weekly observations (07.21.25): 5y5y; stablecoin BID for bonds; "We capitulate on last month’s constructive view on UST", S&P golden cross = HIGHER 10yy (BAML); stopped OUT 5s, re buy (MS)

Good morning / afternoon / evening - please choose whichever one which best describes when ever it may be that YOU are stumbling across this weekends shorter than short note…

Friday I offered a look at 10yr BREAKS breakin and today — dunno why — feelin a 5y5y fwd vibe …

… for more on the differences, I trust you can also head over TO ChatGPTon yer very own … See what you wanna see and IF there is to be a time to technically fade ‘flation data, now, with momentum extended and TLINE coming into play, would seem to be as good a time as any.

There are, as always, compelling cases for the ‘flation to continue — math, YoY comps, PPI feeding into PCE into H2 — reasons to believe that, tariffs aside, might NOT cooperate and looking at a chart like the one above, can be read BOTH ways.

I’ve marked significant troughs and what IF ‘Liberation Day’ was another such trough? We could be headed back up North of 2.50%…

I’m no longer in a seat where I have to have or feel compelled to offer a guess.

It would seem to ME to be worth sitting that dance out right ‘bout now and lean on Global Wall and other experts because, as you will see below …

… Meanwhile, 10-year yields continue to bore… -Brent Donnelly

… And I’ll quit while I’m behind and move right along. Before I head TO Global Wall recaps, a couple of Friday data inputs …

ZH: Renter Nation Returns: Surge In Multi-Family Unit Starts & Permits Saves US Housing Market

ZH: UMich Sentiment Surges Higher As Inflation Expectations Plunge

… Most notably, inflation expectations tumbled from 5.0% to 4.4% (1Y) and from 4.0% to 3.6% (5-10Y)...

And the same picture emerges on the longer-term expectations.

… and yes, I’m done.

HIMCo’s latest yet to drop and so …

I’ll move on TO some of Global Walls WEEKLY narratives — SOME of THE VIEWS you might be able to use. A few things which stood out to ME this weekend from the inbox

THE bank of the land seems to have ‘capitulated’ and when I see this — even though a couple days old — I pause, read, share …

17 July 2025 BAML: The Fixed Income Digest Overweight high yield credit; underweight duration, UST

…UST, duration: high return volatility = underweight We capitulate on last month’s constructive view on UST and duration and recommend an underweight. Bond rally potential remains, but our baseline view is 10y yield (4.45%) remains range bound between 4.25%-4.75%. However, after yet another month of yield whipsaw (high return volatility), we think underweight allocation to duration and quality bonds in UST and muni’s makes most sense. If income alone is the objective, we think money market or floating rate assets continue to look relatively attractive: they provide comparable income potential to long duration exposures and does so without the return volatility. With economic resilience dominant and little signs of meaningful economic slowing (June NFP of 147 K), we think it is too early to position for that development…

…US treasuries, duration: high return volatility = underweight In the context of the broad themes discussed above (fiscal excess, large deficits, resilience, Fed on hold, weak bank demand), we capitulate on last month’s constructive view on UST and duration and recommend an underweight. We acknowledge that bond rally potential remains, although our baseline view is that the 10y yield (4.45%) remains range bound, between 4.25%-4.75% (Exhibit 7). After yet another month of yield whipsaw (high return volatility), we think underweight allocation to duration and quality bonds in UST and muni’s makes most sense. If income alone is the objective, we think money market or floating rate assets continue to look relatively attractive: they provide comparable income potential to long duration exposures and does so without the return volatility. With economic resilience dominant and little signs of meaningful economic slowing (June NFP of 147 K), we think it is too early to position for that development – pretty much the exact same story since 2023.

Forecastsand yields The official BofA economics and rates forecasts can be seen in Exhibit 8 through Exhibit 10. BofA Economics maintains view that there is no recession and the Fed does not cut in 2025.

Exhibit 11 and Exhibit 12 show yields in low yield and high yield sectors over time. High quality bond yields moved higher over the past month, as concerns over fiscal profligacy weighed on UST. Given passage of One Big Beautiful Bill, elevated deficits are expected to persist, creating upward pressure on bond yields…

Next day, this …

18 July 2025 BAML: Global Rates Weekly Musical Chairs

The View: Europe data in focus before Aug tariff deadline Europe in focus next week with the ECB, credit and confidence data. Japan Upper House election another risk event for markets. While in the US, Fed leadership may continue to dominate headlines.

