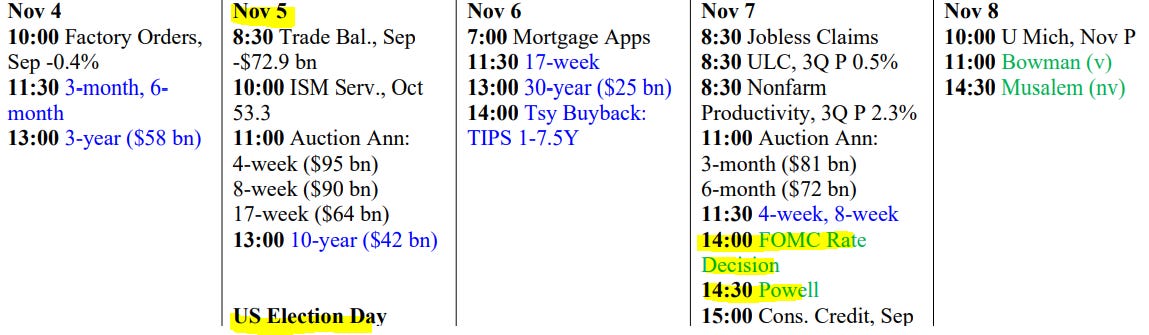

weekly observations (11.04.24): 10s oversold, rate risks 'asymmetrically skewed to the downside', "Awaiting Clarity, Avoiding Treasuries?" and more to read / consider into days / week ahead

Good morning / afternoon / evening - please choose whichever one which best describes when ever it may be that YOU are stumbling across this weekends note…

The week ahead will be one of the more consequential ones of the year and with this weeks upcoming supply of duration (58bb 3yrs Monday, 42bb 10yrs Tues and 25bb bonds on Wed), and having just passed along a monthly visual of long bonds Friday, I thought a somewhat longer-term view of 10s — the global bench — would be as good a place to start as any …

10yy WEEKLY: momentum overSOLD and 4.50% ‘support’ is nearby …

… clearly technicals do NOT matter as much as event-risk but … at least a level to consider into the days and week ahead …

I’ll attempt to have a look at shorter-term view as auctions arrive but clearly, this is more of a week to stop, think THEN trade rather than get into a hole and work your way out — just an opinion …

First UP, as is customary, allow me to deal with a couple / few items from the week just passed (in other words, a couple snarky ZH links which contain visuals and info graphics helping tell the tale of markets — INCLUDING rates — which you may / may not have already stumbled upon) …

ZH: Jobs Shock: October Payrolls Huge Miss As Private Jobs Drop For First Time Since 2020

...Stocks were not quite as whipsawed as bonds. the 2Y yield crashed 15bpas on the payrolls print... only to rip all back higher to close up 3bps on the day...

… and in light of YESTERDAYS longer-term (MONTHLY) look at long bonds, here’s a much shorter-term view of 10yy 12mins AFTER the print … the knee-jerk reaction …

… Ok I’ll move on AND right TO the reason many / most are here … some WEEKLY NARRATIVES — SOME of THE VIEWS you might be able to use — here are some (NFP)recaps, (FOMC)pre-caps and general victory laps …

…US: If Trump & strong NFP, reds / greens at risk. If Harris, the opposite. Refunding: holding pattern. Funding & spreads: tighter still.

… Overall, we continue to believe the rate outlook looks asymmetrically skewed to the downside. We see the potential for a sharp reds/greens selloff in a Trump win scenario & continued strong US data, however, this scenario seems very well priced, while a Harris win scenario & US data moderation seem underpriced (Exhibit 8 & Exhibit 9)…

…Bottom line: With many risks ahead, our preference is still to buy dips, but we have less conviction in our duration and curve views into the election. We have stronger conviction in short spreads and funding views + lower vol after election.

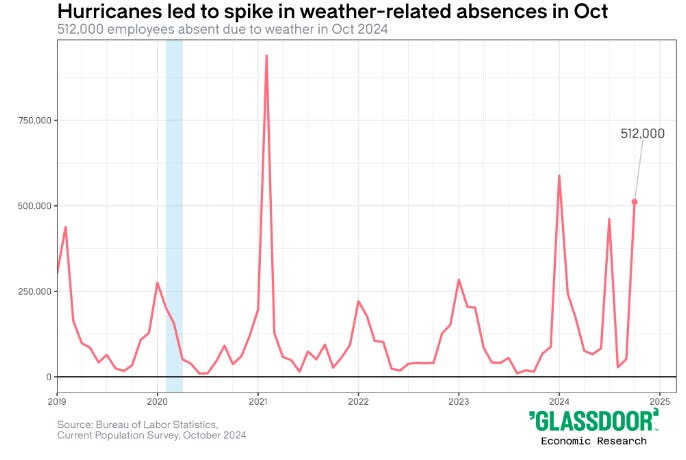

October nonfarm payrolls posted a weaker-than-expected 12k gain reflecting strikes and hurricane-related disruptions, hence providing little signal about the underlying pace of jobs gains. Downward-revised August and September estimates and the unemployment rate edging up 9bp to 4.1% likely cement a 25bp rate cut next week.

