weekly observations (08.05.24): it's the end of the world as we know it ... "Got that Sahm-ertime Sadness" -DB; 'change of call' (pretty much everyone)

Good morning / afternoon / evening - please choose whichever one which best describes when ever it may be that YOU are stumbling across this weekends note…

NFP - sky is officially falling!! Team Rate CUT for the absolute DUB …

Steepening fans, take a victory lap (yes, even if you claimed ‘trade of the year in 2022 and 2023 and most of 2024 … even stopped clock right 2x a day!!)

#GotBONDS, steepeners? If NOT, oh well, too late because …

Ok … I’m saying this and realizing full-well that i’ve nothing less than healthy dose of skepticism (please see below for Apollo’s latest and a reminder that things are … “Slowing, but Still a Soft Landing” ) — but the data Thursday + Friday = overwhelmingly support Team Rate CUTs and their aspirations … they did in fact, ‘told us so’ !!

AND … I’ll begin with some bullets / links in effort to contextualize the downside SURPRISE and SAHM RULE TRIGGER!!

But wait, there was apparently MORE (or less, depending on yer view …) Downward REVISIONS … let the inter-meeting CUT talks CONTINUE (didn’t know they were taking place until just ahead of the data and surely that print, well, will inspire MORE …) and so …

CalculatedRISK: July Employment Report: 114 thousand Jobs, 4.3% Unemployment Rate

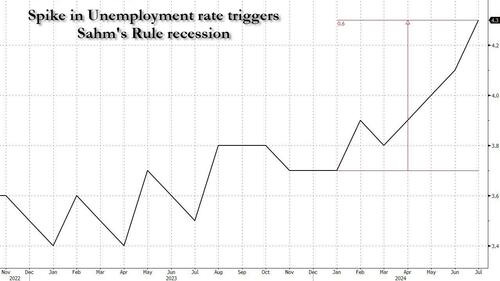

ZH: Recession Triggered: Payrolls Miss Huge, Up Just 114K As Soaring Unemployment Rate Activates "Sahm Rule" Recession

… The rule, for those who don't remember is that a recession is effectively already underway if the unemployment rate (based on a three-month moving average) rises by half a percentage point from its low of the past year. And that's what just happened, with the unemployment rate surging 0.6% from the year's low.

ZH: Stocks, Crude, & Bond Yields Plunge As 'Growth Scare' Sparks Surge In Rate-Cut Hopes

… This morning's payrolls data was 'bad news' and so we see rate-cut expectations explode higher with over four full cuts now priced in for 2024...

ZH: Wall Street Begs Fed To Panic: Goldman Sees 3 Consecutive Rate Cuts, JPM Hopes Two For 50bps, Citi Even Crazier

NEXT UP lets deal with a couple / few things items from the week just passed (in other words, a couple snarky ZH links which contain visuals and info graphics helping tell the tale of markets — INCLUDING rates — which you may / may not have already stumbled upon) …

Clearly, we’ve got some NFP recapping and victory lapping (later on, courtesy of Global Wall) to do … but first, a visual as you contemplate the week that was and the one that will be AND set on your journey to plan your trades and TRADE your plans …

2yy WEEKLY

I’ll let YOU make as much or as little of this past weeks 50bps DECLINE in yields and near certainty of a 50bps rate CUT in September … and beyond (and / or perhaps sooner)?

… Now in as far as some OTHER of what is driving the ever shifting narrative landscape …

ZH: 'Growth Scare' Narrative Builds As US Factory Orders Plunge Most Since COVID Lockdowns In June

… Ok I’ll move on AND right TO the reason many / most are here … some WEEKLY NARRATIVES — SOME of THE VIEWS you might be able to use — and which Global Wall Street (and, on occasion, other 3rd party sources) are selling HOPING for street cred and / or FLOW …

THIS WEEKEND, here a few things which stood out to ME from the inbox … one LARGE part NFP related and, well, another part just stuff to help pass the weekend AND week ahead which looks to ME to be nearly VOID of tradeable funDUHmental data … and so, without further adieu … when the facts change, Global Walls narrative shape shifts once again … note JPMs newly minted and LOWER yield f’casts and …

… Rates: No Fed pushback = stop ins US: Intermediate tenors likely to lead rate decline as first Fed cut nears. UST bill shift => coupon delay; 5s30s 50+bps steep likely needs slowdown

… Bottom line: July FOMC or UST refunding doesn’t change core views: belly rates likely to lead declines as first Fed cut nears and bill shift isn’t game changer for 30Y spread short. On the curve, it will likely take sharp econ slowdown for 50bps+ in 5s30s.