Rates: Fed independence genie US: Fed independence erosion supports our long 10y inflation B/E view Stay paid Dec ’25 FOMC OIS with solid inflation; spread views need WAM help…

…Technicals: Golden cross on SPX favors higher 10Y yield US 30Y yield traded up to 5.07%, a pinch away from our tactical target of +/- 5.08% set on July 7. A golden cross signal for the SPX has tended to favor higher 10Y yield

… We studied macro trends after a golden cross signal on the S&P 500 and found the US 10Y yield tended to rise (price declined). For more, please see: Quantifying Technicals: Macro trends after SPX’s golden cross 14 July 2025

Wimbledon now a fading memory and best I reckon the sponsor bank isn’t out there sponsoring The Open but still, sponsoring all sorts of GREAT economic research …

Resilient US consumer data and robust Q2 earnings for now dominate over initial signs of tariff effects on CPI, continuing threats of tariff escalations and increasing political pressures on the Fed. The focus next week is on Japan's election, flash PMIs, the ECB meeting and more corporate earnings.

…US Outlook Something wild

This week was eventful, with the media reporting an imminent firing of Powell that failed to materialize. In any case, we doubt that such a move would succeed at lowering Treasury yields. With activity looking resilient, and inflation regaining traction, we nudge up our GDP growth in Q2 and Q3

This week's data undermine hopes that the FOMC might contemplate an earlier rate cut. Activity data look resilient, with June estimates of retail sales and industrial production exceeding expectations. Meanwhile, consumer price inflation appears to be emerging from its earlier soft patch, with commodity prices now showing signs of tariff cost-push pressures.

This resilience may be related to a slower realization of tariffs and compositional shifts. After overhauling our estimates using granular trade data, we estimate that the trade-weighted tariff in May was about 9.5%, below our prior assessment of ~13%. In light of this, and momentum from the resilient activity data, we upgrade our GDP growth outlook by 0.5pp in both Q2 and Q3.

Although Waller reiterated his support for a 25bp cut in July, on the grounds that the labor market is showing "some cracks," we do not think this rationale is gaining traction within the voting committee. We retain our view that the FOMC will resume cuts in December, conditional upon the tariff-driven acceleration of consumer prices we expect this autumn.

Pressures on the Fed's independence are intensifying, with a White House official reporting that Chair Powell would soon be fired on the grounds that he had mishandled Board building renovations. The president downplayed this possibility, which would likely be challenged in the courts. We suspect such a move would be counterproductive if the goal is to lower Treasury yields.

Best in the biz (and you’ve another chance to vote, in case you hadn’t heard, the II survey now called something else, is currently accepting ballots) … Anywho’s, they are in 10s30s flatteners, SFRM6/M7 steepeners and lookin to BUY 10y BREAKS (below 240bp) …

In the week ahead, the flow of relevant economic data slows sharply, the highlights being jobless claims and the June Durable Goods release. With these second-tier offerings the only fundamentals on the docket, the US rates market will be reliant on political developments and the price action in other asset classes as Trump's August 1 round of tariffs quickly approaches. The narrow window for new bilateral trade deals is closing, which begs the question: will there be another extension or is the President content to implement the newest levies and respond/adjust accordingly in the event of a sharp market reaction. We’re in the latter camp – Trump’s messaging, combined with the muted response to the looming tariffs seen thus far in the equity market, reinforces this stance. The one nuance that we’ll offer is that while we expect no further tariff delays, we ultimately anticipate that there will be revisions and reductions to the new levies over time as the process of redefining the global trade landscape unfolds.

Given that only two weeks remain before Tariff-Day 2.0, it follows intuitively that there will be headlines from Washington regarding the process, and it wouldn’t be particularly surprising to learn of a few eleventh-hour agreements – even if we anticipate that the vast majority of new levies will be implemented in-line with the recent announcements. Future negotiations will dictate carve-outs, exemptions, and reductions – a reality that will further contribute to our view that the trade negotiations are quickly losing their market relevance. To be fair, the economic ramifications of shifting trade winds are going to be the defining event of the next few months – without question. Our observation is simply confined to the process of ironing out the details and nuances of the new tariff regime. As a result, the market will be reminded that waiting is the hardest part.