This US election implies particularly high uncertainty for the global economy, given some of the policy proposals by candidate Trump, and it may potentially take weeks before the outcome is known. Economic data have been volatile, suggesting a still decent growth outlook, but limited visibility on central bank rate paths.

US Outlook Much depends on November payrolls This week's data flow reiterated the tensions between employment and activity, with the activity and spending estimates remaining strong alongside a weak jobs number. The key question is the extent that October's weak NFP reflects signal versus hurricane-related noise. This redirects the spotlight to November's estimates.

Incoming labor market data were soft, with October job gains at just 12k, on the heels of downward-revised estimates for August and September and JOLTS job openings resuming their descent. Meanwhile, the unemployment rate held steady and payroll income looked healthy.

Data on spending and activity remain robust, with the incoming Q3 GDP estimate showing a 2.8% q/q saar gain, propelled by strong gains in private domestic final purchases. Consumer spending is on a very solid trajectory, implying sizable carryover effects into Q4. PCE price inflation is now looking firmer, following a series of soft prints.

October's weak payrolls make a 25bp funds rate cut next week nearly certain and solidify our baseline of another cut in December. However, uncertainty about weather effects helps keep a December pause in play, with November jobs estimates due on the eve of December's blackout.

… The October payrolls report was not as weak as the headlines implied but there was clearly evidence of softening from the prior month's report … according to the BLS, "There was no discernible effect [by the hurricanes] on the national unemployment rate from the household survey." …

… We were stopped out of our long 10s position for a loss on Monday at 4.290%. We haven’t revised our outlook to be bond bullish in the medium-term, although it’s been clear that the near-term balance of risks has favored higher yields from the market’s perspective. We're on-board with buying a post-election selloff in 10s, and will look to do so at the extremes …

October’s 12k gain in nonfarm payrolls reflects a 100k-plus drag from storms and strikes -- more than we expected.

We think a snapback is likely in November – and the October print may later be revised up – but the weight of evidence points to a gradually softening job market.

The print makes us more confident in our base case for 25bp rate cuts by the Fed at coming meetings.

We expect the Fed will proceed with a widely anticipated 25bp rate cut at the November FOMC meeting.

The statement is unlikely to see major changes, but may highlight special factors that weighed on the latest US jobs report. We see that report as consistent with an ongoing economic soft landing, and as reinforcing our base case for 25bp cuts through March 2025.

It will likely be too early for Fed Chair Powell to comment on the monetary policy implications of the US election.

Recent US economic data supports our view that a Fed skip is more likely to happen in early 2025 than late 2024.

FX will likely be the first asset class to move as the US election results roll in. Buy the USD on a Trump victory, sell it if Harris wins.

The makeup of Congress will be key for fixed income’s response. Markets may need to be patient for these results.

…11pm: 78 electoral votes in play. Balance of power could be emerging. At this point in 2016, it was apparent that Trump had likely won, even though the Associated Press (AP) did not call the presidential race until about 2:30pm EST on Wednesday. In 2020, the call came four days later…

We expect the Fed to deliver a 25bp cut at Thursday's FOMC meeting. This action would mark a continuation of "recalibrating" the monetary policy stance to an environment with lower inflation and more balanced risks to the Fed's dual mandate. A 25bp reduction is likely to be broadly supported on the Committee, in our view, though future decisions could be more contentious.

We believe Powell is unlikely to provide forward guidance about the policy path ahead. While he will continue to frame the outlook as tilted towards normalizing policy over time, we expect he is likely to note that future reductions will be data dependent and occur on a meeting-by-meeting basis. Our recent work showed that while policy rules are consistent with another reduction in December, the case becomes less clear cut beyond (see "Policy rules suggest it's a bit premature to plan a pause").

Our baseline remains that the Fed will deliver another 25bp reduction in December, and guide the policy rate back towards its nominal neutral level of ~3.5% next year. While the Chair will emphasize that the election had no impact on their decision to cut rates at this meeting, we have argued the election outcome could produce significant changes in policies that would impact the economic outlook and thus the Fed. Our views on this are detailed in recent notes: "Election outcomes: Growth and deficits impacts" and "Looking beyond the next 25bps to '25: The Fed outlook post election".