… Technicals: US10Y yield death cross, US election seasonals US 10Y yield hit by the death cross, or 50d SMA crossing below 200d SMA, and this supports our bullish H2 bias. US election year seasonals a risk to our view.

… Tale of the Tape: central banks cutting fastest pace since Aug’20 (Chart 4), BofA says 56 global cuts in H2'24 …

… The Biggest Picture: July US ISM weak (46.8); only other period ISM <50 for long time without negative payroll was Sep’84-Apr’86 (overvalued US dollar – Chart 2); July payrolls >200k…consensus stays "soft landing" but <125k & 10yr yield heading to 3.5%.

Nonfarm payroll growth slowed to 114k amid broad-based softness, alongside an increase in the unemployment rate and smaller workweek. Although hurricane effects were likely behind the payroll softness, we think strong labor supply poses upside risks to the unemployment rate. We now expect three 25bp Fed cuts in 2024.

BARCAP: Global Economics Weekly Ready, set... slow

The global economy is showing signs of slowing, with manufacturing weakening and the US labour market cooling. The Fed held, but is now likely to conduct three 25bp cuts by year-end; the BoE delivered its first cut and looks to go again in November. The BoJ surprised with a hike, with the yen and real rates on their mind.

… US Outlook Weather or not July's employment report showed broad-based softness, with payroll employment slowing and the unemployment rate jumping to 4.3%. Although we think that a hurricane was likely behind payroll softness, we now think strong labor supply will push up the unemployment rate. We also recalibrate to show three 25bp Fed cuts in 2024.

BMO: NFP Disappoints, UNR 4.3% - Sahm Rule triggered as 2s/10s hit -5.6 bp

… Treasuries were rallying into the event and the proverbial bar was high for an additional move to lower rates and that is precisely what payrolls provided. 10- year yields dropped to 3.786% and 2s got as low as 3.84%. The bull steepening has extended with 2s/10s reaching -5.6 bp. From here, there is little to suggest this move should be reversed and we expect it has further room to run

BMO: Goldilocks has Left the Building (booked profits long 5s, looking to get into 2s10s steepener around -15bps)

… It’s with this backdrop that we are unwilling to push back against the price action until we’ve seen a more durable period of relative stability. Wholesale repricing moves such as what was seen on Friday aren’t often limited to a single session. Therefore, as the week ahead unfolds, we anticipate that the curve steepening momentum that was clearly one of the biggest takeaways from the July employment data will extend further. We’re targeting a return of the 2s/10s curve into positive territory by the end of the week. The underlying logic is two-fold. First, the rise in the Unemployment Rate has created more downside risk for policy rates – both this year and for 2025 (and beyond). Second, the refunding auctions still need to be underwritten and given the light data calendar, supply will be the main event. Moreover, a 2s/10s curve at -5.6 bp on Friday is a lot closer to positive territory than the local lows of -27 bp…

A sizable deceleration in payrolls and the fourth consecutive increase in the unemployment rate (which triggered the Sahm Rule) point to broadening signs of weakness, we think, particularly with lack of explicit impact from Hurricane Beryl, according to the BLS.

Notable were a 0.2pp increase in the new layoffs-driven U-2 measure of unemployment, a jump in the number of people working part-time for economic reasons and a sharp decline in the breadth of job creation.

The totality of the labor market data suggests we are entering a more uncomfortable zone for the Fed in terms of its labor market mandate.

In our view, the report highlights the risk of a steeper set of reductions in the policy rate this year than we had envisioned prior to Friday’s data. Still, we think the Fed would need to see another soft print in August data before it considers starting the cycle with a larger 50bp rate cut in September.

BNP DM rates: Extending targets on long US trades (extend and pretend? don’t book profits and re-enter some trades? okie dokie)

We entered into a combination of trades over the past few months to express our structural view that risks to US rates are asymmetrically skewed to the downside as inflation data has been decelerating quickly and the labor market is rebalancing. These trades include a cross-Atlantic trade (long 10y SOFR swap, short 10y ESTR swap), 5s30s UST steepeners, and 3m5y A/A-30bp receiver spreads.

On Friday, July NFP posted a substantial downside surprise that saw weakness across all sectors and metrics, with the unemployment rate triggering the Sahm Rule. This induced a sharp bull steepening of the US yield curve that now has markets pricing the potential for a 50bp rate cut in September and terminal rates closer to 3%.

With deeper rate cuts in the US now appearing more plausible, we hold our 3m5y A/A-30 receiver spread and extend our targets/raise our stops for our cross-Atlantic trade and 5s30s UST steepener.