Powell’s comments on Tuesday have been cited as a potential market event but given that his appearance is at a regulatory conference and comes during the Fed’s pre-FOMC period of radio silence, there won’t be any monetary policy guidance. The bigger question remains whether Trump will eventually attempt to remove Powell before the end of his term in May 2026. Investors have become accustomed to extreme rhetoric from the President regardless of the topic, which implies a willingness to downplay the threat of an early exit for Powell. At least for the time being. The airtime given to Warsh and others auditioning for Powell’s seat has been on the rise and the establishment of a ‘shadow Fed’ (or at least chair-in-waiting) may soon be in the offing. Frankly, an ‘early’ announcement of Trump’s nominee is a far more benign outcome than attempting to fire Powell.

With this backdrop, we’ll add that the technical landscape is currently at stressed levels. Specifically, stochastics indicate that duration is well into oversold territory – which is consistent with either a retracement lower in yields or, at a minimum, an extended period of consolidation. The dearth of fundamentals in the week ahead will incrementally add to the influence of the technicals. On the supply side, Wednesday’s 20-year auction of $13 bn will be closely scrutinized once again for any indication of the long-feared buyers’ strike that has thus far failed to materialize. We’re anticipating a solid round of sponsorship for supply and see demand concerns as overdone – particularly in light of the remarkably strong performance of Treasury auctions since Liberation Day …

A rather large German bank attempting to call out the tip of the ice berg … you can, as always, see what you wanna see and here are a couple charts which ‘spoke to me’ …

18 July 2025 DB: US Inflation Outlook: Tip of the tariff iceberg

…Median and trimmed mean CPI slightly stronger than core and more in line with our ex-ante expectations

…Recent market rally will boost portfolio management in the near term

Details within the CPI and PPI point to 0.30% core PCE print for June

Progress on core PCE seems to have stalled

Same shop with cursory look at positions and flows, primary source of stock jockey positions out there on the intertubes …

18 July 2025 DB: Investor Positioning and Flows - Trending Higher

Resilient earnings growth suggests room for equity positioning to keep rising. Equity positioning has historically been well aligned with fundamental drivers such as earnings growth. In early April, positioning had collapsed to be in line with a mid-teen drop in earnings but has since recovered and is now in line with mid-single-digit growth, still slightly below our expectation for Q2 at 7.6% yoy (Q2 Earnings: Looking For A Slight Deceleration Amidst Tariff Fog, Jul 07 2025). Looking further out, we as well as the bottom-up consensus see earnings growth dipping only slightly further in the second half, before picking up again into double digits next year. We expect investors to look through any temporary slowing.

Volatility has continued to creep lower with sensitivity to inflation releases near the lowest in 3 years. Implied vols have fallen sharply, not just in equities but across most asset classes, with FX a notable exception. The decline in implied vols largely reflects falling realized volatilities, and in fact are arguably too high relative to them. While inflation continues to remain in focus in the context of tariff impacts, the volatility priced into the S&P 500 vol curve ahead of CPI days has been falling sharply, and for this week’s CPI release was near the lowest in 3 years (The CPI Event Risk Rally, Nov 2022).

If vol stays subdued, systematic strategies will raise equity exposure. Systematic strategies’ equity positioning is currently just above neutral. Vol Control funds have raised exposure significantly and have only a little room to add before reaching historical maximums. CTAs however are moderately long equities and have room to add, especially in small caps where they are still short. Their longs in US large caps are moderate while those in Europe, Japan and EM are elevated. For risk parity funds, positioning fell in all asset classes in early April, especially in equities which saw the largest relative spike in vol. If vol remains at current levels and correlations among asset classes remains subdued, we expect risk parity funds to raise equity exposure.

The pockets of exuberance are growing. A basket of stocks with very high net call volume in the previous week, a good indicator in our view of buying driven by momentum and risk appetite, outperformed sharply again this week. The stocks benefiting are highly volatile and have poor profitability. Meanwhile, crypto funds ($3.4bn) continued their strong run with their largest weekly inflows in 8 months. However, other measures of exuberance remain subdued, with for example, continued outflows from US equities overall, as well from leveraged and single-stock ETFs.