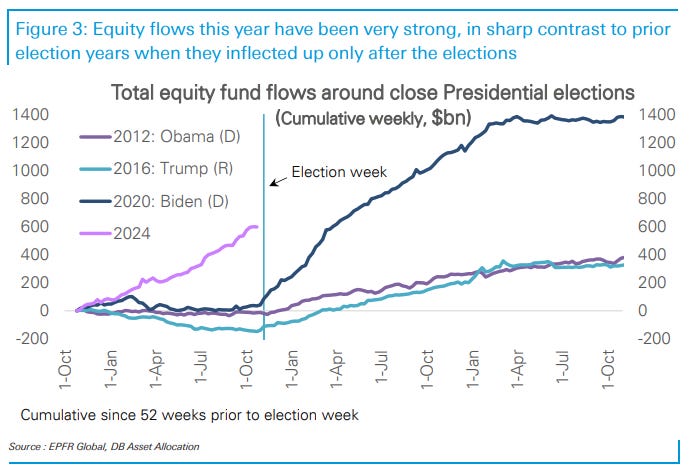

DB: Investor Positioning and Flows - Performance, Positioning And Flows Going Into The Election

…Equity inflows have been very strong for a year ($500bn+), in sharp contrast to prior years when they inflected higher only after the election. As we laid out in another piece published earlier today, driving the strong equity (and bond) inflows are a combination of supportive fundamentals and massive cash holdings built up around the pandemic ($2.4 trillion above trend), that have freed up households to not set aside more cash and instead allocate a disproportionately large part of their new savings to equities and bonds (What's Driving The Inflows Boom? Nov 1 2024). While bond flows this year have been strong as well, they look typical relative to past election years…

ING: Weak US jobs report confirms Fed has increasing room to cut rates

The US economy only added 12,000 jobs in October, but this was depressed by strike action and hurricane disruption. Nonetheless, the trend in hiring is obviously slowing and with the inflation backdrop looking less threatening, the Federal Reserve clearly has scope to move policy closer to neutral

…Changes in employment YoY% change in full-time employment and part-time employment with recessions circled

ING: Federal Reserve to cut by 25bp irrespective of election outcome

An anticipated close election outcome could prompt significant market volatility, but this won't deter the Fed from cutting interest rates by 25bp on 7 November. Inflation is less of a worry, and the Fed is putting more focus on a cooling jobs market. In turn, we expect it to continue cutting rates closer to neutral irrespective of which candidate wins

…Fed funds ceiling with duration between last interest rate hike in a cycle and the first rate cut (%)

Storms, strikes, and revisions exaggerated weakness in the October employment report, but the labor market is cooling. That backdrop supports gradual further rate cuts from the Fed.

MS: Once More unto the Election | Global Macro Strategist

The Constitution of the United States says that the executive power shall be vested in a President every four years. The time has come for citizens, and investors, to vote on the future of the world's largest economy. We stay neutral on duration, yield curve shape, and the USD into the election.

…Interest Rate Strategy United States We review the "shocking" history of nonfarm payroll surprises and offer investors two takeaways: 1) investors should expect three payroll reports each year to be "complete shockers," i.e., outside the high/low range, and almost half to be "big misses" versus consensus; and 2) investors should prepare for another payroll surprise in early December, when the BLS delivers the November payroll report.

… Of the 10 payroll reports for November that came outside the high/low range over the past 26 years, six came below the range, and four came above…

We suggested investors pay the belly of the SOFR swap 7s10s30s PCA fly last week. The belly of the fly screened rich on a 3-month Z-score basis, and technical indicators suggested an attractive entry level. Since then, the fly reverted back to a positive Z-score, so we suggest investors exit the trade.

Finally, we review the Treasury Quarterly Refunding Announcement. We believe the key part of the refunding statement was it continued to guide that nominal coupon and FRN auction sizes are not expected to be increased for "at least the next several quarters."

We note that an optimal bill share of total of outstanding marketable debt “averaging 20% over time” affords Treasury important flexibility in its financing needs, in consideration of expectations for a higher deficit path.

Expiration of the federal debt limit suspension introduces additional uncertainty with respect to Treasury's financing needs, with coupon sizes unlikely to be increased until there is a resolution. Once the new debt limit becomes binding on January 2, 2025, with coupons expected to be stable we think risks then skew toward less bill issuance and a lower TGA cash balance.

