weekly observations (10.21.24): The First National Bank of Lindsay, OK (is, well, NOT okay), 10s vs 200dMA (DipOrTunity?), "No Landing Continues" -Apollo

Good morning / afternoon / evening - please choose whichever one which best describes when ever it may be that YOU are stumbling across this weekends note…

Still waiting for some light from Lacy Hunt and as I’ve just checked site for Q3 update and it’s not yet available, well, I’ll be brief …

AND before I begin, I’ll interrupt your regularly scheduled weekend programming for this note from the FDIC which hit inbox last night at 722p

PRESS RELEASE | OCTOBER 18, 2024 First Bank & Trust Co., Duncan, OK, Acquires Insured Deposits of The First National Bank of Lindsay, Lindsay, OK

WASHINGTON – The First National Bank of Lindsay, Lindsay, Okla., was closed today by the Office of the Comptroller of the Currency (OCC), which then appointed the Federal Deposit Insurance Corporation (FDIC) as receiver. To protect depositors, the FDIC entered into a purchase and assumption agreement with First Bank & Trust Co. Duncan, Okla., to assume the insured deposits of The First National Bank of Lindsay…

… All customers of The First National Bank of Lindsay will have access to their insured deposits. Over the weekend, customers of The First National Bank of Lindsay can access their deposits by writing checks or using ATM or debit cards. Checks drawn on the bank will continue to be processed. Loan customers should continue to make their payments as usual …

… as usual, the majority will pass this one by and not make too much of it and HOPE it is a one-off. For somewhat more on banks and flows, I hope you’ll scroll to the bottom and note, “US Banks Suffer Biggest Weekly Deposit Outflow Since SVB Crisis”. I’m quite sure all is a coincidence and will move right along myself. I will wondering if the economy is as strong as some of the (seasonally adjusted) data might assert and would thoroughly enjoy a debate between Team Rate Cut and say, the other guys (Bianco and Torsten Slok).

For NOW, though, without a public debate existing (to the best of my knowledge), i’m forced to try and make assumptions based on rates markets and pricing and to that end, a quick look at the bond market to best of my current ability …

10yy: support up nearer 4.18 — 200dMA — is near, some suggest a ‘DipOrTunity’ …

… momentum IS overSOLD and a push higher might very well bring in some bids

… Ok SO the wait for Lacy Hunt continues and I’ll move on … THIS WEEKEND, a few things which stood out to ME …

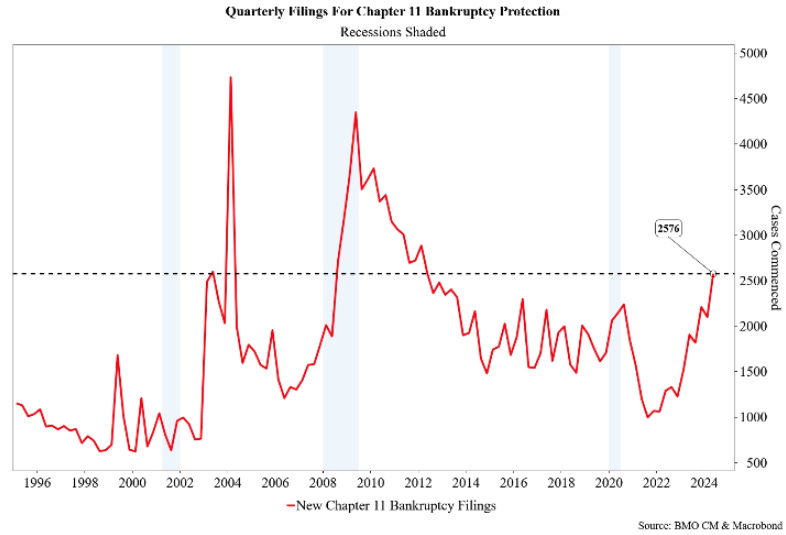

First up, best in biz watching 200dMA and leaning on bankruptcy filings, perhaps econ not all that strong and so, will look to BUY 10s at 200dMA (4.17) and watching triple top (4.116%) …