…Positioning is slightly below the level implied by Q2 earnings growth, but we see room for it to rise higher as investors look through any temporary slowing

Mr. Markets forcing mea culpa’s all the time and here’s an updated view …

July 18, 2025 MS: Busted On A Duration Bad Beat, But Buying Back In | US Rates Strategy

Reacting to the initial estimate of core PCE inflation for June, 5y UST yields rose to 4.05% this past week - above our suggested stop level of 4.03%. PPI subsequently brought down our core PCE estimate, and Governor Waller made the case for a July cut. Buy 5y USTs again, keep UST 3s30s steepeners.

Key takeaways

The market prices in more rate cuts this year than our economists think occur in the baseline, but fewer than our economists think occur next year.

With downside risks to growth levered to the outcome of August 1 tariff proposals, we do not suggest fading the market pricing of rate cuts this year.

We suggest positioning portfolios in a way that benefits from the market pricing a lower trough policy rate from the Fed - a trough likely to occur in 2026.

The Fed could deliver a lower-than-currently-priced trough policy rate either because the neutral rate (r*) declines or because it needs accommodative policy.

We continue to suggest holding UST 3s30s yield curve steepeners and term SOFR 1y1y vs. 5y5y steepeners, and suggest buying 5-year US Treasury notes again.

…United States | Waller-Waller Bing Bang …We suggest re-entering a duration long at the 5y point Treasury yields increased over the past few weeks as a result of more than just term premium expansion. The June CPI report catalyzed a rise in market-implied trough rates that lifted yields higher as well. The report caused our economists to revise their projections for core PCE inflation to 35bp M/M from 28bp.

As a result, the Treasury market sold off - bringing 5y Treasury yields 2bp above our suggested stop. The next day, the PPI report caused our economists to revise their June core PCE projection to 27bp - helping Treasury yields fall back. Treasury yields should now incorporate their final forecast of 29bp - close to their initial view.

With Treasury yields back below our suggested stop, we are comfortable suggesting investors buy 5-year notes again. Why choose the 5y maturity?

Looking at curve-spanning 50-50 SOFR swap flies, i.e., wings positioned at the front-end and long-end of the curve, we find the fly with the 5y belly as one of the most related to the level of rates (see Exhibit 5).

Outright carry and rolldown continues to be negative at the 5y point in swaps space, but combining it with other points in a fly can provide relatively attractive C&RD (see Exhibit 6), another possible avenue for a bid and outperformance…

…In addition, the 5y point continues to outperform on the 2s5s30s 50-50 SOFR swap fly (see Exhibit 7). Momentum hints at more outperformance, given a relative strength index (RSI) of 34 and a MACD line below the indicator and zero line (see Exhibit 8).

The key risk to the trade is a surprising rise in core PCE inflation for June - something similar to the 35bp initial forecast revision explained above. In addition, surprising strong labor market data for July and/or surprising high CPI inflation for July pose risks.

…Trade idea: Enter UST 5y at 3.9% with a target of 3.25% and a stop of 4.05%.

…Trade idea: Maintain UST 3s30s yield curve steepener at 1.15% with a target of 2.10% and a trailing stop of 0.90%.

… said another way, if at first you don’t succeed, try try again? (forget that other one about doing the same thing and HOPING for different results … bla bla bla). In ANY case, please don’t forget to get those II (or whatever it’s called) votes in early and often?

Covered wagons consistent and solid although NOT the best in biz, at least not by Global Walls balloting process …

July 18, 2025 Wells Fargo: Weekly Economic & Financial Commentary

United States: Economic Data Clears the Bar, but Doesn’t Raise It The economic data calendar was packed this week. Better-than-expected retail sales, industrial production and home construction suggest activity has regained its footing after a loss of momentum during the first five months of the year. At the same time, data on inflation indicate the costs of tariffs are starting to get passed on to consumers, albeit slowly…

…Interest Rate Watch: Fighting Fire with Fire The potential firing of Chair Powell jolted markets this week. Even if President Trump were to bring in a dovish successor, changes in monetary policy are determined by a voting committee and the long end of the curve is influenced by factors outside the Federal Reserve's purview…

Topic of the Week: Foreign Suppliers Resisting Tariff Pressures If foreign exporters were absorbing the cost of tariffs, U.S. import prices would be declining in proportion to the rise in the tariff rate. Yet, nonfuel import prices, which exclude the cost of tariffs, rose 1.2% year-over-year in June. With little relief on import prices, domestic firms are stomaching the cost of higher tariffs and starting to pass it on to consumers.

