weekly observations (08.19.24): fade Harris trades; UST liquidity remains 'orderly'; stay in / with steepeners; REAL FF rates; econ FINE, spoos best week since Oct;

Good morning / afternoon / evening - please choose whichever one which best describes when ever it may be that YOU are stumbling across this weekends note…

FIRST up a quick look at a couple charts in effort to find something to focus on as this coming week will surely be all JPOW all the time with his speech at Jackson Hole slotted for Friday at 9am …

5yy DAILY: I’m watching 3.75% into the week ahead (speech Friday) …

5yy WEEKLY: while 3.75% remains important, my eyes drawn to bearish momentum (stochastics, bottom panel) …

… bearish momentum into a rate CUT ? what could possibly go wrong …

Moving along and TO Barrons who is out this weekend helping set the table for the week ahead…

… “At the front end of the yield curve, there’s almost no juice left, with [futures] pricing in more than four cuts this year,” says BlackRock’s Rieder. “There isn’t a lot of money left to be made there unless you really think the economy is going to slow dramatically, which I don’t.”…

… and from a quick look ahead, I’ll interrupt this weekends regularly scheduled programming and take a look back … perhaps we’ve gotta fire up the wayback machine for this here one …

Bloomberg: Henry Kaufman, 93, Looks Back on ‘The Day the Markets Roared The former Salomon Brothers economist known as “Dr. Doom” explains how his memo to portfolio managers ignited a huge rally on Aug. 17, 1982.

…NEXT UP lets deal with a couple / few things items from the week just passed (in other words, a couple snarky ZH links which contain visuals and info graphics helping tell the tale of markets — INCLUDING rates — which you may / may not have already stumbled upon) …

ZH: Housing Starts & Building Permits Plunged To COVID Lows In July

… This decline dragged both Starts and Permits to their lowest since the COVID lockdowns...

… Ok I’ll move on AND right TO the reason many / most are here … some WEEKLY NARRATIVES — SOME of THE VIEWS you might be able to use — and which Global Wall Street (and, on occasion, other 3rd party sources) are selling HOPING for street cred and / or FLOW …

THIS WEEKEND, here a few things which stood out to ME from the inbox …

Contrary to conventional wisdom and recent polling, we still believe the race is Trump’s to lose, though we consider it still premature to trade this election.

While the next administration’s policies remain very uncertain, three things are clear: there are no prospects for significant fiscal consolidation, Chinarelated policies will remain hawkish (though possibly less so under Trump), and industrial policies will continue.

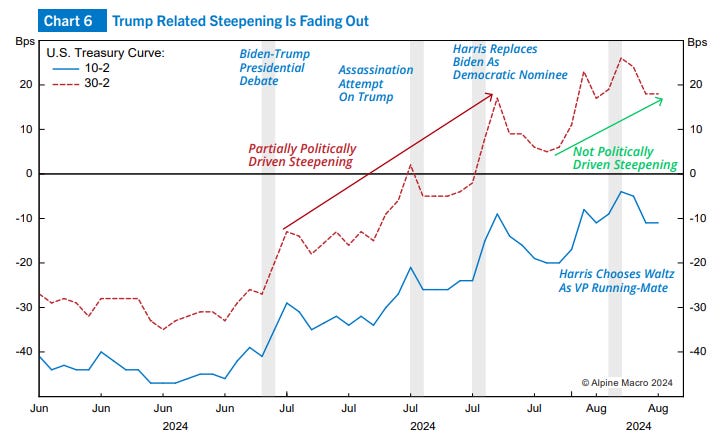

… we don't believe a Trump presidency would be particularly inflationary, despite such market fears. Chart 6 shows how the “Trump risk” is receding in U.S. Treasury markets, especially now, as Harris rises in the polls…

… The Price is Right: … investors to say global monetary policy most “restrictive” since Oct'08 (Chart 4) …

… Fiscal to Monetary: US national debt up >$1tn YTD to >$35tn; interest payment on debt $0.9tn past 12 months (13.4% of govt spend), and set to rise to $1.4tn by Jul'25 given debt dynamics if rates unchanged…even if Fed cuts 200bps interest payments rise to $1.2tn (Chart 5); reversal of fiscal impulse (US govt spend -5% YoY) + cost of debt = many Fed cuts-a-coming