MS: FOMC Preview: November Meeting | US Economics & Global Macro Strategy

Strong growth but inflation running closer to target lead the Fed to cut by 25bp. Chair Powell is expected to recognize recent economic strength. Our strategists maintain long MBS basis.

…Our rates strategists suggest investors remain neutral on US Treasury duration and yield curve shape ahead of the US general election and November FOMC meeting…

MS: Sunday Start | What's Next in Global Macro: The US Election: Hurry Up and Wait

… Don’t read much into near-term market moves...compare ‘what’s in the price’ to the ‘plausible policy path’: We’ve spilled plenty of ink on how short-term market reactions to elections are noisy, but resulting public policy choices can drive durable moves. To that point, there are some markets where moves during the vote counting and immediately after a result is clear may not be indicative of medium-term trends. Consider the exchange rate between the US dollar and the Mexican peso (MXN). We’ve long argued that a Republican win puts a US tariff on Mexican imports in play, creating pressure on the peso. But as my colleague Ioana Zamfir points out, the peso has weakened considerably in the past couple of months, consistent with Republican strength in prediction markets and weakness among equity sectors perceived to be supported by Democratic policies. Hence, further pressure on MXN immediately following a Republican win may be limited, but the view would still be bearish in the medium term given a combination of global trade policy-related risks (tariffs, USMCA negotiations) and local policy uncertainties. A similar story is playing out in US Treasuries, per my colleague Matthew Hornbach. Large moves up in yields in the days following Republicans’ win in 2016 may have reflected expectations of tax cuts fueling more growth, deficits, or both. Republicans enter this election with a similar policy agenda and, given a chance of winning the White House and Congress, opportunity. A Republican sweep could drive longer-end yields higher over time via higher policy rate expectations. Yet a 2016-style near-term reaction is less likely because 1) a Trump win would catch investors less off-guard, 2) investor expectations – and pre-election positioning – have been grounded in the post-2016 election price action, which 3) clearly contrasts with the stance of global monetary policy and related central bank forward guidance. In equities, certain sectors perceived to benefit from Republican policies (financials and industrials) have been recent outperformers, though some of this is tied to sector-specific fundamentals. Where we have seen a clearer performance trend that suggests certain stocks may be discounting a higher probability of a Republican win is within consumer retail and brands. Some of these stocks that are disproportionately exposed to tariff risk have underperformed notably, as have renewables. And, of course, if the Democrats win, many of these recent market moves could unwind, but that shouldn’t be taken as a signal of long-term macro expectations.

Bottom line – the US election is incredibly important, but the process is likely to be incredibly noisy. Some patience, and a plan, can make the difference between navigating the noise and getting lost in it.

RBC: U.S. October job counts distorted by hurricanes/strikes

Bottom line:

The tiny 12k payroll employment gain in October was heavily distorted by the impact of hurricanes, a large strike in the manufacturing sector, and an unusually low initial survey response rate. The unemployment rate was likely a ‘cleaner’ read on labour markets in October, and it was unchanged from September and still slightly below levels in the summer..

Underlying details are still consistent with a softening in labour markets – permanent layoffs rose and downward revisions knocked 112k off payroll employment growth in August and September – but still at a very gradual pace that is consistent with a ‘normalization’ from unusually low unemployment levels rather than a faltering.

Interest rates are still likely higher than they need to be for inflation to return fully back to the Fed’s 2% inflation target, and today’s data helps to reinforce our expectation that the Fed will cut rates by 25 basis points next week.

Wells Fargo: October Employment: Searching for the Signal in the Noise

Summary We expected a noisy October employment report due to Hurricanes Helene and Milton as well as some strike activity, and the event delivered on those expectations. Nonfarm payrolls rose by just 12K in October, the weakest reading for payroll growth since December 2020. It is clear that the hurricanes and strikes reduced employment growth below what it otherwise would have been. That said, when doing our best to look through the noise, there were some signs of softening in the labor market. The industry composition of employment growth in October hinted at some weakness beyond the one-off factors that drove the poor headline reading. Job growth in August and September was revised down by a cumulative 112K, suggesting that last month's stellar employment report was not as strong as previously believed. The unemployment rate should have been less impacted by the hurricanes and strikes, and on an unrounded basis it rose by one-tenth of a percentage point.

On balance, the unusually weak employment report in October should be taken with a healthy dose of skepticism. The special factors at play likely will keep the FOMC from repeating its September 50 bps rate cut at its meeting next week. That said, the continued softening in employment conditions was consistent with the other labor market data released this week. A decline in job openings and slowdown in employment cost growth are additional signals that inflationary pressures are no longer emanating from the labor market. A 25 bps rate cut at next week's FOMC meeting seems highly likely in our view.