… Moving along TO a few other curated links from the intertubes, which I HOPE you’ll find useful …

Wall-E must be right, rates need to come down, labor market is slowing …

July 18, 2025 Apollo: Comparing Wage Growth for Job Stayers and Job Switchers

When the labor market is hot, wage growth for job switchers is higher than wage growth for job stayers, see chart below.

Today, wage growth for job switchers is lower than wage growth for job stayers, suggesting that the labor market is cooling down.

Sources: Federal Reserve Bank of Atlanta, Macrobond, Apollo Chief Economist

… AND the debate ‘bout Wall-E will continue amongst the pundits … some are more smug (Dutta HERE) IMO, while others offer an equally funTERtaining if even OPPOSITE view (Bianco HERE).

Which side or tact do you most closely align yerself with?

I’m thinking more about rate cuts and lower yields for while now thinking about things Ms DiMartino Booth has said / continues to say. Her delivery is different (again, not as smug IMO as, say, Dutta).

Clearly not working out (see MS above — having bot 5s, gotten stopped out, and re bot) but it’s a marathon, not a sprint…

Still waiting for latest from HIMCo and while we wait, cannot think of anyone better to read than this next fella — maybe the up and coming / NEXT Lacy Hunt …

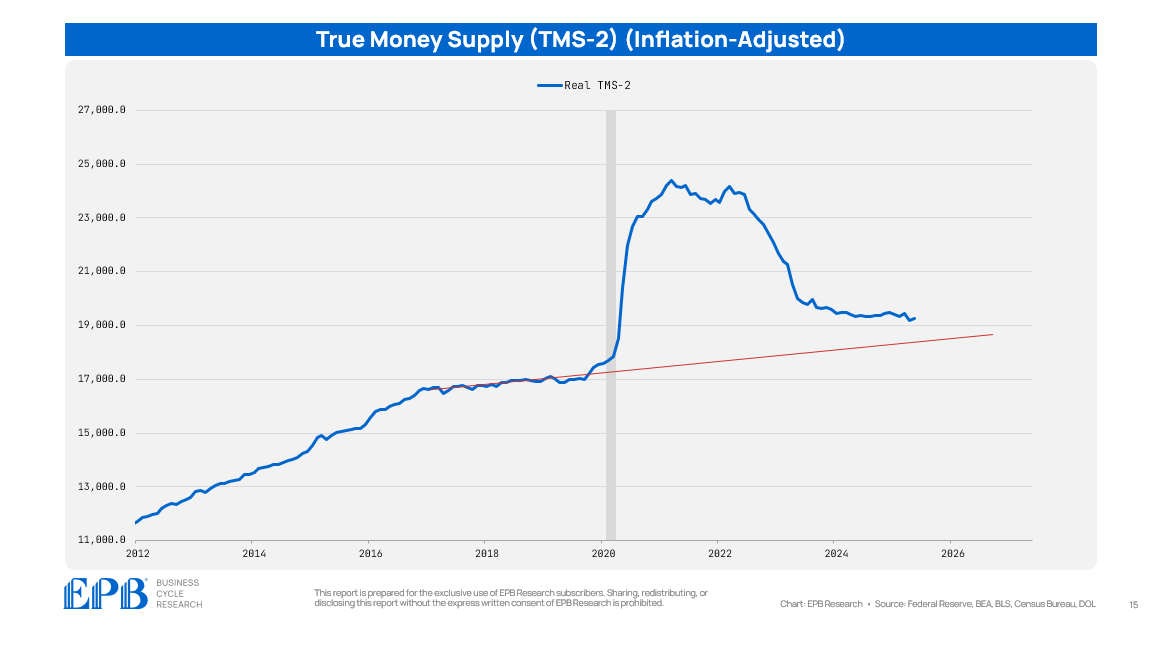

Jul 19, 2025 EPB: Real Money Supply Is Still Contracting — And Housing Is the Next Domino Despite a continued decline in real money, the excess from past stimulus is still buffering the economy, but continued contraction will push tightening effects deeper into the business cycle.

…Real Money Supply Today

The real money supply situation today is more complicated and requires nuance.