In the US, inflation data have cleared the hurdle for the first cut at the upcoming FOMC, though the totality of the data still argue for a measured pace. In Europe, rates remain towards the bottom of their 2024 range, as worries around left-tail outcomes persist. In the UK, gilt supply for the rest of 2024 looks daunting…

… United States: Treasuries Treasury liquidity conditions remain orderly

Liquidity conditions and market functioning in the Treasury market have remained orderly in the latest risk-off move despite congested dealer balance sheets. There are no signs of major dislocations. Spline errors modestly increased but mostly at the front end and investors are exhibiting some preference for futures and CTD

… Modest increase in dislocations at the front end Figure 3 show the aggregate errors (RMSEs) to the Treasury spline. Barclays' measure shows that dislocations have increased but not as much as suggested by the Bloomberg index, which is distorted by the inclusion of high coupon seasoned 30y issues at the front end that are trading significantly rich on the spline (see here). Using our spline, dislocations have been uneven across maturity sectors ( Figure 4) and the increases are largely driven by securities at the front end under 3y sector, as well as the 20y sector (11-21y). In particular, the RMSEs in the 2-3y sector are elevated but have moderated in recent days. Crowded balance sheets and repo rate heaviness may be hindering participants from securing funding to arbitrage some of these dislocations.

BARCAP: Global Economics Weekly: A change in narrative As central bankers gather in Jackson Hole next week, the narrative for policy easing is building. Inflation is in retreat, evidenced by another benign US CPI print, and growth is slowing, albeit unevenly across regions. In the US, robust retail sales eased fears of collapsing demand, pointing to gradual rate cuts.

…US Outlook Premature burial Rate cut expectations moderated this week as retail sales greatly surpassed consensus expectations, underscoring a series of other data points that suggest that the resilience narrative is alive and well. Although this likely rules out aggressive cuts, July's inflation prints keep the FOMC on course for 25bp in September.

BMO: From Wyoming with Dove (hold 2s10s steepener, ‘bumpin stop down to -25bps and will add if dips below -20bps)

… The Jackson Hole Fed symposium will be the week’s policy focus. With the topic of “Reassessing the Effectiveness and Transmission of Monetary Policy,” it follows intuitively that the market is wary of a wholesale change in the Fed's approach to policymaking. This apprehension is compounded by the history of the forum being used to begin the conversation with the market about framework changes, etc. Our expectations are for Powell to more clearly signal that we’ll see a September cut and offer greater context for what the Fed envisions for the pace of forward rate reductions. The cooling inflationary trend lessens any urgency for the Fed to truly ‘reassess’ whether monetary is effective, although it would be a good opportunity for the Chair to open the discussion about ending QT before 2025…

…It goes without saying that Powell’s comments will provide the most current policy insight, even if the FOMC Minutes will be more detailed – at least as it relates to the collective wisdom of the Committee. We’ll be looking for any context as to how close the Fed was to cutting rates at the July 31st meeting and any skew regarding the magnitude of the first move. Investors will be seeking the same clarity from the Minutes that they hope Powell will provide, although we ultimately expect both events will lean heavily on the data-dependent state of policy with the backdrop of having finally reestablished price stability despite the Q1 bout of reflation. This is an ideal setup for the 10-year to continue consolidating in the 3.80% to 4.00% range and the 2s/10s curve to tick steeper – both of which we expect will define trading in US rates during the week ahead.

In the attached Weekly we discuss how the latest CPI data might play into the Fed’s pursuit of greater confidence that inflation is headed to the 2% target, we provide some thoughts on retail sales, jobless claims, and employment given the state employment breakdown and looking ahead to next week’s preliminary benchmark revision estimate for payrolls, and we highlight some new work by the New York Fed on judging the ampleness of bank reserves and how this informs on the Fed’s balance sheet reduction.