Long 10y US SOFR versus short EUR 10y ESTR: Entry: 125.7bp. New target: 85bp. New stop: 120bp. 1m carry and roll: -0.2bp. Current level: 107bp. Risk: 15k/bp.

5s30s UST steepener: Entry: 28.25bp. New target: 75bp. New stop: 35bp. 1m carry and roll: -2.7bp. Current: 47bp. Risk: 20k/bp.

DB: US Economic Chartbook - Got that Sahm-ertime Sadness

The July employment report was uniformly weak with headline (114k vs. 179k previously) and private (97k vs. 139k) payroll gains well below their three-month averages (170k and 146k, respectively) and the unemployment rate rising by a couple of tenths to 4.3%. Indeed, the latest uptick in the unemployment rate has now technically reached the “Sahm rule” threshold – defined as a 0.5 percentage point rise in the 3-month average of the U-3 rate from its lowest level over the prior 12 months. In addition, both average hourly earnings (+0.2% vs. +0.3%) and hours worked (34.2 vs. 34.3) slipped, resulting in the year-over-year growth rate of the payroll proxy for compensation falling by 20bps to 4.9% – the lowest since January 2024. The breadth of hiring was also notably soft with the 1-month diffusion index of private payrolls falling to 49.6% – the lowest since the pandemic.

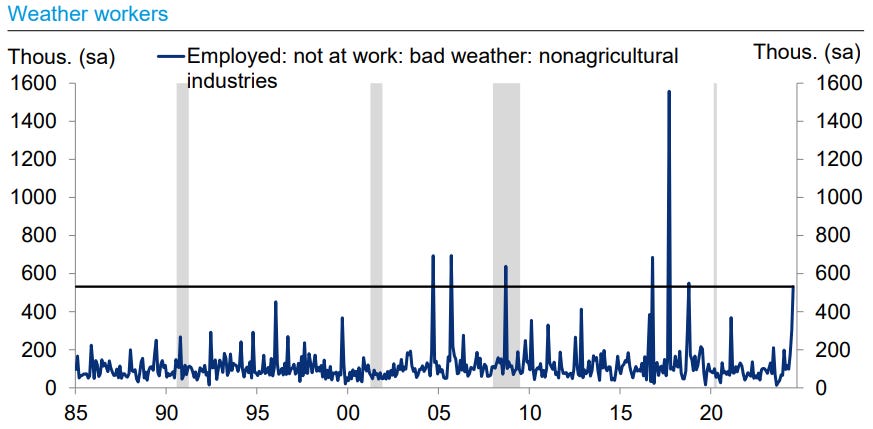

To be sure, there are reasons to question the degree of weakness in the report given evidence of potential weather disruptions from Hurricane Beryl. Recall that Beryl caused substantial flooding in Houston – the 4th largest city in the U.S. – during the survey periods for both the establishment and household surveys. Case in point, the number of nonagricultural workers in the household survey that reported that they were not at work due to “bad weather” jumped to 436k (non-seasonally adjusted) – the largest for any July on record. Additionally, the jump in the unemployment rate was largely due to a 31% month-over-month increase (249k) rise in those workers stating that they were “on temporary layoff” – the largest in percentage terms since the pandemic. While it is difficult to quantify the degree to which the hurricane may have impacted nonfarm payrolls in the establishment survey, prior spikes in July “weather workers” that were less than half the magnitude of what was seen this year were accompanied by nonfarm payroll prints notably below their prior six-month averages – namely, July 2019 and 2012.

As we have highlighted for some time, strong payroll gains in the first half of the year were more a function of a still historically low layoff rate as opposed to strong hiring – a trend confirmed in the June JOLTS data. That being said, today’s employment data likely overstate the degree of recent cooling in the labor market given the potential weather disruptions. Hence, we continue to expect three 25bps rate cuts this year starting at the September meeting (see “Keeping the expansion alive with 75(bps) before ‘25”). While risks of more aggressive easing – starting with 50bps in September – have undoubtedly increased, Fed officials are unlikely to over-react to one data point, a point made forcefully by Chicago Fed President Goolsbee in an interview after the release of the jobs report. The onus will be on the August data to confirm whether or not the labor market is experiencing a “further unwanted material cooling” that Chair Powell mentioned in his post-meeting press conference earlier in the week (see “July FOMC recap: Just a little bit more”).

