Good morning / afternoon / evening - please choose whichever one which best describes when ever it may be that YOU are stumbling across this weekends note…

These days, the end of Summer, bring with them some anniversaries. This past week was one such occassion and omorrow (Sunday) is another.

There are plenty of voices far smarter and more experienced than mine who will weigh in and I’m sending this note out now with little more than tip of the hat to all of them.

As was the case this past week, well, I remember where I was during the GFC(nothing great ‘bout it) and how it defined and changed lives as well as market structure.

I’m going to carry on with an abbreviated weekend note and get back to family and watching Coach Prime Time at ‘The Fort’…

And while the world debates who’s gonna win the coinflip like a bunch of degenerate gamblers on Fanduel or Draftkings, I’ll look TO the markets for some signal (to help rise above all the noise) …

5yy WEEKLY:

… overBOUGHT and THRU resistance …

First UP lets deal with a couple / few things items from the week just passed (in other words, a couple snarky ZH links which contain visuals and info graphics helping tell the tale of markets — INCLUDING rates — which you may / may not have already stumbled upon) …

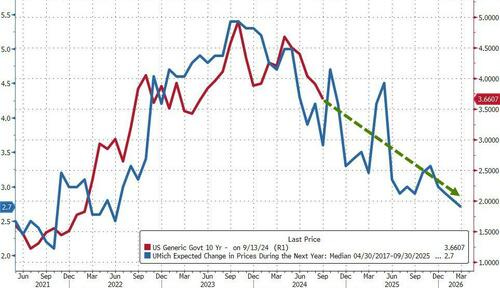

ZH: Inflation Expectations Rebound In September As Partisan Gaps In Sentiment Surge

… However, more notably, medium-term inflation expectations picked up (while short-dated expectations - which largely reflect oil prices - fell to their lowest since Dec 2020)...

...which suggests (on a lagged basis) that 10Y yields are going a lot lower...

… Ok I’ll move on AND right TO the reason many / most are here … some WEEKLY NARRATIVES — SOME of THE VIEWS you might be able to use — and which Global Wall Street (and, on occasion, other 3rd party sources) are selling HOPING for street cred and / or FLOW …

THIS WEEKEND, a few things which stood out to ME from the inbox … BMO booking profits in steepeners at target and stopped OUT short 2s, adding 2s30s steepener just the tip of the iceberg …

BARCAP: Federal Reserve Commentary: September FOMC preview: The time has come

With inflation muted and the labor market showing signs of cooling, we expect the FOMC to cut rates 25bp next week and the Summary of Economic Projections to show a total of 75bp in cuts this year and 125bp cuts in 2025. We retain our baseline projection of three 25bp cuts this year, with a risk of larger cuts.