United States: It’s Halloween. Everyone’s Entitled to One Good Scare. Nonfarm payrolls rose a much weaker-than-expected 12K in October. Worker strikes and hurricanes played a major role in the headline miss. The unemployment rate, which is derived from the household survey and counts those not working due to a strike or severe weather as employed, held steady at 4.1%. A 25 bps rate cut at next week's FOMC meeting remains highly likely.

…Interest Rate Watch: What Goes Up, Must Come Down We expect the FOMC to elect to reduce the federal funds rate 25 bps at next week's monetary policy meeting. Economic growth has generally remained solid since the Committee last met in September, but the restrictive stance of policy today supports a further reduction.

Yardeni: DEEP DIVE: Ten Useless Macroeconomic Theories

… MMT’s zealots within the current administration have been essentially using a blank check to load up on fiscal stimulus even though the economy is already growing faster than 3.0% y/y. The interest cost on the federal debt is increasing rapidly due to the record debt issuance and higher rates (Fig. 16 below).

Figure 16

… (3) Disinverting yield curve. The Treasury yield curve has flipped positive in September, with the 10-year yield now roughly 15bps above the 2-year yield (Fig. 20 below). Historically, a recession has followed soon after such a disinversion—but only because the Fed was cutting interest rates rapidly to stem a crisis, which then morphed into a recession. This time around, the Fed is cutting rates as a preventative measure.

Figure 20

… AND more. MUCH, much more…

… Moving along and away FROM highly sought after and often paywalled and Global Wall Street narratives TO a few other things widely available and maybe as useful from the WWW

When the Fed started raising interest rates in March 2022, a lot of Fed speeches and market conversations focused on the long and variable lags of monetary policy, i.e., the time it takes before Fed hikes begin to slow down the economy.

Traditional impulse-response functions in VAR models and the Fed’s own model of the US economy, FRBUS, suggest that it should take 12 to 18 months before tighter monetary policy begins to slow the economy down.

However, it has been 30 months since the Fed started raising interest rates, and we have still not seen any sign of a slowdown. This week, we got GDP growth for the third quarter, and it came in at 2.8%. And the Atlanta Fed’s GDP estimate for fourth quarter GDP is 2.3%, above the CBO’s 2% estimate for long-run growth.

This is the key issue across the S&P 500, credit, FX, and private markets: What happened to long and variable lags? Why is GDP growth still above potential, and why did Fed hikes not slow down consumer spending and capex spending the way the textbook would have predicted?

There are three reasons:

First, the US economy has been less sensitive to interest rate increases because consumers and firms locked in low interest rates during the pandemic.

Second, the US economy continues to experience a big structural boom in AI and data centers.

Third, fiscal policy is easy with a 6% budget deficit, driven by the CHIPS Act, the IRA, the Infrastructure Act, and defense spending.

These tailwinds combined have offset the mildly negative impact of Fed hikes on highly leveraged consumers and firms.

In addition, these three tailwinds are unique to the US, which is why the business cycle is strong in the US and weak in the rest of the world.

With the Fed now cutting rates and these three tailwinds still in place, the outlook for the US economy continues to be positive.

Our latest chart book with daily and weekly indicators for the US economy is available here.

… One big difference this year is that a lot more of the voting is being done early, ahead of the Nov. 5 official election day. So if the change in polling results are accurately reflecting shifting mood among voters (and yes, that is a BIG if), then any drift in the polling data which echoes the movements of bond yields will not affect votes that have already been cast. But early voters also tend to be more firmly committed to their choice ahead of time, and thus they are not as likely to be voters whose decisions might change at the last minute.

WolfST: Buffett T-bills & Chills: Piled up T-bills, Ditched Stocks, Bonds, and Share Buybacks in Q3

Oracle of Omaha will sit on lots of dry powder when the S hits the fan and there will finally be some stocks worth buying.

… AND for any / all (still)interested in trying to plan your trades and trade your plans in / around FUNduhMENTALs, here are a couple economic calendars and LINKS I used when I was closer to and IN ‘the game’.

First, this from the best in the strategy biz is a LINKthru TO this calendar,

Finally, a couple pictures and first one is a PSA …

… you are welcome … NEXT up, having just returned from a funeral for a good friend who lost his 95y father — lived a good live and never is it a ‘good time’ BUT just made me ponder my current situation and, well, some truth …

… AND, well, THAT is all for now. Enjoy whatever is left of YOUR weekend …

{kind=link}

{kind=link}