… However, there is evidence that bad weather may have impacted the July labor data

DB: Investor Positioning and Flows - Sliding Further (positioning sliding further … watching …)

Last week we noted that equity positioning had pulled back sharply but was still elevated, and risk appetite in our reading remained high, suggesting buy-the-dip rallies but also larger pullbacks if hitherto missing negative catalysts emerged (Sharp Pullback But Not There Yet, Jul 26 2024). The market selloff in response to the weak payrolls report is not surprising in this context. Equity positioning has continued to slide (z score 0.48, 72nd percentile), especially with systematic strategies cutting exposure as vol spiked higher. While not low in absolute terms, positioning has now caught down to earnings growth which as we note in our takes piece published earlier today, moderated slightly from 11.5% in Q1 to a still solid 10.7% in Q2 (Q2 2024 Earnings Takes: Modest Deceleration, Slow Rotation, Aug 2 2024). Inflows to equity funds ($8.9bn) continued for a 15th straight week but at a somewhat slower pace, while strong inflows into bond funds ($14.6bn) persisted.

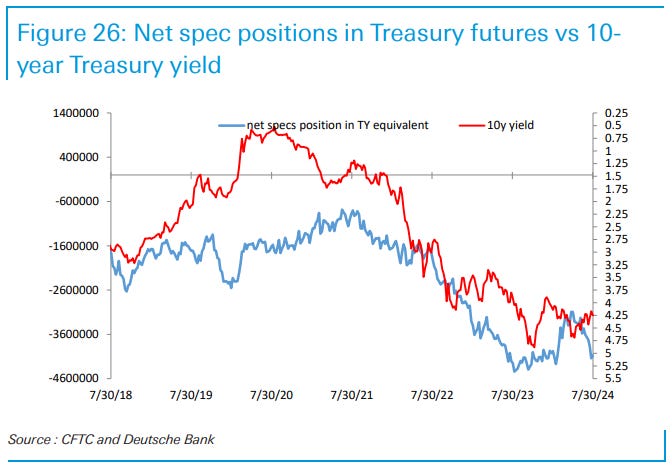

Interest Rates: Speculators were bearish in Treasury futures, extending their net short positions by 134K contracts in TY equivalents over the week prior to July 30 (Tuesday).

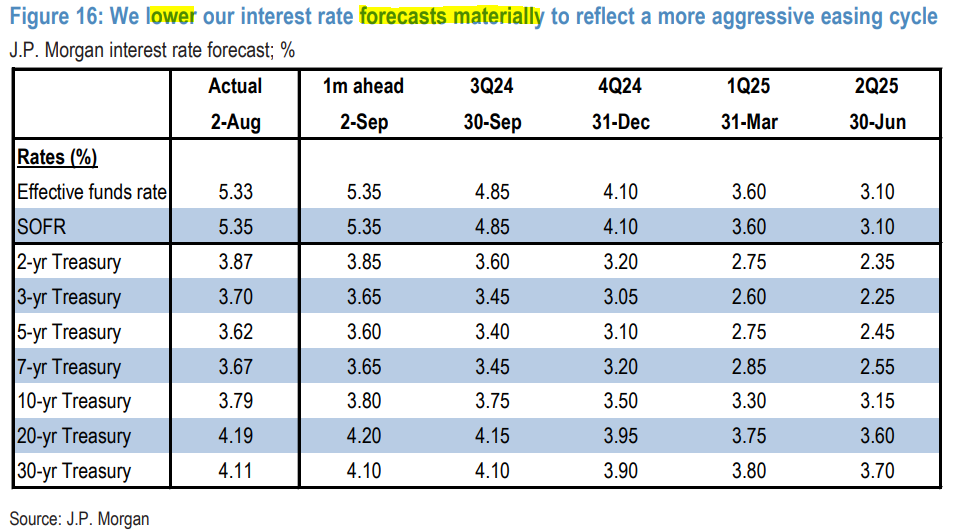

JPM: U.S. Fixed Income Markets Weekly (updated and LOWER yield f’casts … marking TO market …)

…Treasuries Far from the shallow (easing cycle) now?

Treasury yields dropped to their lowest levels since the end of last year amid evidence of a sharp weakening in the labor market and a dovish Fed. We now expect 50bp cuts at both the September and November meetings, followed by 25bp cuts at every meeting thereafter

We see reasons for wanting to chase this rally, given Fed easing cyclicals and the risk of an intermeeting ease. However, we stay neutral duration for now, given the magnitude of the recent rally, the lack of near-term catalysts, and the fact that intermeeting eases are uncommon historically

We continued to hold 5s/30s as a more strategic representation of our bullish view. The curve has begun to line up with other easing cycles, its carry profile is less punitive than outright longs, a more aggressive easing cycle supports a larger steepening of the long end, and we continue to think supply-demand dynamics support higher term premium