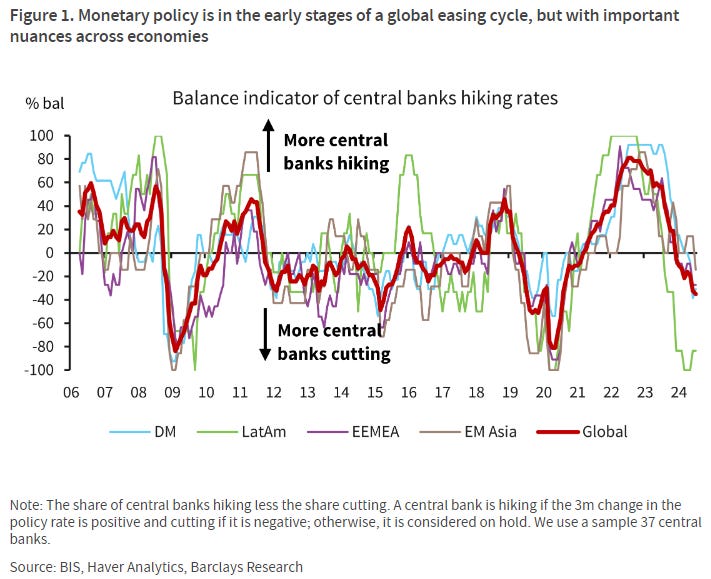

BARCAP Global Economics Weekly: Calibrating the cycle

It is easing season for monetary policy, with the Fed highly likely to join other central banks in reversing some of the steep post-pandemic hiking cycle. However, a closer look across regions shows the global cycle to be far from fully synchronised. Japan’s unique macro mechanics make the BoJ adjust its policy rates higher when its peers lower theirs; China’s occupation with exchange rate and domestic financial stability keeps it from lowering rates as much as the acute deflationary dynamics would otherwise dictate; and Brazil, to take one prominent EM example, is about to start hiking rates again next week, just as the Fed is only starting its cutting cycle (and having originally hiked much ahead of the Fed). Thus, the notion of a synchronous global easing cycle misses many nuances…

… As we grow increasingly concerned that we’ve underestimated the FOMC’s willingness to move aggressively during the early stages of cuts, we find ourselves nonetheless biased toward 25 bp. Albeit 25 bp and nervous. As for the longer run dot, it was recently nudged up to 2.75% from the prior 2.562% projection – leading us to assume that it will be stable for the time being. After all, constantly revising the longer run dot undermines the credibility of the guesstimate. The balance of the SEP will likely see growth and unemployment estimates moved up modestly, with inflation unchanged as the realized figures have printed more in line with the Fed’s target.

Taking a step back, our medium-term constructive outlook on the Treasury market has only been galvanized by the current price action and investors' discussion surrounding how far the Fed will need to cut this cycle. It strikes us that the US rates market is quickly concluding that the yield profile is more likely than not to return to prepandemic norms. An upward-sloping yield curve with 10-year rates comfortably below 4.0% will eventually prove the sustainable path for the Treasury market. 2s/10s managed to trade above 8 bp on Friday – marking the steepest the curve has been since July 2022..

DB CoTD: 25 or 50? What does DB's proprietary AI tool say?

… Matt and Shreyas Gopal from our FX team decided to put the WSJ article into DB Research’s new proprietary AI tool alongside that of the famous WSJ June 2022 article (see here) by the same author indicating that the Fed was leaning towards a 75bp hike, a hawkish surprise to markets. Although Matt’s view was that yesterday’s article had lower conviction than the one in 2022, we wanted to see if AI’s unbiased opinion about the level of conviction was the same.

See the piece here to find out what our AI tool told us about next week’s meeting given the new info. Its a fascinating use case for AI.

… In summary: The June 2022 article conveys a strong sense of urgency and conviction regarding the need for a significant rate hike to combat inflation. The September 2024 article, while discussing the possibility of a rate cut, presents a more balanced and less decisive outlook, reflecting the Fed's cautious approach in navigating economic uncertainty.

DB Investor Positioning and Flows - Near Neutral With A Defensive Tilt

ING: The Fed's set for a 25bp cut, but it's a close call

The US Fed has made it clear that monetary policy is going to be eased meaningfully from next week onwards. We had favoured a 50bp cut, but the latest job and inflation numbers suggest officials will more likely vote in favour of 25bp. Nonetheless, they will leave the door open to potentially more aggressive action down the line

ING: China's data dump shows that time is running out to achieve this year's growth target

Data largely came in weaker than already cautious forecasts, and with a less supportive base effect we will need to see a significant stimulus push to reach this year's growth target

MS: A Clarifying Cut Ahead | Global Macro Strategist

In the eyes of investors, the FOMC decision to cut 25 or 50bp, its explanation, and forward guidance will clarify how it thinks about the balance of risks to the economy. Investors will act on the perception of how Fed thinking compares to their own and move markets – providing clarity to all.

…Interest Rate Strategy

United States We suggest investors maintain UST 2s20s steepeners, as well as flatteners between the September FOMC OIS rate and November FOMC OIS rates. Our economists expect the median 2025 dot to fall 100bp to 3.125% from 4.125% in June. That decline compares to the market-implied trough rate falling 90bp over the same period, i.e., between the June FOMC meeting and today.

The downward adjustment to appropriate policy rates probably reflects the additional slowing in the US labor market and inflation since June – both factors that affected market prices. As such, it makes sense that the risk premium embedded into market prices looks similar to June.