In the week ahead, there is a limited docket of fundamental events that could inspire trading direction in the US rates market. The resulting environment will be one in which external markets, headlines, and other developments will have a disproportionately large influence on the direction of yields. It’s also a backdrop for the technicals to be of elevated relevance as the recent bearish tone has brought yields to the top of the local yield range. The 200-day moving-average in 10s remains a bearish beacon at 4.170% and in the event of another leg lower, this will be our target as well as a potential inflection point for dip-buyers. Even if the 200-day initially fails to hold as support, we anticipate otherwise sidelined buyers awaiting an opportunity to add duration exposure to get involved before 4.25%. Global central banks are in rate cutting mode and while the FOMC is poised to downshift to a quarter-point cadence in November, policy rates are heading lower – a dynamic that has effectively created a ceiling for yields in a selloff….

… Our first chart shows the number of quarterly filings for Chapter 11 bankruptcy protection. For context, the vast majority of Chapter 11 cases are filed by incorporated businesses, but it is also available to individuals who do not qualify for Chapter 7 or 13. Chapter 11 bankruptcy filings totaled 2,576 in the three-month period ending June 30, 2024 (2,462 of those cases were 'business' and 114 were 'nonbusiness'). This was the highest number of quarterly filings since 2Q 2012. To help frame the magnitude of the recent gains on an annual basis – 1,198 cases were filed in 2Q21, 1,291 were commenced in 2Q22, and 1,906 were recorded in 2Q23.

In other words, the latest quarter showed double the amount of Chapter 11 bankruptcy filings than the comparable period from just two years ago. Over the summer, ABI Executive Director Amy Quackenboss said, “The continued increase in bankruptcy filings reflects the growing economic strain on businesses and households.” The persistent uptrend in bankruptcy filings has offered a clear sign of financial distresses among businesses and households that have and will continue to face an array of economic headwinds…

… a note on STOCKS, investor positioning and flows from German institution …

DB: Investor Positioning and Flows - Taking Stock Of The Five Catalysts

Two weeks ago, we noted five key catalysts and considerations for this month: lingering growth concerns, the earnings season, geopolitical risks, and of course the US elections, all amidst a continued robust demand-supply backdrop for equities (Five Considerations For A Catalyst Rich Month, Oct 4 2024). The unusually large number of potential catalysts saw implied volatility in equities rise sharply at the beginning of the month, well above realized vol. In our reading, the news over the last two weeks has tilted positive on each of the five. That has seen the vol premium shrink and in turn an equities rally.

On the growth front, positive surprises started with the robust payrolls report two weeks ago but have continued since, with the Atlanta Fed’s GDP growth tracker rising to 3.4% now. Data surprises have clearly turned positive over the last two weeks after spending 5 months in negative territory. That phase of negative data surprises followed the unprecedented 15-month phase of positive data surprises through 2023 and early 2024. We would characterize the end of the recent negative phase as a return to the normal pattern of periodic positive and negative phases lasting about 4 to 5 months on average.

On the US earnings season, it is still early, but the results so far are slightly stronger than expected going in, especially for the Financials where investor positioning in our reading was below neutral coming in but has now moved higher (Q3 2024 Earnings: Looking For A Modest Deceleration And Average Beats, Oct 3 2024).

On the geopolitical risk front, news flow out of the Middle East over the last two weeks has been far more benign than feared. Indeed, oil prices are down sharply, the backwardation in futures prices remains very modest and the implied vol premium in oil quite low (albeit with realized vol still very high).

The demand-supply balance for equities has remained robust with positioning rising modestly with plenty of room to go higher, another week of strong inflows, and buybacks slowly turning up to full strength as blackout periods end.