We see growing risks for a more significant front end steepening and believe 2s/5s steepeners will offer value, especially as we get closer to September, but will remain patient

We revise our interest rate forecast lower to reflect a more aggressive easing cycle: we lower our year-end 10-year Treasury yield forecast by 65bp to 3.50% and our 2-year forecast by 110bp to 3.20% …

… Separately, we make revisions to our interest rate forecast to reflect the more aggressive Fed easing cycle (Figure 16We lowruintes rafocts maerily toefcamr gesivan cyle). We expect yields to decline in the months ahead and into year-end: we lower our year-end 10-year Treasury yield forecast by 65bp to 3.50% and our 2-year forecast by 110bp to 3.20%.

The US employment report for July caused a free fall in equity prices, bond yields, and the USD. While price action looks dramatic, we advise against fading it until expectations stabilize.

Global Macro Strategy We discuss the importance of central bank communications to macro markets in this next period where economic data may disappoint more than appease. We also discuss how the combination of market dynamics – risk off, but well-behaved EM local markets – is unlikely to last for much longer.

Interest Rate Strategy We maintain UST 2s20s steepeners and Sep/Nov FOMC OIS flatteners. We enter ECB Sep/Oct OIS steepeners and maintain ERZ5ERZ6 flatteners, short 10y BTP/Bund, and long ERZ4 96.625/96.875/97.125 call fly. We close Sep '24–Feb '25 MPC and pay 5s10s30s SONIA fly, while keeping long SFIZ4 95.40-55-70 call fly, 10s30s gilt flattener, and short 15y ASW. We shift from JGB 5s20s flattener to long 20y JGB vs. pay 2y OIS. We maintain SOFR/TONA basis pay 5y on 2s5s20s fly and long 5s10s ASW box flattener…

With the cutting cycle set to start in September as expected, the pace of further cuts is now the debate. Markets are pricing more than one cut in September after today's weak NFP print, but to contemplate a 50bp cut, the Fed needs more data to separate signal from noise.

… Bottom line: U.S. labour market started the third quarter with a downside surprise. The July data also marked a clear deceleration in labour market conditions that had been gradually unfolding through the past year. The unemployment rate rose to 3.9% in April from 3.4% in the April of 2023, and then rose to 4.3% within the span of three months. In the press conference for the Fed meeting this week, Powell continued to characterize ongoing labour market weakening as conditions normalizing from being overheated. He did stress that the Fed will be ready to respond “if labour market were to weaken unexpectedly.” We continue to expect the Fed will cut interest rate at the next meeting in September, and see risks tilting towards more cuts than less for the rest of this year.

UBS - US economy: Softer data opens door to more rapid rate cuts

We maintain our view that the US economy is headed for a soft landing.

Recent data on both inflation and the labor market has surprised to the downside.

We now expect the Fed to cut rates by 100 bps by year-end.

Wells Fargo: July Employment: That Was Sahm Jobs Reports

Summary The ongoing deterioration in the jobs market was on full display in the July Employment report. Nonfarm payrolls posted the second smallest gain in 3.5 years with an increase of 114K, average hourly earnings growth eased to 3.6% year-over-year and the unemployment rate jumped to 4.3% from 4.1% in June. The landfall of Hurricane Beryl at the start of the survey week looks to have had no significant impact on the change in payrolls or the increase in the unemployment rate.

The increase in the unemployment rate now puts it over the 0.5 point Sahm Rule threshold that has historically been associated with the economy being in a recession. The rise in unemployment due to labor force entrants over the past year suggests the current increase may not be the sure-fire sign of a downturn it has been in the past. However, the significant rise in job losers over the past year underscores genuine weakening in labor market conditions that are quickly raising the risk of recession. We expect the Fed to begin reducing its policy rate in September as a result, with the possibility of a 50 bps cut at least on the table after today's report.

… Interest Rate Watch: Open Door to a September Cut, Where Have I Heard That? This week's Fed meeting noted progress on inflation and opened the door to a rate cut in September. Why does this sound so familiar?

Yardeni: Beryling Toward Rate Cuts (NOT hard-lander … worth a read, good stuff here …)

Some macroeconomic storm clouds are brewing. Markets are fleeing for shelter in Treasuries, leaving behind almost everything else, including their prized LargeCap tech stocks and recently acquired SMidCaps. Here's the market action as of midday:

The Nasdaq officially entered a correction, down more than 10% from its record high reached roughly a month ago.

The CBOE Volatility Index (VIX) popped to 29, which hasn’t been seen since mini regional banking panic in March 2023.