We don't think that investors will take comfort in how our economists think Chair Powell is likely to communicate in the press conference – especially after having delivered a 25bp rate cut instead of a 50bp cut. These investors, many of whom think the economy is slowing more noticeably than the Fed appears to think, may shun risky assets – especially after their recent recovery.

A deterioration in the price of risky assets should help 2y Treasury yields decline from current levels. In addition, a steepening of the yield curve should accompany the decline in 2y yields…

MS: FOMC Preview: September Meeting | US Economics & Global Macro Strategy

The cycle begins with a 25bp cut and a stress on both sides of the dual mandate. The dot plot will have to change, but we do not expect Chair Powell to be firm on the size of future cuts. Our strategists maintain 2s20s steepeners.

Key expectations

The FOMC cuts the fed funds rate by 25bp to 5.125%. The FOMC statement acknowledges further progress on inflation and risks to the labor market. The Summary of Economic Projections (SEP) will likely show a shift to three cuts this year instead of one, marking-to-market for softer inflation and labor market data.

In the press conference, we do not expect Chair Powell to commit to a cadence for cuts, but to indicate that future decisions will be based on the data.

We look for three 25bp cuts total this year.

Our rates strategists suggest investors maintain UST 2s20s steepeners and maintain flatteners between the September FOMC OIS rate and November FOMC OIS rates.

Our FX strategists recommend short USD/JPY positions as the Fed starts its cutting cycle.

On the agency MBS side, our strategists remain neutral on the mortgage basis and prefer buying up-in-coupon conventionals.

The FOMC is widely expected to kick off the long-awaited easing cycle at its meeting next week. Looking ahead to the September 17-18 meeting, we see three key developments

Wells Fargo: Rate Cut Expectations Not Full Remedy for Consumer Sentiment

Consumer sentiment rose in early September amid prospects of lower rates in the year ahead. Yet uncertainty around the presidential election and slowing jobs market are holding back optimism. Not to mention, while inflation isn't as big of a problem as it once was, higher prices remain a challenge for consumers.

… Moving along and away FROM highly sought after and often paywalled and Global Wall Street narratives TO a few other things widely available and maybe as useful from the WWW … I’d NOTE

Questions on how restrictive Fed IS (APOLLO answer by one, not very…SpectraMarkets says VERY much so). Specs are MORE SHORT and nearly at a record clip AND, well … some links

Many FOMC members argue that the Fed funds rate at 5.5% is very restrictive because the Fed’s r-star model says that neutral monetary policy would mean a Fed funds rate at 3%.

But maybe this r-star estimate of the terminal Fed funds rate is wrong. At least that is what the incoming data suggests.

If monetary policy is very restrictive, why are default rates going down, see the first chart?

If monetary policy is very restrictive, why is the Atlanta Fed GDP Now estimate for third quarter GDP at 2.5%, well above the CBO’s estimate of long-run growth at 2%, see the second chart?

If monetary policy is very restrictive, why is weekly data for consumer spending still strong, see the third chart?

The bottom line is that the Fed funds rate at 5.5% does not seem very restrictive.

Our latest chart book with daily and weekly indicators is available here

Bloomberg: World Braces for Fed Easing Amid 36-Hour Rate Rollercoaster

Hedgopia CoT: Peek Into Future Through Futures, How Hedge Funds Are Positioned

There is quite a lot of chicanery this week as the market suddenly realized… Right around 10:55 a.m. NY on Wednesday… That the world isn’t ending because of a 0.1 topside miss on one of two pieces of the CPI reading.

Then Thursday things got REALLY interesting as Nick Timiraos (who is presumed by many to be the Fed’s not-so-secret rates whisperer) came out with an article detailing why the first cut is a coin toss, not a 25bp sure thing. The FT then followed with an article that looked like a GPT-4 remix of the WSJ article.

Line going lower = more rate cuts

The most interesting aspect of this, of course, is that it means next week’s meeting is in play. It’s 45/55 or something. Another titillating aspect is that it will offer us another clue as to whether or not the Fed is leaking analysis and information to the public in contravention of its own blackout policy which says:

During each blackout period, FOMC staff officers as well as staff who have knowledge of information that is related to the previous or upcoming FOMC meeting will refrain from expressing their views or providing analysis to members of the public about current or prospective monetary policy issues.