The focus in our view is likely to shift back to the US elections, where the key question is if we get a typical close election pullback. As is evident from the above, the market is not reacting to just election news. However, the market perception in the last few days has been that the Presidential race is moving toward former President Trump. As we have said often previously, when the race becomes less close, the market reacts positively. The polls meanwhile remain extremely tight and, in our view, still point to a close election, especially considering uncertainty around Congressional races. The vol premium for the day after the election is about 4 points over current realized vol, not too far from that seen at this stage of the last 2 elections. Our base case remains it will rise as we get closer to the election, as it did in 2016 (15 points) and 2020 (30 points) and the historical pattern play out (To Year End, Sep 12 2024)…

… AND a global MACRO note i’ve come to know, love and rely on …

MS: The Election Godot Will Show | Global Macro Strategist

Most macro investors in most macro markets now await the US general election – the outcome of which, while uncertain, will certainly come. We remain on the sidelines in US rates and the US dollar, and focus on risk exposure in Europe, the UK, and dollar bloc rates and currencies.

…Interest Rate Strategy In the US, we remain neutral on duration and curve shape….

…United States We remain neutral on the US rates duration and curve shape until we get past the US general election. Once investors see the results and respond, rates markets will likely move to price in risk premiums around a new baseline view of the future that may be substantially different from what investors hold today. In the rates market, investor views and the risk premiums markets price around them should link closely to Fed policy.

We discuss how the market pricing of Fed policy dominated US rates markets across the curve year-to-date. We analyze how (1) the number of months until the next market-implied rate move, (2) the pace of moves in the 12 months following the next market-implied rate move, and (3) the market-implied peak or trough policy rate affected longer tenor OIS rates.

We also discuss the idea that investors reduce or limit their risk exposures into US general elections. After creating normalized indexes of the open interest in euro-dollar and SOFR futures since 2000, we assessed the impact of elections on the amount of risk investors may carry. Our findings give credibility to the general view of how investors handle US elections. They also suggest short-term US rates markets should remain range-bound into the US election, but could move dramatically in the months after investors know the outcome.

At November refunding, we expect Treasury will keep both nominal coupon and FRN auction sizes unchanged following guidance from August that coupon sizes will be unchanged for the next several quarters. We believe further clarity on deficit trends, and thus issuance needs, will come after the outcome of the November US presidential election. Both the outcome of the US presidential election, as well as the composition of the House and Senate, will help to inform the number of quarters that coupons remain at current sizes.

The consumer remains resilient. August recession fears should be fully laid to rest. But for the string of Fed rate cuts that we expect, inflation needs to continue to cooperate.

The US consumer has surprised on the upside recently. But these gains have been primarily driven by high-income, asset-rich households. No wonder anger about rising inequality is once again shaping the political discourse. Add to that US corporate profit margins reaching unprecedented levels, at the expense of workers, and you might have a big problem brewing for investors.

… Aside from Greedflation, which we wrote about last week (link), one other unprecedented event in this cycle that has boosted corporate profits is that large cap companies were able to lock into super-low fixed borrowing rates in 2020/21 and put the proceeds on deposit at variable rates. Hence corporate net interest payments have shrunk despite interest rates surging higher.

…Debbie and I have found over the years that the CSI is more sensitive to inflation than the Consumer Confidence Index (CCI), which also is inversely correlated with the Misery Index but tends to be more sensitive to labor market conditions. The CCI is showing a happier reading of 98.7 during September, solidly above its 92.7 average since 1978 (Fig. 6 below).

Figure 6

Inflation over the past two years remains a sore point with consumers even though it has been moderating since last summer and even though wage gains have mostly kept pace with price increases.

Consider the following ten points:

(1) Since the start of the pandemic during March 2020 through September of this year, the CPI is up 21.9%, with CPI goods and CPI services up 20.3% and 22.8%, respectively (Fig. 7 and Fig. 8). Interestingly, the CPI goods price level has been flat since June 2022. However, the CPI services price level has continued to rise since then, led by its shelter component…

Moving along and away FROM highly sought after and often paywalled and Global Wall Street narratives TO a few other things widely available and maybe as useful from the WWW …

…Why is the incoming data so strong? Because the list of tailwinds to the economy keeps growing:

1) A dovish Fed

2) High stock prices, high home prices, and tight credit spreads

3) Public and private financing markets are wide open

4) Continued support to growth from the CHIPS Act, the IRA, the Infrastructure Act, and defense spending

5) Low debt-servicing costs for consumers with locked-in low interest rates

6) Low debt-servicing costs for firms with locked-in low interest rates

7) Geopolitical risks easing

8) US election uncertainty will soon be behind us

9) Continued strong spending on AI, data centers, and energy transition

10) Signs of a rebound in construction order books after the September Fed cut

These 10 tailwinds are increasing the likelihood that the Fed will have to reverse course at its November meeting.