In 2017, real money supply growth slowed down - it was still increasing, but at a 1% annualized pace, which is relatively tight. This led to a slowdown in 2019, rate cuts from the Federal Reserve, and a neutral rate that was roughly 2.5%.

The pandemic stimulus efforts pushed real money supply 25% above that 2017-2019 trendline, ushering a boom through the housing and manufacturing sectors, high inflation, and robust economic growth for a short time.

As the Federal Reserve raised interest rates and broadly tightened policy, real money supply started to contract. We can also see that even with the first round of 100bps of rate cuts, real money supply is still declining which tells us monetary policy remains tight enough to prevent increases in real money.

However, the complication with this cycle is that the stimulus from 2020 and 2021 was so great that there is still excess in the system. The current level of real money supply remains above the 2017-2019 trendline.

So while monetary policy is undoubtedly contractionary given the impact on real money supply, the economic impact has been delayed or blunted by the excess that still remains…

… when EPB talks, people listen …

SHORT positions building out the yield curve …

19 JUL 2025 Hedgopia CoT: Peek Into Future Through Futures, How Hedge Funds Are Positioned

10-year note: Currently net short 772.4k, down 68.2k.

The 10-year treasury yield edged up a basis point this week to 4.43 percent, but not before ticking 4.49 percent intraday in each of the three sessions through Thursday. On 1 July, these notes were yielding 4.21 percent.

In the right circumstances for bond bears (on price; yield and price have an inverse relationship), the 10-year would have had a shot at 4.7 percent, which is where a falling trendline from October 2023 when rates peaked at five percent lies.

But for now, odds favor yields are headed lower in the sessions to come. If this comes to pass, the 50- and 200-day lie at 4.41 percent and 4.36 percent respectively; bond bears are likely to try to defend these averages. Failure to do so will make the July low exposed.

30-year bond: Currently net short 130.1k, up 21.4k.

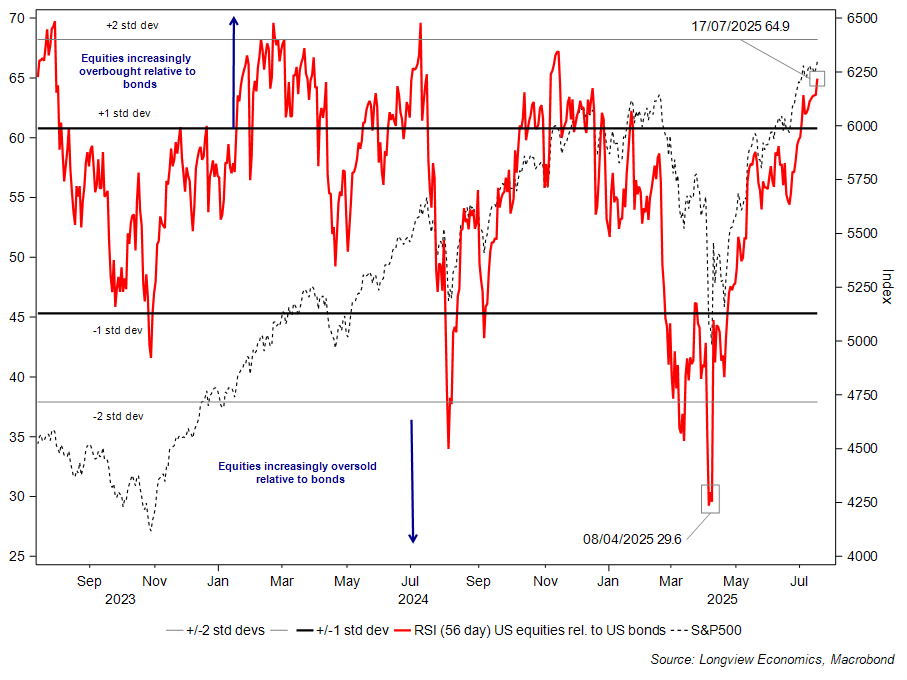

An update from The (Long)View … this one caught MY attention as it details relative strength of stonks vs bonds …

The State of Markets: "Equities Overbought (Relative to Bonds)"

By Thursday’s close key US markets were eking out small gains for the week. The S&P500 was 0.6% higher on the week; the Dow Jones was up by 0.3%; while the NDX100 had fared better (+1.3%). By half way through the session on Friday, those markets were modestly lower (basically flat). US earnings, which began in earnest this week, have been a key factor pushing markets, and single names, higher. Key banks have been mostly beating expectations, along with high profile stocks like Netflix. With that (modest) strength in the S&P500 and NDX100, both markets have (just) broken out to the upside of their recent multi week trading ranges (i.e. from the first half of July).