… There is clear evidence of continued disinflation in the July data, and we are particularly encouraged by three-month trimmed-mean CPI of 2.0%, six-month of 2.8%, and a 12-month trimmed-mean inflation rate of 3.3% (the lowest since August 2021).

DB: Outlining the cut strategy: how much action in Jackson?

With the Fed's annual gathering in Jackson Hole just a week away, we detail our expectations for Chair Powell's speech. We begin by framing the outlook for rate cuts around prescriptions from traditional policy rules. We then present arguments for our base case of 25bps cuts this year versus a more aggressive path starting with 50bps (see “Keeping the expansion alive with 75(bps) before ‘25”).

With the Fed’s decision on the pace of rate cuts data dependent, it will be difficult for Powell to pre-commit to a particular trajectory at Jackson Hole. Nonetheless, his comments could point to a few themes. First, there is a strong base case for a September cut. Second, with downside risks to the labor market, rate cuts are likely to be faster than a quarterly pace. Third, with rate cuts framed as dialing back restraint, it is unclear if rates will fall well below neutral. Fourth, with r-star uncertain and policy risks evident following the election, rate cuts beyond the first 75-125bps are more uncertain.

DB: Investor Positioning and Flows - Back Up To Moderately Overweight

After the abrupt cut to underweight last week, our measure of aggregate equity positioning bounced to turn moderately overweight again (z score 0.33, 63rd percentile), but is still well below the mid-July highs at the top of the historical band. Discretionary investor positioning (z score 0.63, 84th percentile) jumped sharply to fully recoup last week’s decline and is now well above average again. Systematic strategies positioning (z score 0.19, 50th percentile) also rose to modestly above average as volatility receded…

The sell-off in risky assets and rally in government bonds in early August was likely amplified by a notable deterioration in liquidity conditions, with both S&P and 10y UST market depth revisiting previous historical lows.

In terms of the price impact of volumes, or market width, the deterioration was particularly evident in Japanese equity, 10y JGB and yen futures.

What has the market’s reaction to economic news been telling us about investor positioning?

Despite the correction in risk assets, the financial conditions impulse remains supportive.

This year’s stablecoin expansion has been largely a reflection of the increase in total crypto market cap

… What about bond markets? Starting with market depth metrics, Figure 4Market dphon10y USTsand 10yBund ftresshows the market depth of 10y cash USTs and 10y Bund futures. It suggests that both markets saw a sharp deterioration in liquidity, with the diamonds showing the trough in daily observations on Aug 5th. For 10y USTs, over the past five years the level has only been lower than the Aug 5th observation of just over $40mn in March 2023 during the SVB crisis and in March 2020 during the pandemic. For 10y Bund futures, the deterioration was similarly sharp, though not quite to their lows over the past five years. That said, market depth has seen a notable recovery, with both Aug 12th and 13th at around $120mn for 10y USTs, only modestly below its average in the final week of July of just under $140mn.

MS: Did 'Sahm'-one Say Recession? | Global Macro Strategist (keep 2s20s steepener)

US economic data over the past two weeks calmed nerves about a possible recession – initially brought about by a triggering of the Sahm Rule and a partial unwind of yen carry trades. Defensive positioning offended instead of pleased, but we stay in UST curve steepeners into supply/Jackson Hole.

Trahan: Are The World’s Weak Links A Problem For U.S. Equities?

These last few weeks have been a wild ride for financial markets. Given the context, there is nothing super surprising going on, apart perhaps from the timing. Indeed, a peak in the fed funds rate typically starts with a Fed-relief rally (Q4’23/H1’24) and an eventual shift toward defensive leadership (Utilities in Q2). The latter is generally a sign that the clock is ticking for the equity market. The next step in the process is what we have seen this summer – a change in the correlation between stocks and bond yields. The positive correlation seen in the past month is a sign that “bad economic news is bad stock market news” once again.

Yes, it took a weak labor report to get investors to finally worry about the risk of a recession. Employment is the driving force behind S&P 500 earnings, so the last few weeks are the markets prepping for an eventual downturn in the economy as well as company top lines. The Fed should be easing policy shortly as the gradual unwind of the yield curve inversion suggests. The chart above illustrates very well that the yield curve does not begin to steepen again until labor markets start to fall apart. This is also when volatility moves higher and problems for equities intensify.