In short, the no landing continues.

See our chart book with daily and weekly indicators for the US economy.

Source: Redbook, Haver Analytics, Apollo Chief Economist…

… funny thing happened on way to rate CUTS … mortgage rates went up …

Bloomberg: Perverse Timing For People Who Want to Refinance Their Mortgage

… Of course, the perversity here is that the rate cut timing ended up being the recent bottom in the market for mortgage rates. The cost of a 30-year fixed-rate mortgage has been increasing since then, and is currently hovering just under 7%.

Maybe some lucky people managed to refi their mortgage on exactly that day. But mostly probably didn’t. And certainly anyone who expected that the Fed cutting 50bps would somehow mechanically lead to a 50bps reduction in mortgage costs will have been sorely disappointed…

… JPM with some eye candy on 60/40 …

JPM: T-minus 75 till 2025: What every investor should know

…For example, take a basic 60/40 portfolio over the last year (60% invested in S&P 500 stocks and 40% in U.S. Bloomberg Aggregate Index bonds), which has notched an almost 27% total return. Without rebalancing, the same portfolio would now be overweight stocks at 64% and underweight in bonds at 36%, given the performance differential between the two asset classes.

… In addition to the stock bond mix, there have also been rotations within asset classes – right-sizing AI exposures, adjusting European allocations, and leaning into health care – specifically into more opportunistic exposures like weight loss drugs. With a soft landing as the base case, the team is focused on diversifying risk while maintaining a pro-cyclical stance at the portfolio level, with significantly less downside risk than broad equity markets.

… a great visual from across the pond on how the Fed offered markets BIG rate cut and that reduced future cut pricing …

The Fed’s big 50 basis point interest rate cut revealed a strong bias toward getting ahead of downside risks. This is good news for the economy, but economic data has remained surprisingly strong, which increases the risk of inflation down the road.

… finally, given the FDIC news Friday night …

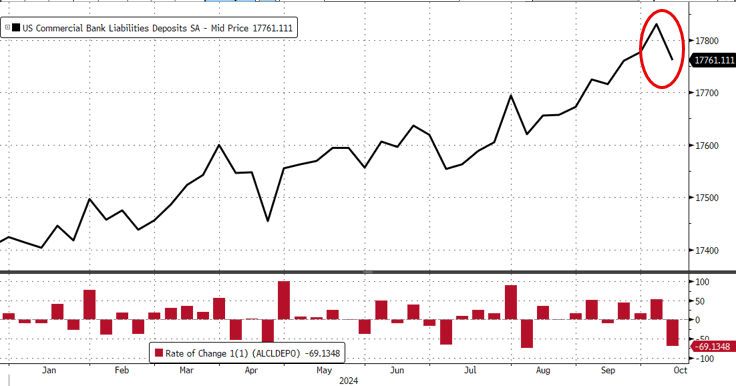

ZH: US Banks Suffer Biggest Weekly Deposit Outflow Since SVB Crisis

After the massive deposit inflows the prior week, US banks saw total deposits plunge in the week-ending 10/09 (latest data released today), down a stunning $69BN (on a seasonally-adjusted basis), erasing the prior two weeks deposit inflows...

Source: Bloomberg…

AND for any / all (still)interested in trying to plan your trades and trade your plans in / around FUNduhMENTALs, here are a couple economic calendars and LINKS I used when I was closer to and IN ‘the game’.

{kind=link}

{kind=link}

{kind=link}