The 2-year US Treasury is down roughly 25 basis points to 3.9%. Investors are worried the Fed is behind the curve on cutting interest rates, risking a policy error. Odds of a 50 basis point cut to the federal funds rate (FFR) versus a 25 bps cut are now 2:1 in September.

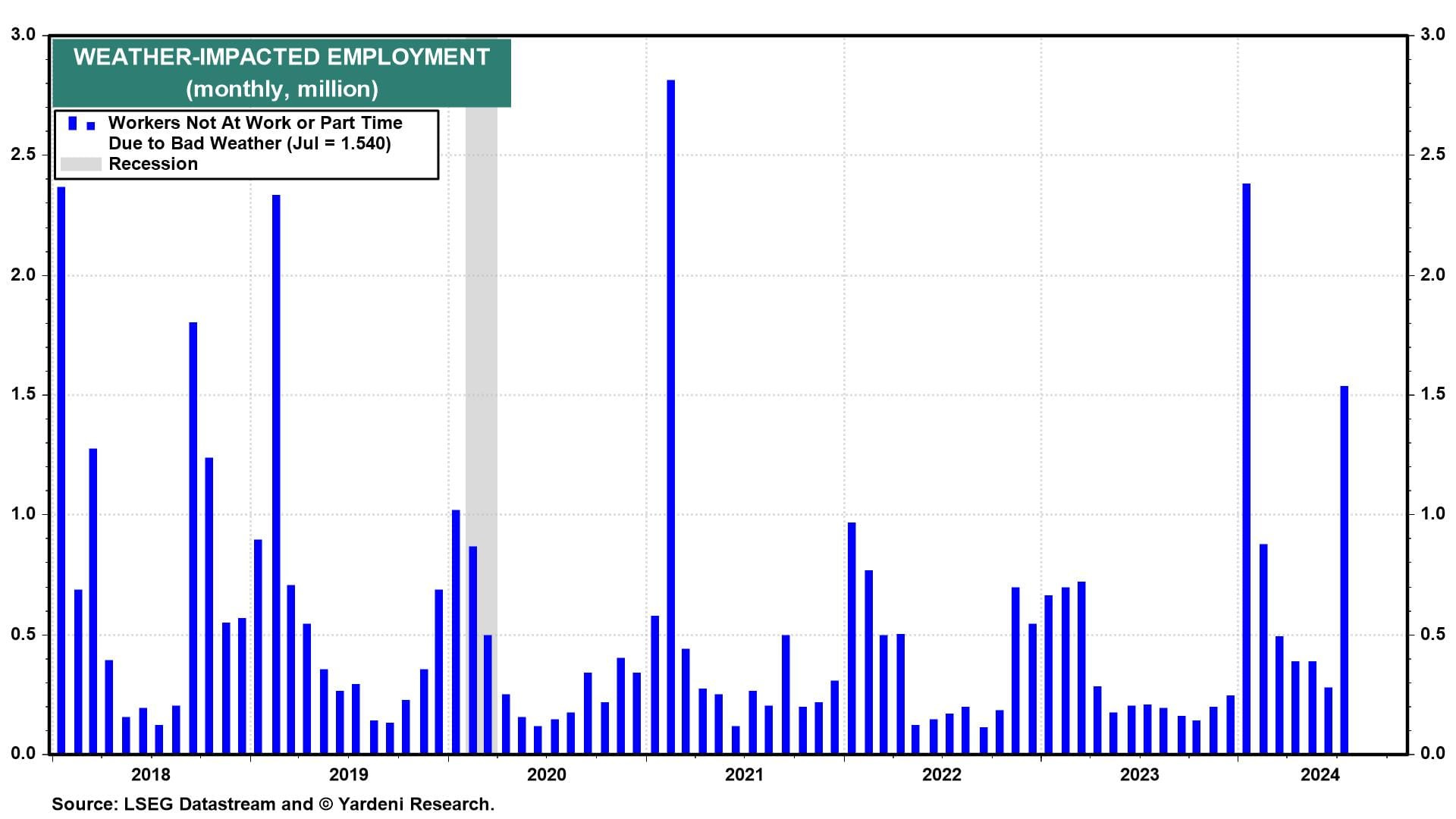

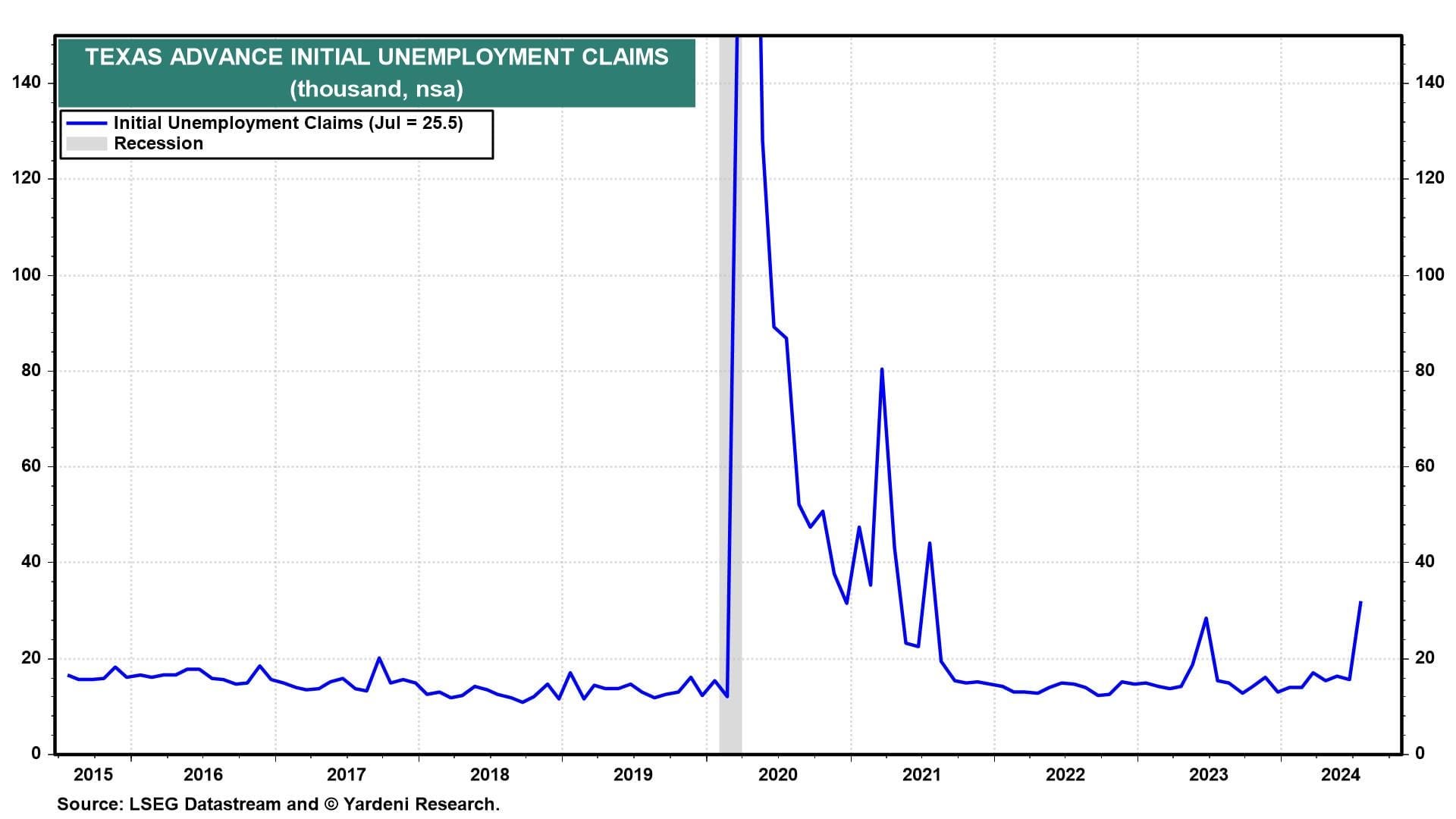

We hate to spoil the party for the diehard hard-landers, but we won't be joining them after today's July employment report. We blame much of the weakness on the weather. Yes, we know, the Bureau of Labor Statistics (BLS) noted that Hurricane Beryl had no impact on the report. Yet, the BLS household employment survey showed that 1.54 million workers were either not working or only part time due to weather, far above the historical average (chart).

… Many of these temporary layoffs showed up in the initial unemployment claims in Texas (chart). We expect both series to revert lower in August.

Finally, the party for the recession cheering squad started yesterday when July’s M-PMI came in at 46.8, much lower than expected. It was led by a sharp drop in the M-PMI’s employment component. Yet, today’s report showed that manufacturing employment edged higher. Go figure! …

… Moving along and away FROM highly sought after and often paywalled and Global Wall Street narratives TO a few other things widely available and maybe as useful from the WWW

AllStarCharts: Bonds are Back (wait, what? they ever left?)

US Treasuries are sticking a bullish reversal – an admirable feat following an unforgettable selloff.

If you aren’t buying bonds yet, it’s time to reconsider.