While there are clearly domestic issues confronting U.S. equities, the S&P 500 is essentially a global benchmark considering that about 30% of its companies' revenues are generated abroad. This week we review some global episodes that ended up being a problem for U.S. stocks. We also explore where some of the weak spots may be in the rest of the world. A U.S. slowdown, after all, could very well be the catalyst that exposes some of the at-risk countries. It’s a heavy topic for an August report, but it’s important considering the issues at hand…

Wells Fargo: Consumer Sentiment Rebounds Slightly as Inflation Cools

Summary Prices are still a problem for consumers, but as the rapid pace of inflation that was crushing sentiment a couple of years ago has given way to a much slower pace more closely in-line with the Fed's 2.0% target, sentiment is rebounding, if only incrementally.

…Interest Rate Watch: Fishing in Jackson Hole for Clues About the Fed Rate Path

… While not every speech by Fed Chairs at Jackson Hole makes waves, we see the potential for Powell's address this year to signal another important policy shift. The FOMC has held the fed funds rate at 5.25%–5.50%, its highest level since 2001, for more than a year now in an effort to corral decadeshigh inflation. Since the FOMC last adjusted its policy rate in July 2023, inflation has fallen significantly, even though it has not returned all the way back to the FOMC's 2% target. The core PCE deflator has declined from a year-over-year rate of 4.2% to 2.6% and is likely to remain near that 12-month pace through the end of the year by our estimates. As a result, there has been passive tightening in monetary policy over the past year when looking at the fed funds rate on an inflation-adjusted basis (chart).

…Powell may frame possible easing in terms of a risk-management approach to policy. With economic growth still strong and inflation not fully snuffed out, we would expect Powell to suggest that any easing at this juncture would be a dialing-back of policy restriction, with the policy setting normalizing alongside economic conditions. While his speech is likely to hint that a rate cut is coming as soon as the FOMC's next meeting, we expect him to stop short of offering any clues as to the size of a potential rate adjustment, since there is another month of employment and inflation data still to come before the Committee's September 17–18 meeting…

Wells Fargo: July's Downtrend in Hiring Evident in State Labor Markets Job Gains Take a Step Back and Unemployment Rates Pick Up Across States

Moving along and away FROM highly sought after and often paywalled and Global Wall Street narratives TO a few other things widely available and maybe as useful from the WWW

Looking at the latest daily and weekly data shows that retail sales are strong, jobless claims are falling, restaurant bookings are strong, air travel is strong, hotel occupancy rates are high, bank credit growth is accelerating, bankruptcy filings are trending lower, credit card spending is solid, and Broadway show attendance and box office grosses are strong. The Atlanta Fed’s GDP Now estimate for third quarter GDP is 2.4%, and the Dallas Fed weekly GDP indicator is 2.3%. Finally, we added a new chart with state-level GDP for New York, California, and Texas, which also shows continued strength, see below. The bottom line is that there are no signs of a recession in the incoming data, see also our chart book with daily and weekly data available here.

at Barchart

S&P 500 $SPX just had its best week since Halloween

WolfST: A Big Week for Stocks, a Huge 7 Days for Nvidia (+26%), after the Battering They’d Taken

Much of the heavy lifting of these mindboggling amounts was done in two trading days.

ZH: Harris Unveils Plan To Fix Last 4 Years Of Economic Destruction

… AND for any / all (still)interested in trying to plan your trades and trade your plans in / around FUNduhMENTALs, here are a couple economic calendars and LINKS I used when I was closer to and IN ‘the game’.

First, this from the best in the strategy biz is a LINKthru TO this calendar,

Being Old School, it's rather remarkable how quickly Stonk markets & VIX recovered SO quickly. No stimulus provided. Can Hopes of (BIG) Cuts really do all that?

Being Old School, it's rather remarkable how quickly Stonk markets & VIX recovered SO quickly. No stimulus provided. Can Hopes of (BIG) Cuts really do all that?