Equities, though, are notably overbought relative to bonds (see chart below). In recent quarters, that’s been an effective indication that the equity rally is due a ‘breather’ (or indeed ‘some giveback’). The BAML FMS this week appeared to confirm that sense (i.e. ‘the market is due a breather’), reporting that there has been: ‘a record surge in risk appetite in the past 3 months’ (source: BAML FMS, July 2025).

Next week, the US quarterly earnings season continues with a large number of companies reporting. Key features include earnings from Alphabet and Tesla (both Wednesday); an ECB policy meeting (Thursday), which will be preceded by the ECB Bank lending survey (i.e. credit conditions on Tuesday). Elsewhere there’s a housing theme in the US with both existing home sales and new home sales out this week (Wed & Thurs). In the UK, it’ll be all eyes on the public finances data update, due Tuesday (given the concern about a potential UK fiscal crisis). Flash PMIs from across the globe will also be watched closely (on Thursday).

Key Chart: Medium term RSI (equities relative to bonds) vs. S&P500

Lookin’ for an EDGE … a couple visuals from this weekends note caught MY attention and am sharing, hope you find it thought-provoking, too …

…“I Want Someone Provocative and Talkative”: Fed Expectations

As we noted above, the market is expecting the Fed to begin cutting rates in the relatively near future, with the World Interest Rate Probability (WIRP) screen from Bloomberg showing the probabilities of rate cuts at future Fed meetings.

Source: Bloomberg, as of 7-18-25

Notably, these probabilities for imminent rate cuts have been falling in recent weeks as growth and employment data in the U.S. have remained more resilient in the face of tariff uncertainty. Our view has been that this Fed will remain on hold until the labor market data shows greater signs of weakness due to the uncertainty about the future path of inflation in this new tariff regime.

We emphasize this Fed, because of the chorus of calls, led by President Trump, that Powell is keeping interest rates too high and that he should be replaced.

Even as growth forecasts remain healthy, though slightly below trend, as seen in the first chart below, and inflation forecasts have CPI remaining above the Fed’s 2% target through 2026, as seen in the second chart below, the market is pricing in four rate cuts by this time next year, seeing a Powell replacement as likely to deliver on the President’s rate cut desires.

As of 7-18-25

As of 7-18-25

Seen another way, as Ernie Tedeschi pointed out in a Bloomberg Law article this week, based on today’s economic backdrop using the Taylor Rule (a formula to determine where rates should be given growth and inflation), the Fed’s current policy stance does not look too tight and is even below where the Taylor Rule suggests Fed policy should be set.

As of 7-18-25

We can see this from yet another angle of broad financial conditions, which include inputs like equity valuations and credit spreads. Current financial conditions remain in easy/stimulative territory, which suggests that neither the equity nor the credit market is screaming that the Fed needs to cut rates because the economy is at risk of imminent decline. Of course, the stock and credit markets are not perfect discounting mechanisms and have often been complacent near economic peaks (we’re looking at you 2007).

As of 7-18-25

This is not to say that the level of interest rates is not weighing on economic activity in certain areas, with housing being the most prominent victim of high rates (though housing is more driven by long-term rates, which as we argued above are less sensitive to the Fed’s interest rate policy). Further, for smaller businesses that tend to borrow from banks (and increasingly private credit lenders) at a floating rate, today’s high Fed Funds Rate is certainly a burden.

But Trump is not demanding that the Fed needs to cut interest rates because the economy is weak (that would be a dangerous admittance), but instead that cuts need to come in order to relieve funding pressure on the Treasury. This, in combination with Treasury Secretary Bessent’s discussion of focusing Treasury issuance on shorter-term bills, has raised concerns about how a deterioration in Fed independence and regulatory capture increases risk of future inflation, ushers in an era of fiscal dominance, and potentially erodes the attractiveness of U.S. debt across the curve.