Here’s the US T-Bond ETF $TLT trading above a rising 200-day moving average as it violates a multi-year downtrend line:

These are the early signs of a trend reversal.

Now, bond bulls want to witness the 14-week RSI post fresh multi-year highs. (We may see such a print following today’s action.)

Heading into the close, the 30-year T-bond is registering its largest one-week rate of change since spring 2020. And on a more tactical time frame, the 14-day RSI is reaching overbought conditions.

Both data points suggest an initiation thrust, supporting further upside for US treasuries – a move that could last weeks or even months.

But who knows how long this bond will rally? I’m guessing months, maybe quarters, but not years.

The soft July employment report is inconsistent with the hard data for economic activity, see charts below and our chart book. There are no signs of a slowdown in restaurant bookings, TSA air travel data, tax withholdings, retail sales, hotel demand, bank lending, Broadway show attendance, and weekly box office grosses. Combined with GDP in the second quarter coming in at 2.8%, the bottom line is that the current state of the economy can be described as slowing, but still a soft landing.

BESPOKE

Seven-day streaks of falling 10-year yields aren't uncommon, but if the current streak stretches into next week, that's another story.

Bonds vs. stocks. $agg relative to $spy. Big move this week. For passive portfolios that haven't rebalanced for a long time, looks like the market took care of some of the work

The Takeaway: Bonds broke out to new 52-week highs, while Stocks sold off for the third straight week. The 60/40 portfolio is working again, but there's nothing bullish about this flight to safety.

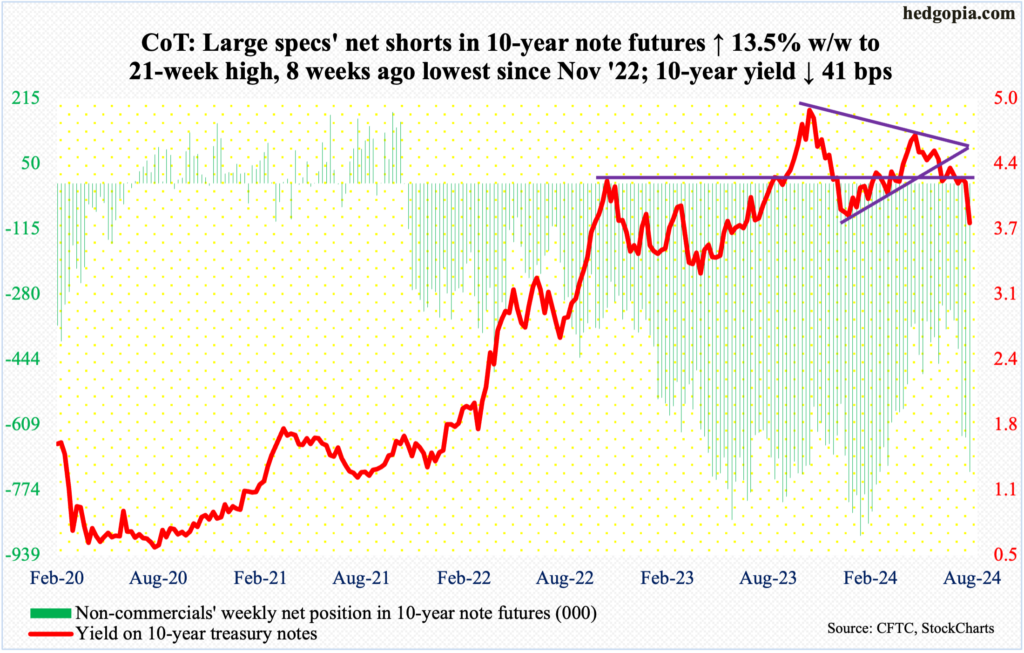

HedgopiaCoT: Peek Into Future Through Futures, How Hedge Funds Are Positioned (MORE SHORT 10s)

RIA Advice: Inversion Of Yield Curve Finally Reversing

Fed or no Fed, people suddenly notice fundamentals again, a scary thing at this altitude.

… AND for any / all (still)interested in trying to plan your trades and trade your plans in / around FUNduhMENTALs, here are a couple economic calendars and LINKS I used when I was closer to and IN ‘the game’.

First, this from the best in the strategy biz is a LINKthru TO this calendar,

{kind=link}

REM : It's The End Of The World As We Know It (And I Feel Fine) (Remastered 2006)

https://youtu.be/8OyBtMPqpNY?si=6zOvonfsiytrEzl

Turn it up...........

LOVE IT !!!!!!!!!!!!!!!!!!

September should be Spicey at this rate :)