If the Fed ends up cutting 50bps, this will likely be perceived as another in a long series of unsavory rule-violating Fed stunts following hot on the heels of all the trading scandals and the most recent determination that yet another Fed Governor joined his peers in violating internal rules designed to safeguard the reputation and credibility of the Fed.

Then again, if the Fed goes 25bps, the last 24 hours will just be a strange dream.

May you live in interesting times.

You can make pretty good arguments for both 25 and 50 bps because Fed policy is incredibly tight relative to market pricing right now (cut 50!) but there is no emergency, and inflation is still above target (cut 25!).

Meanwhile, the current macro backdrop (2.5% growth, 2.5% inflation, trend jobs growth, minimal firing) makes it hard to get excited about recession. In fact, it’s beginning to look a lot like pre-COVID, everywhere you go…

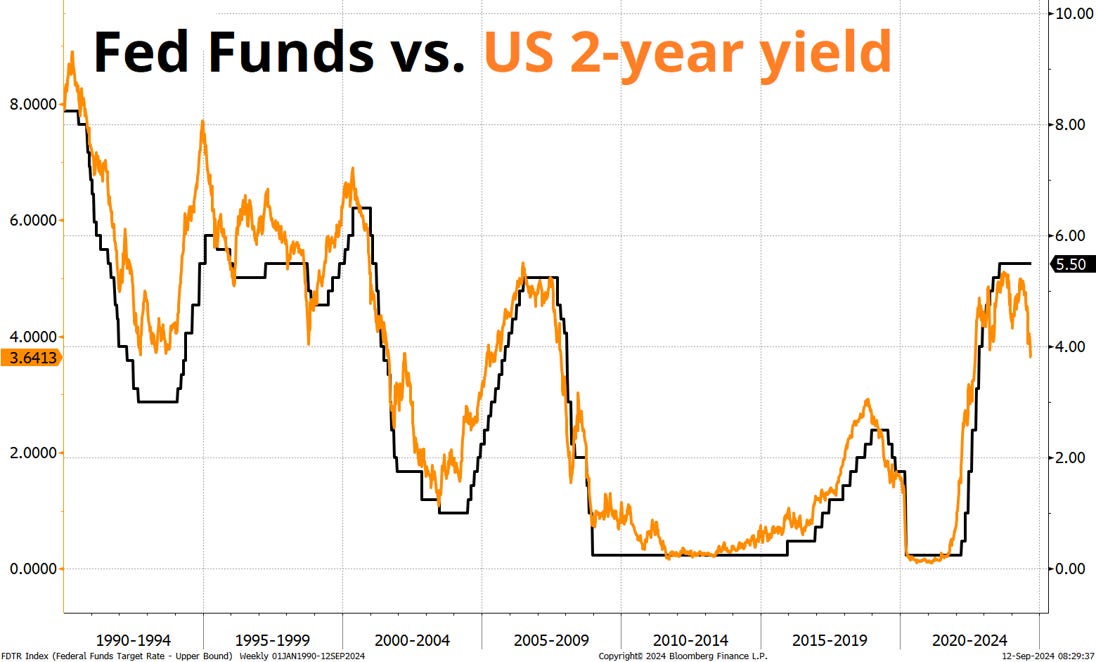

…To give you a sense of just how tight policy is right now, here is a chart.

Markets are not always right, but they usually lead the Fed as you can see in this next chart, which shows the two variables separately.

Note how the orange line usually moves before Fed Funds. But not always. As a rule, the market tells the Fed when to cut or hike. Note, though, that there is tremendous circularity because Fed communications influence the 2-year yield and… Bonds trade every day, whereas the FOMC only meet eight times per year. Anyway, the last time Fed Funds was this high above the 2-year yield, this guy was running things.