As of 7-18-25

These are sticky and complex issues, which we are sure to explore in greater detail in the coming weeks, but for now, let’s explore how the potential loss of Fed independence (Trump gets a new “provocative and talkative” Fed chair/board of governors) could impact the supply and demand dynamics impacting the yield curve…

This next note highlights how it is rates are un-highlight-able … Brent’s one of the good ones and always a good read and so … but … and …

July 18, 2025 Spectra Markets: All The Trump Things Fly Skyward

… And with no visibility on US government plans, the Fed waits and wonders what to do next. Inflation is about to rise as the tariffs finally appear in the data, but real clarity now won’t be achieved until at least the September and October data (released in October and November) because the bulk of the tariffs won’t take effect until August 1. That’s if there are not more flip flops, ofc. No reasonable human being in the market can wait that long, but a central bank can. Each delay in the tariffs delays clarity and forces the Fed to wait longer. Sure, you can argue that tariffs aren’t inflationary, but you’re just guessing. Maybe they are and may they’re not. We’ll see.

Meanwhile, 10-year yields continue to bore.

There’s some vague weakness in the labor market and consumer spending, but Initial Claims are falling back down, inflation is still firm/sticky, and term premium remains necessarily wide as deficits balloon and central bank independence is threatened. That all leads to a tie and yields continue to do pretty much nothing.

One of my clients sent me a cool chart showing the dislocation in treasuries after Liberation Day and how term premium got added and then we went back to the normal correlation between policy and the back end of the bond market. Thanks Chris, cool chart!

This is part of why it’s so hard to trade the bond market right now. There’s all the normal macro stuff, but then there’s the term premium caused by government policy weirdness…

TICS … foreign PRIVATES … those NOT defending a currency and who then can go anywhere that makes sense and provides return ON capital …

Jul 18, 2025 WolfST: The Foreign Investors Who Bought the Recklessly Ballooning US Debt: July 2025 Update US Treasury debt surged by $441 billion since the debt ceiling, to $36.7 trillion. Foreign demand for this stuff is an increasingly important issue.

… But “foreign official” holders, such as central banks and government entities, have trimmed their stash of Treasury securities over the years. And their holdings dipped again in May to $3.90 trillion (blue in the chart below).

Private foreign investors – such as financial firms, companies, bond funds, individuals, etc., in foreign countries – have piled on Treasury securities from record to record. In May, their holdings jumped by $55 billion, and by $815 billion year-over-year, to a record $5.15 trillion (red).

… nothing to see here as far as the lack of faith IN USTs. Sorry. No boycott. Not here. Not yet best I reckon …

… AND for any / all (still)interested in trying to plan your trades and trade your plans in / around FUNduhMENTALs, here are a couple economic calendars and LINKS I used when I was closer to and IN ‘the game’.

First, this from the best in the strategy biz is a LINKthru TO this calendar,

July 18, 2025, 5:56 pm EDT Barrons: Trump Wants to Cut Deficits. Powell-Bashing, Stablecoins, and T-Bills Could Help.

… Tilting Treasury borrowing to the short end is “stealth QE,” according to Dario Perkins, managing director for Global Macro. Quantitative easing describes central bank buying of securities to inject liquidity into the financial system. The idea behind QE is to reduce the supply of long-term government paper available to investors and force them to buy corporate and mortgage debt to stimulate the economy, as former Fed Chair Ben Bernanke explained back in 2010…

… Now comes the crypto connection to all of this. The passage this week of the so-called Genius bill sets standards for stablecoins, which are digital currencies pegged to the dollar or another actual currency. Stablecoins would have to be fully collateralized by safe assets, notably U.S. government debt.

That would boost demand for Treasury bills, Torsten Sløk, Apollo Global Management’s chief economist, wrote recently. He cites a recent Bank for International Settlements paper that estimates that an aggregate $3.5 billion flowing in stablecoins lowers the three-month T-bill rate by 2.5 basis points in 10 days and five basis points in 20 days. (A basis point is a hundredth of a percentage point.)

Circle July 30 on your calendars to see how these disparate forces come together. The Treasury is due to announce its quarterly financing plans that morning, while the Federal Open Market Committee will announce its rate decision that afternoon, followed by Powell’s news conference.

THAT is all for now. Enjoy whatever is left of YOUR weekend …

I don't really understand stable coins....somehow tokens are used as substitutes

for the original asset ???

I don't know....it's a mystery to me..