are on track for their best month of inflows on record, according to data compiled by Bloomberg.

Bloomberg: Bond Routs Turn Explosive in 5% Rates World: Credit Weekly

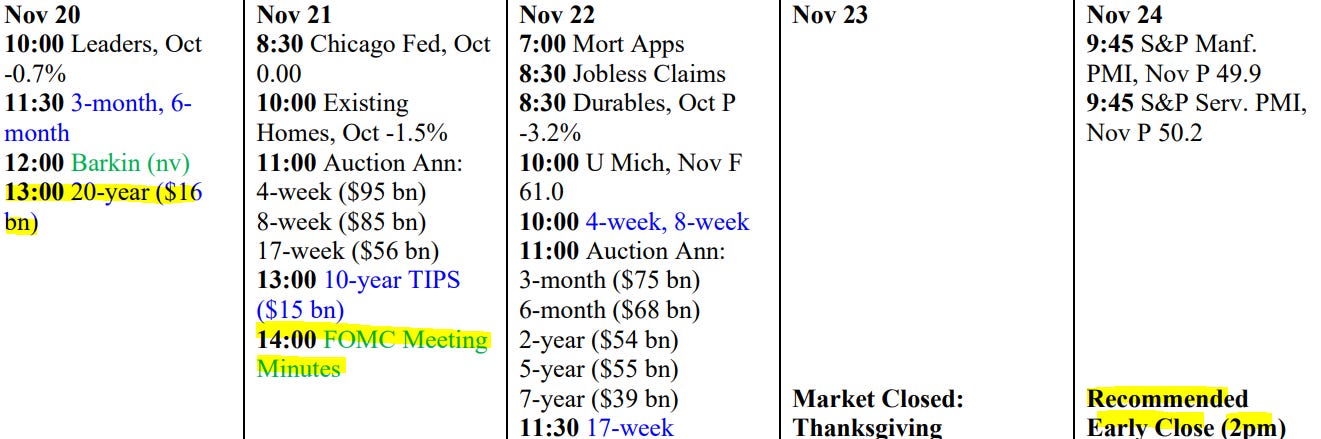

… AND for any / all (still)interested in trying to plan your trades and trade your plans in / around FUNduhMENTALs, here are a couple economic calendars and LINKS I used when I was closer to and IN ‘the game’.

First, this from the best in the strategy biz is a LINKthru TO this calendar,

{kind=link}

I've never been to a dinner THAT formal before, unless the 1972 Surrealist Ball counts :)