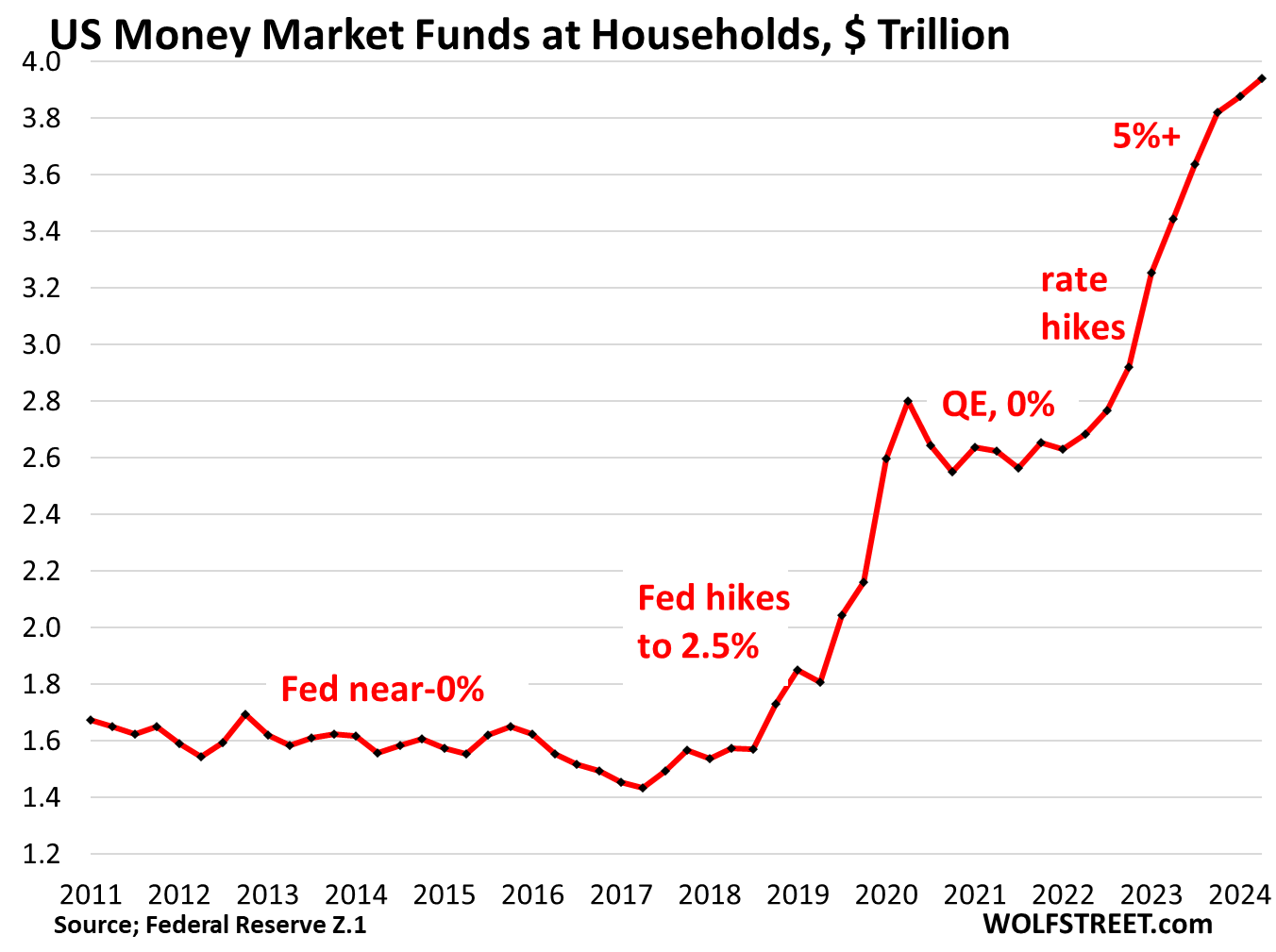

WolfST: Money Market Funds, Large CDs, Small CDs, and T-Bills: Americans and their Huge Piles of Interest-Earning Cash

Households’ money market fund & CD balances rise to a record $7.4 trillion; “savings” are far from depleted, they’re bigger than ever.

… AND for any / all (still)interested in trying to plan your trades and trade your plans in / around FUNduhMENTALs, here are a couple economic calendars and LINKS I used when I was closer to and IN ‘the game’.

First, this from the best in the strategy biz is a LINKthru TO this calendar,

America now has fewer employed workers, than it did a year ago

https://t.co/dho04OOC29